- Construction & Engineering

- Steel Sections Market

Steel Sections Market Size, Share, and Growth Forecast, 2026 - 2033

Steel Sections Market by Product Type (Hot-Rolled Steel Sections, Cold-Formed Steel Sections, Others), Application (Construction, Renewable Energy, Others), Section Shape, and Regional Analysis for 2026 - 2033

Steel Sections Market Size and Trends Analysis

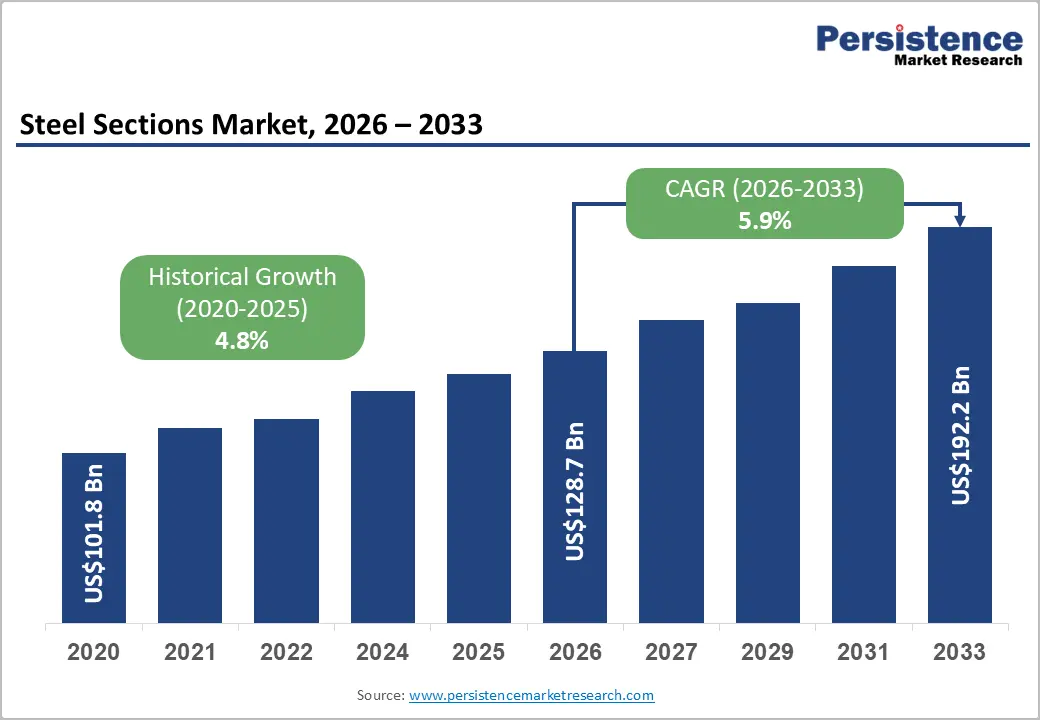

The global steel sections market size is likely to be valued at US$128.7 billion in 2026 and is expected to reach US$192.2 billion by 2033, growing at a CAGR of 5.9% between 2026 and 2033, driven by large-scale infrastructure spending, recovery in construction activity, rising renewable-energy investments, and growing demand for fabricated structural steel systems.

Public infrastructure programs in the U.S., India, and Southeast Asia continue to support demand for structural beams, channels, and heavy steel profiles used in transportation, industrial, and utility projects. Decarbonization initiatives are also reshaping procurement strategies, encouraging steel producers to develop lower-emission long products, advanced high-strength sections, and regionally integrated processing networks.

Key Industry Highlights:

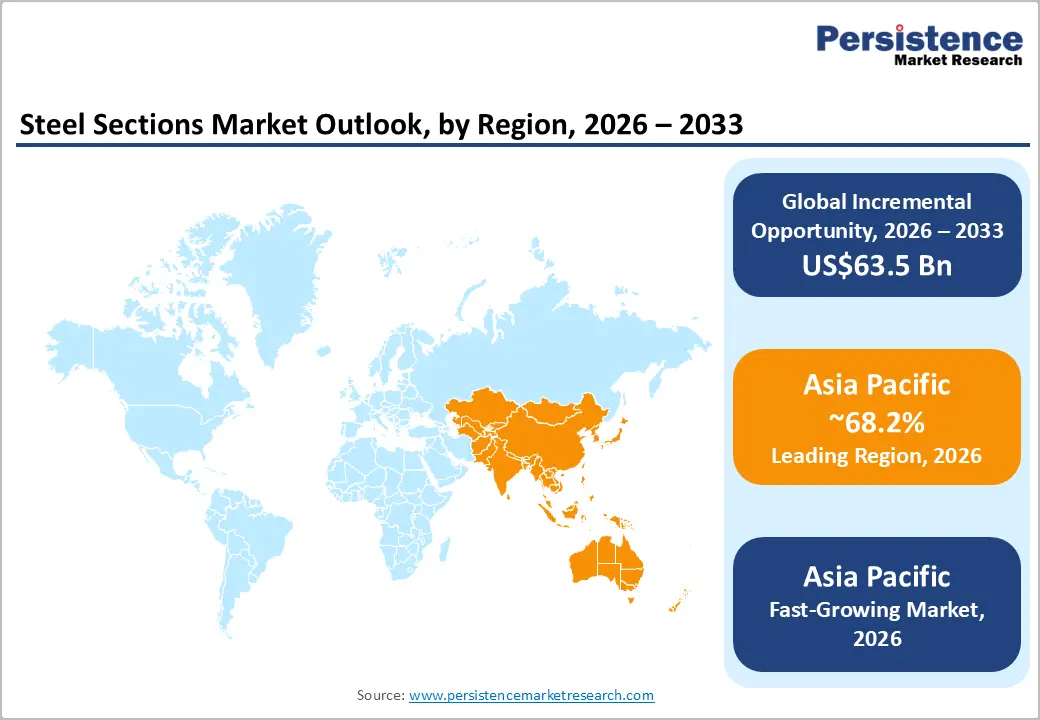

- Leading Region: Asia Pacific is projected to account for approximately 68.2% of market revenue in 2026, supported by large-scale infrastructure development, manufacturing concentration, and strong construction activity across China, India, Japan, and ASEAN countries.

- Fastest-growing Region: Asia Pacific is projected to remain the fastest-growing regional market during the forecast period, driven by rapid urbanization, renewable-energy investments, industrial corridor development, and expanding logistics infrastructure in India and Southeast Asia.

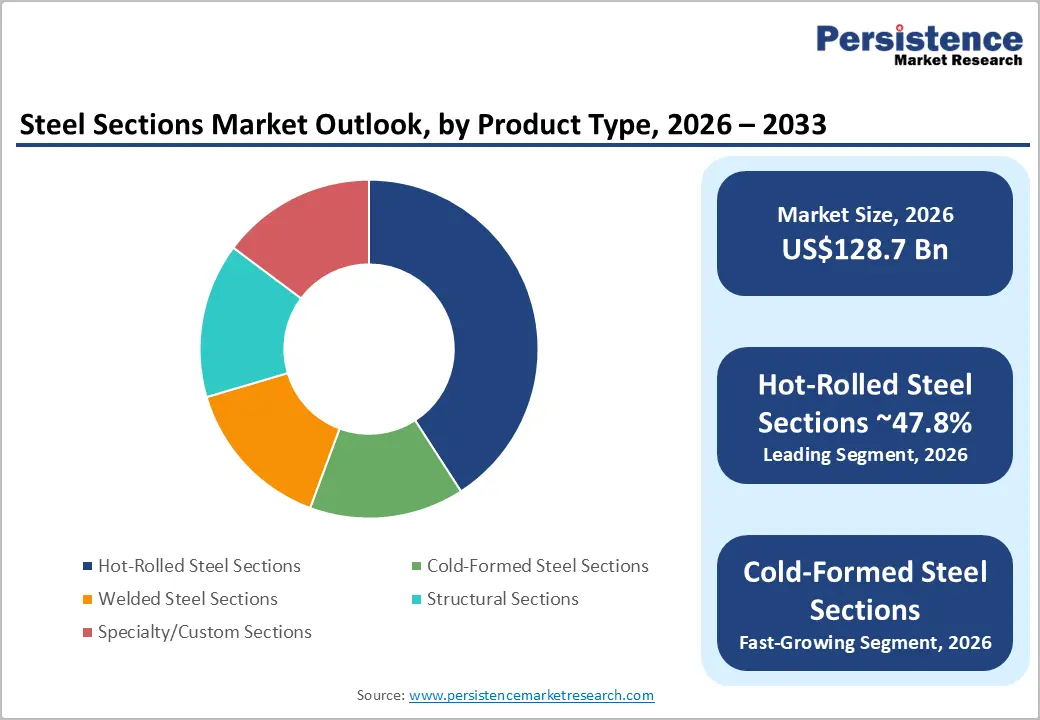

- Dominant Product Type: Hot-rolled steel sections are anticipated to account for approximately 47.8% of market revenue in 2026, owing to extensive use in bridges, industrial facilities, transportation infrastructure, and commercial construction projects.

