- Industrial Goods & Service

- Punching Machine Market

Punching Machine Market Size, Share, and Growth Forecast, 2026 - 2033

Punching Machine Market by Machine Type (CNC Punching Machines, Pneumatic Punching Machines, Others), Mode of Operation (Fully Automatic, Fully Automatic, Others), End-user, and Regional Analysis for 2026 - 2033

Punching Machine Market Size and Trends Analysis

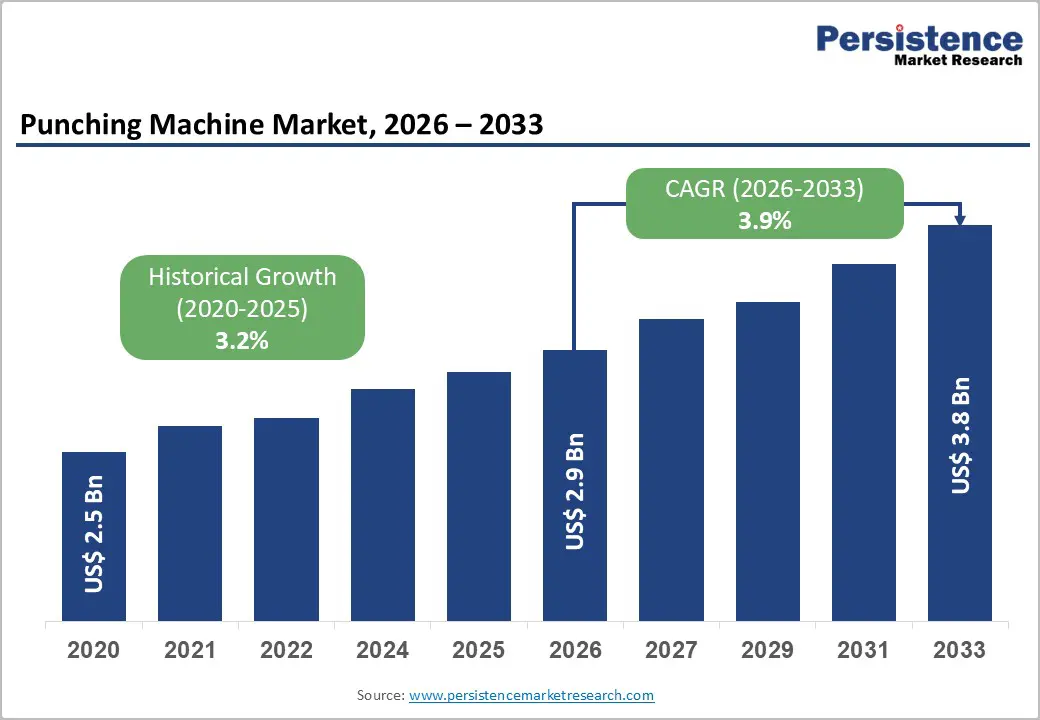

The global punching machine market size is likely to be valued at US$2.9 billion in 2026 and is expected to reach US$3.8 billion by 2033, growing at a CAGR of 3.9% between 2026 and 2033, driven by increasing automation in metal fabrication facilities, rising demand for precision sheet-metal components, and modernization of manufacturing plants through Industry 4.0 technologies.

Manufacturers are replacing traditional mechanical punching equipment with CNC-controlled and servo-electric punching machines that offer higher efficiency, accuracy, and integration with digital production systems. Regional manufacturing expansion and supply-chain diversification are also supporting equipment demand. Asia Pacific currently represents the largest share of global revenue, driven by expanding industrial production in China, India, Japan, and Southeast Asia.

