- Metals & Minerals

- Recycled Metals Market

Recycled Metals Market Size, Share, and Growth Forecast 2026 - 2033

Recycled Metals Market by Metal Type (Ferrous Metals: Steel, Iron; Non-ferrous Metals: Aluminum, Copper, Zinc, Others; Precious Metals: Gold, Silver, Platinum; Rare Earth Metals: Light Rare Earth Metals, Heavy Rare Earth Metals), Scrap Source (Industrial Manufacturing Waste, Old Scrap), Industry, and Regional Analysis, 2026 - 2033

Recycled Metals Market Size and Trend Analysis

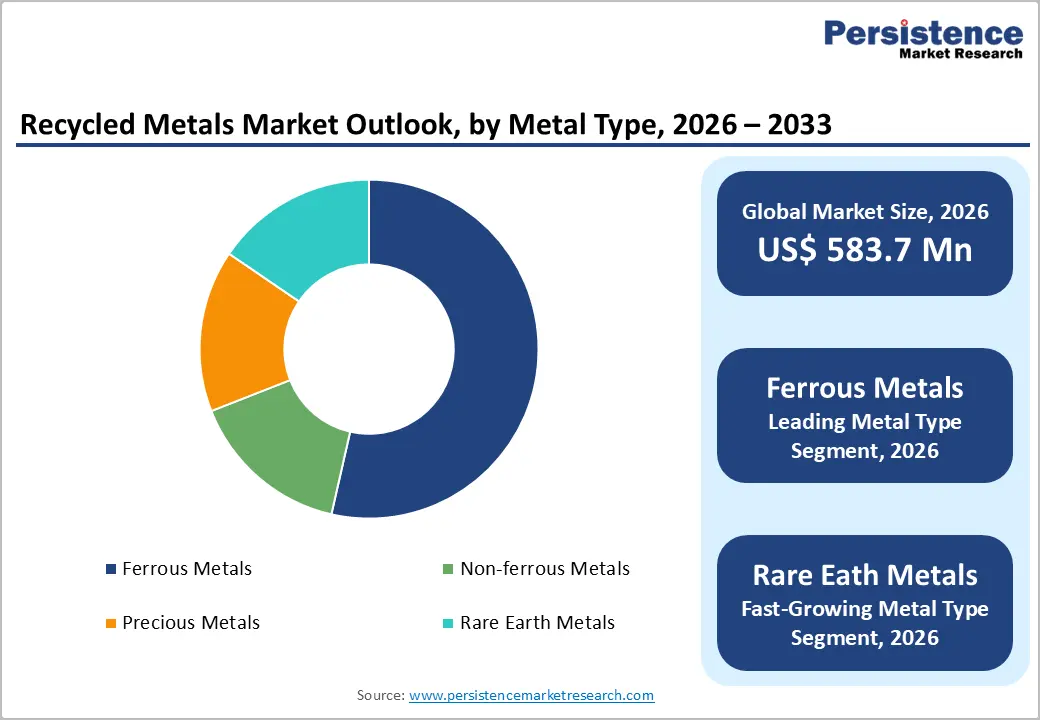

The global recycled metals market size is expected to be valued at US$ 583.7 million in 2026 and projected to reach US$ 937.3 million by 2033, growing at a CAGR of 7.0% between 2026 and 2033. This sustained growth is anchored in the convergence of tightening global circular economy legislation, surging demand for low-carbon-intensity metals from EV and renewable energy manufacturers, and volatile primary metal prices that make recycled feedstock economically compelling for manufacturers seeking cost-stable raw material supply chains.

The United Nations Environment Programme (UNEP) estimates that recycling metals consumes 2-10% of the energy required for virgin primary metal production, an efficiency advantage that is becoming a strategic imperative as carbon border adjustment mechanisms and industrial decarbonization mandates progressively penalize primary metal use in regulated markets.

