- Bulk Chemicals

- Silicone Surfactants Market

Silicone Surfactants Market Size, Share, and Growth Forecast 2026 - 2033

Silicone Surfactants Market by Product Type (Cationic Silicone Surfactant, Anionic Silicone Surfactant, Nonionic Silicone Surfactants, Amphoteric Silicone Surfactants), Application (Emulsifiers, Foaming Agents, Defoaming Agents, Wetting Agents, Dispersants, Others), End-user (Personal Care, Construction, Textiles and Non-wovens, Paints & Coatings, Furniture & Upholstery, Agriculture, Medical and Healthcare), and Regional Analysis, 2026 - 2033

Silicone Surfactants Market Size and Trend Analysis

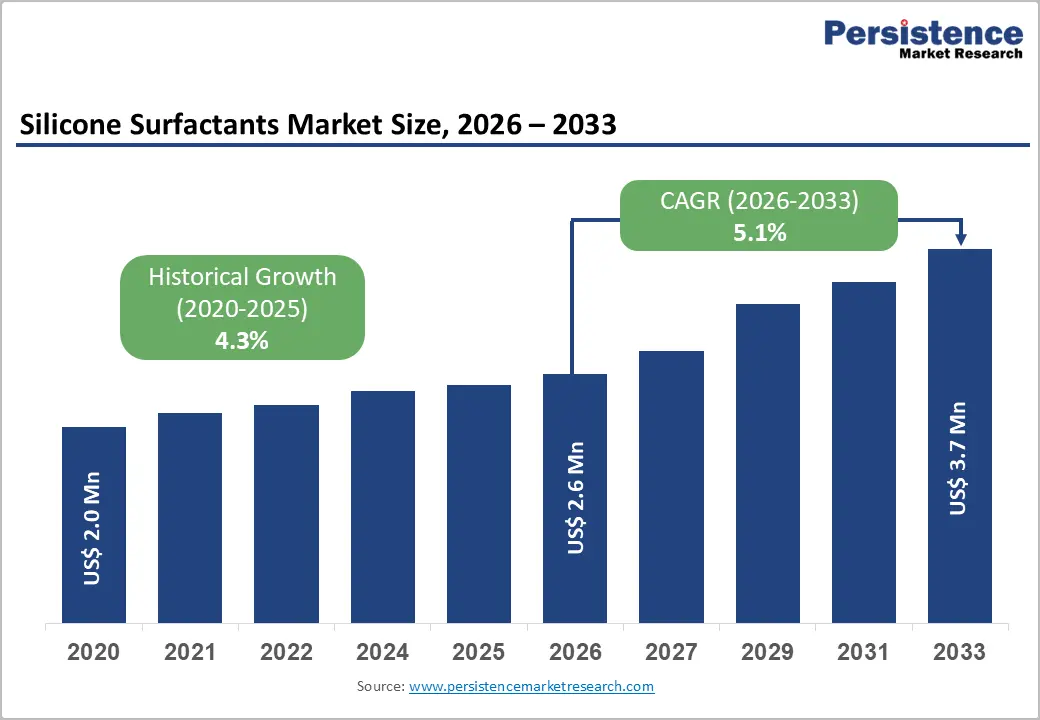

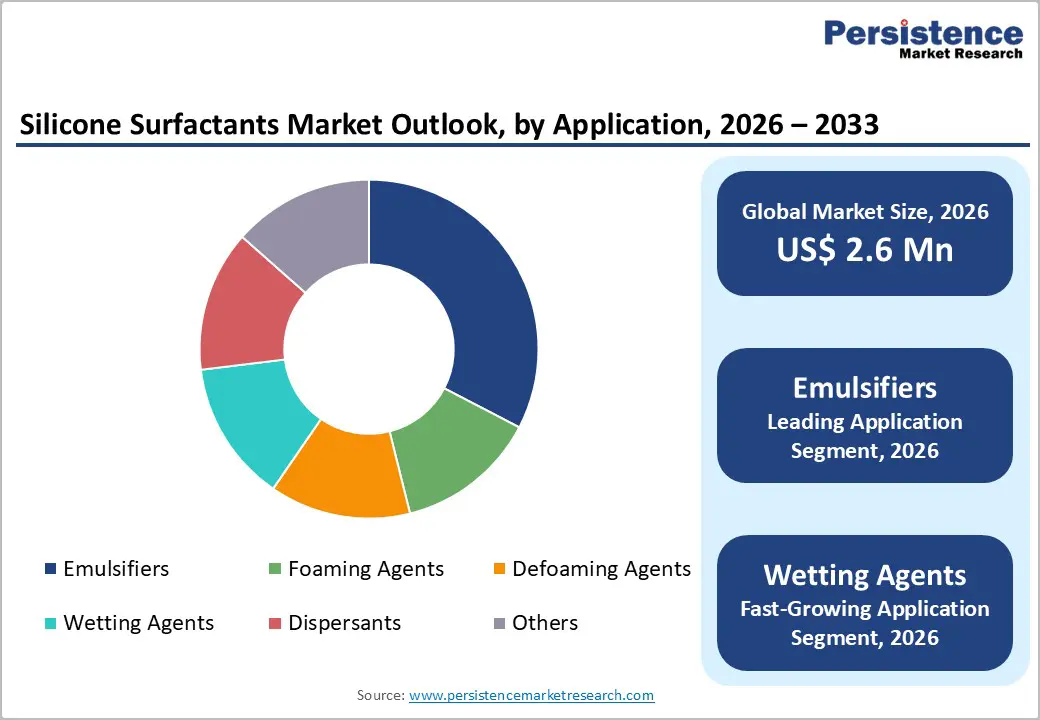

The global silicone surfactants market size is expected to be valued at US$ 2.6 billion in 2026 and projected to reach US$ 3.7 billion by 2033, growing at a CAGR of 5.1% between 2026 and 2033.

Rising demand across personal care, agriculture, and construction industries is the primary growth catalyst for the silicone surfactants market. Silicone surfactants offer unmatched surface activity, thermal stability, and low surface tension reduction compared to conventional organic surfactants, making them indispensable in high-performance formulations.

Stricter agricultural productivity mandates driven by Food and Agriculture Organization (FAO) food security targets, growing consumer preference for premium personal care products, and expanding green building initiatives are collectively reinforcing sustained volume growth in both developed and emerging economies.

Key Industry Highlights:

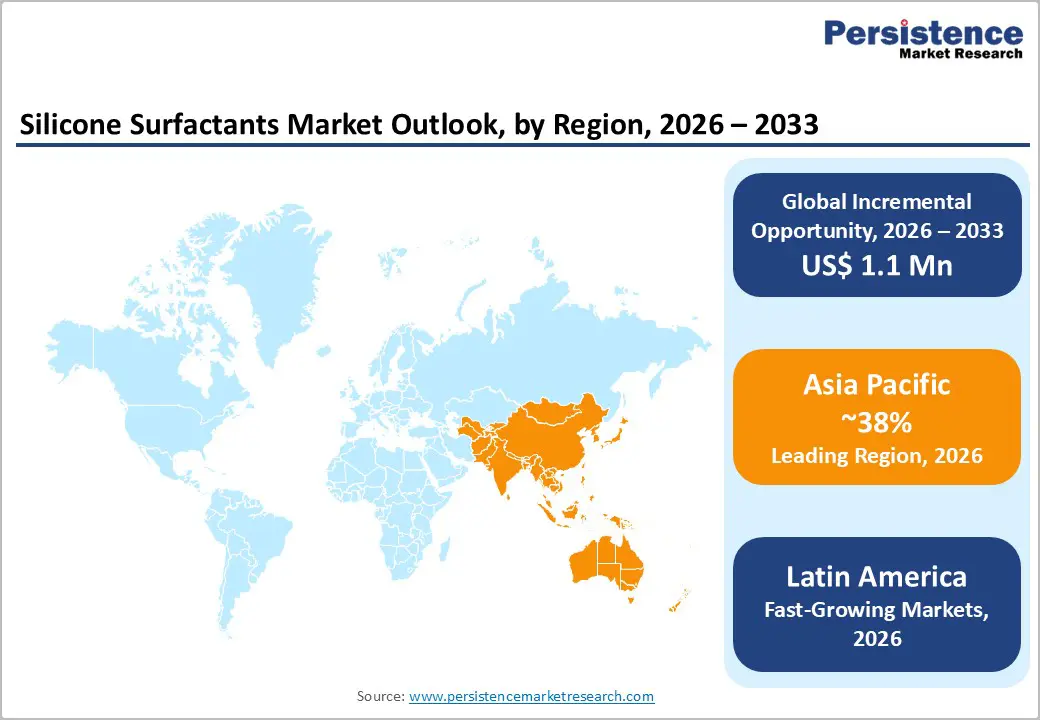

- Leading Region: Asia Pacific leads the global silicone surfactants market with approximately 38% share in 2025, underpinned by China's dominant silicon metal production capacity, India's rapidly expanding personal care and agrochemical industries, and regional government manufacturing incentive policies.

- Fastest Growing Region: Latin America is identified as one of the fastest-growing regional markets, driven by expanding precision agriculture adoption, rising agrochemical adjuvant demand across Brazil and Argentina, and growing personal care consumption tied to rising middle-class incomes.

- Dominant Segment: Nonionic silicone surfactants are the dominant product type segment, holding approximately 43% of market share in 2025, owing to their broad pH compatibility, low irritation profiles, and versatile emulsification performance across personal care, agricultural, and industrial coating applications.

- Fastest Growing Segment: Wetting agents represent the fastest-growing application segment, propelled by accelerating precision agriculture adoption globally and the proven efficacy of trisiloxane-based silicone wetting agents in reducing agrochemical application volumes while maximizing crop protection effectiveness.

- Key Opportunity: The medical and healthcare end-use segment presents the most transformative long-term market opportunity, with biocompatible, pharmaceutical-grade silicone surfactants positioned to capture growing demand from drug delivery, wound care, and minimally invasive medical device applications against a backdrop of rising global healthcare expenditure and aging demographics.

| Key Insights | Details |

|---|---|

| Silicone Surfactants Market Size (2026E) | US$ 2.6 Billion |

| Market Value Forecast (2033F) | US$ 3.7 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.1% |

| Historical Market Growth (2020 - 2025) | 4.3% |

DRO Analysis

Drivers - Expanding Demand from the Global Personal Care and Cosmetics Industry

The personal care industry represents one of the strongest demand anchors for silicone surfactants globally, and this trend shows no signs of reversing. Silicone surfactants function as conditioning agents, foam stabilizers, and emulsifiers in shampoos, conditioners, skin serums, and sunscreens. According to the Personal Care Products Council, global cosmetics and personal care revenues surpassed US$ 500 billion in 2023, with the skincare and haircare segments recording consistent year-on-year growth of approximately 4-6%. Nonionic polyether-modified polydimethylsiloxane (PDMS) surfactants are particularly favored for their mildness and compatibility with sensitive skin formulations. As consumers across Asia Pacific, North America, and Western Europe increasingly shift toward premium, multifunctional beauty formulations, particularly driven by the K-beauty movement and clean-label trends, manufacturers are incorporating higher concentrations of silicone surfactants, directly driving revenue expansion in this application space.

Rising use of Silicone Surfactants as Agrochemical Adjuvants

Silicone surfactants have become mission-critical adjuvants in modern crop protection formulations, enhancing the spreading, wetting, and stomatal infiltration of pesticides and herbicides on plant leaf surfaces. Trisiloxane-based silicone surfactants, most notably the Silwet series developed by Momentive Performance Materials, are recognized industry-wide for their super-spreading capabilities, enabling a documented 20-30% reduction in pesticide dosage while maintaining equivalent efficacy. According to the FAO, global pesticide consumption exceeded 3.5 million tonnes in 2021, and agrochemical adjuvant demand has grown in tandem with intensifying food security pressures. As global arable land per capita shrinks and precision agriculture adoption accelerates across India, Brazil, Southeast Asia, and Sub-Saharan Africa, demand for high-performance silicone-based adjuvants capable of optimizing agrochemical delivery is expected to sustain strong market momentum through the forecast period.

