- Non-food Packaging

- Tube Packaging Market

Tube Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Tube Packaging Market by Material Type (Laminated Tubes, Aluminum Tubes, Others), Packaging Type (Laminated Tubes, Squeeze & Collapsible Tubes, Others), Application, and Regional Analysis for 2026 - 2033

Tube Packaging Market Size and Trends Analysis

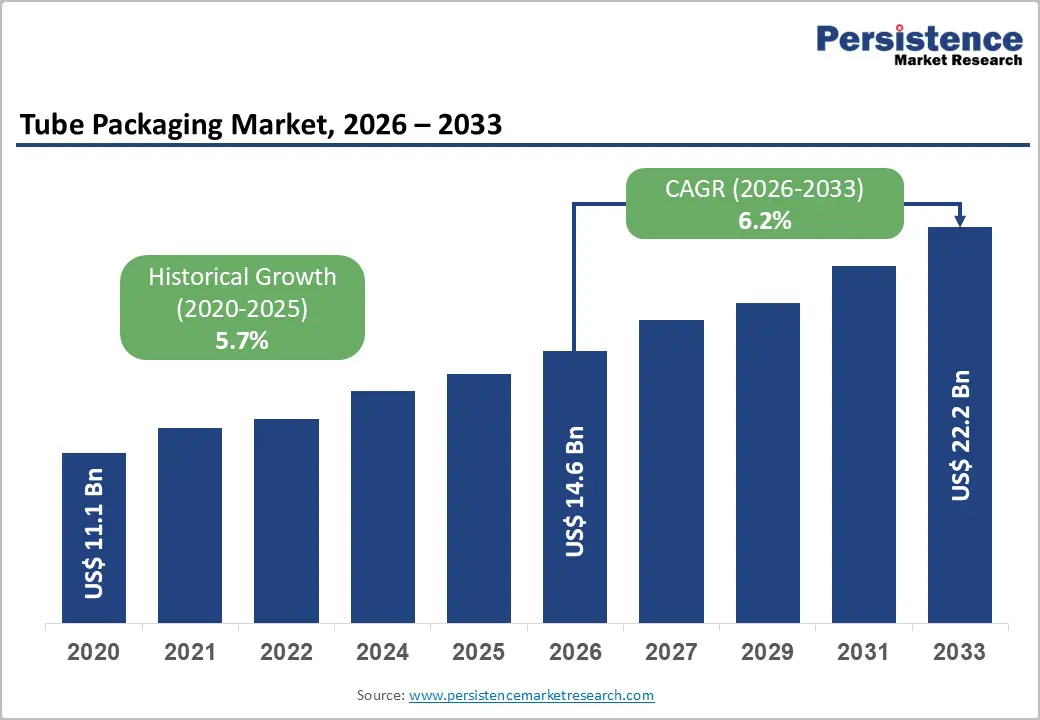

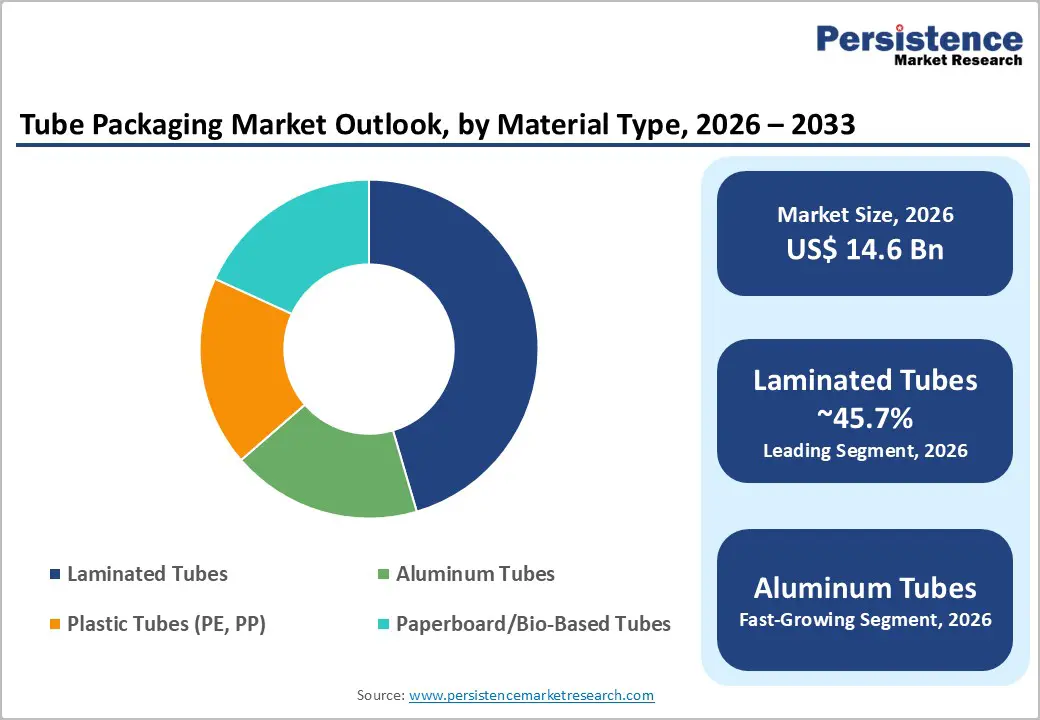

The global tube packaging market size is likely to be valued at US$ 14.6 billion in 2026 and is expected to reach US$22.2 billion by 2033, at a CAGR of 6.2% during the forecast period from 2026 to 2033, driven by the strong demand from cosmetics and personal care applications, rising adoption of tube formats in oral care and pharmaceuticals, and increasing demand for recyclable and sustainable packaging materials.