Key Industry Highlights:

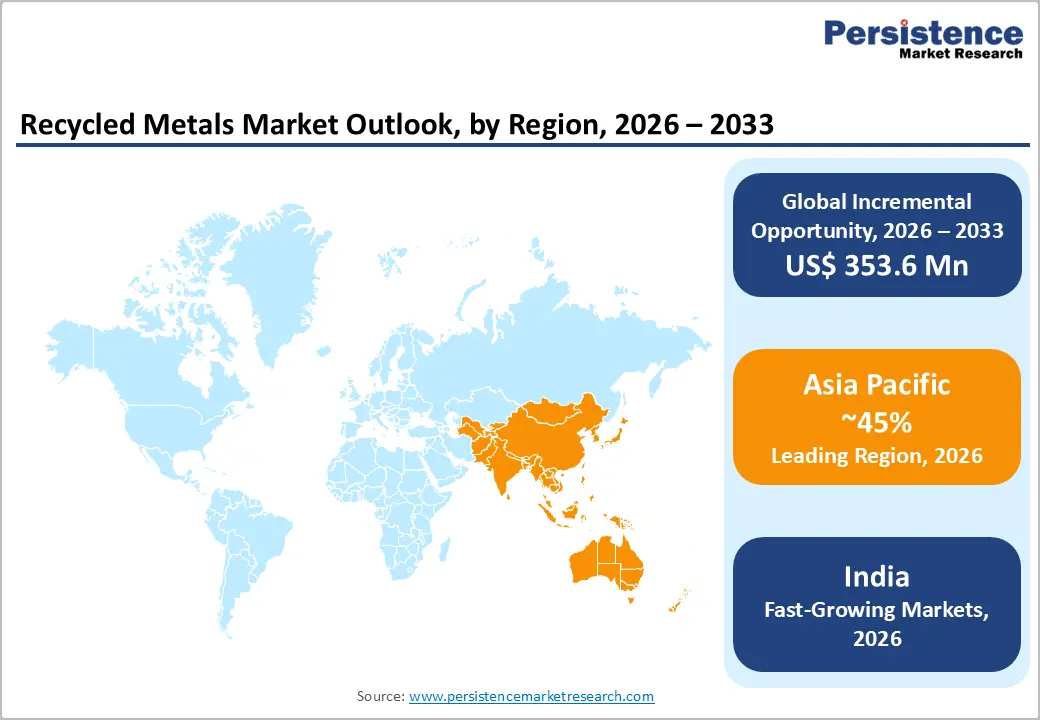

- Leading Region: Asia Pacific commands the largest global share of the recycled metals market at approximately 45% revenue share in 2025, anchored by China's dominant EAF steel production base and Japan and South Korea's world-class non-ferrous and e-waste precious metal recycling infrastructure.

- Fastest Growing Region: India is projected to grow at approximately 8.2% CAGR through 2033, the highest national growth rate globally, driven by the National Steel Policy's 300 Mt capacity target and the NIP's infrastructure investment mandating recycled metal-intensive construction material procurement.

- Dominant Metal Type: Ferrous metals lead with approximately 58% metal type market share in 2025, entrenched by the EAF steelmaking model's structural scrap dependency, with the World Steel Association documenting 630 million tonnes of global annual steel scrap recycling, and EAF's growing share of global steel production.

- Fast-Growing Metal Type: Rare earth metal recycling is the fastest-growing category, propelled by USGS data showing 85%+ Chinese supply concentration in primary rare earths, the EU's CRMA 15% recycled content target by 2030, and IRA incentives for domestic rare earth processing capacity development.

- Key Opportunity: Rare earth recyclers with CRMA and IRA-compliant processing capability, targeting EV motor magnet neodymium and dysprosium, represent the market's highest-margin, most policy-backed growth position, with first-mover certification advantages impossible to replicate quickly once supply agreements with EV OEMs are secured.

Market Dynamics

Drivers - Circular Economy Legislation and Carbon Border Adjustment Mechanisms Are Structurally Compelling Industrial Buyers to Prioritize Recycled Metal Feedstock

For recycled metals market participants, the most consequential structural signal is that regulatory frameworks in the EU, UK, and progressively in North America are converting environmental preference for recycled metals into enforceable procurement obligations, fundamentally changing the economics of scrap metal sourcing. The European Union's Carbon Border Adjustment Mechanism (CBAM), phased in from 2026, imposes carbon costs on imports of primary steel, aluminum, and other metals from high-emission geographies, directly improving the cost competitiveness of domestically recycled alternatives that carry significantly lower embedded carbon.