Key Industry Highlights

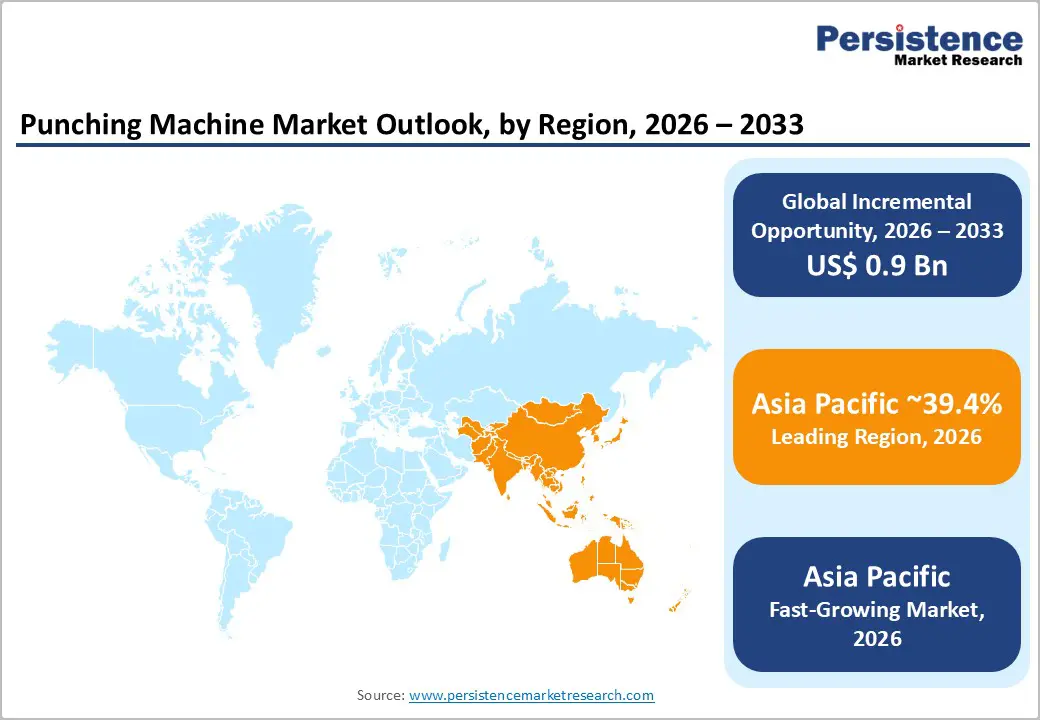

- Leading Region: Asia Pacific is projected to account for approximately 39.4% of revenue share, supported by large-scale manufacturing activity in China, Japan, India, and Southeast Asia, and strong demand from automotive, electronics, and appliance production sectors.

- Fastest-growing Region: Asia Pacific is also the fastest-growing regional market, driven by rapid industrialization, government-backed manufacturing initiatives such as India’s “Make in India” program, and expansion of electronics and automotive production facilities across emerging Southeast Asian economies.

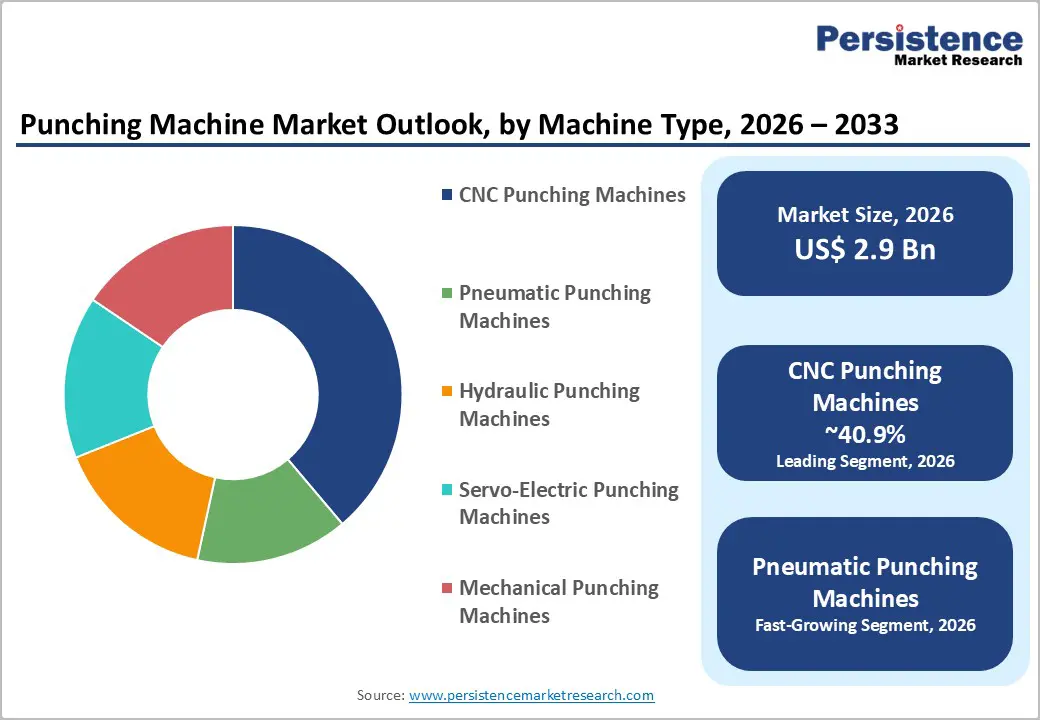

- Dominant Machine Type: CNC punching machines are anticipated to hold approximately 40.9% market share, driven by their high precision, programmable flexibility, and integration capabilities with automated production lines used in automotive, appliance, and industrial component manufacturing.

