- Plastics, Polymers & Resins

- Specialty Polymers Market

Specialty Polymers Market Size, Share, and Growth Forecast, 2026 - 2033

Specialty Polymers Market by Product Type (Synthetic Specialty Polymers, Fluoropolymers, Others), End-user Industry (Electronics & Electrical, Healthcare & Medical Devices, Others), Source, and Regional Analysis for 2026 - 2033

Specialty Polymers Market Size and Trends Analysis

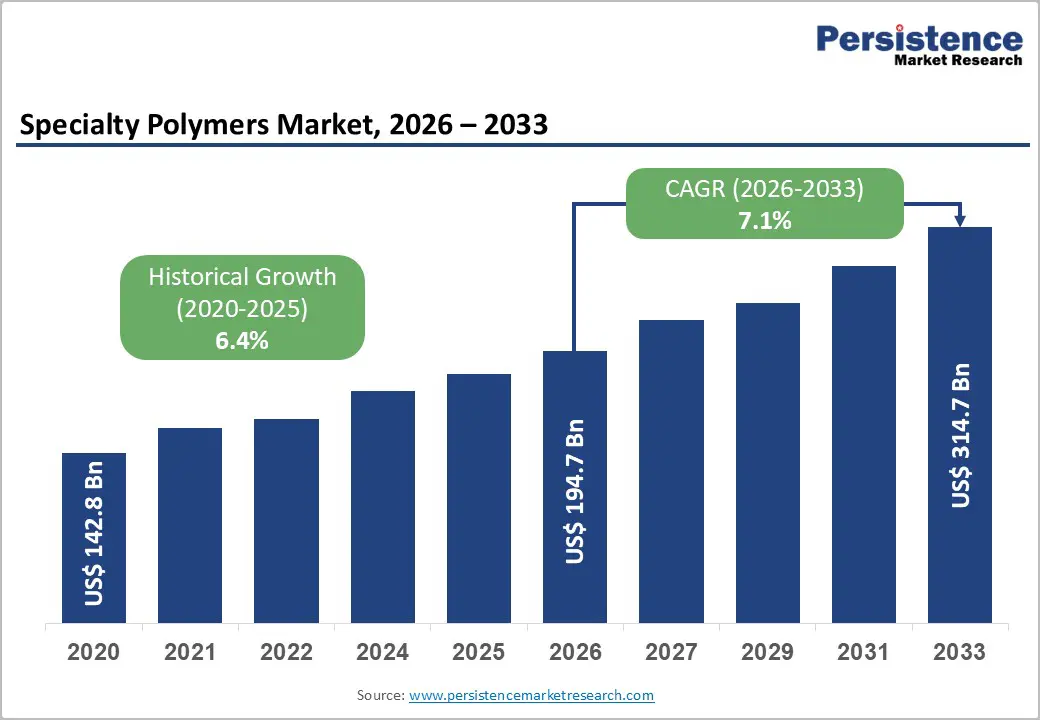

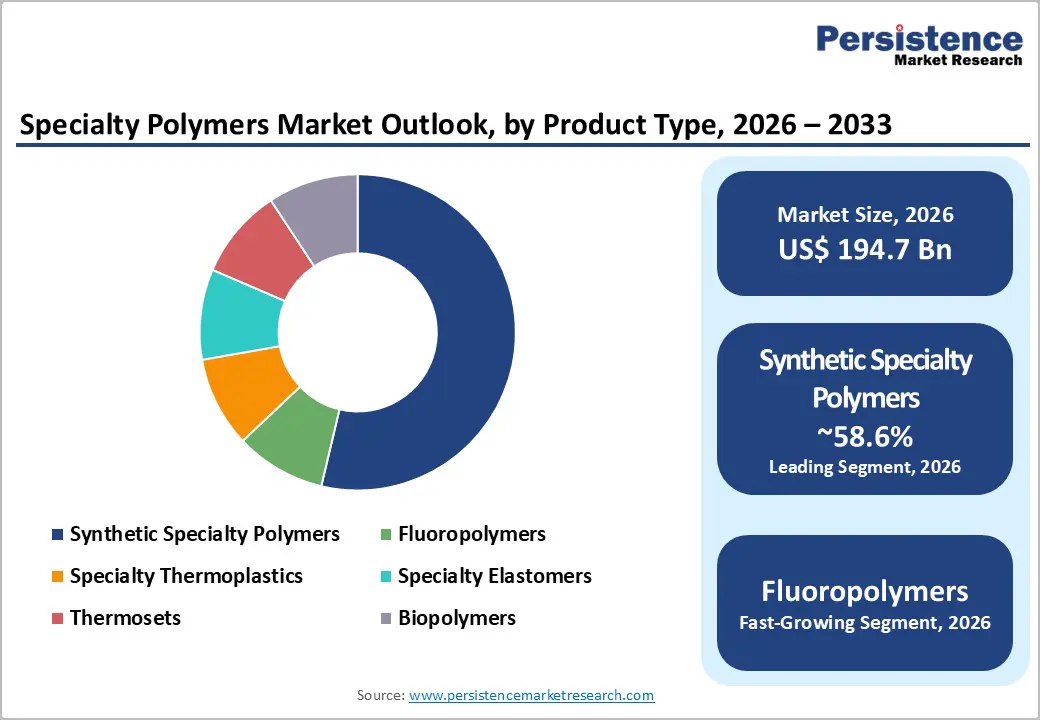

The global specialty polymers market size is likely to be valued at US$194.7 billion in 2026 and is expected to reach US$314.7 billion by 2033, growing at a CAGR of 7.1% between 2026 and 2033, driven by rising demand for high-performance materials across electronics, electric vehicles, healthcare devices, and sustainable packaging.

Regulatory pressure to reduce emissions and improve recyclability is accelerating the adoption of advanced polymer formulations. Material innovation and application-specific customization are also strengthening the role of specialty polymers in high-value industrial ecosystems.

Key Industry Highlights:

- Leading Region: Asia Pacific is projected to account for approximately 41.2% of the market share, driven by large-scale manufacturing, strong electronics production, and expanding automotive demand.

- Fastest-growing Region: Asia Pacific is also the fastest-growing region, supported by rapid industrialization, increasing localization of production, and rising demand from China, India, and ASEAN economies.

- Investment Plans: The market is witnessing increased investments in capacity expansion, bio-based polymer production, and recycling technologies, particularly in the Asia Pacific and Europe, as companies focus on sustainability and regional supply chain strengthening.

- Dominant Product Type: Synthetic specialty polymers account for approximately 58.6% of market share, driven by their scalability, consistent performance, and widespread industrial applications.

