- Biotechnology

- Prostate Cancer Biomarkers Market

Prostate Cancer Biomarkers Market Size, Share, and Growth Forecast 2026 - 2033

Prostate Cancer Biomarkers Market by Product Type (Genetic, Protein Biomarkers), Application (Screening and Early Detection, Diagnosis and Risk Stratification), End-user (Hospitals and Diagnostic Laboratories), and Regional Analysis, 2026 - 2033

Prostate Cancer Biomarkers Market Size and Trends Analysis

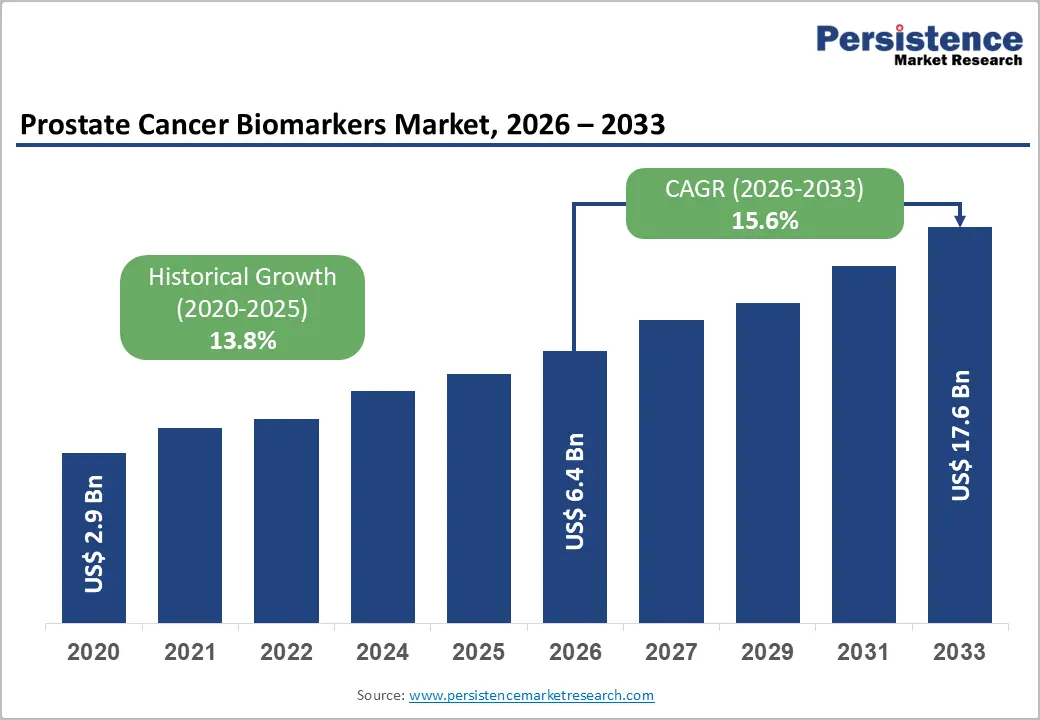

The global prostate cancer biomarkers market size is likely to be valued at US$6.4 billion in 2026 and is expected to reach US$17.6 billion by 2033, growing at a CAGR of 15.6% during the forecast period from 2026 to 2033, driven by the rising shift toward non-invasive diagnostic approaches such as liquid biopsy and urine-based biomarker tests. These help in reducing reliance on traditional biopsy procedures.

Key Industry Highlights

- Leading Product Type: Protein biomarkers, approximately 58.3% share in 2026, as these enable early detection and monitoring of disease progression by recognizing abnormal protein expression patterns.

- Dominant Application: Screening and early detection, nearly 46.8% share in 2026, owing to rising disease prevalence and adoption of non-invasive tests.