- Leading Mode of Operation: Fully automatic punching machines dominate with an anticipated 68.6% market share, supported by increasing adoption of automated fabrication lines, robotic sheet handling systems, and lights-out manufacturing strategies across large-scale production facilities.

| Key Insights | Details |

|---|---|

| Punching Machine Market Size (2026E) | US$2.9 Bn |

| Market Value Forecast (2033F) | US$3.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Growing Adoption of Industry 4.0 Automation in Metal Fabrication

Manufacturers are increasingly investing in digitally integrated fabrication systems to improve operational efficiency and reduce labor dependency. Modern punching machines are now integrated with CNC controls, automated tool changers, robotic sheet loaders, and factory management software, enabling continuous production with minimal operator involvement. Industrial automation initiatives across automotive, electronics, and appliance manufacturing are accelerating the adoption of fully automated punching systems capable of operating in lights-out manufacturing environments. These systems improve throughput, reduce scrap rates, and enhance precision in high-volume manufacturing processes. From a market perspective, automation upgrades are shifting customer demand toward high-value CNC punching machines and servo-electric systems. Vendors increasingly bundle punching machines with material handling automation and predictive maintenance software, expanding equipment revenue and long-term service contracts.

Expanding Demand for Precision Sheet-Metal Components

The global manufacturing ecosystem relies heavily on sheet-metal components for structural and functional applications. Industries such as automotive, electronics, HVAC systems, appliances, and industrial machinery require punched metal components, including brackets, panels, housings, and structural frames. Electric vehicle manufacturing is further increasing demand for battery enclosures, thermal management components, and lightweight chassis elements, all of which rely on high-precision sheet-metal fabrication. Similarly, electronics manufacturing requires miniaturized metal components with tight tolerances, increasing the need for programmable punching systems. This growing complexity of metal parts is encouraging manufacturers to adopt advanced punching technologies capable of flexible tooling and programmable part production. As product designs evolve, fabricators require machines capable of quick setup changes and digital programming, strengthening long-term demand for modern punching equipment.

Energy Efficiency and Lifecycle Cost Optimization

Industrial manufacturers increasingly evaluate equipment purchases based on total cost of ownership (TCO) rather than initial purchase price. Traditional hydraulic punching machines consume significantly more power and require more frequent maintenance than newer servo-electric systems. Servo-electric punching machines deliver higher energy efficiency, reduced maintenance requirements, and improved process control, resulting in lower lifecycle operating costs. These advantages are particularly important in regions with high electricity prices or strict sustainability requirements. As sustainability reporting and energy-efficiency regulations become more prominent, companies are prioritizing equipment that reduces operational energy consumption. This shift is gradually increasing the share of servo-electric and CNC punching machines within overall equipment installations, supporting long-term revenue growth for advanced equipment manufacturers.

Barrier Analysis - High Capital Investment and Long Equipment Replacement Cycles

Punching machines represent a significant capital investment for fabrication companies. Large automated punching systems integrated with material handling equipment can require substantial upfront expenditure. Many small and medium-sized fabrication businesses continue operating older mechanical punching machines due to their durability and long service life. Replacement decisions often depend on production expansion or major process modernization, resulting in extended equipment replacement cycles. These long investment cycles limit short-term equipment demand and can slow market expansion, particularly in regions with limited access to industrial financing.

Supply Chain Constraints for Specialized Components

Punching machines rely on precision components, including servo motors, high-tolerance tooling systems, CNC controllers, and automated tool-handling mechanisms. Supply disruptions affecting these components can delay machine manufacturing and delivery schedules. Fabrication companies often require customized tooling and automation configurations tailored to their production processes. Supply chain delays for specialized components may extend equipment lead times and increase project implementation costs. Such supply constraints create operational challenges for machine manufacturers and can delay end users' capital investment decisions.