- Leading End-User Industry: Automotive and transportation remain the leading segment, contributing around 29.8% of the market, driven by demand for lightweight materials, electric vehicle components, and enhanced fuel efficiency.

| Key Insights | Details |

|---|---|

| Specialty Polymers Market Size (2026E) | US$194.7 Bn |

| Market Value Forecast (2033F) | US$314.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.4% |

DRO Analysis

Driver Analysis - Semiconductor Miniaturization Driving High-Performance Polymer Demand

Miniaturization in electronics and advanced packaging is strengthening demand for specialty polymers. Semiconductor architectures are evolving toward higher density and performance, requiring materials that can deliver thermal stability, dielectric strength, and chemical resistance. Specialty polymers are widely used in connectors, circuit boards, encapsulation, and insulation layers, where dimensional precision and reliability are critical. The transition toward advanced packaging technologies, including system-in-package and heterogeneous integration, is increasing polymer consumption per device. This trend creates long-term value for suppliers, as once a material is qualified, switching costs remain high and support recurring demand across product cycles.

EV Electrification Increasing Polymer Intensity and Value

Electric vehicle growth is expanding the use of lightweight and heat-resistant polymer systems. Electrification is fundamentally increasing polymer intensity in vehicles due to requirements for battery insulation, thermal management, vibration damping, and lightweight structural components. Specialty thermoplastics, elastomers, and fluoropolymers are increasingly used in battery packs, power electronics, wiring harnesses, and charging systems. Compared to internal combustion engine vehicles, electric vehicles require higher-performance materials to manage heat and electrical loads. This shift not only increases total demand volume but also drives value growth through premium-grade materials that command higher margins.