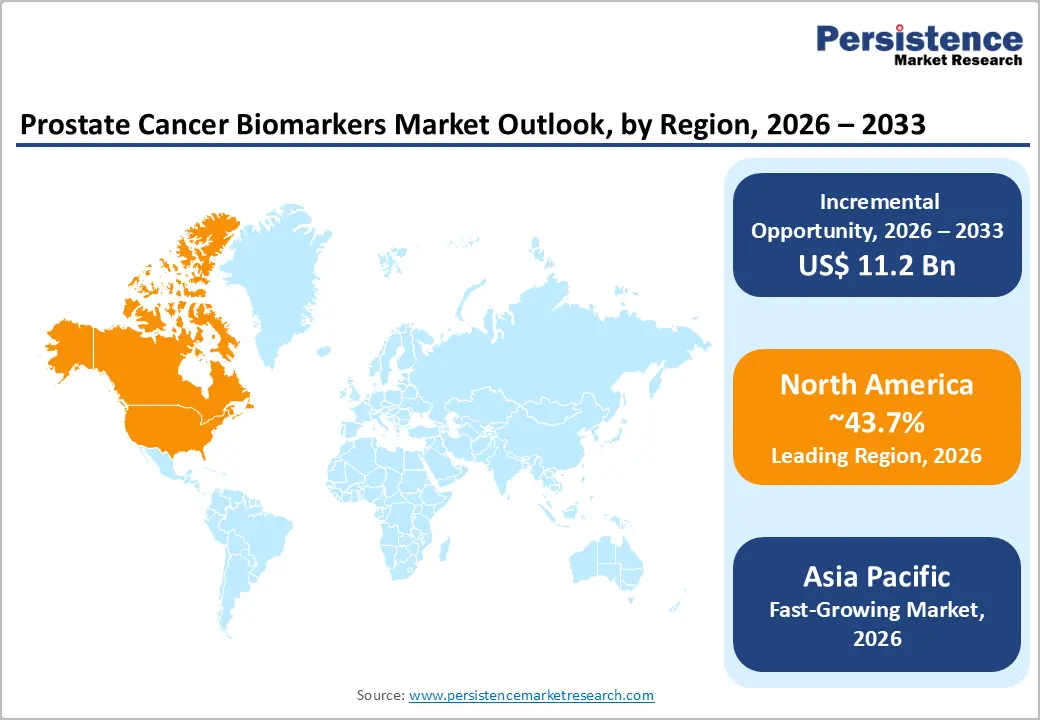

- Leading Region: North America, with about 43.7% share in 2026, backed by increasing adoption of biomarker-based diagnostics and significant research funding.

- Fast-growing Region: Asia Pacific, spurred by increasing emphasis on early diagnosis and rising cancer awareness.

- New Study: A multi-center study led by investigators from Sylvester Comprehensive Cancer Center, UC San Diego, UCSF, Scripps Research Institute, and Guardant Health demonstrated that serial liquid biopsies tracking circulating tumor DNA could reveal how metastatic prostate cancer evolves under treatment pressure in real time.

DRO Analysis

Driver - Rising Demand for Early-stage and Accurate Disease Detection

Prostate cancer is often detected at a stage where treatment outcomes are already compromised. The core problem is that early-stage disease rarely shows symptoms. This is exactly where biomarkers have started to close a real clinical gap. In 2025, the American Urological Association updated its Early Detection of Prostate Cancer Guideline, integrating new evidence on biomarker use alongside imaging to improve screening decisions.

New tests such as ExoDx Prostate IntelliScore and MyProstateScore are now being used to add clinical weight to borderline PSA readings, helping clinicians decide whether a biopsy is truly required. The Food and Drug Administration’s (FDA) December 2025 approval of Cleveland Diagnostics' IsoPSA, a blood test that identifies structural variants of the PSA protein, is a direct response to this unmet need. It specifically targets high-grade cancer detection in men aged 50 and older with elevated PSA levels. These tools are shifting early detection from a guessing game to a data-backed clinical decision.

Surging Shift Toward Personalized Prostate Cancer Treatment

The shift toward personalized prostate cancer treatment is no longer theoretical. It is showing up in trial data and regulatory decisions. Precision medicine has changed prostate cancer management by integrating genomic profiling and biomarker-backed patient stratification into clinical practice. For instance, in the Phase 3 TALAPRO-2 trial, talazoparib combined with enzalutamide reduced the risk of disease progression or death by 55% in patients with HRR-deficient metastatic castration-resistant prostate cancer, leading to FDA approval.

