- Electrical Equipment & Services

- Rice Milling Machine Market

Rice Milling Machine Market Size, Share, and Growth Forecast 2026 - 2033

Rice Milling Machine Market by Machine Type (Fully Automatic, Semi-Automatic, Manual), Technology (Conventional Milling, Smart/IoT-Enabled Milling, Energy-Efficient Milling Systems), Operation (Pre-cleaning, Separating, Grading, Rice Whitening, Other), Capacity (Small-scale below 10 tons/day, Medium-scale 10-50 tons/day, Large-scale above 50 tons/day), End-user (Commercial Mills, Farmers/Small Millers), and Regional Analysis for 2026 - 2033

Rice Milling Machine Market Size and Trend Analysis

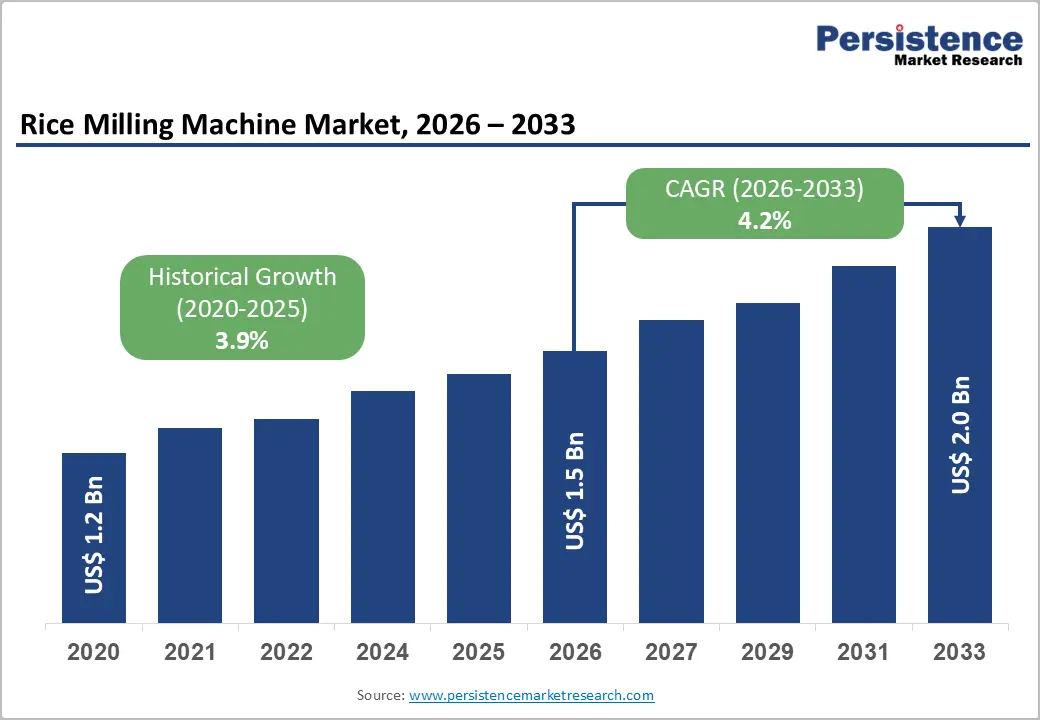

The global rice milling machine market is expected to be valued at US$ 1.5 billion in 2026 and is projected to reach US$ 2.0 billion by 2033, growing at a CAGR of 4.2% between 2026 and 2033. This growth is fundamentally driven by the increasing mechanization of rice processing across Asia Pacific's dominant rice-producing economies, escalating commercial milling capacity investments in South and Southeast Asia, and the progressive shift from manual paddy milling technology to automated milling systems that reduce labor dependency and improve milled rice quality and recovery rates.

The Food and Agriculture Organization of the United Nations (FAO) reports that rice is the staple food for more than half the world's population and over 500 million tonnes of paddy are produced globally each year a production scale that demands continuous investment in rice processing equipment and milling infrastructure upgrades to minimize post-harvest losses, which the FAO estimates at 10-15% of production in developing economies where mechanization remains incomplete.