The EU's Circular Economy Action Plan sets binding recycled content targets for construction materials and packaging that will create codified demand for certified recycled metal inputs, a procurement shift that recyclers with verified chain-of-custody documentation and low Scope 1 and 2 emission profiles are positioned to exploit at premium pricing. Recyclers who invest in carbon accounting infrastructure and third-party emission verification now will establish competitive certification advantages that late movers cannot easily replicate once regulatory timelines compress.

Electric Vehicle and Renewable Energy Manufacturing Are Creating Compounding Demand for Recycled Aluminum, Copper, and Rare Earth Metals

The global transition to electric vehicles and renewable energy infrastructure is creating a structural demand acceleration for specific recycled metals that no primary supply expansion can match in pace or cost-competitiveness, and this dynamic rewards established recyclers with the sorting, processing, and certified purity capabilities required for EV and energy sector specifications. The International Energy Agency (IEA) reported that global EV sales exceeded 14 million units in 2023, with each BEV containing approximately 80 kg of aluminum and 83 kg of copper, metals for which recycled content commands a growing cost and carbon premium advantage over primary production.

The IEA's Critical Minerals Outlook identifies recycled rare earth metals as a strategic priority for reducing dependence on primary production concentrated in China, creating government-backed incentive programs in the U.S. under the Inflation Reduction Act (IRA) and in the EU under the Critical Raw Materials Act (CRMA) that directly expand the addressable market for rare earth metal recyclers with qualified processing capabilities.

Restraints - Scrap Metal Quality Variability and Contamination Suppress Premium Pricing Potential and Create Technical Barriers in High-Specification End Markets

Mixed-composition and contaminated scrap streams, a structural characteristic of old scrap sourced from end-of-life consumer goods and demolition waste, impose significant processing cost and quality uncertainty that constrains recycled metals' penetration in premium end markets requiring tight alloy specifications.

The European Aluminium trade association has documented that contaminated scrap streams require additional sorting and refining steps that increase processing costs by 15-30% relative to clean industrial manufacturing waste, a cost burden that erodes the economic advantage of recycled feedstock in price-competitive markets. For recyclers targeting automotive and electronics manufacturers who specify tight alloy grade tolerances, inconsistent input scrap quality creates yield variability that undermines supply contract reliability and prevents the establishment of the certified-quality commercial relationships that command sustained margin premiums.

Geopolitical Trade Restrictions on Scrap Metal Exports Create Supply Chain Volatility and Regional Market Imbalances

National scrap export restrictions, increasingly deployed by major scrap-generating economies including Turkey, India, and China as industrial policy tools, create supply chain fragmentation that suppresses the efficiency of global scrap metal recycling markets and creates regional feedstock price spikes that compress processing margins.

The Bureau of International Recycling (BIR) has documented multiple instances of government-imposed scrap export restrictions in recent years that disconnected domestic recyclers from their established export customer relationships, forcing abrupt reorientation of scrap volumes and creating significant short-term margin compression. For international recyclers and metal manufacturers dependent on cross-border scrap trade flows, the escalating geopolitical use of export controls constitutes a supply chain risk that is difficult to hedge and materially elevates the cost and complexity of long-term procurement strategy.

Opportunities - Rare Earth Metal Recycling Represents the Highest-Value, Most Policy-Backed Growth Opportunity Across the Entire Recycled Metals Market

Rare earth metal recycling is the fastest-growing and most strategically consequential segment within the recycled metals market, driven by the intersection of supply security policy, EV motor and wind turbine magnet demand, and near-zero secondary supply infrastructure that makes first-mover recycling capability an extraordinarily durable competitive advantage.

The U.S. Department of Energy (DOE) has identified neodymium, dysprosium, and other heavy rare earth metals as critical materials with severe supply concentration risk, over 85% of global rare earth processing remains controlled by China per U.S. Geological Survey (USGS) data, driving the IRA to direct hundreds of millions of dollars toward domestic rare earth recycling capacity development.

EU's Critical Raw Materials Act (CRMA) sets a binding target that at least 15% of the EU's annual consumption of strategic raw materials must be met through recycled sources by 2030, a codified demand signal that justifies investment in rare earth recycling infrastructure now. Companies, including Umicore and Dowa Holdings, that have invested in rare earth separation and recycling technology are positioned to capture the premium pricing and long-term supply agreements that EV motor manufacturers will compete to secure from qualified rare earth recyclers.