- Leading Application: Construction is estimated to account for 59.1% of market share in 2026, supported by urbanization, government-backed infrastructure spending, commercial real-estate expansion, and industrial development projects worldwide.

DRO Analysis

Drivers - Infrastructure Investment Accelerates Structural Steel Demand

Infrastructure development remains the strongest growth driver for the steel sections market. Governments across major economies continue allocating significant capital toward transportation networks, industrial corridors, energy systems, airports, railways, and urban infrastructure projects. In the U.S., infrastructure modernization programs are supporting sustained demand for structural beams, channels, and fabricated steel systems used in bridges, highways, ports, and public transit projects. India is also expanding infrastructure spending through rail modernization, metro projects, smart cities, and industrial corridors, resulting in rising consumption of hot-rolled and fabricated steel sections.

The direct market impact includes stronger order volumes for industrial plants, warehouses, logistics parks, renewable-energy installations, and commercial construction projects. Steel section manufacturers benefit from long-term project pipelines that improve production planning and capacity utilization. Infrastructure-led demand also supports higher value-added fabricated sections, customized structural systems, and downstream processing services.

Energy Transition Expands Demand for Structural Steel Systems

The global transition toward renewable energy is creating substantial opportunities for steel section manufacturers. Solar farms, wind towers, transmission systems, substations, and energy-storage infrastructure all require large quantities of structural steel profiles and fabricated support systems. Renewable-energy expansion programs across Europe, North America, China, and India are increasing demand for heavy structural sections, corrosion-resistant profiles, and high-strength fabricated components.

Wind energy installations represent a particularly important growth segment as turbine towers, offshore foundations, and transmission infrastructure require large-scale structural steel applications. Steel producers are increasingly supplying low-carbon and traceable structural products to renewable-energy developers seeking reduced lifecycle emissions. This shift strengthens demand for advanced structural sections while encouraging investment in cleaner steelmaking technologies, recycled-content steel, and localized fabrication capacity.

Restraint - Raw Material Volatility and Regulatory Compliance Pressure Profitability

Fluctuating raw material costs remain a major challenge for steel section manufacturers. Variations in iron ore, scrap steel, coal, electricity, and transportation costs directly influence steel pricing and production margins. Geopolitical tensions, trade restrictions, shipping disruptions, and energy-market volatility continue to affect global steel supply chains and procurement strategies.

Regulatory compliance requirements also create operational complexity. Carbon-emissions regulations, environmental reporting obligations, and cross-border carbon adjustment mechanisms increase administrative and production costs for steel producers and importers. In Europe, stricter emissions standards are accelerating the transition toward lower-carbon steel production, requiring substantial capital investments in electric arc furnaces, hydrogen-based technologies, and energy-efficient manufacturing systems.

Smaller manufacturers without sufficient financial resources may struggle to adapt to evolving regulatory expectations, potentially affecting competitiveness and market participation.

Opportunity - Low-Carbon Steel Sections Create High-Value Growth Opportunities

The transition toward sustainable construction and industrial decarbonization is generating new opportunities for low-carbon steel sections. Governments, infrastructure developers, renewable-energy companies, and multinational corporations increasingly prioritize reduced-emission construction materials in procurement decisions. This trend encourages steelmakers to expand green-steel production, improve recycled content utilization, and develop transparent emissions-reporting systems.

Steel section suppliers capable of offering certified low-emission structural products are positioned to gain competitive advantages in infrastructure, commercial construction, and renewable-energy projects. Investments in electric arc furnace technology, renewable-powered steel production, and advanced recycling systems are expected to strengthen market differentiation. Regionalized processing and fabrication facilities also support faster delivery times and improved project responsiveness, particularly for modular construction and industrial manufacturing applications.

Prefabricated and Modular Construction Supports Specialty Section Growth

The expansion of modular construction and prefabricated building systems is increasing demand for lightweight, customizable, and high-strength steel sections. Developers and contractors are increasingly adopting off-site manufacturing approaches to reduce construction timelines, labor dependency, material waste, and project costs. Cold-formed sections, Z-sections, and specialty profiles are gaining popularity in warehouses, industrial sheds, commercial buildings, logistics facilities, and modular residential structures.