Opportunity Analysis - Modernization of Legacy Fabrication Equipment

A significant installed base of legacy punching machines exists across global manufacturing facilities. Many of these systems operate without modern automation, digital connectivity, or advanced control systems. Equipment manufacturers have an opportunity to offer retrofit solutions, including CNC controllers, servo drives, automation modules, and digital monitoring systems. These upgrades allow fabrication companies to improve productivity and energy efficiency without replacing entire machines. The modernization of installed equipment provides a substantial aftermarket revenue stream through service contracts, replacement tooling, and digital upgrades.

Growth of Integrated Hybrid Manufacturing Systems

Manufacturing processes are increasingly shifting toward flexible production lines capable of performing multiple fabrication processes in a single system. Hybrid machines combining punching, laser cutting, or shearing functions allow manufacturers to produce complex parts efficiently. Integrated fabrication systems reduce production steps, minimize material handling requirements, and improve production flexibility for small-batch manufacturing. Equipment manufacturers that develop integrated punch-laser or punch-shear systems with automated material handling are well-positioned to capture demand from high-mix manufacturing sectors such as electronics and industrial equipment production.

Manufacturing Expansion in Emerging Economies

Emerging economies are rapidly expanding their manufacturing sectors to support domestic consumption and export growth. Countries such as India, Vietnam, Thailand, and Indonesia are strengthening industrial production capabilities across automotive, electronics, and consumer goods sectors. Government initiatives promoting domestic manufacturing and industrial infrastructure development are encouraging investment in fabrication equipment. Many manufacturers are establishing new production facilities in these regions to diversify supply chains. This industrial expansion creates strong opportunities for punching machine suppliers offering cost-competitive equipment, regional service support, and localized production capabilities.

Category-wise Analysis

Machine Type Analysis

CNC punching machines are expected to lead, accounting for an anticipated 40.9% of market share in 2026. Their dominance is primarily attributed to high precision, automation capability, and compatibility with digital manufacturing systems. CNC punching machines allow operators to program complex punching patterns, significantly reducing setup time while enabling rapid production changes across multiple product designs. Automotive and appliance manufacturers widely rely on CNC punching machines for high-volume production of metal panels, brackets, enclosures, and structural components. Leading fabrication equipment manufacturers such as Amada Co., Ltd. and TRUMPF Group offer advanced CNC punching systems that integrate tool libraries, automatic sheet loaders, and software-based process control to support Industry 4.0 production environments. Integration with automated material handling systems and robotic unloading units further increases productivity, making CNC machines the preferred choice for modern sheet-metal fabrication facilities focused on scalability and repeatable accuracy.

Pneumatic punching machines are the fastest-growing machine type. Their growth is driven largely by cost-sensitive manufacturing operations that require reliable yet affordable fabrication equipment. Pneumatic systems provide efficient punching performance for light-to-medium sheet-metal applications and typically require relatively simple maintenance compared to hydraulic systems. Small and mid-sized fabrication businesses are increasingly adopting pneumatic machines to expand production capacity while keeping investment costs manageable. For example, many regional manufacturers supplying metal parts for electrical enclosures and HVAC components deploy pneumatic punching machines due to their lower operational complexity. Improvements in pneumatic control systems, modular tooling platforms, and programmable feed mechanisms are further enhancing the competitiveness of these machines, particularly in emerging manufacturing markets across Southeast Asia and Latin America.

Mode of Operation Insights

Fully automatic punching machines dominate the market, accounting for an anticipated 68.6% of market share. Their leadership reflects the manufacturing sector’s increasing focus on automation, operational efficiency, and consistent production quality. Fully automated punching systems integrate CNC programming, automated sheet loading, tool changing, and part stacking, enabling continuous production with minimal operator involvement. Automotive and appliance manufacturers rely heavily on such systems to achieve high production volumes while maintaining tight dimensional tolerances. Equipment providers such as Murata Machinery and Prima Power have introduced automated punching lines that integrate robotics and smart sensors to improve throughput and reduce downtime. Automated systems also improve workplace safety by reducing manual handling of metal sheets and tooling, which are often associated with injury risks in traditional fabrication environments.

The fully automatic segment is also identified as the fastest-growing mode of operation, reflecting the rapid adoption of advanced automation technologies across global manufacturing facilities. Increasing labor costs and shortages of skilled machine operators are pushing manufacturers to invest in equipment capable of operating with minimal human supervision. Fully automated punching systems support lights-out manufacturing, in which production continues without operators during night shifts or on weekends. For instance, large automotive component suppliers increasingly deploy automated punching cells integrated with robotic storage systems to support continuous production schedules. Integration with production planning software, Industrial Internet of Things (IIoT) platforms, and predictive maintenance analytics further enhances operational efficiency by enabling manufacturers to monitor machine performance and reduce unexpected downtime.