Industrial Manufacturing Waste Scrap Streams Offer Superior Economics and Quality Consistency

Industrial manufacturing waste, comprising clean, mono-material scrap generated at automotive stamping plants, aluminum die casters, and electronics assembly facilities, represents the highest-quality, most processable input stream available to recycled metals producers, and the recyclers who secure long-term manufacturing waste supply agreements today are establishing feedstock advantages that materially differentiate their product quality and cost position from old scrap-dependent competitors.

The World Steel Association documents that industrial scrap recycling rates in advanced manufacturing economies exceed 90% for ferrous metals, rates that demonstrate both the economic value of clean industrial scrap and the structural loyalty that manufacturing facilities show toward their scrap processors when service quality and logistics reliability are maintained consistently.

Automotive OEMs operating closed-loop aluminum programs, including Novelis' partnerships with BMW and Ford, are establishing precedents for long-term tolling and closed-loop recycling arrangements that lock in both scrap supply and recycled metal offtake, a commercial model that delivers the most durable margin protection in the recycled metals value chain. Recyclers who invest in on-site scrap logistics infrastructure at major manufacturing facilities and demonstrate alloy-specific sorting capability are best positioned to establish these high-value, competitively insulated manufacturing waste supply relationships.

Category-wise Analysis

Metal Type Insights

Ferrous metals (steel and iron) lead the metal type segment with approximately 59% share in 2026, a position anchored in steel's status as the world's most recycled material by volume, the World Steel Association reports that the global steel industry recycles approximately 630 million tonnes of steel scrap annually, and the electric arc furnace (EAF) steelmaking model's structural dependence on scrap as its primary raw material input.

The EAF route, which uses 100% scrap as feedstock, now accounts for over 29% of global crude steel production per World Steel Association data, and its share is expanding in North America (where EAF already exceeds 70% of production), Europe, and progressively in Asia as decarbonization mandates make blast furnace operations economically uncompetitive. Ferrous metals' market leadership is durable because it is structurally embedded in EAF capacity investment cycles, each new EAF minimill creates decades of assured scrap demand, rather than dependent on fluctuating consumer preference.

Scrap Source Insights

Industrial manufacturing waste scrap leads the scrap source segment with approximately 55% market share in 2026, reflecting its decisive quality, logistics, and processing cost advantages over old scrap collected from post-consumer end-of-life streams.

Industrial manufacturing waste is generated at consistent volumes, predictable alloy compositions, and low contamination levels at manufacturing facilities that are typically anchored to long-term production programs, characteristics that enable recyclers to optimize processing yields, minimize sorting investment, and reliably deliver certified alloy specifications to demanding end markets.

The European Aluminium association documents that industrial manufacturing scrap achieves recovery rates of 95%+ versus 60-70% for post-consumer old scrap, a yield differential that directly translates into superior recycler economics per tonne processed. Old Scrap's growth rate is faster, however, as expanding ELV regulations and extended producer responsibility frameworks formalize post-consumer scrap collection in emerging markets.

Industry Insights

Construction & Infrastructure leads the Industry segment with approximately 35% market share in 2025, reflecting the construction sector's position as the largest single consumer of recycled steel rebar, structural sections, and aluminum profiles globally, volumes sustained by the physical scale of global infrastructure investment that dwarfs the consumption intensity of any other single application sector.

The Global Infrastructure Hub estimates that the world needs USD 94 trillion in infrastructure investment by 2040, with a significant proportion of this steel and aluminum intensive, creating demand for recycled metal that extends well beyond the forecast period.

Recycled steel rebar and sections from EAF minimills are cost-competitive with or cheaper than virgin primary alternatives in most regional markets, creating a natural commercial floor beneath construction sector recycled metal demand that sustains the segment's volume leadership regardless of short-term commodity price cycles.

Energy & Renewables is the fastest-growing end-use segment, driven by solar panel aluminum frame, wind turbine copper wiring, and EV charging infrastructure steel demand that carries growing recycled content expectations from public procurement specifications.

Regional Insights

North America Recycled Metals Market Trends and Insights

North America is a mature and technologically advanced recycled metals market, where the electric arc furnace steelmaking model's dominance, EAF accounts for over 70% of U.S. steel production per the American Iron and Steel Institute (AISI), creates the world's most scrap-intensive major steel industry and sustains the region's position as both the largest per-capita scrap generator and the most sophisticated scrap processing market globally.