Aging Population Expanding Biocompatible Polymer Applications

Healthcare aging and device innovation are widening the addressable market for biocompatible polymers. The global aging population is driving sustained demand for medical devices, including implants, catheters, diagnostic systems, and drug-delivery solutions. Specialty polymers play a critical role due to their ability to meet stringent requirements for sterilization, flexibility, chemical resistance, and long-term biocompatibility. Advancements in additive manufacturing and patient-specific device design are further expanding applications. This segment offers high-margin opportunities because of strict regulatory approval processes and long product life cycles, which create strong barriers to entry and limit substitution risk.

Restraint Analysis - Petrochemical Feedstock Volatility Compressing Margins

Feedstock and energy volatility continue to pressure margins, particularly for synthetic and petrochemical-based materials. Specialty polymer production is closely linked to petrochemical inputs, making it sensitive to fluctuations in crude oil and natural gas prices. These cost variations affect resin pricing, production economics, and overall profitability. While manufacturers can partially pass on increased costs, pricing adjustments are often delayed due to long-term contracts and qualification cycles. This dynamic can compress margins, disrupt procurement planning, and discourage capacity expansion, especially for smaller or regionally focused players.

PFAS-Linked Regulatory Pressure on Fluoropolymers

Regulatory scrutiny around fluorinated compounds is increasing compliance complexity. Environmental and chemical safety regulations are tightening, particularly for fluoropolymer-related materials associated with PFAS concerns. Compliance now requires extensive testing, reporting, and lifecycle assessments, increasing operational costs. Uncertainty around evolving regulations can delay customer adoption and investment decisions in certain applications. This challenge is particularly pronounced in regions with stringent environmental frameworks, where manufacturers must balance performance requirements with regulatory expectations and potential substitution risks.

Opportunity Analysis - Bio-Based Polymers Gaining Traction from Sustainability Mandates

Bio-based specialty polymers present a strong growth opportunity driven by sustainability mandates. Governments and regulatory bodies are promoting the use of renewable and recyclable materials to reduce environmental impact. This shift is creating demand for bio-based polymers in packaging, healthcare, and consumer goods. These materials offer the advantage of a reduced carbon footprint while maintaining performance standards. Companies that can deliver certified, traceable, and application-specific bio-based solutions are well-positioned to capture premium market segments, particularly where sustainability is a key purchasing criterion.

Asia Pacific Localization Boosting Capacity and Demand

Asia Pacific localization is unlocking capacity expansion and demand growth. The region continues to lead global consumption due to its strong manufacturing base, expanding industrial output, and growing domestic markets. Increasing localization of production facilities is improving supply chain resilience and reducing costs. Investments in regional capacity, particularly in Southeast Asia and India, are enabling faster response to customer needs. This creates opportunities for both global and regional players to strengthen their presence through partnerships, joint ventures, and localized production strategies.

High-Purity Semiconductor and Battery Applications Driving Premium Growth

High-purity semiconductor and battery applications are emerging as premium demand segments. Advanced electronics and energy storage systems require materials with extremely high purity, thermal stability, and chemical resistance. Specialty polymers are increasingly used in semiconductor fabrication, advanced packaging, and battery components. These applications demand highly customized formulations, which limits competition and supports higher margins. As industries such as artificial intelligence, renewable energy, and electric mobility expand, demand for these specialized materials is expected to accelerate.

Category-wise Analysis

Product Type Insights

Synthetic specialty polymers are anticipated to remain the leading segment, accounting for approximately 58.6% of market share in 2026. Their dominance is supported by well-established global supply chains, scalable production processes, and consistent performance characteristics across diverse applications. These polymers are extensively used in automotive components such as fuel systems and lightweight structural parts, in electronics for insulation and connectors, and in healthcare for tubing and device housings. Their ability to be precisely engineered for mechanical strength, thermal stability, and chemical resistance makes them the preferred choice for high-volume and high-reliability applications. The widespread availability of petrochemical feedstocks further ensures stable production, reinforcing long-term market leadership.