Regional Insights

North America Punching Machine Market Trends - CNC Automation and Reshoring Driving Smart Sheet-Metal Fabrication Adoption

North America represents a technologically advanced market for punching machines, supported by a well-established manufacturing ecosystem and strong adoption of industrial automation technologies. The U.S. dominates the regional market, driven by its large automotive, aerospace, and industrial equipment manufacturing sectors. According to data from the U.S. Census Bureau and the National Association of Manufacturers, the United States maintains one of the world’s largest metal fabrication and machinery manufacturing industries, creating sustained demand for high-precision sheet-metal processing equipment. Manufacturers increasingly deploy digitally controlled punching systems integrated with automated material handling to improve productivity and operational efficiency.

Manufacturers across the region are investing in CNC punching machines and automated fabrication lines to address skilled labor shortages and rising operational costs. Equipment suppliers such as Amada America and TRUMPF Inc. have expanded demonstration centers and technical training facilities in the United States to support customers adopting advanced fabrication technologies. For instance, TRUMPF expanded its Smart Factory capabilities at its Chicago-area facility, showcasing integrated punching, laser cutting, and automation solutions designed for digital manufacturing environments. These initiatives encourage regional manufacturers to adopt Industry 4.0-compatible equipment capable of data-driven production monitoring. The automotive and aerospace industries remain major demand drivers for punching machines across North America. Aerospace manufacturers require high-precision sheet-metal components for aircraft fuselage structures, engine housings, and interior assemblies. Companies such as Boeing and major aerospace suppliers rely on precision fabrication technologies to maintain strict quality standards and regulatory compliance. Punching machines integrated with automated tool-changing systems are widely used to produce structural panels and lightweight metal components required in aircraft manufacturing.

Reshoring initiatives are also strengthening regional demand for fabrication equipment. Several U.S. manufacturers have been relocating or expanding production facilities domestically to reduce supply-chain disruptions and improve production resilience. This trend has encouraged investments in modern automated punching systems capable of supporting high-mix manufacturing environments. For example, contract metal fabricators across the Midwest manufacturing corridor have upgraded production lines with CNC punching systems supplied by companies such as Prima Power and Murata Machinery to improve production flexibility and lead times.

Investment trends indicate increasing adoption of fully automated punching cells capable of lights-out manufacturing. Equipment providers are expanding service networks across North America to offer predictive maintenance, remote diagnostics, and digital monitoring platforms. These solutions support long-term machine performance and help manufacturers reduce downtime, strengthening the region’s position as a key market for advanced punching machine technologies.

Europe Punching Machine Market Trends - Advanced Engineering and Flexible Manufacturing Systems Strengthening Precision Fabrication

Europe represents one of the most technologically sophisticated markets for punching machines, characterized by strong engineering capabilities and widespread adoption of industrial automation technologies. Countries including Germany, Italy, the United Kingdom, France, and Spain represent major demand centers for sheet-metal fabrication equipment. The region’s advanced automotive, aerospace, and industrial machinery sectors require high-precision metal components, creating steady demand for modern punching systems integrated with CNC control and automation.

Germany leads the European market due to its highly developed manufacturing sector and strong presence of advanced machinery producers. German manufacturers consistently invest in automated sheet-metal fabrication technologies to maintain productivity and global competitiveness. Major equipment manufacturers such as TRUMPF Group and LVD Group supply CNC punching machines and integrated production systems used across European automotive and industrial manufacturing plants. TRUMPF’s continuous investment in automated sheet-metal processing technologies, including punching-laser combination machines, has strengthened the region’s position as a global hub for advanced fabrication equipment.

Italy also plays an important role in the market as a major equipment manufacturing hub. Italian companies such as Prima Power specialize in automated sheet-metal processing systems and flexible manufacturing lines used in the production of appliances, automotive components, and industrial equipment. The company has introduced integrated punching and bending systems designed to support high-mix, low-volume manufacturing, which is common across European industrial sectors. Manufacturers across Europe are also adopting flexible manufacturing systems capable of handling customized production runs. These systems integrate punching, laser cutting, bending, and automated material handling within unified production lines. This trend supports the region’s shift toward advanced digital manufacturing and reinforces Europe’s leadership in high-precision sheet-metal fabrication technologies.