Key Industry Highlights:

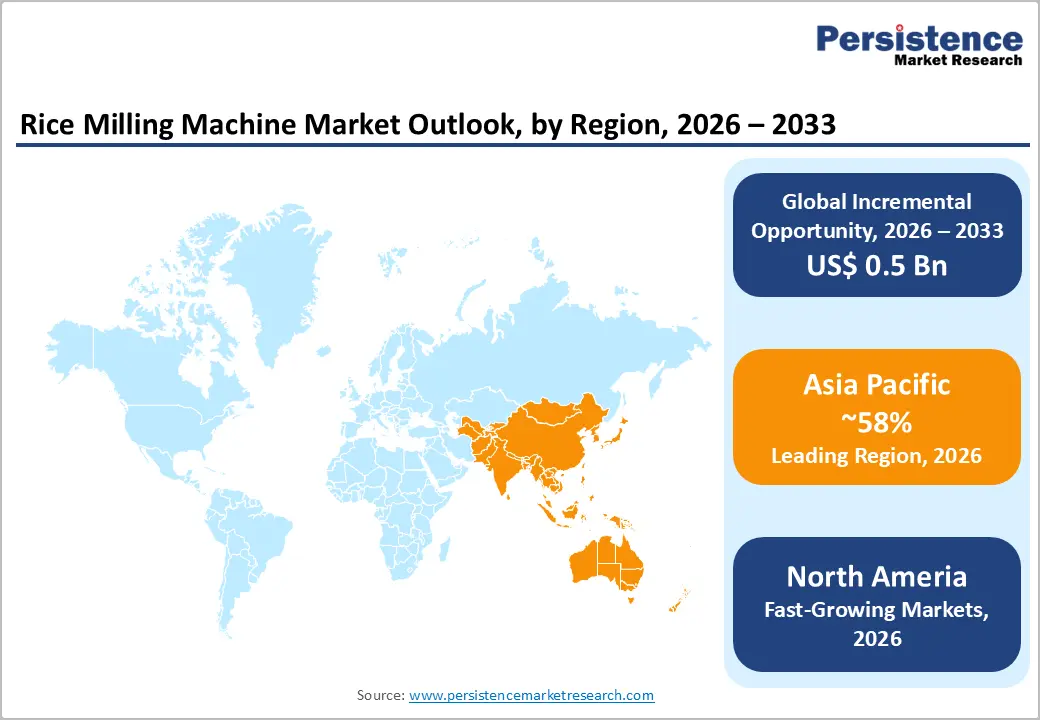

- Regional Dominance: Asia Pacific leads the global rice milling machine market with approximately 58% share in 2025, driven by massive paddy production, government mechanization programs, and rapid modernization across China, India, Vietnam, and Indonesia.

- Semi-Automatic Leadership: Semi-automatic rice milling machines are likely to register 43% share in 2026 due to their optimal cost-performance balance, delivering 5-8% higher rice recovery while remaining 30-40% cheaper than fully automatic systems.

- Automation Growth Surge: Fully automatic rice milling machines are the fast-growing machine segment, expanding at around 6.5% CAGR supported by China and India’s subsidy-driven smart agriculture and export-quality rice initiatives.

- Smart Milling Expansion: Smart/IoT-enabled milling systems are projected to grow at approximately 7.8% CAGR, generating 25% premium pricing alongside recurring software and connectivity revenue opportunities for manufacturers.

- Commercial Mills Dominance: Commercial mills nearly account for nearly 64% share in 2026, as professional operators prioritize throughput efficiency, export-grade rice quality, and energy savings, enabling premium equipment positioning and long-term maintenance contracts.

