- Industrial Machinery

- Rebar Processing Equipment Market

Rebar Processing Equipment Market Size, Share, and Growth Forecast 2026 - 2033

Rebar Processing Equipment Market by Equipment Type (Rebar Bending Machines, Rebar Cutting / Shearing Machines, Rebar Decoiling & Straightening Machines, Rebar Threading Machines, Rebar Welding Machines, Others), Automation Level (Manual, Semi-Automatic, Fully Automatic), by Mobility Type (Stationary, Portable / Mobile), Rebar Diameter Capacity, End-user, Regional Analysis, 2026 - 2033

Rebar Processing Equipment Market Size and Trend Analysis

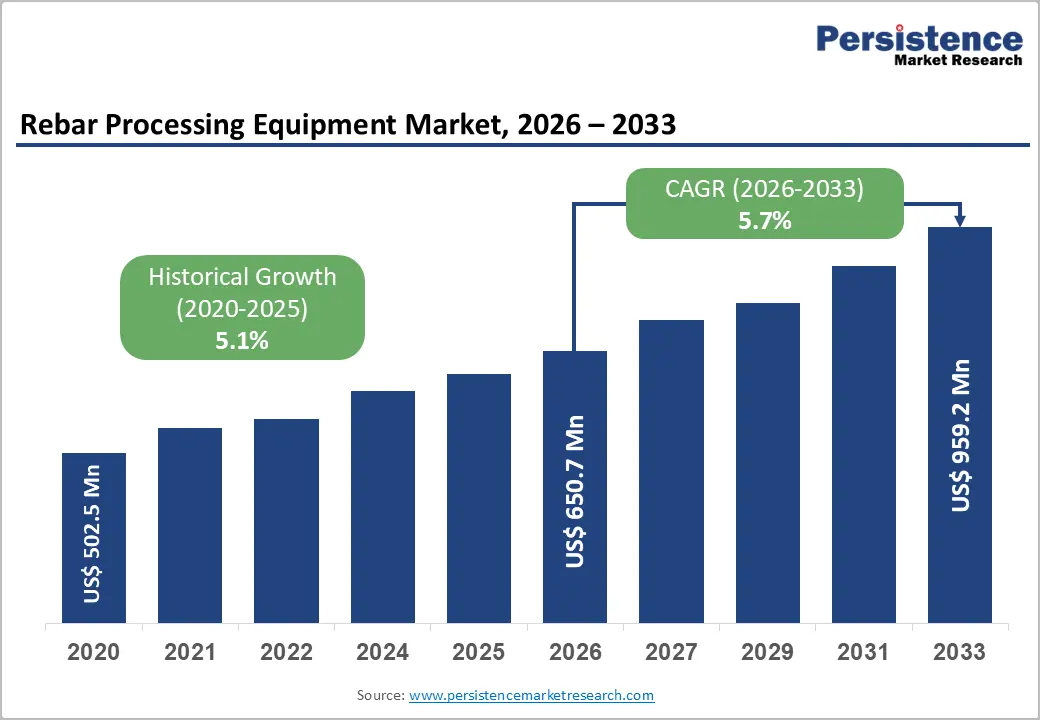

The global rebar processing equipment market size is likely to reach US$ 650.7 million in 2026 and is expected to reach US$ 959.2 million by 2033, growing at a CAGR of 5.7% during the forecast period from 2026 to 2033.

Sustained growth in the rebar processing equipment market is driven by accelerating global construction activity, large-scale infrastructure investment programs, and a structural industry shift toward automated and semi-automated rebar fabrication to address labor shortages and improve precision.

Key Industry Highlights:

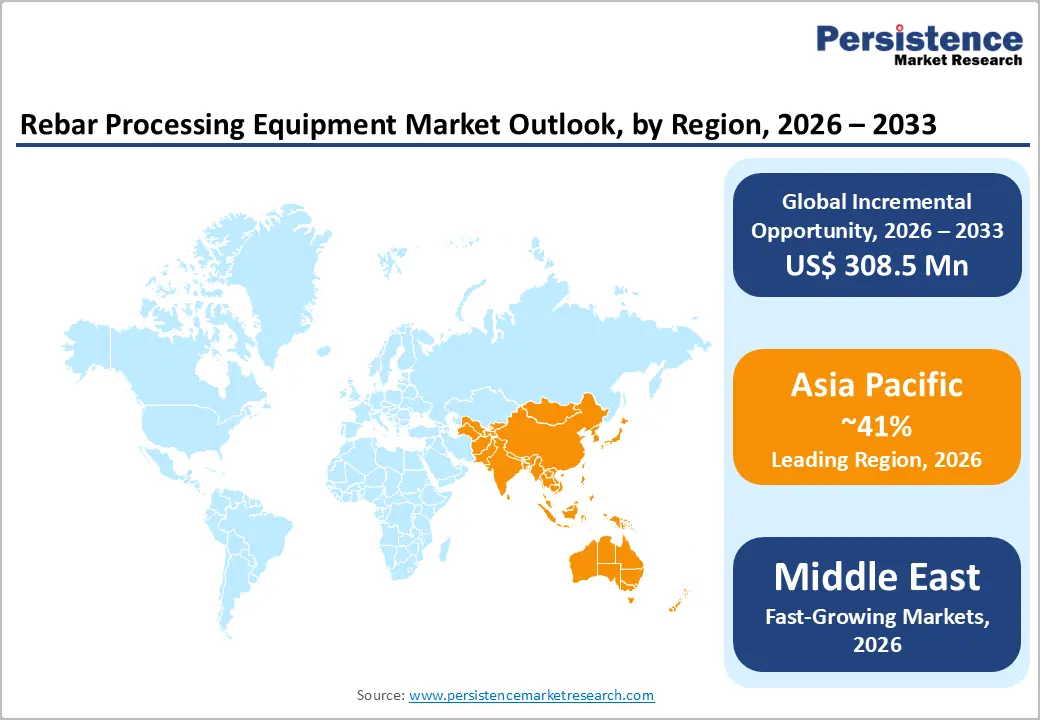

- Leading Region: Asia Pacific dominates the rebar processing equipment market, with a 41% share, driven by China's massive construction and steel consumption base, India's infrastructure investment pipeline, and Japan's demand for precision CNC processing systems across seismic-compliant construction projects.

- Fastest Growing Region: The Middle East is the fastest growing region with a rising CAGR of 7.4%, driven by Saudi Arabia's Vision 2030 mega-projects, including NEOM, UAE infrastructure diversification, and Qatar's post-event construction investments generating exceptional rebar processing equipment demand through 2033.