Asia Pacific Punching Machine Market Trends - Rapid Industrialization and Manufacturing Expansion Boosting CNC Punching Demand

Asia Pacific represents the largest and fastest-growing region in the punching machine market, accounting for approximately 39.4% of the market share. The region’s large manufacturing base in automotive, electronics, appliances, and industrial machinery creates sustained demand for punching machines capable of supporting high-volume production. China dominates regional manufacturing output and maintains one of the world’s largest installed bases of sheet-metal fabrication equipment. Chinese manufacturers are increasingly upgrading production facilities with CNC-controlled punching systems and automated fabrication lines to improve product quality and compete in international markets.

Domestic equipment producers and global suppliers such as Amada and TRUMPF continue expanding their presence in China to support growing industrial demand. These companies have strengthened regional service networks and technical training centers to support manufacturers transitioning toward automated production systems. India is emerging as one of the fastest-growing markets due to strong government initiatives promoting domestic manufacturing. Programs such as “Make in India” and industrial production incentives are encouraging the expansion of automotive, electronics, and appliance manufacturing facilities. These industries require modern sheet-metal fabrication technologies, increasing demand for punching machines capable of supporting large-scale production operations. Equipment manufacturers are responding by expanding distribution networks and technical support services in major Indian industrial hubs.

Localization strategies, expanding industrial infrastructure, and increasing adoption of automation technologies are expected to further strengthen the Asia Pacific’s leadership in the global punching machine market. Continued investment by equipment manufacturers and manufacturing firms across the region will support long-term growth and reinforce its position as a critical hub for sheet-metal fabrication equipment.

Competitive Landscape

The global punching machine market is moderately concentrated, particularly in the high-end equipment segment. Established global manufacturers dominate the premium segment with advanced CNC punching machines, hybrid fabrication systems, and fully automated production lines. The market includes numerous regional manufacturers that produce cost-competitive punching machines for small and medium-sized fabrication companies. This results in a dual-tier market structure, where global leaders compete through technological innovation while regional players focus on price competitiveness and localized service.

Leading manufacturers focus on automation innovation, energy-efficient machine design, digital manufacturing integration, and expansion of global service networks. Companies are also developing hybrid fabrication systems and region-specific machine models to address diverse production requirements across developed and emerging manufacturing markets.

Key Industry Developments

- In April 2025, TRUMPF Group demonstrated the integration of its TruMatic 5000 punching-laser machine with a STOPA automated storage system, allowing the production line to operate continuously without personnel. The solution enables 24-hour lights-out manufacturing while automatically managing material flow and finished parts handling.

- In May 2025, Amada Co., Ltd. announced the launch of the ORSUS-3015AJe fiber laser cutting machine and SRB-1003 press brake for global markets, expanding its advanced sheet-metal fabrication equipment portfolio and strengthening its integrated manufacturing solutions for industrial customers.

Companies Covered in Punching Machine Market

- TRUMPF Group

- Amada Co., Ltd.

- Prima Power

- Salvagnini

- Murata Machinery, Ltd.

- Bystronic Group

- LVD Company

- Cincinnati Incorporated

- Ermaksan

- Tailift Co., Ltd.

- Yangli Group

- AIDA Engineering, Ltd.

- Komatsu Industries Corp.

- Yamazaki Mazak Corporation

- Schuler Group

- Durmazlar Machinery

- Nisshinbo Mechatronics Inc.

- Otto Bihler Maschinenfabrik GmbH & Co. KG

Frequently Asked Questions

The global punching machine market is estimated to reach US$2.9 billion in 2026.

The punching machine market is projected to reach US$3.8 billion by 2033.

Major trends include the growing adoption of fully automated punching systems, increasing integration with Industry 4.0 manufacturing platforms, rising demand for servo-electric and CNC punching machines, and expanding use of automated material handling and lights-out production systems in fabrication facilities.

CNC punching machines represent the leading machine type segment, accounting for around 40.9% of total market share, driven by their precision, programmability, and compatibility with automated production systems.

The punching machine market is expected to grow at a CAGR of 3.9% between 2026 and 2033.

Major companies with strong product portfolios include TRUMPF Group, Amada Co., Ltd., Prima Power, Salvagnini, and Murata Machinery.