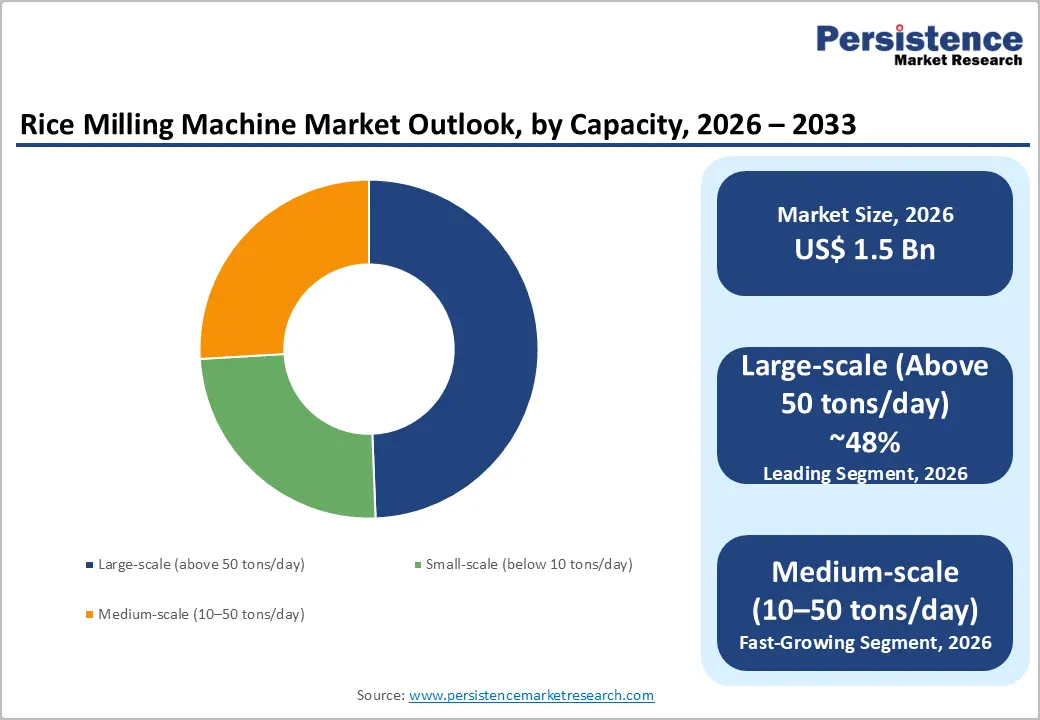

- Large Capacity Leadership: Large-scale mills above 50 tons/day dominate with approximately 48% revenue share in 2026, driven by industrial processing complexes where full integrated installations can reach USD 1-5 million per project.

- Government Subsidy Momentum: China’s agricultural mechanization subsidies exceeding CNY 200 billion and India’s SMAM mechanization programs are accelerating procurement of automated rice milling equipment, creating durable policy-backed replacement and upgrade cycles.

- Frontier Market Opportunity: Sub-Saharan Africa and South Asia represent major greenfield growth opportunities, supported by food security investments and mechanization programs targeting 50% post-harvest loss reduction and affordable mid-tier milling systems adoption.

- India-China Procurement Strength: China controls nearly 35% of Asia Pacific market share while India holds around 22%, together forming the world’s largest rice milling equipment procurement ecosystem with strong modernization-driven CAGR growth above 5.2%.

Market Dynamics

Driver - Rising Global Rice Consumption and Post-Harvest Loss Reduction Mandates Are Compelling Investment in Modern Rice Processing Equipment

The structural imperative for upgrading rice processing equipment globally is driven by the combination of rising rice consumption with the FAO projecting global milled rice demand to approach 520 million tonnes by 2030 and government-mandated post-harvest loss reduction programs across Asia's major paddy-producing nations. Modern rice milling machines equipped with multi-stage processing pre-cleaning, husking, whitening, and grading can achieve milled rice recovery rates of 68-72% from paddy input, compared with 60-65% achievable by manual and semi-mechanized traditional processing, delivering commercially significant yield improvements on high-volume commercial mill contracts.

India's National Food Security Mission and PM Kisan agricultural support programs have both funded rice milling equipment upgrades as explicit components of post-harvest loss reduction initiatives, and the ASEAN Food Security Framework has similarly identified rice processing equipment modernization as a priority investment across its member states. For suppliers of rice processing equipment, this combination of volume growth and policy-backed modernization investment creates a durable, government-reinforced demand cycle that extends well beyond typical capital equipment replacement cycles.

Agricultural Mechanization Programs and Government Subsidies Across Developing Asia Are Accelerating Smart Milling Technology Adoption

The accelerating adoption of automated milling systems and smart/IoT-enabled milling technology across Asia Pacific's developing rice economies represents the market's most consequential demand growth signal for equipment manufacturers targeting premium machine type segments. China's Ministry of Agriculture and Rural Affairs (MARA) reports that agricultural machinery mechanization rates in paddy cultivation and processing have risen consistently, with the government's 14th Five-Year Agricultural Plan (2021-2025) allocating over CNY 200 billion in agricultural mechanization subsidies a significant proportion directed at rice processing equipment including fully automatic milling systems with optical grain sorting and real-time quality monitoring.

India's Agricultural Mechanization Sub-Mission (SMAM) under the National Mission on Agricultural Mechanization has subsidized thousands of improved rice milling units across rice-growing states including West Bengal, Uttar Pradesh, and Andhra Pradesh, progressively shifting the installed base from manual paddy milling technology toward semi-automatic and fully automatic alternatives. Manufacturers who position smart/IoT-enabled milling platforms compatible with government subsidy qualification criteria in both China and India are best positioned to capture this policy-amplified demand cycle.

Restraints - High Capital Cost of Fully Automatic Systems Constrains Adoption Among Small-Scale Millers and Farming Communities in Price-Sensitive Markets

The capital intensity of fully automatic rice milling systems with commercial-scale installations requiring investments ranging from USD 50,000 to over USD 500,000 depending on throughput capacity and automation level creates a structural adoption barrier that restricts modern grain processing machinery penetration among the large population of small-scale and subsistence-level millers who represent the majority of installed milling units in South and Southeast Asia.