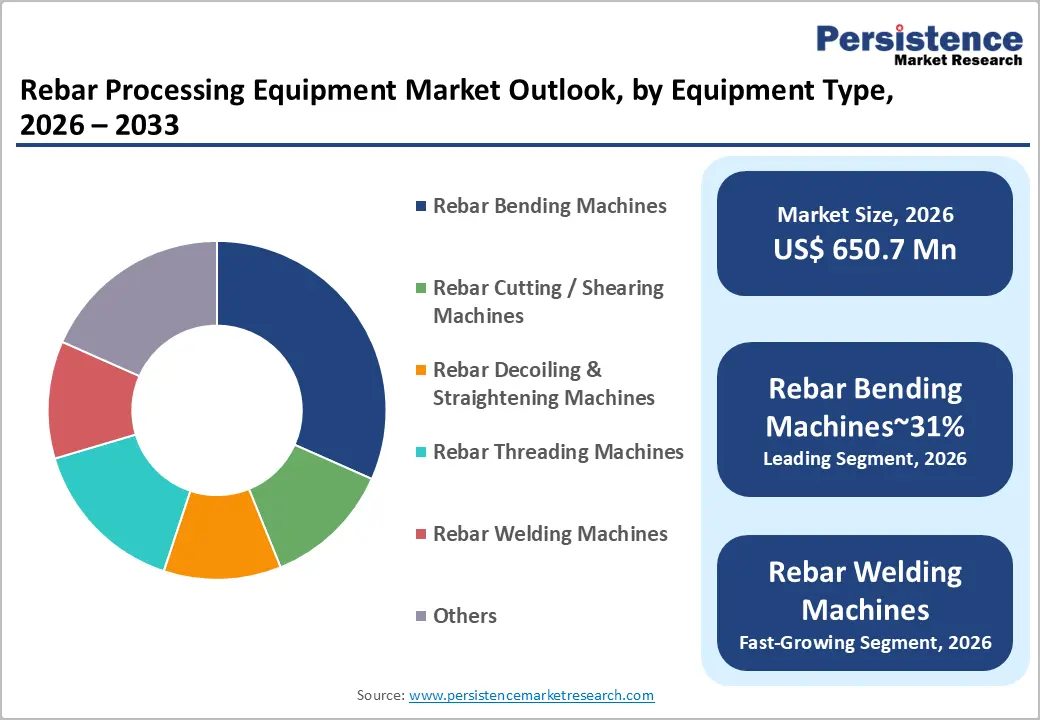

- Dominant Product Segment: Rebar Bending Machines leads the product category with approximately 31% market share, as they are universally required across all reinforced concrete construction project types and available in both portable and stationary configurations.

- Fastest Growing Segment: Fully Automatic systems are the fast-growing, propelled by global construction labor shortages, the shift toward centralized prefabrication, and integration of CNC and BIM technologies, driving superior output accuracy and throughput.

- Key Opportunity: Fully automatic CNC rebar processing lines integrated with BIM software for prefabrication facilities, and heavy-duty equipment targeting Middle East mega-projects, represent the highest-value growth opportunities for manufacturers through the 2026 - 2033 forecast period.

Market Dynamics

Drivers - Large-Scale Global Infrastructure Investment Programs

The acceleration of public infrastructure investment across major economies is the single most powerful demand driver for rebar processing equipment. In the United States, the Bipartisan Infrastructure Law has committed US$ 1.2 trillion to transportation, water systems, broadband, and energy infrastructure, projects that require massive quantities of processed rebar for reinforced concrete structures.

The European Union's REPowerEU Plan and Cohesion Fund are directing hundreds of billions of euros toward construction-intensive green energy and transport projects. India's National Infrastructure Pipeline (NIP), with a projected outlay exceeding US$ 1.4 trillion, represents the single largest planned infrastructure program among emerging economies. Each of these programs, directly and indirectly, drives demand for high-capacity rebar bending, cutting, and straightening equipment at fabrication shops and construction sites worldwide.

Construction Sector Labor Shortages Accelerating Automation Adoption

Chronic skilled labor shortages in the construction industry are compelling contractors, fabricators, and infrastructure companies to invest in automated and semi-automatic rebar processing solutions. According to the Associated General Contractors of America (AGC), over 88% of U.S. construction firms reported difficulty filling craft worker positions as of 2023. Similar labor scarcity trends are documented in Europe and Australia.

Automated rebar processing equipment, capable of executing bending, cutting, and decoiling operations with minimal human intervention, directly addresses this constraint by reducing the skilled labor requirement per unit of output while improving dimensional accuracy and reducing material waste. The economics of automation become increasingly compelling as labor costs rise, driving a structural shift toward fully automatic CNC-controlled rebar processing lines at prefabrication facilities.

Restraints - High Capital Investment and Maintenance Costs

The primary adoption barrier for advanced rebar processing equipment, particularly fully automatic and CNC-controlled systems, is the substantial upfront capital investment required. High-capacity automated rebar processing lines from premium manufacturers can cost between US$200,000 and US$2 million, or more, depending on configuration and throughput.

For small and medium-sized contractors and regional fabricators, who constitute a significant share of end-users, these capital requirements are prohibitive, particularly in price-sensitive emerging markets. Ongoing maintenance costs, spare parts availability, and the need for trained operators further constrain adoption among smaller market participants.

Volatility in Steel and Rebar Raw Material Prices

Rebar processing equipment demand is intrinsically linked to construction activity levels, which, in turn, are highly sensitive to steel and rebar price fluctuations. The World Steel Association noted that global steel prices experienced extreme volatility between 2020 and 2023, with hot-rolled coil prices fluctuating by more than 100% in a single calendar year.

Sharp increases in rebar costs reduce the viability of construction projects and can delay or cancel them, indirectly suppressing equipment procurement. This price volatility creates investment uncertainty among contractors and fabricators, leading to delayed capital equipment purchases and compressed market growth during commodity price peaks.

