- HVAC

- Point of Entry PFAS Treatment Systems Market

Point of Entry PFAS Treatment Systems Market Size, Share, and Growth Forecast, 2026 - 2033

Point of Entry PFAS Treatment Systems Market by Treatment Technology (Separation & Concentration Technologies, Destruction Technologies, Others), Core System Type (Reverse Osmosis Systems, Others), End-user, and Regional Analysis for 2026 - 2033

Point of Entry PFAS Treatment Systems Market Size and Trends Analysis

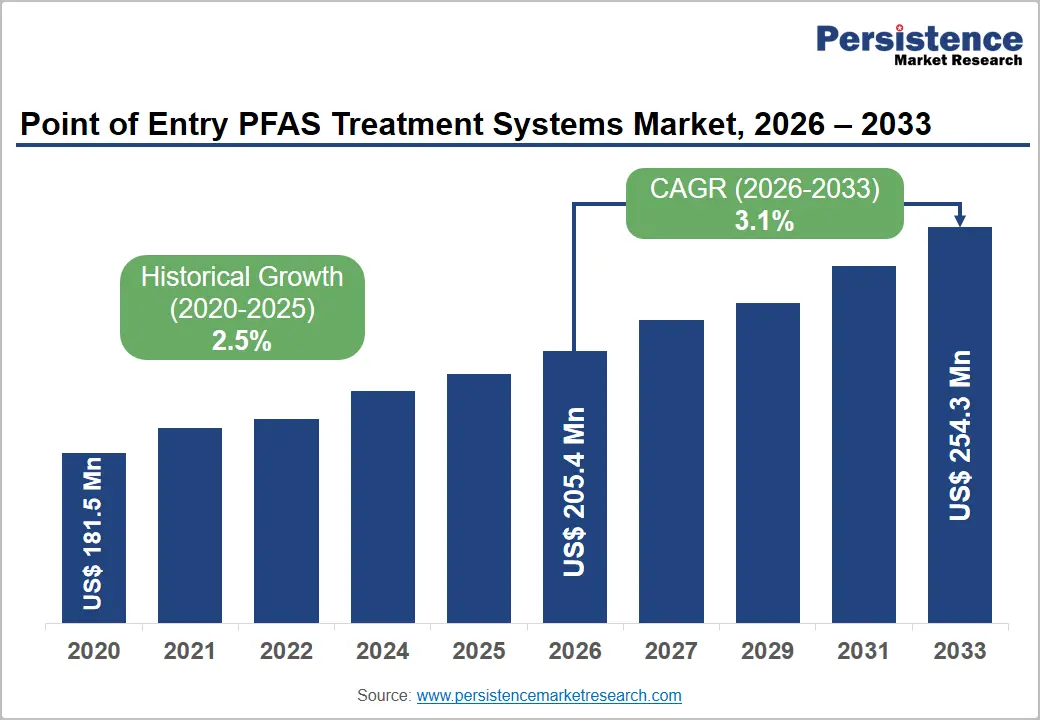

The global point of entry PFAS treatment systems market size is likely to be valued at US$205.4 million in 2026 and is expected to reach US$254.3 million by 2033, growing at a CAGR of 3.1% during the forecast period from 2026 to 2033, driven by the tightening of drinking water regulations for per- and polyfluoroalkyl substances (PFAS) across major regions.

Rising awareness of PFAS-related health and environmental concerns, coupled with enhanced monitoring requirements and increasing investments in water treatment infrastructure, is supporting demand for advanced treatment solutions. Point-of-entry PFAS treatment systems are gaining traction for their ability to provide building-wide water treatment, making them a preferred choice for municipalities, commercial establishments, industrial facilities, and institutional users seeking to ensure regulatory compliance and improve water quality.