The Asian Development Bank (ADB) has documented that rural agricultural equipment financing remains severely constrained in low-income farming communities, with limited access to formal credit for capital equipment purchases deterring investment even when technology benefits are well understood by prospective buyers. This cost barrier directly suppresses the addressable market for premium milling equipment in the geographies with the highest volume of under-mechanized paddy processing, limiting revenue growth from the largest geographic demand pools.

Skilled Operator Shortage and Inadequate Rural Service Networks Constrain Operational Uptime and Deter Technology Adoption in Frontier Markets

The commercial viability of advanced rice milling systems in rural processing environments depends critically on access to trained operators and responsive maintenance service networks both of which are absent in many high-potential markets across Sub-Saharan Africa, Bangladesh, and Myanmar. Fully automatic and IoT-enabled milling platforms require operators capable of interpreting sensor diagnostics, performing preventive maintenance procedures, and managing software updates capabilities that exceed the technical training levels prevalent among rural millers in these geographies.

Equipment downtime from preventable mechanical failures caused by operator error or delayed servicing directly suppresses milling throughput and economic returns that create a negative adoption experience.

Opportunities - Smart/IoT-Enabled Milling Technology Offers Premium Positioning and Data-Driven Value Creation for Forward-Looking Manufacturers

The smart/IoT-enabled milling technology segment represents the highest-growth, highest-margin opportunity within the rice milling machine market for manufacturers willing to invest in sensor integration, connectivity platforms, and data analytics capabilities that convert milling operations from throughput-focused commodity services into quality-optimized, data-driven businesses. Modern IoT-integrated rice mills incorporate sensors for real-time paddy moisture monitoring, automated whiteness degree control, optical color sorting, and production efficiency dashboards capabilities that enable mill operators to document premium quality output required for export-grade milled rice markets.

Japan's Ministry of Agriculture, Forestry and Fisheries (MAFF) has specifically promoted smart agricultural machinery including IoT-connected rice processing equipment as a component of its Smart Food Chain initiative, and South Korea's Rural Development Administration (RDA) has funded pilot smart milling programs at cooperative processing facilities.

For agricultural processing equipment manufacturers, the smart milling segment commands 15-25% hardware price premiums over conventional equivalents and generates additional recurring software and connectivity subscription revenue making it the strategic priority for companies targeting above-market margin growth through the 2026 - 2033 forecast period.

Sub-Saharan Africa and South Asia's Underpenetrated Rice Processing Infrastructure Represents a Greenfield Growth Opportunity for Mid-Tier Equipment Suppliers

The long-term growth opportunity for rice milling machine manufacturers lies in Sub-Saharan Africa and South Asia's vast under-mechanized paddy processing capacity, where the combination of rising rice consumption, government food security investment, and low current milling mechanization rates creates an addressable market for mid-tier semi-automatic and small-scale milling equipment that is growing faster than either the established Asian markets or the premium smart milling segment.

The African Development Bank (AfDB) has identified rice value chain mechanization as a priority investment under its Feed Africa strategy, targeting a 50% reduction in post-harvest losses by 2025, and multiple national governments including Nigeria, Ghana, and Tanzania have launched subsidized rice milling equipment procurement programs aligned with domestic rice production expansion targets.

In South Asia, Bangladesh's Rice Processing Mechanization Programme and the government's target of achieving zero post-harvest loss by 2030 are generating procurement demand for affordable small-to-medium capacity milling equipment. Manufacturers who develop cost-optimized equipment variants compatible with government procurement specifications particularly in energy-efficient milling systems that reduce operating costs for electricity-constrained rural operators can establish first-mover market positions in rapidly growing frontier markets before competitive density increases materially.

Category-wise Analysis

Machine Type Insights

Semi-Automatic rice milling machines lead the machine type segment leading with approximately 43% share in 2026. Semi-automatic machines automate the core husking, whitening, and grading operations while retaining manual operator control at key process transitions a design compromise that reduces capital cost by 30-40% relative to fully automatic systems while delivering milled rice recovery improvements of 5-8 percentage points over manual processing.

The International Rice Research Institute (IRRI) has documented that semi-automatic multi-stage mills have become the standard technology for community-level rice processing in the Philippines, Vietnam, and Bangladesh, displacing single-pass manual hullers progressively as mechanization programs expand. The durable installed base of semi-automatic equipment in Asia's hundreds of thousands of rural and peri-urban rice mills generates consistent replacement demand that sustains the segment's market share leadership through normal equipment lifecycle replacement cycles.