Laminated tubes and aluminum tubes offer superior barrier protection, extended shelf life, and attractive decoration capabilities, making them widely preferred across consumer industries. Growing e-commerce activity and brand differentiation strategies also favor flexible and durable packaging solutions such as tubes. Increasing manufacturing investments across Asia Pacific and regulatory pressure toward sustainable packaging further accelerate adoption across multiple industries.

Key Industry Highlights:

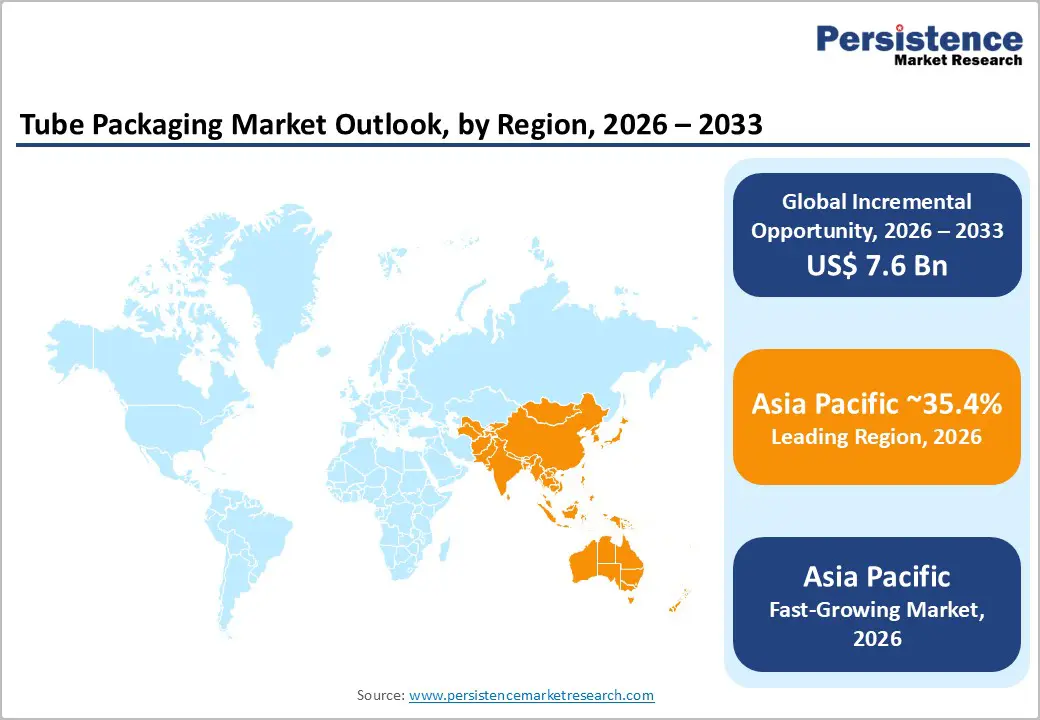

- Leading Region: Asia Pacific is projected to account for approximately 35.4% of the market share, driven by strong manufacturing capacity, expanding consumer goods industries, and increasing demand for cosmetics and personal care products in countries such as China, India, and Japan.