The IRA's domestic content incentives and critical minerals provisions are generating renewed investment in rare earth and specialty metal recycling capacity, positioning North America for above-market growth in the highest-value recycled metal categories through the forecast period.

U.S. Recycled Metals Market Size

The United States commands approximately 80% of the North American recycled metals market, driven by the world's largest EAF steel production base, with companies including Nucor Corporation and Steel Dynamics operating over 50 EAF minimills across the country. U.S. recycled metals demand grows at approximately 6.8% CAGR through 2033, supported by IRA domestic content requirements for EV and renewable energy projects that are embedding recycled metal specifications into federal procurement frameworks and creating structured demand visibility for domestic recyclers.

Europe Recycled Metals Market Trends and Insights

Europe is the world's most regulatory-driven recycled metals market, where the EU's CBAM, Circular Economy Action Plan, and Critical Raw Materials Act are collectively constructing the most comprehensive policy architecture for recycled metal demand creation globally.

The region's existing recycling infrastructure, anchored by companies including Aurubis AG, European Metal Recycling (EMR), and Remondis, provides a competitive advantage in certified recycled metal supply that the CBAM will amplify by penalizing high-carbon primary imports. Europe is heading toward mandatory recycled content thresholds in construction, packaging, and automotive applications that will structurally elevate recycled metal premiums relative to primary alternatives.

Germany Recycled Metals Market Size

Germany holds approximately 23% of the European recycled metals market, anchored by its world-class automotive and industrial manufacturing base that generates the continent's highest volumes of high-quality industrial manufacturing waste scrap. Aurubis AG, headquartered in Hamburg, is one of the world's largest copper recyclers, processing complex copper scrap from European electronic waste streams. Germany's recycled metals segment grows at approximately 7.1% CAGR through 2033, driven by CBAM compliance demand and the country's Energiewende renewable energy buildout, creating copper and aluminum recycled metal consumption.

U.K. Recycled Metals Market Size

The United Kingdom accounts for approximately 14% of the European recycled metals market, with demand underpinned by the UK's large EAF steel sector, where Liberty Steel and British Steel EAF operations are the primary scrap consumers, and European Metal Recycling (EMR)'s dominant domestic scrap collection and processing position. The UK's Net Zero commitment and planned transition to a circular economy under the Resources and Waste Strategy are structurally expanding recycled metal demand. The UK market grows at approximately 6.9% CAGR through 2033.

France Recycled Metals Market Size

France represents approximately 12% of the European recycled metals market, with demand driven by its large automotive manufacturing sector, Stellantis and Renault operations generating significant high-quality industrial manufacturing waste aluminum and steel, and by France's progressive Loi anti-gaspillage pour une économie circulaire (AGEC) law mandating recycled content in public procurement. France's nuclear and renewable energy infrastructure investment is also expanding recycled metals consumption. The French market grows at approximately 6.7% CAGR through 2033.

Asia Pacific Recycled Metals Market Trends and Insights

Asia Pacific is the largest and fastest-growing regional recycled metals market, anchored by China's dominant position as the world's largest steel producer, with the China Iron and Steel Association (CISA) reporting progressive EAF capacity expansion as part of China's 14th Five-Year Plan steel sector decarbonization mandate, and by Japan and South Korea's world-class non-ferrous metal recycling industries. China is progressively tightening scrap quality import standards while simultaneously building domestic scrap processing capacity, creating structural demand growth for domestically sourced and processed recycled metals. For companies scaling in Asia Pacific, China's regulatory shift represents a generational opportunity to establish domestic scrap processing partnerships before the market consolidates.

India Recycled Metals Market Size

India holds approximately 18% of the Asia Pacific recycled metals market and is among the region's fast-growing markets at approximately 8.2% CAGR by 2033. India's National Steel Policy targets 300 million tonnes of steel capacity by 2030, with EAF and induction furnace scrap-based production representing the fastest-growing production route. India's surging automotive manufacturing and construction infrastructure investment, under the National Infrastructure Pipeline (NIP), are driving domestic recycled ferrous and non-ferrous metal consumption at rates that domestic scrap collection infrastructure is struggling to match.