Fully automatic is the fast-growing machine type projected to expand at approximately 6.5% CAGR significantly above the market-wide forecast. Government subsidies in China and India, the growth of large-scale commercial rice processing enterprises seeking to reduce labor costs, and the adoption of automated milling systems for export-grade rice production are collectively driving above-market growth in fully automatic machine procurement, representing the premium expansion frontier for equipment manufacturers targeting value-over-volume growth strategies.

Technology Insights

Conventional milling technology leads the technology segment with approximately 61% market share in 2026, underpinned by its entrenched position as the standard processing technology across the hundreds of thousands of existing rice mill installations in Asia Pacific and Africa each representing a long-duration asset that generates replacement part and service demand rather than new system investment. Conventional milling systems are well received by operators and maintenance technicians across all major rice-producing geographies. It is also supported by extensive third-party spare parts networks and local service infrastructure that IoT-enabled and energy-efficient alternatives.

The FAO's post-harvest management surveys consistently identify conventional multi-stage hulling and whitening equipment as the dominant paddy milling technology in commercial-scale mills across Southeast Asia and South Asia, with only the highest-tier export-oriented facilities having transitioned to sensor-integrated smart alternatives. The large installed base of conventional equipment also generates consistent consumable demand for rubber rolls, abrasive whitening stones, and screen sieves creating recurring revenue streams for manufacturers with established aftermarket parts supply networks.

Smart/IoT-enabled milling systems are the fast-growing technology segment, projected to expand at approximately 7.8% CAGR through 2033, driven by government smart agriculture programs in Japan and South Korea, export-grade rice quality certification requirements, and the progressive cost reduction of IoT sensor and connectivity components that is bringing smart milling economics within reach of mid-scale commercial mills.

Operation Insights

Rice whitening is likely to lead the operation segment with approximately 32% share in 2026, occupying the highest-value processing stage in a rice milling line where machine performance directly determines the commercial grade and price premium achievable for finished milled rice. Whitening machines encompassing both abrasive and friction-type whiteners remove the bran layer from husked brown rice to produce white rice conforming to the specified degree of milling (DOM) standards required by domestic and export grade specifications.

The Codex Alimentarius Commission standard for milled rice (Codex Stan 198-1995) and national procurement standards, including the Food Corporation of India's (FCI) specifications for rice procurement, specify whitening uniformity parameters that can only be reliably met with precision whitening equipment capable of consistent pressure and rotational speed control. Equipment manufacturers who provide integrated whitening systems with adjustable whiteness monitoring calibrated to export market standards command premium pricing from commercial mills targeting high-value export markets in the Middle East, Africa, and Europe.

Grading is the fastest-growing operation segment, expanding at approximately 5.8% CAGR through 2033, as export-grade quality requirements and consumer premium for visually uniform, broken-grain-free milled rice are elevating demand for optical and weight-based grain sorting and grading systems that previously were deployed only in the most sophisticated commercial milling facilities.

Capacity Insights

Large-scale (above 50 tons/day) capacity mills lead the market with approximately 48% revenue share in 2025, driven by the concentration of commercial rice milling investment in high-throughput industrial facilities that serve regional and export markets and generate the largest per-contract equipment procurement values. Large-scale integrated rice milling complexes encompassing intake systems, pre-cleaners, multi-stage hullers, whiteners, optical sorters, and packaging lines represent the highest-value equipment procurement events in the market, with full greenfield installations for facilities above 100 tons/day capacity reaching USD 1-5 million in total equipment value.

The National Cooperative Development Corporation (NCDC) in India and large agri-business conglomerates including India's KRBL Limited and Thailand's CP Group operate integrated large-scale milling complexes that represent reference procurement accounts generating multi-year equipment supply, upgrade, and maintenance revenue for qualified rice processing equipment manufacturers.

Medium-scale (10-50 tons/day) is the fastest-growing capacity segment at approximately 5.3% CAGR through 2033, as government programs in India, Bangladesh, and Sub-Saharan Africa direct mechanization subsidies toward this capacity tier, large enough to serve commercial market supply chains, yet accessible to cooperative and agri-entrepreneur investment levels in rapidly developing rice economy markets.

End-user Insights

Commercial mills are likely to lead the end-use segment with approximately 64% market share in 2026, reflecting the concentration of rice milling investment in professionally operated commercial facilities that purchase the highest-value equipment configurations, maintain consistent replacement and upgrade procurement cycles, and represent the most commercially accessible customer segment for equipment manufacturers and distributors.