Opportunities - Fully Automatic CNC Rebar Processing Lines for Prefabrication Facilities

The global shift toward off-site construction and prefabrication, driven by productivity imperatives, quality requirements, and labor efficiency, is creating significant demand for high-throughput, fully automatic CNC rebar processing systems. Prefabrication facilities producing standardized rebar cages, stirrups, and mesh require processing lines capable of executing precise bending and cutting programs with minimal manual input across high daily volumes.

The Modular Building Institute (MBI) reports that the global modular and prefabricated construction sector has been growing at an annual rate of over 6%. Manufacturers such as Schnell Group, MEP Group, and Progress Maschinen & Automation AG that offer complete, integrated rebar processing lines with software-based BIM (Building Information Modeling) data integration are well positioned to capture this premium, high-margin segment as the prefabrication industry scales globally.

Middle East Infrastructure Supercycle and Mega-Project Construction Demand

The Middle East is executing an unprecedented construction supercycle anchored by Saudi Arabia's Vision 2030 mega-projects, including NEOM (budgeted at over US$ 500 billion), The Red Sea Project, Qiddiya, and ROSHN residential developments. The UAE and Qatar are simultaneously investing heavily in post-event infrastructure and economic diversification construction. The region's rebar consumption is among the world's highest on a per capita basis.

These projects require large-scale rebar fabrication capabilities on-site and in dedicated steel processing centers. Rebar processing equipment manufacturers that establish regional distribution partnerships, provide bilingual technical support, and offer tailored heavy-duty configurations for large-diameter rebar are positioned to capture substantial order volumes from this sustained Middle East construction wave.

Category-wise Analysis

By Equipment Type Insights

Rebar Bending Machines dominate the equipment type segment, accounting for approximately 31% of total market share. Bending machines are the most universally required piece of rebar processing equipment, virtually every reinforced concrete construction project requires shaped stirrups, hooks, and bent bars that cannot be efficiently produced manually at scale.

Both manual and CNC-controlled bending machines address a wide spectrum of end-user requirements, from small contractors to large prefabrication plants. The availability of portable bending machines for on-site use and heavy-duty stationary CNC models for fabrication shops ensures demand across all project types and sizes. Leading manufacturers including Schnell Group, Eurobend GmbH, and TJK Machinery, offer extensive bending machine portfolios, further cementing the segment's market leadership.

By Automation Level Insights

The Semi-Automatic segment leads the automation level category, representing approximately 43% of total market share. Semi-automatic rebar processing equipment occupies the optimal balance point between the low output of manual machines and the high capital cost of fully automatic systems. These machines reduce operator fatigue and improve processing consistency while remaining accessible to mid-sized contractors and fabricators operating in both developed and developing markets.

Semi-automatic models, particularly semi-automatic bending and cutting machines, are extensively used across Asia Pacific, the Middle East, and Latin America, where construction activity is high but full automation investment thresholds remain a barrier. The segment's broad price accessibility, ranging from US$ 5,000 to US$ 80,000 depending on capacity, ensures sustained volume demand.

By Mobility Type Insights

Stationary rebar processing equipment leads the mobility type category, capturing approximately 62% of total market share. Stationary systems, installed in dedicated rebar fabrication shops, steel processing centers, and precast manufacturing facilities, support higher throughput, heavier-gauge rebar processing, and the full range of automated functionality that field-portable machines cannot accommodate.

The global trend toward centralized rebar prefabrication, driven by efficiency imperatives and quality control requirements, is fundamentally reinforcing demand for stationary equipment. Large-scale infrastructure projects increasingly rely on dedicated fabrication facilities that supply pre-cut, pre-bent rebar to construction sites, maximizing on-site labor productivity. Stationary equipment manufacturers also benefit from higher average selling prices and more complex system configurations that include integrated conveyors, stacking systems, and CNC control interfaces.

By Rebar Diameter Capacity Insights

The 12-25 mm diameter capacity segment commands the largest market share, accounting for approximately 44% of total demand. This diameter range corresponds directly to the most commonly used rebar sizes in standard reinforced concrete construction, including residential buildings, commercial structures, bridges, and road infrastructure.