Restraints - Regulatory Pressures on Cyclic Volatile Methylsiloxane Compounds

Growing regulatory scrutiny on cyclic volatile methylsiloxanes (VMS), including D4 (octamethylcyclotetrasiloxane) and D5 (decamethylcyclopentasiloxane), is a meaningful growth restraint for silicone surfactant manufacturers, especially in Europe. The European Chemicals Agency (ECHA) formally classified D4 as a Substance of Very High Concern (SVHC) under the REACH framework and restricted its concentration in wash-off personal care products to 0.1% by weight, effective January 2020. These restrictions have compelled formulators to undertake costly reformulation exercises, extending time-to-market cycles and adding R&D expenditure. The expanding SVHC candidate list reviewed biannually by ECHA creates persistent regulatory uncertainty, limiting investment appetite for product development based on traditional siloxane chemistries and disproportionately burdening small and mid-sized manufacturers that lack in-house regulatory expertise.

Raw Material Price Volatility and Supply Chain Concentration Risks

Silicon metal, the foundational raw material for silicone production, is subject to intense price volatility stemming from energy-intensive manufacturing, geographic production concentration, and geopolitical supply risks. China accounts for approximately 70% of global silicon metal output according to the U.S. Geological Survey (USGS), rendering global silicone supply chains highly susceptible to regulatory changes, energy rationing, and trade policy shifts. During 2021-2022, silicon metal prices escalated by over 300% in spot markets, severely disrupting downstream silicone surfactant production globally. These cost surges erode profitability margins, especially for producers without backward integration or long-term supply contracts, and can precipitate inventory shortages, constraining manufacturers' ability to fulfill growing market demand on a reliable and cost-competitive basis.

Opportunities - Green Construction Boom Creating Demand for High-Performance Silicone Formulations

The global construction industry's accelerating pivot toward sustainable, energy-efficient building materials presents a compelling revenue opportunity for silicone surfactant manufacturers. Silicone surfactants are integral components of polyurethane foam systems used in building insulation, concrete admixtures, waterproofing agents, and sealants, all foundational to green building projects. The U.S. Green Building Council (USGBC) reported over 100,000 LEED-certified projects globally by 2023, with the certification pipeline growing rapidly. Landmark legislative drivers, including the European Green Deal targeting climate neutrality by 2050 and the U.S. Inflation Reduction Act allocating approximately US$ 369 billion toward clean energy and energy efficiency, are channeling capital into building retrofits and new sustainable construction. Companies developing tailored, low-VOC silicone surfactant grades for eco-compliant construction applications are exceptionally well-positioned to capture this expanding, policy-supported demand pipeline.

Medical and Healthcare Sector Unlocking High-Value Specialty Silicone Opportunities

The medical and healthcare industry represents a structurally high-growth opportunity for high-purity, biocompatible silicone surfactants. These specialty compounds are utilized in drug delivery systems, anti-foaming agents in pharmaceuticals, surgical lubricants, advanced wound care dressings, and diagnostic reagent formulations, leveraging their biocompatibility, inertness, and resistance to microbial proliferation. According to the World Health Organization (WHO), global healthcare expenditure reached approximately US$ 9.8 trillion in 2021, representing 10.3% of global GDP. The United Nations projects the global population aged 65 and above will approximately double from 783 million in 2023 to over 1.6 billion by 2050, substantially amplifying demand for wound care, pharmaceutical, and minimally invasive medical device applications. Manufacturers investing in GMP-certified, pharmaceutical-grade silicone surfactant production capabilities are positioning themselves to secure long-term, high-margin contracts in this structurally growth-oriented end-use sector.

Category-wise Analysis

Product Type Insights

Nonionic silicone surfactants dominate the product type category, accounting for approximately 43% of the overall silicone surfactants market share in 2025. Their leadership position is rooted in broad pH-range compatibility, low irritation potential, and highly tunable hydrophilic-lipophilic balance (HLB), which enables formulators across personal care, agriculture, and industrial coating sectors to precisely engineer surface activity for target applications. Polyether-modified polydimethylsiloxane (PDMS) derivatives, the most commercially significant nonionic variants, deliver superior emulsification, wetting, and spreading performance at usage concentrations typically below 2% by weight, making them highly cost-effective. The American Chemical Society (ACS) has recognized polyether-modified silicone surfactants as a rapidly evolving chemical class given their tunable amphiphilic architecture. Leading global producers, including Dow Inc., Shin-Etsu Chemical Co., Ltd., Evonik Industries AG, and Wacker Chemie AG maintain extensive and diversified nonionic silicone surfactant portfolios, further consolidating segment leadership through technological depth, application-specific grades, and global distribution reach.

