- Sporting Goods & Equipment

- String Instruments Market

String Instruments Market Size, Share, and Growth Forecast 2026 - 2033

String Instruments Market by Product Type (Guitar, Violin, Cello, Others), End-User (Professional, Amateurs), Distribution Channel (Specialty Stores, Online Retail, Others), and Regional Analysis for 2026 - 2033

String Instruments Market Size and Trend Analysis

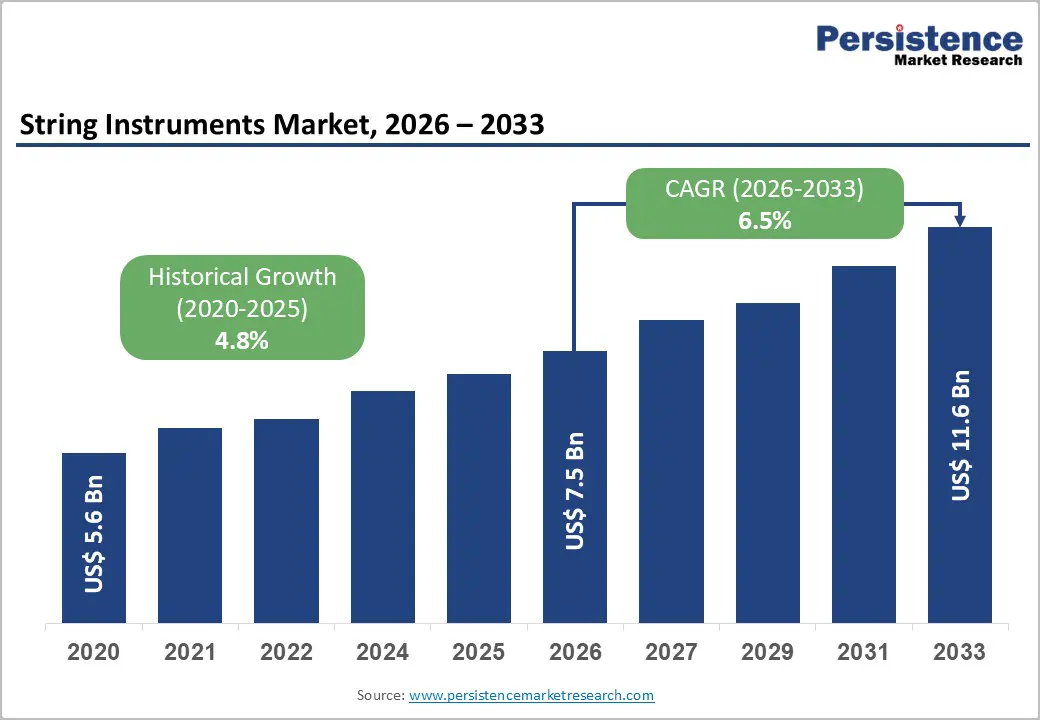

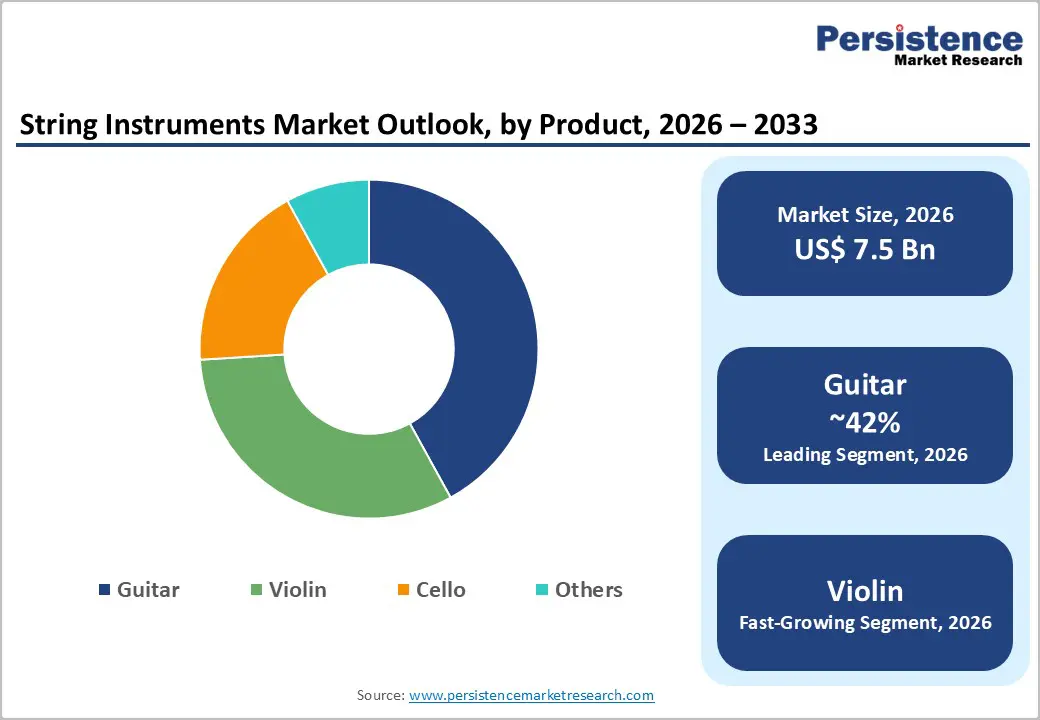

The global string instruments market size is valued at US$ 7.5 billion in 2026 and is projected to reach US$ 11.6 billion by 2033, growing at a CAGR of 6.5% between 2026 and 2033.