- Fastest-growing Region: Asia Pacific is also the fastest-growing regional market, supported by rapid urbanization, rising disposable incomes, and expanding distribution networks for personal care and pharmaceutical products across emerging economies in Southeast Asia.

- Investment Plans: Major packaging companies, including Amcor, Berry Global, and Albéa Group, are expanding manufacturing capacity and investing in recyclable laminate technologies and advanced barrier materials, particularly in Asia Pacific and North America, to support growing demand for sustainable tube packaging solutions.

- Dominant Material Type: Laminated tubes dominate the material type segment with an anticipated market share of approximately 45.7%, owing to their strong barrier protection, lightweight structure, and compatibility with high-quality printing used in oral care, skincare, and cosmetic packaging.

- Leading Packaging Type: Laminated tubes are estimated to account for 43.9% of the market share, supported by increasing adoption in personal care and cosmetic applications where branding, product protection, and convenience are critical.

| Key Insights | Details |

|---|---|

| Tube Packaging Market Size (2026E) | US$14.6 Bn |

| Market Value Forecast (2033F) | US$22.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Demand from Cosmetics and Personal Care Industry

The cosmetics and personal care sector represents the largest demand base for tube packaging globally. Products such as facial creams, lotions, sunscreen, hair treatments, and makeup primers are commonly packaged in tubes due to their convenience, controlled dispensing, and hygienic usage. The growth of skincare routines and premium cosmetic brands has increased demand for high-quality packaging formats that provide both aesthetic appeal and product protection. Oral care products such as toothpaste and whitening gels also contribute significantly to tube consumption. The expansion of travel-size packaging, sample products, and subscription-based beauty services has further increased the use of small-format tubes. As cosmetic brands compete through packaging design and shelf visibility, laminated and decorated tubes are becoming a key element of product differentiation, strengthening overall market growth.

Sustainability Trends and Material Innovation

Environmental regulations and consumer demand for sustainable packaging solutions are accelerating innovation in tube materials. Packaging manufacturers are increasingly developing mono-material laminated tubes, recyclable aluminum tubes, and bio-based materials that reduce environmental impact while maintaining functional performance. Recyclable packaging initiatives by major consumer goods companies have encouraged converters to invest in new manufacturing technologies and material science innovations. Mono-material laminates are gaining attention because they improve recyclability while maintaining barrier protection against oxygen and moisture. Highly recyclable aluminum tubes are also gaining popularity in premium cosmetic and pharmaceutical applications. As sustainability commitments become central to corporate strategies, the adoption of environmentally responsible tube packaging solutions continues to rise.

Growing Pharmaceutical and Healthcare Packaging Needs

The pharmaceutical sector increasingly uses tubes for packaging topical medications, dermatological treatments, and specialty creams. Tubes offer precise dosage control, protect formulations from contamination, and extend product shelf life. These characteristics make them particularly suitable for over-the-counter treatments and prescription medications. Regulatory requirements for tamper-evident packaging and sterile handling are also driving innovation in tube closures and barrier technologies. Advanced dispensing systems, multi-layer barriers, and specialized caps allow pharmaceutical manufacturers to maintain product stability and safety. The continued expansion of healthcare services and pharmaceutical manufacturing globally is expected to support consistent demand for tube packaging solutions.

Barrier Analysis - Raw Material Price Volatility

The tube packaging industry depends heavily on raw materials such as polyethylene, polypropylene, and aluminum. These materials are closely linked to global commodity prices, particularly crude oil and metal markets. Fluctuations in raw material costs can significantly affect production expenses and profit margins for packaging manufacturers. Converters often operate under long-term contracts with consumer brands, which may limit their ability to immediately adjust pricing. As a result, sudden increases in polymer or aluminum prices can place pressure on profitability. Raw material volatility can also influence procurement strategies and delay investment decisions in new packaging technologies.

Technical Complexity in Developing Recyclable Tubes

Developing recyclable tube packaging while maintaining barrier protection and visual quality remains a technical challenge. Traditional laminated tubes use multiple material layers to achieve the necessary functional performance. Transitioning to mono-material constructions requires new engineering solutions and significant equipment modifications. Manufacturers must also conduct extensive testing to ensure compatibility with existing filling lines and recycling infrastructure. These technical and financial challenges can slow adoption among small and mid-sized packaging companies, creating barriers to widespread implementation.