Key Industry Highlights:

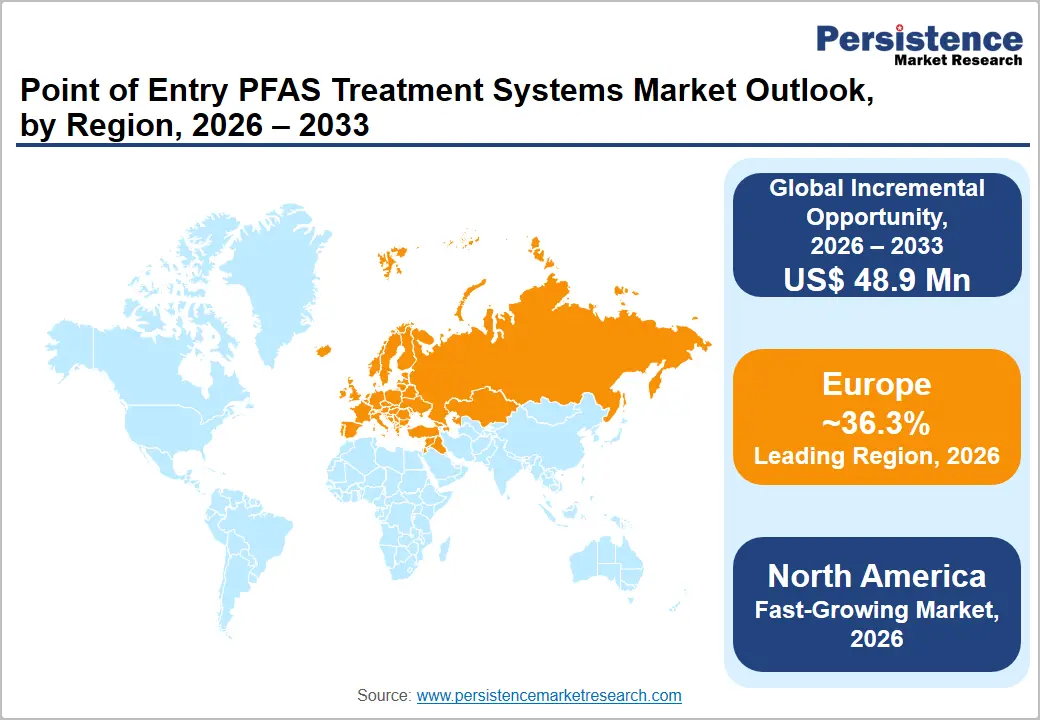

- Leading Region: Europe is projected to lead, accounting for approximately 36.3% of market revenue in 2026, supported by harmonized PFAS monitoring requirements, advanced water infrastructure, and stringent drinking water regulations.

- Fastest-growing Region: North America is projected to be the fastest-growing regional market through 2033, driven by expanding PFAS compliance requirements, large-scale investments in drinking water treatment infrastructure, and increasing adoption of point-of-entry filtration systems across municipal and commercial sectors.