The market expansion is primarily driven by the surge in global music engagement, rising adoption of music education programs, and the proliferation of digital and social media platforms that inspire amateur and professional musicians alike. According to the International Federation of the Phonographic Industry (IFPI)'s Engaging with Music 2023 reports study of over 43,000 respondents across 26 countries 71% of respondents consider music important to their mental health, and 78% use it to relax and cope with stress.

Key Market Highlights:

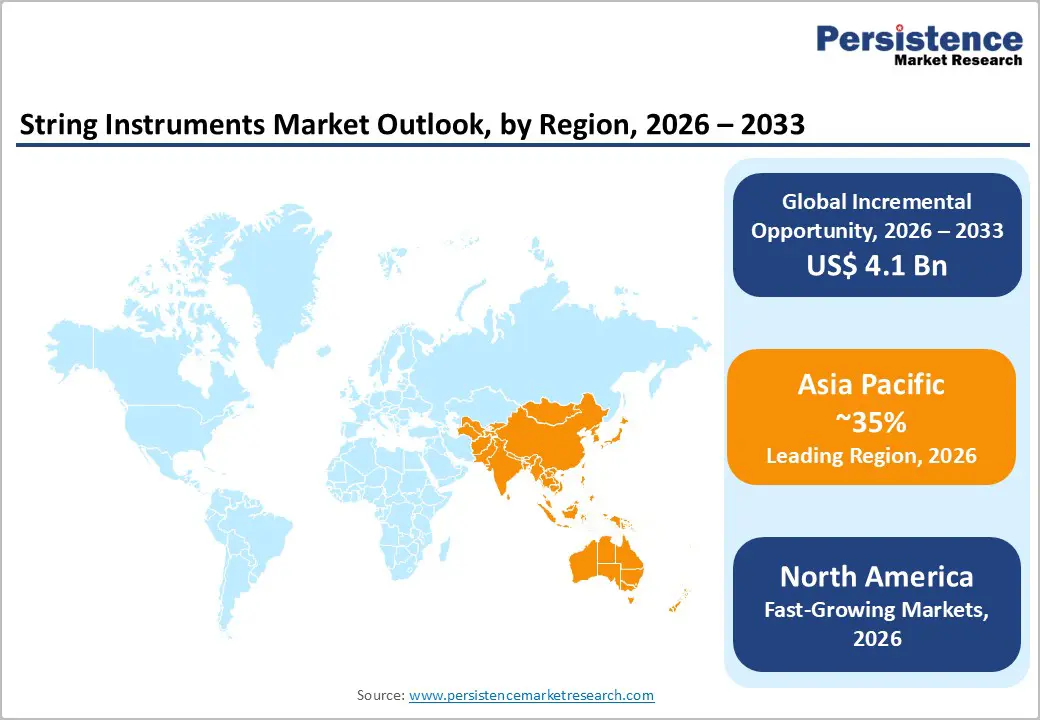

- Leading Region: Asia Pacific dominates the global string instruments market, fueled by large-scale manufacturing in China and India, rising youth interest in music, expanding middle-class income, and strong government support for music education programs.