Commercial mills ranging from regional custom milling services to export-oriented large-scale processing complexes make purchasing decisions based on throughput capacity, milled rice quality metrics, energy efficiency, and total cost of ownership rather than on initial capital cost alone, enabling premium product positioning and solution-based selling approaches that generate higher average selling prices per transaction. The Rice Millers' Association of the Philippines (RMA-P) and equivalent industry bodies across Vietnam, Thailand, and Bangladesh represent organized commercial mill constituencies that serve as influential reference customer channels through which equipment manufacturers can establish product credibility and generate referral-based sales pipelines.

Farmers/Small Millers are the fastest-growing end-use segment at approximately 5.1% CAGR through 2033, as government subsidized village-level and cooperative milling programs across India, Africa, and Southeast Asia extend mechanized processing access to farming communities that previously relied on manual or contract milling services, creating new first-time equipment buyer demand in the small-scale capacity tier.

Regional Insights

North America Rice Milling Machine Market Trends

North America is driven by the United States' domestic rice production in the Mississippi Delta, Arkansas, California, and Louisiana, which collectively produce approximately 9-10 million tonnes of rough rice annually according to the USDA National Agricultural Statistics Service (NASS). U.S. commercial rice millers operate among the world's most technologically advanced milling facilities, incorporating optical color sorters, computerized whiteness control, and near-infrared moisture analyzers as standard equipment, creating demand for premium, precision agricultural processing equipment rather than volume-tier commodity machinery.

The North American market is consolidating around large integrated milling complexes operated by companies including Riviana Foods and American Rice, which are progressively investing in energy-efficient milling systems and digital monitoring platforms to reduce energy costs and meet food safety documentation requirements under FDA Food Safety Modernization Act (FSMA) regulations. The region's emphasis on specialty and organic rice premium segments including jasmine, basmati, and arborio varieties creates demand for precision milling configurations that preserve grain integrity during processing.

- U.S. Rice Milling Machines: Premium Automated Systems for High-Value Rice

The United States accounts for approximately 78% of the North American rice milling machine market and holds a distinctive position as the world's most automation-intensive rice milling geography where equipment procurement decisions are driven by FDA compliance, labor cost reduction, and premium grain variety quality preservation rather than basic mechanization needs. U.S. commercial mills operate at large scale, with individual mill capacities frequently exceeding 100-200 tons/day, making per-installation equipment values significantly higher than Asian market equivalents.

Also, its growth is concentrated in retrofits upgrading existing mills with IoT monitoring and energy-efficient systems rather than new greenfield construction. The USDA's Rural Development loan guarantee programs for food processing facilities support ongoing equipment upgrade investment.

Europe Rice Milling Machine Market Trends

Europe is a niche but growing market for rice milling machines, driven primarily by Italy's world-class rice production in the Po Valley which the Italian Rice Board (Ente Nazionale Risi) reports produces approximately 1.5 million tonnes of paddy annually, making Italy the EU's largest rice producer and by Spain's active Valencian rice cultivation supporting domestic milling operations. European rice millers operate under strict EU Food Information Regulation (EU 1169/2011) documentation requirements that incentivize adoption of automated processing control and traceability systems compatible with premium milling equipment.

Germany, France, and the UK are primarily import markets for milled rice rather than paddy processing geographies, but they represent significant procurement channels for specialty grain processing equipment used in food ingredient processing and value-added rice product manufacturing. The broader European agricultural machinery market is subject to progressive electrification and energy efficiency requirements under the EU Green Deal's Farm to Fork Strategy, which is influencing procurement preferences toward energy-efficient milling systems across the continent's food processing equipment purchasing community.

Germany accounts for approximately 18% of the European rice milling machine market, leveraging its status as Europe's leading food processing equipment engineering hub. While Germany does not produce paddy rice domestically, its machinery manufacturers including specialized grain processing machinery companies export globally and drive domestic revenue through grain processing equipment sales for the broader cereal and specialty food ingredient sectors. Germany's strong engineering base positions it as a supplier of premium milling components and integrated automation systems used in high-specification European and export market rice milling installations. CAGR for Germany's segment is estimated at approximately 3.2% through 2033.

- U.K.: Import-Driven Specialty Rice Processing and Smart Milling Adoption

The United Kingdom represents approximately 14% of the European rice milling machine market, with demand concentrated in specialty and ethnic food ingredient processing sectors where mills operate on imported rough rice. The UK's large South Asian diaspora consumer market creates commercial demand for premium-milled basmati and long-grain rice varieties, supporting investment in precision whitening and optical sorting equipment at specialty rice import processors. Post-Brexit food safety regulatory alignment under the Food Standards Agency (FSA) continues to drive traceability system investments in UK rice processing operations.