The outcomes are only possible when the right biomarker, in this case, HRR gene mutation status, identifies the right patient. The FDA now mandates companion diagnostic testing to determine BRCA mutation status before prescribing olaparib with abiraterone. It is hence creating a direct and institutionalized link between biomarker testing and treatment access. This regulatory framework is a structural driver of market growth.

Restraint - Inability of PSA Test to Detect Cancer Apart from Benign Disease

The Prostate-Specific Antigen (PSA) test remains central to prostate cancer screening, but its inability to distinguish cancer from non-cancerous conditions is a long-standing clinical problem. Benign conditions such as benign prostatic hyperplasia and prostatitis, as well as routine procedures, including digital rectal examination and catheterization, can all raise PSA levels. The scale of this issue is significant. Studies show that up to 86% of individuals with benign prostatic hyperplasia may have high PSA levels.

The downstream consequences are not trivial. About 75% of men with a raised PSA level are subsequently found to have a negative prostate biopsy. It means the majority of men who go through an invasive procedure do not have cancer. The U.S. Preventive Services Task Force estimates that overdiagnosis rates for screen-detected prostate cancer range from 22% to 42%. This diagnostic imprecision erodes both clinician confidence and patient trust, limiting how aggressively biomarker-based screening programs can be expanded.

Opportunity - Increasing Shift Toward Multi-Parametric Panels

The clinical limitations of PSA alone have created a real commercial opening for multi-biomarker panels that combine several signals into a single, more reliable risk score. FDA- and CLIA-recognized tests such as the 4Kscore, Prostate Health Index (PHI), PCA3, MyProstateScore, SelectMDx, and ExoDx Prostate IntelliScore have been recommended by the NCCN and the AUA/SUO guidelines for clinical application, signaling growing institutional backing.

These tests don't replace PSA, but they reframe it. For instance, combinations of PHI or 4Kscore with multiparametric MRI have demonstrated AUCs above 0.850 in diagnosing high-grade prostate cancer, meaningfully outperforming PSA in isolation. The opportunity is in building diagnostic pathways where PSA acts as an initial flag, and multi-marker panels or imaging then triage who genuinely requires a biopsy. This approach reduces unnecessary procedures while improving detection of clinically significant disease.

AI to Turn Existing Data into Sharp Diagnostic Signals

AI is creating a second-order opportunity in prostate cancer biomarkers, not by finding new molecules, but by extracting more from data that already exists. Across the prostate cancer pathway, AI systems for MRI interpretation, digital pathology, and biomarker discovery have consistently raised diagnostic performance and reduced unnecessary biopsies in validated studies.

On the regulatory side, Artera's ArteraAI Prostate received FDA De Novo authorization in August 2025 as the first AI-backed software cleared to prognosticate long-term outcomes in non-metastatic prostate cancer. These approvals confirm that AI-assisted biomarker interpretation is moving from research into reimbursable clinical practice.

Category-wise Analysis

Product Type Insights

Protein biomarkers are expected to lead in 2026, with a share of nearly 58.3%, boosted by the deep clinical history and institutional trust built around PSA. New protein-based tests have addressed PSA's well-known limitations while staying within familiar clinical workflows. The 4K score, which integrates four kallikrein proteins, including total PSA, free PSA, intact PSA, and hK2, has been shown through meta-analysis to improve biopsy predictive accuracy by 8 to 10% and reduce the rate of unnecessary biopsies by 48 to 56%.

Metabolomic biomarkers are anticipated to be the fastest-growing in 2026, as these provide the ability to distinguish severe prostate cancer from non-threatening disease at the biochemical level. Research published in November 2025 in the journal Cancers showed that drastic metabolite changes in clinically significant prostate cancer often involve fatty acid metabolism, sphingolipid metabolism, glycolysis, the citric acid cycle, and purine/pyrimidine metabolism.