- Fastest Growing Region: North America remains the second-largest market for string instruments globally, anchored by the United States's deeply embedded musical heritage spanning rock, jazz, country, classical, and folk genres.

- Dominant Segment: Guitars lead the product type category with approximately 42% revenue share, supported by strong cultural affinity, social media influence, wide genre applicability, and continuous new model launches from Fender and Gibson.

- Fastest Growing Segment: The amateur end-user segment is the fastest growing, propelled by online learning platforms, affordable entry-level instruments, and a growing hobbyist culture among younger demographics globally, especially in emerging economies.

- Key Market Opportunity: Integration of smart technology and digital connectivity into string instruments represents the most significant market opportunity, enabling manufacturers to capture the growing cohort of tech-savvy, app-guided learners and hybrid music creators.

| Key Insights | Details |

|---|---|

| String Instruments Market Size (2026E) | US$ 7.5 Billion |

| Market Value Forecast (2033F) | US$ 11.6 Billion |

| Projected Growth CAGR (2026 - 2033) | 6.5% |

| Historical Market Growth (2020 - 2025) | 4.8% |

DRO Analysis

Drivers - Rising Music Engagement and Expanding Music Education Programs

The growing cultural and wellness-oriented significance of music is one of the most powerful drivers propelling string instrument demand worldwide. The IFPI's landmark global study reveals that average weekly music listening time rose to 20.7 hours in 2023, up from 20.1 hours in 2022, reflecting a deepening public engagement with music across age groups. Simultaneously, governments and private institutions have been expanding formal music education initiatives.

Countries such as the United Kingdom have enacted structured program for instance, in October 2025, Communities Minister Gordon Lyons announced 134 grants to individuals, bands, and groups across Northern Ireland under the 2025/26 Musical Instruments Programme. Such initiatives increase the pool of active learners and sustain demand for entry-level and intermediate string instruments, particularly guitars and violins, across developed and emerging economies alike.

Influence of Digital Platforms and Social Media on Instrument Adoption

The explosive rise of digital platforms, particularly short-form video platforms like TikTok and YouTube, has transformed how consumers discover, learn, and engage with music. According to the IFPI Engaging with Music 2023 report, among 16-24-year-olds, short-form video is the single most popular way to engage with music daily, with 82% of surveyed youth accessing music through such platforms.

This viral exposure has significantly lowered the psychological barrier to picking up string instruments, especially guitars. Moreover, e-commerce expansion has made instruments more accessible globally; in 2024, global e-commerce sales for instruments exceeded 60 million units, representing a 17% increase in online adoption compared to 2022. This convergence of digital influence and improved retail access positions the string instruments market for accelerated growth through the forecast period.

Restraints - High Cost of Premium Instruments Limiting Affordability

A significant barrier to broader market penetration is the prohibitive pricing of high-quality string instruments. Premium violins, cellos, and guitars commonly retail from several hundred to thousands of U.S. dollars, making them inaccessible for beginners and budget-sensitive consumers in developing economies. In recent years, tariff volatility and raw material cost escalation, particularly for tone woods such as spruce and rosewood, have further inflated retail prices.

The scarcity of certain regulated tone woods under CITES (Convention on International Trade in Endangered Species) regulations has added additional cost pressure on instrument manufacturers. This pricing constraint risks excluding a large segment of prospective musicians, especially in lower-income economies across South Asia and Sub-Saharan Africa, from entering the market.

Supply Chain Disruptions and Raw Material Availability

The string instruments manufacturing sector remains vulnerable to global supply chain disruptions and raw material sourcing challenges. Tonewood availability, which is central to acoustic instrument quality, has faced increasing scrutiny due to environmental regulations and sustainable sourcing requirements. Additionally, geopolitical tensions and logistical bottlenecks, particularly those experienced post-pandemic, have led to inconsistent component availability and extended delivery timelines.

Counterfeit instruments have also emerged as a growing concern; for instance, U.S. Customs officers seized approximately 3,000 fake Gibson guitars in 2024 alone, reflecting the scale of intellectual property infringement that legitimate market players must contend with. These structural vulnerabilities continue to exert downward pressure on production efficiency and market growth.

Opportunities - Online Learning Platforms and Amateur Segment Expansion

The rapid proliferation of online music education platforms represents a transformative opportunity for the string instruments market. As of 2024, 65% of new music learners began their journey through online platforms, democratizing music education and significantly expanding the addressable consumer base. Platforms such as Fender Play and Yousician have enrolled millions of users globally, directly catalysing entry-level guitar and violin sales.