Opportunity Analysis - Expansion in Emerging Markets

Emerging economies across Asia, Latin America, and parts of Africa are experiencing rapid growth in consumer goods consumption. Rising disposable incomes, urbanization, and expanding retail networks are driving demand for packaged cosmetics, personal care products, and healthcare items. Local brands in these regions are increasingly adopting advanced packaging formats to compete with international brands. Tube packaging manufacturers can capitalize on this trend by establishing regional production facilities and forming partnerships with local consumer goods companies.

Advanced Dispensing Technologies and Smart Packaging

Innovations in dispensing technologies provide significant opportunities for packaging manufacturers. Airless tubes, precision applicators, and advanced closures improve product usability and minimize waste. These features are particularly attractive in premium skincare and pharmaceutical products. Smart packaging solutions such as tamper-evident closures and enhanced barrier technologies also help brands comply with regulatory requirements while improving consumer confidence. Companies investing in research and development of advanced tube systems can capture higher margins and strengthen relationships with global consumer brands.

Development of Bio-Based and Paperboard Tubes

Growing environmental awareness is encouraging the development of alternative tube materials such as paperboard and bio-based polymers. These materials offer a lower environmental footprint compared with conventional plastics and can help companies meet sustainability goals. Although such materials are currently limited to specific applications, including dry products and powders, continuous innovation may expand their usability. Retailers and consumer brands seeking environmentally responsible packaging solutions represent a promising market segment for these emerging technologies.

Category-wise Analysis

Material Type Insights

Laminated tubes are anticipated to hold the largest share of the tube packaging market, accounting for more than 45.7% of the market share in 2026. These tubes combine multiple layers of polymer films and barrier materials to deliver excellent protection against moisture, oxygen, and contamination. Their multi-layer structure also supports high-quality graphics and decorative finishes, which are essential for cosmetic and personal care packaging where branding and product presentation strongly influence consumer purchasing behavior. The versatility of laminated tubes makes them suitable for a wide range of applications, including oral care products, skincare creams, pharmaceuticals, and specialty cosmetics.

For example, toothpaste brands such as those produced by major global consumer goods companies commonly use laminated tubes because they offer flexibility, durability, and efficient product dispensing. Similarly, skincare brands frequently use laminated tubes for moisturizers, facial cleansers, and sunscreen formulations. Manufacturers favor laminated tubes because they balance functional performance, cost efficiency, and visual appeal. Advanced printing technologies, including digital printing and high-definition flexography, allow brands to create highly customized packaging designs that strengthen brand recognition and shelf impact in competitive retail environments.

Aluminum tubes are anticipated to be the fastest-growing material segment. Aluminum provides superior barrier protection against light, air, and moisture, making it particularly suitable for sensitive formulations that require extended shelf life and protection from oxidation. The material is also widely recognized for its recyclability and durability, aligning with global sustainability initiatives aimed at reducing plastic waste. Premium cosmetics and pharmaceutical companies increasingly adopt aluminum tubes to enhance product quality perception and ensure optimal preservation of active ingredients.

For instance, dermatological creams, medicinal ointments, and pharmaceutical gels often use aluminum tubes because they prevent contamination and maintain formulation stability. Luxury skincare brands also favor aluminum packaging for products such as eye creams and specialty treatments, as it conveys a premium appearance and provides enhanced protection. The continued growth of high-end skincare products, medicinal ointments, and specialty cosmetics is expected to contribute significantly to the rising demand for aluminum tube packaging solutions.

Packaging Type Insights

Laminated tubes are anticipated to dominate with around 43.9% market share in 2026 and are also expected to remain the fastest-growing category. Their widespread adoption stems from their lightweight structure, flexibility, and ability to accommodate advanced printing and decoration techniques that improve product visibility on retail shelves. These tubes are widely used in personal care and oral care products where product appearance and convenience play a critical role in consumer purchasing decisions.

Toothpaste packaging is one of the most common applications of laminated tubes, with many global oral care brands relying on laminated constructions for their durability and barrier performance. In addition, cosmetic products such as facial cleansers, hair styling gels, and hand creams frequently use laminated tubes due to their ability to support high-quality branding elements and vibrant product labeling. The compatibility of laminated tubes with automated, high-speed filling lines also makes them a cost-effective choice for large-scale production and global distribution.