Manufacturers that combine steel production with downstream processing services such as coating, punching, precision cutting, and prefabrication are expected to capture higher-value opportunities. Demand for customized structural systems is particularly strong in rapidly urbanizing regions where construction efficiency and project speed remain critical competitive factors.

Category-wise Analysis

Product Type Insights

Hot-rolled steel sections are anticipated to account for approximately 47.8% of market revenue during the forecast period. Their leadership is supported by extensive use in bridges, industrial plants, airports, rail infrastructure, and high-rise commercial buildings. Products such as I-beams, channels, and heavy structural profiles are widely used in projects including metro rail systems in India, highway bridge construction in the U.S., and industrial expansion projects across Southeast Asia due to their high load-bearing strength and cost efficiency.

Cold-formed steel sections are projected to witness the fastest growth, due to rising adoption in modular buildings, warehouses, prefabricated housing, and logistics facilities. These lightweight profiles improve installation speed and reduce material waste, making them increasingly preferred in industrial sheds and e-commerce distribution centers. For example, cold-formed sections are widely used in prefabricated commercial buildings and solar mounting structures across China and Europe, where faster construction timelines and energy-efficient building practices are becoming industry priorities.

Application Insights

The construction segment is anticipated to hold approximately 59.1% of the market share in 2026. Steel sections are extensively utilized in commercial complexes, bridges, rail corridors, airports, industrial facilities, and residential towers. Major infrastructure programs such as smart-city developments in India, transportation modernization projects in the U.S., and urban redevelopment initiatives in the Middle East continue driving structural steel consumption. Fabricated steel systems are increasingly preferred in data centers, logistics parks, and manufacturing plants due to their durability and construction efficiency.

Renewable energy is expected to be the fastest-growing application segment, due to expanding investments in wind farms, solar parks, and transmission infrastructure. Structural steel sections are essential in wind turbine towers, solar mounting systems, substations, and grid-support frameworks. Offshore wind projects in Europe and large-scale solar installations in China and India are significantly increasing demand for heavy structural sections and corrosion-resistant fabricated steel systems. The global transition toward low-carbon energy infrastructure is expected to create sustained long-term opportunities for steel section manufacturers.

Regional Insights

North America Steel Sections Market Trends

North America remains a technologically advanced and stable steel sections market, supported by infrastructure modernization, industrial reshoring, renewable-energy investments, and commercial construction activity. The region continues to witness strong demand for structural beams, channels, and fabricated steel systems used in transportation infrastructure, industrial facilities, logistics parks, and utility projects. Steel producers across North America are also increasing investments in electric arc furnace technology, recycled steel utilization, and lower-emission manufacturing processes to align with sustainability objectives.

U.S. Steel Sections Market Trends

The U.S. dominates regional demand due to large-scale transportation upgrades, manufacturing expansion, and utility infrastructure investments. Federal infrastructure funding programs continue supporting long-term structural steel consumption in bridges, highways, railways, airports, and ports. Industrial reshoring and data-center expansion are also increasing demand for steel-intensive manufacturing facilities and warehouse construction. Renewable-energy projects, particularly utility-scale solar and wind installations, continue strengthening demand for fabricated structural systems.

Canada Steel Sections Market Trends

Canada contributes significantly through energy infrastructure, mining projects, and commercial construction activity. Demand for steel sections remains supported by investments in transmission infrastructure, industrial facilities, and transportation upgrades. The country’s focus on sustainable construction and renewable-energy expansion is also increasing the use of recycled and lower-emission structural steel products.

Europe Steel Sections Market Trends

Europe remains a strategically important market driven by industrial modernization, renewable-energy investments, and sustainability-focused infrastructure development. The region is strongly influenced by decarbonization initiatives, carbon-emission regulations, and green-building standards, which are accelerating investments in low-carbon steel production and energy-efficient fabrication systems. Demand for traceable and environmentally compliant structural steel products continues to increase across commercial construction and industrial projects.

Germany Steel Sections Market Trends

Germany leads regional demand due to its advanced manufacturing base, automotive industry, engineering sector, and industrial construction activity. Investments in renewable-energy infrastructure, industrial retrofitting, and hydrogen-based steelmaking technologies continue to support the demand for steel sections. Offshore wind projects and logistics infrastructure are also contributing to rising structural steel consumption.