Fluoropolymers are the fastest-growing segment due to increasing demand for high-performance materials in extreme environments. These polymers offer exceptional resistance to heat, chemicals, and environmental stress, making them essential in semiconductor fabrication equipment, wire and cable insulation, and clean energy systems such as solar panels and hydrogen infrastructure. Growth is particularly strong in applications requiring durability under harsh conditions, including chemical processing and advanced electronics manufacturing. Specialty thermoplastics continue to gain traction due to their recyclability and ease of processing, while specialty elastomers are widely used in automotive sealing systems and electronic components for vibration control. Thermosets and biopolymers are also expanding, particularly in aerospace composites and sustainable packaging, though their growth remains more application-specific.

End-user Industry Insights

The automotive and transportation segment is anticipated to account for approximately 29.8% of the market in 2026. Growth is driven by the increasing need for lightweight, durable, and fuel-efficient materials. Specialty polymers are widely used to replace metals in components such as dashboards, fuel systems, battery enclosures, and wiring harnesses, reducing overall vehicle weight and improving energy efficiency. In electric vehicles, these materials play a critical role in thermal management, insulation, and structural integrity. At the same time, the electronics and electrical sector represents a high-value demand segment, with specialty polymers used in connectors, printed circuit boards, and advanced semiconductor packaging, where miniaturization and reliability are essential.

Healthcare and medical devices are the fastest-growing segment, driven by rising healthcare demand and technological advancements. Specialty polymers are essential for applications such as catheters, surgical instruments, implantable devices, and diagnostic equipment due to their biocompatibility, resistance to sterilization, and flexibility. The adoption of advanced manufacturing techniques, including 3D printing of medical devices, is further expanding their use. Packaging is also experiencing steady growth, particularly in sustainable and high-barrier materials for food and pharmaceuticals. Meanwhile, the construction and industrial machinery sectors continue to adopt specialty polymers for applications that require corrosion resistance, durability, and reduced maintenance, thereby ensuring a balanced demand profile across industries.

Regional Insights

North America Specialty Polymers Market Trends - Innovation-Led Growth in EVs, Semiconductors, and Sustainable Materials

North America remains a technologically advanced and innovation-driven market for specialty polymers, with the U.S. leading regional demand. This leadership is supported by strong consumption across automotive, aerospace, healthcare, and electronics industries, alongside a highly developed R&D ecosystem. Major manufacturers such as DuPont, Dow, and Celanese continue to invest in high-performance polymer solutions, particularly for electrification and advanced manufacturing. The region benefits from advanced processing technologies and a strong focus on high-specification materials, enabling faster commercialization of next-generation polymers.

Growth is being reinforced by increasing electric vehicle adoption, semiconductor reshoring, and rising healthcare demand. For instance, the expansion of semiconductor manufacturing capacity under U.S. industrial policy has increased demand for ultra-pure polymers used in wafer processing and advanced packaging. Companies such as Avient Corporation are actively developing sustainable polymer solutions, including recycled-content materials for packaging and consumer applications, aligning with regulatory and customer expectations.

Regulatory frameworks emphasizing environmental compliance and product safety are also accelerating innovation in recyclable and low-emission materials. Investment trends in North America increasingly focus on advanced materials research, circular economy initiatives, and localized production, enabling companies to respond more effectively to supply chain disruptions and evolving end-user requirements.

Europe Specialty Polymers Market Trends - Regulation-Driven Circular Economy and Advanced Material Innovation

Europe is characterized by a highly structured regulatory environment and a strong emphasis on sustainability and circular economy principles. Key markets such as Germany, the U.K., France, and Spain drive demand through automotive, industrial, and healthcare sectors. The region prioritizes high-quality, compliant materials that meet strict environmental and safety standards. Companies such as BASF and Arkema are at the forefront of developing advanced polymers that align with these regulatory requirements, particularly in engineering plastics and bio-based materials.