Regional Insights

North America Tube Packaging Market Trends - Premium Cosmetic Packaging Innovation and Recyclable Tube Development

North America represents a mature yet technologically advanced market for tube packaging. High consumer spending on personal care products and well-established retail networks contribute to consistent demand across the region. The U.S. leads the regional market, supported by a large cosmetics industry and strong pharmaceutical manufacturing capabilities. Major consumer goods companies such as Procter & Gamble, Colgate-Palmolive Company, and Johnson & Johnson continue to rely heavily on tube-based packaging formats for products such as toothpaste, medicated creams, and skincare formulations.

For example, oral care brands under Colgate-Palmolive use laminated tube packaging to support high-volume toothpaste production, reinforcing the demand for advanced laminated structures in the region. Premium packaging designs and advanced dispensing systems are widely adopted in North America. Consumer brands frequently invest in packaging innovation to differentiate their products in highly competitive retail environments. For instance, Estée Lauder Companies and L'Oréal Group have increasingly adopted decorative laminated tubes and aluminum tubes for premium skincare products. Packaging manufacturers such as Berry Global and Albéa Group have introduced advanced decoration technologies, including digital printing and metallized tube finishes, to support luxury cosmetic packaging. These innovations enhance shelf visibility and enable brands to create distinctive packaging designs that improve consumer engagement.

Regulatory frameworks in the U.S. and Canada emphasize product safety, labeling compliance, and packaging sustainability. Environmental initiatives introduced by organizations such as the U.S. Environmental Protection Agency encourage manufacturers to adopt recyclable materials and reduce packaging waste. Extended producer responsibility programs and recycling targets in several U.S. states have accelerated the development of recyclable tube formats. In response, packaging companies such as Amcor have launched recyclable laminate tube structures designed to replace traditional multi-material tubes that are difficult to recycle. Investment activity in North America also includes the modernization of manufacturing facilities and the development of new barrier materials.

For example, Albéa has expanded production capacity for recyclable laminate tubes in North America to meet rising demand from personal care and oral care brands. Packaging companies are increasingly partnering with consumer goods manufacturers to develop customized tube packaging solutions with improved barrier properties, lightweight structures, and enhanced sustainability performance.

Europe Tube Packaging Market Trends - Sustainability Regulations and Demand for Recyclable Aluminum and PE Tubes

Europe is one of the most advanced regions in terms of sustainable packaging regulations and technological innovation. Countries such as Germany, the U.K., France, and Spain represent major markets for tube packaging. The region benefits from a strong cosmetics and pharmaceutical industry, with global brands such as Unilever, Beiersdorf, and L'Oréal Group driving demand for high-quality tube packaging formats across skincare, oral care, and medicinal product segments.

European consumers place strong emphasis on environmentally responsible packaging, which encourages manufacturers to invest in recyclable materials and eco-friendly designs. Aluminum tubes and mono-material laminated tubes are gaining popularity due to their improved recyclability and environmental performance. Packaging companies such as Hoffmann Neopac and Albéa Group have introduced fully recyclable polyethylene laminate tubes designed to meet the region’s sustainability standards. These developments support the transition toward circular packaging solutions in Europe’s cosmetics and personal care markets. The region’s well-developed cosmetics industry also contributes significantly to demand for decorative and premium packaging formats.

Luxury beauty brands in France and Italy frequently use high-quality aluminum tubes and sophisticated printing techniques to enhance product presentation. For example, premium skincare lines from L’Oréal and dermatological products from Beiersdorf often utilize aluminum or laminated tubes with advanced decoration techniques such as hot stamping, embossing, and high-resolution digital printing. These packaging formats support brand positioning in the premium cosmetics segment while ensuring product protection.

Government regulations addressing packaging waste and recycling targets continue to shape market development across Europe. Policies implemented under the European Union Circular Economy Action Plan and packaging waste directives encourage companies to adopt recyclable packaging materials and improve waste management systems. As a result, packaging manufacturers are investing in innovative materials and manufacturing technologies to comply with environmental standards while maintaining functional performance and product safety.

Asia Pacific Tube Packaging Market Trends - Expanding Cosmetics and Consumer Goods Manufacturing Driving Tube Demand

Asia Pacific is projected to hold the largest regional share of approximately 35.4% and is also the fastest-growing market for tube packaging. Rapid industrialization, population growth, and expanding middle-class consumer bases are driving demand across multiple product categories, including cosmetics, pharmaceuticals, and packaged food products. Strong manufacturing capabilities and cost advantages have also made the region a global hub for packaging production. China, India, Japan, and Southeast Asian countries represent major demand centers. China’s large manufacturing base and expanding cosmetics industry create strong demand for laminated tubes and flexible packaging solutions.