Application Insights

Emulsifiers represent the dominant application segment, capturing approximately 28% of the silicone surfactants market share in 2025. Silicone-based emulsifiers are highly valued for their ability to stabilize oil-in-water (O/W) and water-in-oil (W/O) emulsions at remarkably low active concentrations, typically 0.1-2% by weight, while simultaneously imparting smoothness, spreadability, and enhanced skin feel in personal care formulations. The Personal Care Products Council estimates that emulsifier consumption within cosmetic formulations has grown consistently at approximately 5% annually, commensurate with overall sector expansion. Beyond personal care, silicone emulsifiers are critical functional ingredients in textile finishing concentrates, agrochemical emulsion formulations, industrial release coatings, and construction sealant systems. Their multifunctional character, stabilizing emulsions while also enhancing wetting, film formation, and conditioning, sustains their leading application market position across multiple end-use industries that simultaneously demand stability and performance efficiency.

End-user Insights

The personal care industry is the commanding dominant end-use segment, accounting for approximately 34% of the global silicone surfactants market share in 2025. This leadership is driven by silicone surfactants' unique ability to elevate sensory attributes in cosmetic formulations, imparting silky skin feel, improving foam quality, boosting hair manageability, and enhancing moisturizer spreadability, attributes increasingly expected in premium formulations. Global beauty and personal care expenditure has grown robustly with personal care segment ranking among the top three consumer spending categories across major economies in 2023. The proliferation of premium skincare brands, the clean beauty movement emphasizing ingredient safety, and the pervasive global influence of K-beauty innovation are propelling formulators to integrate high-performance silicone surfactants at growing inclusion rates. Companies including Wacker Chemie AG, Momentive Performance Materials, and Evonik Industries AG specifically develop and market silicone surfactant grades tailored to the exacting performance, safety, and sensory requirements of the personal care industry.

Regional Insights

North America Silicone Surfactants Market Trends and Insights

North America accounts for approximately 26% of the global silicone surfactants market share in 2025, with the United States as the dominant regional contributor. The U.S. market benefits from an established personal care and cosmetics manufacturing base, a technologically advanced agricultural sector, and robust construction activity stimulated by infrastructure investment under the Infrastructure Investment and Jobs Act of 2021, which committed US$ 1.2 trillion to infrastructure renewal. Domestic production leadership from Dow Inc., headquartered in Midland, Michigan, and Momentive Performance Materials ensures sustained innovation and supply reliability.

Regulatory guidance from the U.S. Environmental Protection Agency (EPA) and U.S. Food and Drug Administration (FDA) continues to shape product standards and drive investment in safer, low-VOC silicone surfactant alternatives. The Canada Green Buildings Strategy, released in 2022, is further stimulating demand for silicone surfactants in thermal insulation and weatherproofing construction applications, establishing Canada as a secondary but growing demand center within the North American regional market.

Europe Silicone Surfactants Market Trends and Insights

Europe represents approximately 23% of the global silicone surfactants market share in 2025, with Germany, France, and the United Kingdom collectively accounting for over 60% of regional consumption. Germany's globally significant specialty chemicals and automotive coatings manufacturing base, combined with its advanced technical textile sector, sustains strong demand for industrial-grade silicone surfactants. European headquarters of Evonik Industries AG and Wacker Chemie AG ensure that the region retains significant R&D and innovation infrastructure, supporting the development of next-generation, compliant silicone surfactant grades.

Regulatory harmonization under REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) and the broader European Green Deal framework are fundamentally reshaping product development priorities. The European Chemicals Agency (ECHA) continues to evaluate additional silicone compounds under its SVHC candidate list, driving accelerated investment in biodegradable and reduced-environmental-impact silicone surfactant innovations. Companies that successfully develop compliant, high-performance alternatives stand to gain sustainable competitive differentiation across the EU market through the forecast period.