Rebar in the 12-25 mm range covers #4 through #8 bars (Imperial) or D12 to D25 (metric), specifications mandated by leading structural design standards, including ACI 318 (American Concrete Institute) and Eurocode 2. The universal applicability of this diameter range across project types ensures the widest possible addressable market, supporting the segment's sustained dominance through the forecast period.

By End-user Insights

Construction Contractors represent the leading end-user segment, accounting for approximately 36% of the total market share. General and specialty contractors, directly executing building, civil, and infrastructure construction, are the primary point of consumption for rebar processing equipment, whether procured for on-site portable use or for project-dedicated fabrication yards.

The global construction industry employs over 100 million workers worldwide according to the International Labor Organization (ILO), and contractor-driven equipment procurement spans the full product spectrum from manual benders to fully automatic CNC processing lines. The sheer scale and diversity of construction contracting activity globally, from residential homebuilding to major civil infrastructure, ensures this segment retains its dominant end-user position throughout the forecast period.

Regional Insights

North America Rebar Processing Equipment Market Trends

North America is a significant and technologically advanced market for rebar processing equipment, led by the United States. The region's market is characterized by strong adoption of automated and semi-automatic systems, driven by persistent construction labor shortages and the emphasis on project efficiency. The Bipartisan Infrastructure Law's US$ 1.2 trillion commitment is generating a multi-year pipeline of bridge reconstruction, highway expansion, and transit projects that directly drive the procurement of fabrication-grade rebar processing equipment. Industry associations, including the Concrete Reinforcing Steel Institute (CRSI), actively publish technical standards and best practices that guide equipment selection and fabrication quality across the U.S. market.

Canada contributes meaningful demand driven by ongoing residential construction and the national Investing in Canada Plan. U.S.-based equipment distributors such as Gensco Equipment Inc. and KRB Machinery serve as critical regional distribution and service hubs for rebar processing lines manufactured abroad. The regulatory environment, governed by OSHA construction safety standards in the U.S. and equivalent provincial standards in Canada, mandates guarded, certified equipment with safety interlocks, creating a quality compliance floor that supports demand for certified, brand-name processing machinery.

Europe Rebar Processing Equipment Market Trends

Europe is a mature, high-quality market for rebar processing equipment, characterized by strong demand for precision-engineered, CE-certified machinery. Italy and Austria are home to globally recognized manufacturers, including Schnell Group, MEP Group, SIMPEDIL SRL (Italy), Progress Maschinen & Automation AG, EVG Entwicklungs- und Verwertungs-Gesellschaft m.b.H. (Austria), that export premium rebar processing systems worldwide. Germany's robust construction sector, supported by the federal government's housing construction programs targeting 400,000 new homes annually, sustains domestic demand for rebar processing equipment.

The United Kingdom's National Infrastructure and Construction Pipeline and France's Grand Paris Express, Europe's largest urban transport project, are generating sustained equipment procurement activity. Spain is investing heavily in renewable energy infrastructure and transport corridors under EU Cohesion Fund programs. The CE marking directive and EN 1992 (Eurocode 2) structural standards provide a harmonized technical framework for equipment and rebar specification across member states, facilitating cross-border equipment trade and standardized fabrication practices.

Asia Pacific Rebar Processing Equipment Market Trends

Asia Pacific is the largest and fastest-growing regional market for rebar processing equipment, accounting for the dominant share of global demand. China is the undisputed volume leader; the country's construction sector consumes over 50% of the world's rebar production, according to the World Steel Association. Chinese manufacturers, including TJK Machinery (Tianjin) Co., Ltd. and Henan Sinch Machinery Co., Ltd., produce cost-competitive rebar processing equipment serving both domestic and export markets across Asia, Africa, and the Middle East. India's rapidly expanding construction sector, driven by the NIP and PM Gati Shakti National Master Plan, represents a fast-growing secondary market.

Japan is a technically sophisticated market with strong demand for precision CNC rebar processing systems from manufacturers such as Toyo Kensetsu Kohki Co., Ltd. The country's seismic construction requirements mandate highly precise rebar fabrication, driving demand for certified, high-accuracy processing equipment. ASEAN countries, particularly Vietnam, Indonesia, and the Philippines, are experiencing rapid infrastructure development backed by Asian Development Bank (ADB) financing, creating growing markets for both imported and locally distributed rebar processing machinery. The region's competitive manufacturing cost base also positions it as a key production hub for rebar processing equipment exported globally.