Domestic beauty brands and international companies such as L'Oréal Group and Estée Lauder Companies continue expanding their presence in China, increasing the demand for high-quality tube packaging formats. Packaging suppliers, including Albéa Group, have expanded manufacturing facilities in China to support the growing personal care and oral care sectors.

Japan, known for its advanced pharmaceutical and cosmetic industries, utilizes high-quality aluminum and specialty tubes for precision packaging applications. Japanese companies emphasize packaging innovation and product quality, particularly for skincare and pharmaceutical products. Premium cosmetic brands in Japan frequently adopt aluminum tubes or high-barrier laminate tubes to preserve sensitive formulations and maintain product integrity. India and Southeast Asia are experiencing strong growth in consumer goods consumption due to urbanization and rising disposable incomes.

Companies such as Hindustan Unilever Limited and Dabur India Ltd widely use tube packaging for oral care products, herbal creams, and personal care items distributed across expanding retail and e-commerce networks. Demand for cost-effective laminated tubes is particularly strong in these markets due to their affordability and scalability for large-volume production.

Investment in new manufacturing facilities and technology upgrades remains strong across Asia Pacific. Global packaging companies, including Amcor and Berry Global, continue expanding regional production capabilities through new plants, capacity expansions, and joint ventures. These investments strengthen regional supply chains and enable packaging manufacturers to meet the rapidly growing demand from consumer goods companies across emerging Asian markets.

Competitive Landscape

The global tube packaging market features a mix of multinational packaging corporations and regional specialty manufacturers. Large global companies dominate high-volume production and serve major consumer goods brands, while regional companies focus on customized solutions for local markets. The top ten manufacturers account for a significant portion of premium tube packaging production, particularly in cosmetics and pharmaceutical applications. Smaller players continue to operate in niche markets, offering specialized materials, decorative capabilities, or local distribution advantages.

Competition is driven by technological capabilities, sustainability initiatives, and the ability to deliver integrated packaging solutions that combine tubes, closures, and decoration. Leading companies focus on sustainability innovation, material efficiency, and geographic expansion. Investments in recyclable materials, advanced dispensing technologies, and integrated packaging systems allow companies to differentiate their offerings and strengthen long-term partnerships with global consumer brands.

Key Industry Developments:

- In April 2025, Amcor secured a commercial order for its AmSky™ HDPE blister packaging system, which eliminates PVC and offers a recyclable solution for healthcare products. The packaging was launched with a chewing gum product distributed across major U.S. retailers, demonstrating the growing demand for recyclable pharmaceutical and consumer packaging solutions.

- In May 2025, Amcor partnered with Metsä Group to develop fiber-based molded packaging solutions with high-barrier liners, combining wood-based materials with advanced packaging technology to create more sustainable packaging for food and consumer goods applications.

Companies Covered in Tube Packaging Market

- Amcor

- Albéa Group

- Berry Global

- EPL Limited

- Hoffmann Neopac

- Montebello Packaging

- CCL Industries

- Huhtamaki

- Linhardt GmbH & Co. KG

- Unette Corporation

- Tubex Holding GmbH

- Sonoco Products Company

- IntraPac International Corporation

- Scandolara S.p.A.

- CLTpack

- Toyo Seikan Group Holdings

Frequently Asked Questions

The tube packaging market is estimated to be valued at US$14.6 billion in 2026.

The global tube packaging market is projected to reach US$22.2 billion by 2033.

Major trends shaping the market include the growing adoption of recyclable and mono-material laminated tubes, increasing demand for aluminum tubes in premium cosmetic and pharmaceutical applications, and technological advancements in printing and decorative packaging solutions.

Laminated tubes represent the leading material and packaging segment, accounting for more than 45.7% of the market share, due to their superior barrier properties, cost efficiency, and compatibility with high-quality printing used in oral care, cosmetics, and skincare packaging.

The tube packaging market is expected to grow at a CAGR of 6.2% between 2026 and 2033.

Some of the leading companies in the market include Amcor, Albéa Group, Berry Global, Hoffmann Neopac, and Huhtamaki.