Asia Pacific Silicone Surfactants Market Trends and Insights

Asia Pacific is the clear dominant regional market, holding approximately 38% of the global silicone surfactants market share in 2025, and is simultaneously the fastest-growing region, projected to expand at a CAGR of approximately 6.5% between 2026 and 2033. China serves as the global epicenter of silicon metal refining and downstream silicone chemical production, housing the world's largest manufacturing capacity and a dense ecosystem of silicone surfactant producers. Shin-Etsu Chemical Co., Ltd. (Japan) and Elkem ASA, with substantial Asian manufacturing operations, are major contributors to the region's global market positioning.

India and the ASEAN bloc are rapidly emerging as high-growth consumption markets. India's personal care market is projected to reach US$ 35 billion by 2025, reinforcing robust downstream demand for silicone surfactants. Agrochemical consumption across Southeast Asia is rising sharply alongside intensifying food security pressures and government-driven agricultural modernization programs. Policy tailwinds, including China's 14th Five-Year Plan for advanced chemical manufacturing and India's Production Linked Incentive (PLI) scheme for specialty chemicals, are accelerating regional manufacturing capacity build-out, reinforcing Asia Pacific's trajectory as both the dominant and highest-growth silicone surfactants market.

Competitive Landscape

The global silicone surfactants market exhibits a moderately consolidated structure, characterized by the presence of large integrated chemical manufacturers alongside regional and niche specialty producers. Leading players maintain a strong competitive position through vertical integration across the silicone value chain, from silicon metal to advanced siloxane intermediates, enabling cost control, supply security, and consistent product quality. Their strategies focus on developing application-specific formulations tailored to polyurethane foams, personal care, and agrochemical applications, supported by robust technical service capabilities and global distribution networks.

At the same time, mid-sized and regional players are intensifying competition by focusing on high-growth niche segments and offering customized, cost-effective solutions. Expansion in Asia Pacific and emerging markets remains a key strategic priority, driven by rising demand and localized production advantages. Companies are also investing in R&D to develop sustainable, high-performance formulations that meet evolving regulatory standards. Strategic collaborations, capacity expansions, and portfolio diversification toward specialty and high-margin applications are increasingly shaping competitive dynamics.

Key Developments:

- December 2025: BRB International launched its Sipostab silicone stabiliser range for polyurethane foam applications, offering a portfolio of silicone surfactants designed for flexible and rigid foams, while enhancing processing performance, customization capabilities, and cost competitiveness through supply chain optimization.

- September 2025: Silibase Silicone launched SilibasePUX-2100 silicone surfactant for polyurethane rigid foam applications, delivering strong foam stabilization and fine cell structure, while offering a cost-effective alternative to global products with comparable performance and suitability for construction, insulation, and appliance uses.

- June 2025: Dow debuted low-carbon silicone elastomer blends for beauty and personal care applications under its Decarbia platform, enabling reduced carbon footprint formulations while delivering high-performance properties across skincare, haircare, color cosmetics, and sun care segments.

Companies Covered in Silicone Surfactants Market

- Dow Inc.

- Innospec

- Momentive Performance Materials

- Elkem ASA

- Shin-Etsu Chemical Co., Ltd.

- Evonik Industries AG

- AB Specialty Silicones

- Supreme Silicones

- Wacker Chemie AG

- Elé Corporation

- JIAHUA CHEMICALS INC.

- CHT Silicones

- BASF SE

- SILIBASE SILICONE

- Elkay Chemicals Pvt. Ltd.

- Siltech Corporation

- KCC Basildon Chemical Company

- Nusil Technology LLC

- BRB International BV

Frequently Asked Questions

The global Silicone Surfactants market is valued at US$ 2.6 billion in 2026, growing steadily across key end-use industries.

Growth is driven by rising personal care demand, increasing use in agrochemicals, and expanding green construction activities.

Asia Pacific leads the market with around 38% share due to strong manufacturing and growing end-use industries.

The healthcare sector offers strong opportunities driven by demand for high-purity, biocompatible silicone surfactants.

Leading companies include Dow Inc., Shin-Etsu Chemical Co., Ltd., Wacker Chemie AG, Evonik Industries AG, Momentive Performance Materials, Elkem ASA, BASF SE, etc.