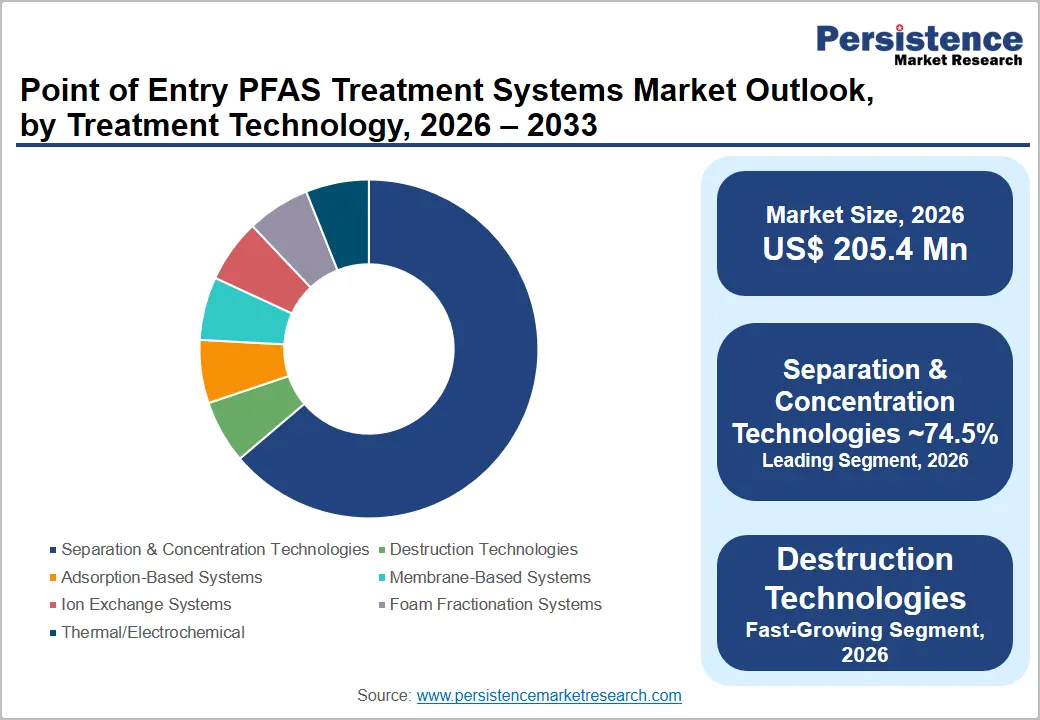

- Dominant Treatment Technology: Separation and concentration technologies are anticipated to account for approximately 74.5% of market share in 2026, maintaining leadership due to proven treatment performance, regulatory acceptance, and widespread deployment of activated carbon, membrane filtration, ion exchange, and foam fractionation systems.

- Leading Core System Type: Reverse osmosis systems are anticipated to hold approximately 30.7% market share in 2026, supported by their high PFAS removal efficiency, broad contaminant-reduction capabilities, and growing adoption across residential, commercial, and institutional applications.

DRO Analysis

Driver - Stringent PFAS Regulations and Drinking Water Compliance Requirements

The implementation of stricter PFAS regulations across North America and Europe remains the primary driver of the Point of Entry PFAS Treatment Systems market. Regulatory agencies have established enforceable limits for multiple PFAS compounds in drinking water, compelling utilities, commercial facilities, and institutional users to deploy advanced treatment solutions. Public water systems are increasingly required to monitor PFAS concentrations, report findings, and implement corrective actions when contamination exceeds permissible thresholds.

These regulatory developments are transforming PFAS treatment from an environmental consideration into a mandatory infrastructure investment. Municipal utilities, schools, healthcare facilities, and commercial property operators are adopting POE treatment systems to ensure compliance while reducing long-term operational risks. The growing emphasis on public health protection and drinking water quality is expected to sustain demand throughout the forecast period.

Advancements in Treatment Technologies and System Reliability

Continuous improvements in filtration and separation technologies are supporting broader market adoption. Activated carbon, ion exchange resins, reverse osmosis, and nanofiltration systems have demonstrated high PFAS removal efficiencies under diverse operating conditions. Technology providers are also enhancing system automation, monitoring capabilities, and maintenance management, improving operational reliability and reducing lifecycle costs.

The availability of modular and scalable treatment solutions has expanded the addressable market by enabling deployment across residential communities, commercial facilities, and industrial sites. Enhanced treatment performance, combined with increasing certification and validation standards, has strengthened customer confidence and accelerated purchasing decisions. As technology continues to mature, operators are increasingly selecting integrated treatment platforms capable of delivering both compliance and operational efficiency.

Restraint - High Capital Investment and Operational Costs

Despite growing demand, the market faces challenges associated with the high lifecycle cost of PFAS treatment systems. Installation expenses typically include engineering design, equipment procurement, site preparation, commissioning, and regulatory verification. Beyond initial investments, operators must account for media replacement, membrane maintenance, monitoring requirements, and disposal of PFAS-containing waste streams.

Smaller municipalities, rural communities, and budget-constrained facilities often face financial barriers when implementing advanced treatment technologies. Cost considerations can delay procurement decisions and encourage phased deployment strategies. In addition, system performance depends on source water quality, contaminant concentrations, and operational expertise, increasing the complexity of project planning and long-term asset management.

Opportunities - Expansion of Service-Based Compliance Solutions

A significant opportunity exists in service-integrated treatment models that combine equipment, monitoring, maintenance, regulatory reporting, and media management. As PFAS regulations become more complex, end users increasingly seek comprehensive solutions that simplify compliance obligations and reduce operational burden.

Service-based business models generate recurring revenue streams while strengthening customer retention. Providers capable of delivering complete lifecycle support, including testing, performance optimization, media replacement, and waste management, are well-positioned to capture growing demand from municipal, commercial, and industrial customers.