Additionally, over 25% of young musicians aged 15-25 now prefer connected instruments that interface with mobile applications for guided learning. This trend creates a significant opportunity for instrument manufacturers to develop affordable, app-compatible entry-level product lines targeting the growing amateur segment, which is expected to register the fastest revenue growth among end-user categories through 2033.

Technological Innovation: Smart Instruments and Hybrid Product Development

The integration of digital technology into string instrument manufacturing opens a high-growth avenue for market participants. Smart guitars and violins equipped with built-in tuners, Bluetooth connectivity, and embedded sensors are gaining traction among both amateur learners and professional musicians seeking enhanced functionality. According to industry data, approximately 45% of musicians now use smart instruments integrated with mobile applications for recording, tuning, and sound customization.

The development of AI-driven sound modelling systems capable of simulating tones from over 1,000 traditional instruments enables cost-efficient production and personalized sound experiences. Companies that invest in hybrid acoustic-digital product pipelines can differentiate themselves significantly. In 2025, over 150 digital instrument models with embedded connectivity and app synchronization features were introduced between 2023 and 2025, underscoring a clear technological trajectory that market leaders should strategically exploit.

Category-wise Analysis

Product Type Insights

Among all product types, the guitar segment holds the dominant position in the global string instruments market, accounting for approximately 42% of total market revenue. This leadership stems from the guitar's unparalleled cultural ubiquity across diverse music genres including rock, pop, country, jazz, and folk combined with its relative affordability and ease of initial learning.

The segment benefits from sustained demand across both professional and amateur end-users, with major brands such as Fender Musical Instruments Corporation and Gibson Brands, Inc. continuously launching new models that attract fresh market entrants. The rise of electric guitar popularity on social media, particularly through TikTok and YouTube, has further amplified demand.

End-user Insights

The professional end-user segment commands the largest revenue share in the string instruments market, estimated at approximately 55% of total market revenue. Professional musicians, orchestras, recording studios, and music academies consistently demand premium-grade instruments that deliver superior tonal quality, durability, and playability. The professional segment's dominance is reinforced by the stable procurement cycles of institutions and touring artists, who require instrument replacement and upgrades on a regular basis.

Instruments at this tier such as hand-crafted violins and custom-shop guitars from C.F. Martin & Co., Inc. and Karl Hofner GmbH & Co. KG command significant price premiums, elevating revenue contribution disproportionately to unit volume. However, the amateur segment is projected to record the fastest CAGR through 2033, driven by hobbyist growth, online tutorial accessibility, and a broadening base of first-time learners globally.

Distribution Channel Insights

The specialty stores segment leads the string instruments market distribution landscape, accounting for roughly 48% of total revenue. Specialty music retail stores retain their dominance because they offer a combination of expert guidance, hands-on instrument testing, and personalized services that are critical to most purchasing decisions, particularly for professional and intermediate players.

The experiential nature of instrument purchase, where tonal resonance, neck feel, and acoustics matter, ensures continued footfall in physical retail environments. However, online retail is emerging as the fastest-growing distribution channel, propelled by the convenience of e-commerce, competitive pricing, detailed product video reviews, and improved logistics. Global e-commerce instrument sales rose 17% between 2022 and 2024.

Regional Analysis

North America String Instruments Market Trends

North America remains the second-largest market for string instruments globally, anchored by the United States's deeply embedded musical heritage spanning rock, jazz, country, classical, and folk genres. The U.S. is home to the headquarters of iconic global brands including Fender Musical Instruments Corporation, Gibson Brands, Inc., and C.F. Martin & Co., Inc., which sustains a robust innovation ecosystem and drives premium product demand. The country hosts a large network of music educational institutes, specialized retailers, and live entertainment venues that ensure persistent instrument demand.

A notable milestone in 2026 is Fender Musical Instruments Corporation's celebration of the 75th Anniversary of the Telecaster, accompanied by a five-model commemorative collection that underscores the region's commitment to instrument heritage and innovation.

Europe String Instruments Market Trends

Europe occupies a distinguished position in the global string instruments market, supported by centuries of classical music tradition and a well-developed institutional framework for music education. Germany, Italy, France, Spain, and the United Kingdom collectively account for most European market revenue. The region hosts over 500 specialized luthier workshops and 50 major manufacturing facilities dedicated to classical and orchestral instruments. Europe's approximately 12 million students enrolled in structured music education programs provide a consistent demand pipeline for entry-level and intermediate string instruments.