Application Insights

The screening and early detection segment is projected to dominate with a share of approximately 46.8% in 2026, as prostate cancer is largely asymptomatic in its early stages. By the time symptoms appear, the disease is often already advanced. In 2025, the American Urological Association updated its Early Detection of Prostate Cancer Guideline, integrating newly published evidence on biomarker use, imaging, and biopsy technique to improve clinical decision-making in screening programs. This regulatory and clinical push creates a direct pipeline for biomarker adoption.

Companion diagnostics is estimated to remain in the second position in the forecast period. The rise of companion diagnostics is directly associated with the wave of targeted therapies that require biomarker confirmation before use. It is now a regulatory requirement. Companion diagnostics are available and, in some cases, required to prescribe PARP inhibitors on-label for prostate cancer. Each new targeted approval creates a new diagnostic obligation.

Regional Insights

Asia Pacific Prostate Cancer Biomarkers Market Trends

Asia Pacific's growth is rooted in an increasingly aging population and healthcare systems that are just beginning to modernize their cancer screening capabilities. The region is expected to witness the fastest growth, boosted by increasing cancer awareness, improving healthcare infrastructure, and rising healthcare expenditure in China, India, and Japan. The demographic shift is substantial. One-quarter of Asia Pacific's population is anticipated to be aged 60 or older by 2050, fueling prostate cancer incidence and the requirement for extensible and non-invasive biomarker-based screening solutions.

China Prostate Cancer Biomarkers Market Trends

China's growth is being fueled by a rising incidence of prostate cancer, partly the result of urbanization, an aging population, and expanding PSA screening programs. The country’s Healthy China Action Plan (2019 to 2030) has emphasized PSA testing as a key early detection measure, with increasing efforts to promote screening in high-risk populations. However, the market is still in a formative phase. China does not yet have a national-level PSA screening policy, but is exploring screening strategies in economically developed regions. The government continues to foster approval of new drugs, introduce novel equipment, and support original research.

India Prostate Cancer Biomarkers Market Trends

India represents one of the most promising emerging opportunities in Asia Pacific, though the market is still developing. The Indian Council of Medical Research estimates that prostate cancer cases will increase by 25% between 2025 and 2030, bolstered by urbanization and changing dietary patterns. Prostate cancer accounts for 5.4% of cancers in Indian men, with annual cases potentially doubling by 2040. Metropolitan cities are already reporting high incidence rates due to lifestyle factors and improved awareness. On the supply side, the government plans to establish Day Care Cancer Centers in every district hospital, with 200 centers targeted for launch between 2025 and 2026. These are aimed at decentralizing cancer treatment and increasing demand for reliable biomarker-based testing.

North America Prostate Cancer Biomarkers Market Trends

In 2026, North America is predicted to dominate with a share of around 43.7% in 2026. This growth is attributed to a well-established clinical infrastructure, regulatory activity, and reimbursement support that no other region has matched. Regulatory agencies such as the FDA have been prolific in approving both standalone biomarker tests and companion diagnostics for prostate cancer. The American Urological Association’s (AUA) PSA Best Practice Statement mandates risk-based screening protocols, outlines biomarker interpretation thresholds, and recommends integration of novel biomarkers into clinical decision-making.

U.S. Prostate Cancer Biomarkers Market Trends

The U.S. is uniquely positioned due to high disease burden, institutional support, and a competitive commercial ecosystem. The pace of FDA activity has been particularly significant in 2025. Within a single year, the agency cleared ArteraAI Prostate (De Novo authorization), approved Cleveland Diagnostics' IsoPSA (premarket approval), cleared Ibex Prostate Detect (510(k)), and approved multiple companion diagnostics for PARP inhibitors in prostate cancer. This wave of regulatory approvals, combined with clinical guideline adoption, is pushing market standardization and reimbursement frameworks that bolster commercial uptake.