Regulatory initiatives promoting recyclability and reduced carbon emissions are reshaping material innovation across the region. For example, Arkema has introduced recyclable thermoplastic resins such as Elium® for composite applications, enabling easier material recovery in sectors such as wind energy and automotive. Similarly, BASF is advancing its ChemCycling™ initiative, which converts plastic waste into feedstock for new polymers, thereby supporting circular-economy goals.

While compliance costs remain relatively high, they create significant barriers to entry and allow established players to maintain premium pricing. Investment is increasingly directed toward low-carbon production technologies, recycling infrastructure, and specialty applications such as battery materials and high-performance composites, reinforcing Europe’s position as a leader in sustainable polymer innovation.

Asia Pacific Specialty Polymers Market Trends - Manufacturing Dominance and Shift toward High-Value Polymer Production

Asia Pacific leads the global specialty polymers market, accounting for approximately 41.2% of total market share, driven by large-scale manufacturing, strong demand from electronics and automotive industries, and rapid industrialization. China remains the largest market due to its extensive manufacturing base and leadership in electric vehicle production. Japan contributes through advanced materials innovation and precision engineering, while India and ASEAN countries are emerging as high-growth markets due to expanding industrial output and domestic consumption.

The region’s competitive advantage lies in cost efficiency, integrated supply chains, and proximity to end-use manufacturing hubs. Recent developments highlight strong investment momentum; for instance, Arkema is expanding its bio-based polyamide production capacity in Singapore, strengthening its position in high-performance and sustainable polymers within the region. Similarly, Chemours has entered strategic agreements in India to enhance fluoropolymer supply, reflecting growing regional demand for advanced materials in electronics and industrial applications. In China, domestic producers such as Sinopec are increasing investments in high-value polymer production to reduce reliance on imports.

These developments indicate a clear shift toward regional self-sufficiency and higher-value manufacturing. While competition remains intense, the Asia Pacific continues to offer strong growth potential due to increasing investments in capacity expansion, infrastructure development, and export-oriented production. Companies that can balance cost competitiveness with product quality, regulatory compliance, and localized technical support are best positioned to capitalize on the region’s evolving market dynamics.

Competitive Landscape

The global specialty polymers market is fragmented to moderately consolidated, with several global players competing across multiple application segments. Market leadership is distributed among large multinational corporations with strong product portfolios and global reach. Competitive advantage is driven by technical expertise, product innovation, regulatory compliance, and customer relationships rather than scale alone. Companies differentiate themselves through specialized applications and high-performance material offerings.

Key players are focusing on innovation, sustainability, and regional expansion. Strategies include developing high-performance materials, investing in recycling technologies, and strengthening supply chain localization. Collaboration with end users and customization of products for specific applications are becoming critical differentiators in a competitive market.

Key Industry Developments

- In September 2025, Arkema announced new high-performance polymer innovations at K 2025, including the launch of its Zenimid™ polyimide range and expansion of Kynar® PVDF capacity in the U.S., targeting growth in electronics, energy storage, and electric mobility.

- In August 2025, Chemours entered strategic agreements with SRF Limited to expand fluoropolymer and fluoroelastomer supply capacity, strengthening global supply chains for semiconductor, automotive, and industrial applications.

Companies Covered in Specialty Polymers Market

- DuPont

- BASF

- Arkema

- Celanese

- Dow

- SABIC

- Eastman Chemical Company

- Victrex plc

- Mitsubishi Chemical Group

- LG Chem

- Kuraray Co., Ltd.

- Asahi Kasei Corporation

- Avient Corporation

- Ensinger GmbH

- Solvay

- Syensqo

Frequently Asked Questions

The global specialty polymers market is estimated to be valued at US$194.7 billion in 2026.

The specialty polymers market is projected to reach US$314.7 billion by 2033.

Key trends include rising demand for high-performance polymers in electric vehicles and electronics, increasing adoption of bio-based and recyclable materials, and growing use of specialty polymers in healthcare and semiconductor applications.

Synthetic specialty polymers lead the market, accounting for approximately 58.6% of market share, driven by scalability, performance consistency, and broad industrial applications.

The market is expected to grow at a CAGR of 7.1% from 2026 to 2033.

Major players with strong portfolios include DuPont, BASF, Arkema, Celanese, and SABIC.