Government-backed music programs further reinforce regional demand. In the United Kingdom, the 2025/26 Musical Instruments Programme distributed 134 grants to musicians and groups across Northern Ireland. European regulatory harmonization around sustainable instrument manufacturing particularly regarding tone wood sourcing under EU environmental frameworks is also shaping production practices.

Asia Pacific String Instruments Market Trends

Asia Pacific is the dominant region in the global string instruments market, driven by manufacturing prowess, rising consumer incomes, and expanding youth interest in music. China and India serve as the primary manufacturing hubs, offering cost-competitive production supported by abundant raw materials and government incentives. In January 2024, China implemented updated regulations for musical instruments mandating stricter product quality standards and testing for imported and domestically manufactured instruments demonstrating the government's commitment to elevating industry standards.

India's rising disposable incomes, widespread smartphone adoption, and growing enthusiasm for Western music genres offer fertile ground for app-linked and entry-level string instruments. South Korea and ASEAN economies further contribute to regional growth through government-supported music education programs.

Competitive Landscape

The global string instruments market exhibits a moderately consolidated structure, with a handful of established multinational brands namely Yamaha Corporation, Fender Musical Instruments Corporation, and Gibson Brands, Inc. Commanding significant market presence alongside numerous regional and boutique manufacturers. Yamaha leads through unparalleled product diversification and a global distribution network.

Key competitive strategies include celebrity artist endorsements, limited-edition model launches, digital integration, and sustainable sourcing initiatives. Emerging trends include direct-to-consumer digital storefronts, AI-guided instrument customization tools, and collaborations with music technology platforms.

Key Developments:

- October 2024: Fender Musical Instruments Corporation announced the launch of Jaguar Bass, an electric bass guitar that combines elements from both the Fender Jazz Bass and Precision Bass, while retaining a distinctive design reminiscent of the original Fender Jaguar guitar. It has a C-shaped maple neck, typically with a 7.25"-radius rosewood fretboard that includes aged pearloid block inlays, a premium touch not commonly found on standard models.

- July 2024: Yamaha Corporation, launched the Back to School Music Sweepstakes to encourage musicians to play musical instruments and audio devices according to their music genre needs.

Companies Covered in String Instruments Market

- Yamaha Corporation

- Fender Musical Instruments Corporation

- Gibson Brands, Inc.

- C.F. Martin & Co., Inc.

- Roland Corporation

- Samick Musical Instruments Co., Ltd.

- Godin Guitars

- Schecter Guitar Research

- Karl Hofner GmbH & Co. KG

- Ibanez

Frequently Asked Questions

The global string instruments market is valued at US$ 7.5 Billion in 2026 and is projected to reach US$ 11.7 Billion by 2033, expanding at a CAGR of 6.5% during the 2026 - 2033 forecast period.

The primary growth drivers include rising global music engagement with average weekly listening time reaching 20.7 hours per person as per IFPI's 2023 study expanding music education programs backed by government initiatives, the viral influence of social media platforms such as TikTok and YouTube, and the growing adoption of online learning platforms that are democratizing music learning and driving entry-level instrument purchases globally.

The guitar segment dominates the string instruments market, accounting for approximately 42% of total revenue. Its leadership is attributed to cultural ubiquity across multiple music genres, strong brand investments by Fender and Gibson, and the segment's accessibility across both professional and amateur user groups. Guitars sold approximately 6.5 million units globally in 2024, underscoring their dominant position.

Asia Pacific is the leading regional market for string instruments, driven by the large-scale manufacturing ecosystems in China and India, innovation leadership from Japan (home to Yamaha Corporation and Roland Corporation), rising disposable incomes, government-backed music education programs, and the growing influence of Western music genres among youth populations across South Korea and ASEAN countries.

The major companies operating in the global string instruments market include Yamaha Corporation, Fender Musical Instruments Corporation, Gibson Brands, Inc., C.F. Martin & Co., Inc., Roland Corporation, Samick Musical Instruments Co., Ltd., Godin Guitars, Schecter Guitar Research, Karl Hofner GmbH & Co. KG, and Ibanez (Hoshino Gakki Co., Ltd.), among others.