- France: Artisan and Specialty Rice Processing with Regulatory Compliance Focus

France accounts for approximately 11% of the European market, with its small Camargue region paddy production supporting a premium specialty rice processing sector. France's Institut National de l'Origine et de la Qualité (INAO) protected geographic indication status for Camargue rice incentivizes investment in precision milling equipment that preserves grain quality required for premium GI certification. French rice processing equipment procurement is also influenced by the EU's Common Agricultural Policy (CAP) modernization funding that supports food processing equipment upgrades for GI-certified producers.

- Italy: EU's Largest Rice Producer Driving Premium Milling Equipment Demand

Italy holds the largest share of the European rice milling machine market at approximately 28%, anchored by the Po Valley's world-class risotto and arborio rice production and the country's export-oriented milled rice industry. Italian commercial rice millers, including Riso Gallo and Acquerello, operate high-value specialty milling lines requiring precision whitening and aging equipment that commands premium technology pricing. Italy's rice processing sector is progressively investing in energy-efficient milling systems and smart process control under Italy's National Recovery and Resilience Plan (NRRP) agri-food innovation funding.

Asia Pacific Rice Milling Machine Market Trends

Asia Pacific is the dominant regional rice milling machine market with approximately 58% global market share in 2026, anchored by the world's largest paddy production volumes in China, India, Indonesia, and Vietnam, collectively accounting for the majority of global rice production per FAO data. The region is undergoing a structural transition from predominantly manual and semi-mechanized paddy milling technology toward semi-automatic and fully automatic rice processing equipment, driven by government mechanization programs, rising rural labor costs, and the growing export aspirations of national rice industries that require certified premium milled rice quality.

China is the region's largest single machine market, with its commercial rice processing sector consolidating around large automated facilities that increasingly deploy IoT-enabled monitoring systems aligned with the government's smart agriculture priorities under the 14th Five-Year Agricultural Plan. Southeast Asian markets including Vietnam, Thailand, and Indonesia are active growth markets for medium-capacity commercial milling equipment as export rice value chain competitiveness becomes a national policy priority.

- China: World's Largest Automated Rice Milling Systems Procurement Hub

China holds approximately 35% of the Asia Pacific rice milling machine market, representing the world's single largest national procurement market for commercial rice processing equipment. China's MARA mechanization subsidy programs, consolidated large-scale milling enterprise development, and the country's ambition to minimize food loss under national food security policy collectively sustain high and growing annual equipment procurement volumes.

China's domestic manufacturers including Zhejiang QiLi Machinery compete alongside international suppliers in the medium-to-high capacity commercial mill segment. The country's segment is estimated to grow at approximately 4.8% CAGR through 2033, above the regional average, driven by smart milling technology adoption.

- India: Massive Installed Base Renewal and Government Subsidy-Driven Mechanization

India holds approximately 22% of the Asia Pacific rice milling machine market, representing the world's largest number of individual rice milling units estimated at over 500,000 operational rice mills of varying scales by India's Ministry of Food Processing Industries (MoFPI). India's market is growing and driven by SMAM subsidy programs, PMFME scheme investment in small-scale food processing, and the large-scale commercial milling sector's modernization to meet export-grade quality standards for milled rice destined for Middle Eastern and African export markets. The transition from single-pass hullers to multi-stage milling systems across India's tier-2 and tier-3 city milling hubs represents the market's largest volume-growth opportunity.

- South Korea: Technology-Led Smart Milling and Precision Quality Control Systems

South Korea accounts for approximately 8% of the Asia Pacific rice milling machine market, operating the world's most technologically advanced per-capita rice milling infrastructure relative to paddy production volume. South Korea's Rural Development Administration (RDA) has systematically promoted smart rice processing equipment with IoT quality monitoring across agricultural cooperative milling facilities, and South Korean manufacturers are global leaders in precision optical grain sorting technology.

South Korea's market grows at approximately 5.5% CAGR through 2033, with growth concentrated in smart milling system upgrades at cooperative processing centers aligned with the country's premium domestic rice market quality requirements.

Competitive Landscape

The global rice milling machine market is moderately fragmented, with a mix of large Asian conglomerates, specialized grain processing machinery companies, and regional manufacturers competing across capacity and technology tiers. Bühler Group (Switzerland), Satake Corporation (Japan), and AGI (AGCO) lead through broad product portfolios spanning full milling line integration, after-sales service networks, and established OEM relationships with commercial mill operators in key export rice economies.

Chinese manufacturers, including Zhejiang QiLi Machinery and Hubei Yongxiang, are intensifying competition in the mid-tier semi-automatic and medium-capacity segments through competitive pricing and government-aligned subsidy qualification. Strategic themes among leaders include IoT platform development for smart milling, energy-efficient drive system integration, and expanded service network investment in South Asian and African growth markets. The market rewards technical service capability and spare parts supply chain depth differentiators that protect established players from pure price competition.