Europe Prostate Cancer Biomarkers Market Trends

Europe benefits from comprehensive public healthcare systems, structured cancer screening programs, and superior academic-industry collaboration in biomarker research. The market is being supported by the incorporation of high-technology diagnostic methods, including multiparametric MRI, next-generation sequencing, and liquid biopsy, to identify prostate cancer. In March 2025, for instance, BC Platforms joined the BRECISE initiative, a five-year Horizon Europe project running from 2025 to 2029. It aimed to boost precision oncology biomarkers for prostate and bladder cancers through multidisciplinary research co-funded by the Innovative Health Initiative.

Germany Prostate Cancer Biomarkers Market Trends

Germany stands out as Europe's most advanced market for prostate cancer biomarkers because of the intersection of high disease burden, superior industry presence, and a policy environment that supports precision diagnostics. Prostate cancer is the most frequently diagnosed malignancy among men in Germany. According to the World Cancer Research Fund, the country recorded 65,269 new cases of prostate cancer in 2022, with 18,015 deaths, making it one of Europe's highest-burden markets.

U.K. Prostate Cancer Biomarkers Market Trends

The U.K. has a distinctive position in Europe. It is an active research hub but lacks a national prostate cancer screening program. This creates both a challenge and an opportunity. Though PSA testing is not part of a national screening program, it is widely available through general practitioners, mainly for high-risk individuals. The country is also a frontrunner in clinical trials as well as research and development, with universities and research institutions actively working on prostate cancer diagnostics.

Competitive Landscape

The global prostate cancer biomarkers market is moderately fragmented. Large diagnostics and life sciences companies such as Roche, Exact Sciences, Bio-Techne, OPKO Health, and Myriad Genetics remain highly influential owing to their commercialized biomarker assays and global distribution networks. Companies providing unique tests such as 4Kscore, SelectMDx, ExoDx Prostate, ConfirmMDx, and Decipher are competing primarily on reducing unnecessary biopsies and improving detection of clinically significant prostate cancer.

Urine-based biomarkers have become one of the most competitive innovation segments as they provide non-invasive alternatives to biopsy. Liquid biopsy competition is accelerating steadily, especially in circulating tumor DNA (ctDNA), extracellular vesicles, and blood-based biomarker platforms. Companies are investing heavily in minimally invasive testing for early detection, treatment selection, and recurrence monitoring.

Key Industry Developments:

- In May 2026, Roche announced a definitive merger agreement to acquire PathAI for US$750 million upfront and up to US$300 million in milestone payments. The companies noted that combining PathAI's AI-based capabilities with Roche's existing companion diagnostics expertise would foster the discovery of new biomarkers.

- In April 2026, PanGIA Biotech published a peer-reviewed clinical study in Diagnostics demonstrating clinical validation of its urine-based liquid biopsy platform, the PanGIA Analysis System. The platform achieved 97.8% sensitivity across all Gleason grades and 97.3% specificity for high-grade cancers.

- In January 2026, Tempus AI launched Paige Predict, an AI-supported biomarker prediction solution for digital pathology. It analyzes H&E whole slide images to predict the likelihood of 123 biomarkers and oncogenic molecular pathways across 16 cancer types, including prostate cancer, using tissue from even scarce biopsy samples.

Companies Covered in Prostate Cancer Biomarkers Market

- Exact Sciences Corporation

- Myriad Genetics, Inc.

- Bio-Techne

- ExoDx

- OPKO Health, Inc.

- Mdxhealth

- Veracyte, Inc.

- Beckman Coulter, Inc.

- Nucleix

- DiaCarta

- Genomic Health

Frequently Asked Questions

The global prostate cancer biomarkers market is projected to be valued at US$6.4 billion in 2026.

The prostate cancer biomarkers market is expected to reach US$17.6 billion by 2033.

Increasing shift toward personalized medicine and surging research efforts for prostate cancer diagnosis are a few key market trends.

Protein biomarkers are expected to be the leading product type with a share of nearly 58.3% in 2026, owing to the rising demand for targeted therapies.

The prostate cancer biomarkers market is expected to grow at a CAGR of 15.6% from 2026 to 2033.

Exact Sciences Corporation, Myriad Genetics, Inc., Bio-Techne, and ExoDx are a few key market players.