Competitive Landscape

The global rebar processing equipment market is moderately fragmented, featuring a blend of European precision engineering leaders, Asian volume manufacturers, and regional specialists. Italian and Austrian manufacturers, including Schnell Group, MEP Group, Progress Maschinen & Automation AG, and EVG, hold premium market positions based on technological sophistication, CNC integration capability, and global after-sales networks.

Chinese manufacturers such as TJK Machinery compete aggressively on price, particularly in developing markets. Key competitive differentiators include BIM software integration, processing line automation depth, rebar diameter range, and service network breadth. Emerging trends include cloud-connected machine monitoring, predictive maintenance systems, and complete turnkey prefabrication line solutions that bundle equipment, software, and training into integrated contracts.

Key Developments:

- January 2025: Schnell Group launched an updated series of fully automatic CNC stirrup bending machines featuring integrated BIM data import capabilities, targeting large-scale prefabrication facilities across Europe and the Middle East.

- October 2024: Progress Maschinen & Automation AG unveiled a next-generation mesh welding line with AI-assisted quality control for precast manufacturers, designed to reduce material waste and improve weld consistency at high production throughput rates.

- April 2024: TJK Machinery (Tianjin) Co., Ltd. announced expansion of its overseas service network across Southeast Asia and the Middle East, establishing dedicated technical support centers to enhance after-sales service for its growing international customer base.

Companies Covered in Rebar Processing Equipment Market

- Schnell Group

- Jaypee India Limited

- Gensco Equipment Inc.

- KRB Machinery

- Eurobend GmbH

- PEDAX GmbH

- TJK Machinery (Tianjin) Co., Ltd.

- Toyo Kensetsu Kohki Co., Ltd.

- Everest Equipment Private Limited

- Ellsen Bending Machine

- EVG Entwicklungs- und Verwertungs-Gesellschaft m.b.H.

- MEP Group

- Progress Maschinen & Automation AG

- SIMPEDIL SRL

- Henan Sinch Machinery Co., Ltd.

- AWM S.p.A.

- Stema Engineering S.r.l.

- Sathya Technologies Private Limited

Frequently Asked Questions

The global Rebar Processing Equipment Market is projected to reach US$ 959.2 Million by 2033, up from US$ 650.7 Million in 2026, registering a CAGR of 5.7% during the 2026 - 2033 forecast period.

The primary growth drivers are large-scale global infrastructure investment programs, including the U.S. Bipartisan Infrastructure Law (US$ 1.2 trillion), India's National Infrastructure Pipeline, and Middle East mega-projects, combined with accelerating automation adoption driven by construction sector labor shortages exceeding 88% difficulty rates in craft worker hiring reported by U.S. contractors.

Rebar Bending Machines leads with approximately 31% of total market share. Their universal requirement across all reinforced concrete construction project types, combined with availability in both portable on-site and high-capacity stationary CNC configurations, ensures consistent and broad-based demand globally from contractors to precast manufacturers.

Asia Pacific is the dominant region, led by China's construction sector consuming over 50% of global rebar production, India's multi-trillion-dollar infrastructure pipeline, and Japan's sophisticated demand for precision CNC processing systems. The region benefits from both the world's largest construction activity base and competitive domestic manufacturing of rebar processing equipment.

The highest-value opportunities include fully automatic CNC rebar processing lines with integrated BIM data connectivity targeting the rapidly expanding global prefabrication sector, and heavy-duty equipment configurations serving the Middle East's construction supercycle anchored by Saudi Arabia's Vision 2030 mega-projects such as NEOM, which alone carries a budget exceeding US$ 500 billion.

The key market participants include Schnell Group, Jaypee India Limited, Gensco Equipment Inc., KRB Machinery, Eurobend GmbH, PEDAX GmbH, TJK Machinery (Tianjin) Co., Ltd., Toyo Kensetsu Kohki Co., Ltd., Everest Equipment Private Limited, EVG Entwicklungs- und Verwertungs-Gesellschaft m.b.H., MEP Group, Progress Maschinen & Automation AG, SIMPEDIL SRL, and Henan Sinch Machinery Co., Ltd.