U.K. Steel Sections Market Trends

The U.K. market is supported by transportation modernization projects, urban redevelopment, and renewable-energy expansion. Offshore wind installations, rail infrastructure upgrades, and commercial building developments continue driving demand for fabricated steel systems and heavy structural sections.

France Steel Sections Market Trends

France remains an important market due to investments in sustainable infrastructure, transportation systems, and industrial modernization projects. Public-sector construction initiatives and renewable-energy development programs are increasing demand for structural steel components in commercial and utility applications.

Asia Pacific Steel Sections Market Trends

Asia Pacific is the largest and fastest-growing regional market, accounting for approximately 68.2% of market revenue in 2026. The region benefits from rapid urbanization, extensive infrastructure development, manufacturing concentration, and strong industrial expansion. Integrated steel supply chains, competitive production costs, and export-oriented fabrication capabilities continue to position Asia Pacific as the global center for steel sections production and consumption.

China Steel Sections Market Trends

China remains the region’s dominant steel producer and consumer due to extensive manufacturing capacity, urban construction activity, infrastructure investment, and export-oriented fabrication industries. Although the country’s real-estate sector has experienced slower growth, government-backed infrastructure spending and industrial expansion continue supporting demand for structural steel sections. Renewable-energy installations and transportation infrastructure projects also contribute significantly to market growth.

India Steel Sections Market Trends

India represents the fastest-growing major market in the region, supported by transportation infrastructure expansion, rail modernization, industrial corridors, renewable-energy projects, and urbanization. Government initiatives focused on manufacturing development, logistics infrastructure, and smart-city projects continue to increase demand for fabricated steel systems, beams, and structural profiles. Growth in industrial warehouses and metro rail projects is also supporting long-term consumption.

Japan Steel Sections Market Trends

Japan contributes through advanced manufacturing, industrial engineering, and commercial infrastructure development. Demand for high-quality structural steel sections remains strong in earthquake-resistant buildings, transportation systems, and industrial modernization projects. The country also focuses heavily on high-strength and precision-engineered steel products.

Competitive Landscape

The global steel sections market is moderately consolidated at the steel-production level but fragmented across downstream fabrication and regional distribution networks. Competition is influenced by production scale, geographic reach, product quality, fabrication capability, pricing strategy, and sustainability performance.

Leading companies are prioritizing regional expansion, low-carbon steel production, value-added fabrication, and supply-chain localization. Investments in processing centers, downstream fabrication capabilities, renewable-energy partnerships, and high-strength steel technologies remain key competitive strategies. Manufacturers increasingly differentiate themselves through sustainability performance, customized structural solutions, shorter delivery timelines, and integrated project support services.

Key Industry Developments:

- In January 2025, Salzgitter AG, ENERCON, and TMGROUP announced the development of the first lower-emissions steel tower for onshore wind turbines in Germany, aiming to strengthen sustainable steel applications in renewable-energy infrastructure.

- In February 2025, Salzgitter AG signed a contract with Siemens Gamesa to supply approximately 25,000 tonnes of heavy steel plates for 36 offshore wind towers for the Thor offshore wind farm in Denmark, supporting the expansion of low-CO2 structural steel solutions for wind-energy projects.

Companies Covered in Steel Sections Market

- ArcelorMittal

- Nippon Steel Corporation

- Tata Steel

- JSW Steel

- Nucor Corporation

- POSCO Holdings

- JFE Steel Corporation

- SSAB AB

- thyssenkrupp Steel Europe

- Salzgitter AG

- Hyundai Steel

- Ternium S.A.

- EVRAZ plc

- Gerdau S.A.

- Commercial Metals Company (CMC)

- Steel Authority of India Limited (SAIL)

Frequently Asked Questions

The global steel sections market is estimated to be valued at US$128.7 billion in 2026.

The steel sections market is projected to reach approximately US$192.2 billion by 2033.

Key trends include increasing adoption of low-carbon steel production, rising demand for modular and prefabricated construction, expansion of renewable-energy infrastructure, and growing investments in high-strength and lightweight structural steel sections.

Hot-rolled steel sections lead the market, accounting for nearly 47.8% of total revenue, owing to extensive use in bridges, industrial facilities, rail infrastructure, and commercial construction projects.

The steel sections market is expected to grow at a CAGR of 5.9% between 2026 and 2033.

Major companies include ArcelorMittal, Nippon Steel Corporation, Tata Steel, JSW Steel, and Nucor Corporation.