Japan Recycled Metals Market Size

Japan represents approximately 20% of the Asia Pacific recycled metals market, operating one of the world's most mature and technologically sophisticated metal recycling systems. Japan's Law for Promotion of Effective Utilization of Resources mandates recycling across electronics, automotive, and packaging streams, sustaining high-quality domestic scrap generation and processing. Dowa Holdings is among the world's leading non-ferrous metal recyclers headquartered in Japan. Japan's market grows at approximately 6.5% CAGR through 2033, with e-waste copper and precious metal recovery driving above-market value growth.

South Korea Recycled Metals Market Size

South Korea accounts for approximately 12% of the Asia Pacific recycled metals market, with demand anchored by its world-class shipbuilding, semiconductor, and electronics manufacturing industries that generate significant industrial manufacturing waste scrap streams. South Korea's Resource Circulation Act and expanding EV battery supply chain, with POSCO and Hyundai investing in battery metal recycling, position the country as a structurally growing rare earth and lithium recycling market.

Competitive Landscape

The global recycled metals market rewards scale and vertical integration at the ferrous tier, where Nucor, ArcelorMittal, and Steel Dynamics compete by controlling both scrap collection and EAF steelmaking to capture full value chain margin, while non-ferrous and precious metal recycling rewards technical specialization and certified purity capabilities that command premium pricing from electronics and automotive customers.

The market is moderately consolidated in ferrous processing but significantly more fragmented in non-ferrous and rare earth segments, where niche specialists, including Umicore, Dowa Holdings, and Aurubis, compete on process technology depth. Strategic themes include vertical integration into scrap logistics, investment in AI-powered automated sorting to improve alloy recovery, and carbon accounting infrastructure development to monetize low-carbon certification premiums under emerging CBAM and voluntary carbon market frameworks.

Key Developments:

- March 2026: Mitsubishi Materials Corporation announced an investment in ReElement Technologies and signed a Japan-U.S. collaboration MOU to expand rare earth and rare metal recycling, strengthening circular supply chains for EVs, semiconductors, and renewable energy materials.

- January 2026: Hindustan Zinc Limited partnered with CIMIC Group companies Sedgman and Leighton Asia to develop India’s first zinc tailings recycling facility at Rampura Agucha Mines, Rajasthan, enabling recovery of zinc and silver from legacy mining waste through advanced processing technologies.

- June 2025: Seiko Epson Corporation announced that its subsidiary Epson Atmix commenced operations at a new ¥5.5 billion metal recycling facility in Japan, converting scrap metals into raw materials for metal powder production to support circular manufacturing and carbon reduction goals.

Recycled Metals Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 409.2 Million |

| Current Market Value (2026) | US$ 583.7 Million |

| Projected Market Value (2033) | US$ 937.3 Million |

| CAGR (2026 - 2033) | 7.0% |

| Leading Region | Asia Pacific, 45% market share (2025) |

| Dominant Category - Metal Type | Ferrous Metals, 58% market share (2025) |

| Top-ranking Category - Scrap Source | Industrial Manufacturing Waste, 54% market share (2025) |

| Incremental Opportunity (2026 - 2033) | US$ 353.6 Million |

Companies Covered in Recycled Metals Market

- Nucor Corporation

- Sims Limited

- Commercial Metals Company (CMC)

- Aurubis AG

- European Metal Recycling (EMR)

- Steel Dynamics Inc.

- Schnitzer Steel Industries (Radius Recycling)

- OmniSource LLC

- Gerdau S.A.

- ArcelorMittal

- Dowa Holdings Co., Ltd.

- Umicore

- Remondis SE & Co. KG

- Tata Steel Limited

- Baosteel Group Corporation

- Novelis Inc. (Hindalco Industries)

- Hydro ASA

Frequently Asked Questions

The global recycled metals market is valued at US$ 583.7 million in 2026 and is projected to reach US$ 937.3 million by 2033 at a CAGR of 7.0%.

Key demand drivers include CBAM regulations, rising EV production, renewable energy expansion, and recycled content mandates under the EU CRMA.

Asia Pacific leads the market with around 45% share, supported by strong steel production and advanced recycling infrastructure in China, Japan, and South Korea.

Rare earth metal recycling represents the largest opportunity due to supply security concerns and increasing EV-related demand.

Major players include Nucor Corporation, ArcelorMittal, Steel Dynamics Inc., Sims Limited, Aurubis AG, and Umicore.