Key Developments:

- April 2026: Satake Corporation launched its new SSW80A mid-capacity rice mill designed for medium-scale millers, offering improved grain yield, enhanced milling efficiency, and lower energy consumption to address the growing global demand for efficient rice processing solutions.

- October 2025: Straw Innovations introduced the “Straw Traktor,” an advanced rice farming machine aimed at improving food security and reducing agricultural emissions. The machine can increase rice yields by up to 65%, enable three harvest cycles annually, and reduce methane emissions by nearly half. The company also expanded its presence across the Philippines, Indonesia, and India.

- March 2025: Satake Corporation launched the RGBA Optical Sorter Series featuring AI-powered defect detection technology for milled rice grading. The system achieved 99.9% sorting accuracy during commercial trials in Vietnam and Thailand, supporting premium export-grade rice quality standards.

- October 2024: Bühler Group integrated its SmartMill digital platform with IoT-enabled rice milling equipment, allowing real-time remote monitoring of key operational parameters such as moisture levels, whiteness, and processing throughput for mill operators across India and Southeast Asia.

- June 2024: Zhejiang QiLi Machinery expanded its export distribution network into Sub-Saharan Africa through new distributor partnerships in Nigeria and Ghana, supporting the deployment of subsidized rice milling equipment under the African Development Bank’s Feed Africa programme.

Companies Covered in Rice Milling Machine Market

- Zhejiang QiLi Machinery Co. Ltd.

- Bühler Group

- Satake Corporation

- Hubei Yongxiang Food Machinery Co. Ltd.

- AGCO Corporation (AGI)

- Fotma Machinery Co. Ltd.

- TW Grandeur Machinery Co. Ltd.

- Milltec Machinery Ltd.

- Matsumoto Machinery

- Lianyungang Huantai Machinery Co. Ltd.

- YANMAR Holdings Co. Ltd.

- Wuhan Zhongliang Grain Machinery Co. Ltd.

Frequently Asked Questions

The global rice milling machine market is valued at approximately US$ 1.5 billion in 2026, growing from US$ 1.2 billion in 2020 at a historical CAGR of 3.9% (2020-2025). The market is projected to reach US$ 2.0 billion by 2033, expanding at a CAGR of 4.2% representing US$ 0.5 billion in incremental opportunity driven by agricultural mechanization programs, post-harvest loss reduction mandates, and smart milling technology adoption.

The primary demand drivers are government agricultural mechanization subsidies including China's MARA 14th Five-Year Plan allocating over CNY 200 billion in agricultural machinery support and India's SMAM scheme combined with the FAO's documentation of 10-15% post-harvest losses in under-mechanized markets creating policy imperatives for rice processing equipment modernization, and rising export-grade quality standards for milled rice in Middle Eastern and African import markets that incentivize commercial mill upgrades.

Semi-Automatic rice milling machines lead the market with approximately 43% market share in 2025. The segment's leadership reflects its optimal cost-performance positioning for Asia Pacific's large commercial mill operator segment delivering 5-8 percentage point milled rice recovery improvements over manual processing at 30-40% lower capital cost than fully automatic systems, as documented by the International Rice Research Institute (IRRI) field studies across Southeast and South Asian markets.

Asia Pacific leads the global rice milling machine market with approximately 58% market share in 2025. China is the dominant country within the region, holding approximately 35% of Asia Pacific market revenue, supported by the world's largest subsidized agricultural mechanization program under the Ministry of Agriculture and Rural Affairs (MARA), India's massive installed base of over 500,000 operational rice mills per MoFPI data, and Southeast Asia's growing export-grade commercial milling sector.

The Sub-Saharan Africa and South Asia's underpenetrated mechanization market, where the African Development Bank's Feed Africa strategy targets a 50% reduction in post-harvest losses through rice processing equipment investment creating government-procurement-backed demand for affordable, energy-efficient semi-automatic and small-to-medium capacity rice milling equipment among first-time mechanized milling adopters in Nigeria, Ghana, Tanzania, and Bangladesh.

The leading companies in the global rice milling machine market include Bühler Group, Satake Corporation, Zhejiang QiLi Machinery, Milltec Machinery Ltd., AGCO Corporation (AGI), YANMAR Holdings Co., Ltd., Fotma Machinery, Hubei Yongxiang Food Machinery, and TW Grandeur Machinery. Market leaders differentiate through integrated rice processing equipment portfolios spanning full milling lines, IoT smart monitoring platforms, global after-sales service networks, and compliance with government subsidy qualification standards in key procurement markets.