Growing Demand for Industrial PFAS Source Control

Industrial facilities represent a substantial opportunity for market expansion. Manufacturers operating in sectors such as chemicals, electronics, aerospace, textiles, and metal processing are under increasing pressure to manage PFAS contamination at the source before it enters municipal water systems or wastewater networks.

The shift toward upstream treatment strategies creates opportunities for technology providers offering integrated solutions that combine industrial pretreatment, point-of-entry filtration, and waste management services. Industrial customers are increasingly prioritizing proactive contamination control to reduce environmental liabilities, improve regulatory compliance, and support sustainability objectives.

Category-wise Analysis

Treatment Technology Insights

Separation and concentration technologies are anticipated to account for approximately 74.5% of the market share in 2026. Their leadership is supported by proven removal efficiency, regulatory acceptance, and widespread commercial deployment. Key technologies include adsorption-based systems, membrane filtration, ion exchange, and foam fractionation. Examples include granular activated carbon (GAC) systems used by municipal utilities, reverse osmosis units installed in commercial buildings, and ion exchange resin systems deployed in schools and healthcare facilities. Their scalability, reliability, and compatibility with existing treatment infrastructure continue to support market leadership.

Destruction technologies are projected to be the fastest-growing treatment segment during the forecast period as end users seek permanent PFAS elimination rather than contaminant transfer. These technologies address the disposal challenges associated with spent carbon, resins, and concentrated waste streams. Examples include plasma-based PFAS destruction systems for industrial wastewater, electrochemical oxidation units at remediation sites, and supercritical water oxidation (SCWO) technologies under pilot-scale deployment for hazardous waste treatment. Growing emphasis on lifecycle PFAS management is expected to accelerate adoption across industrial and environmental remediation applications.

Core System Type Insights

Reverse osmosis systems are anticipated to hold approximately 30.7% of the market share in 2026. Their ability to remove PFAS alongside dissolved solids, heavy metals, and other contaminants has made them a preferred solution for residential, commercial, and institutional users. Examples include whole-building reverse osmosis systems installed in schools and hospitals, as well as commercial PFAS filtration systems used in office complexes and hospitality facilities. Their consistent treatment performance and broad contaminant removal capabilities continue to drive adoption.

Hybrid multi-stage systems are expected to register the fastest growth through 2033 due to their ability to combine multiple treatment technologies within a single platform. These systems typically integrate activated carbon, ion exchange, reverse osmosis, and digital monitoring capabilities to maximize PFAS removal efficiency. Examples include municipal treatment systems combining GAC and reverse osmosis, industrial facilities using ion exchange with membrane polishing, and modular packaged units equipped with real-time monitoring sensors. Their flexibility and ability to address varying contamination levels are driving rapid market acceptance.

Regional Insights

North America Point of Entry PFAS Treatment Systems Market Trends

North America is expected to be the fastest-growing regional market during the forecast period. The region benefits from a mature water treatment industry, extensive regulatory oversight, and significant investments in drinking water infrastructure. Growing concerns regarding PFAS contamination, coupled with mandatory monitoring and remediation requirements, continue to drive demand for point-of-entry treatment systems across municipal, commercial, and institutional applications.

U.S. Point of Entry PFAS Treatment Systems Market Trends

The U.S. represents the largest market in North America and serves as the primary growth engine for the region. Federal and state agencies have expanded PFAS testing and compliance requirements, encouraging municipalities, healthcare facilities, educational institutions, and commercial property owners to invest in advanced treatment solutions. The country also hosts a strong ecosystem of filtration technology providers, engineering firms, and environmental service companies, supporting continuous innovation in PFAS treatment technologies.

Canada Point of Entry PFAS Treatment Systems Market Trends

Canada is witnessing increasing adoption of PFAS treatment systems as provincial authorities strengthen drinking water quality standards and contamination monitoring programs. Municipal utilities are investing in upgraded filtration infrastructure, while industrial operators are implementing treatment systems to reduce environmental liabilities and comply with evolving regulatory expectations.

The region continues to attract investment in treatment technology development, digital monitoring platforms, and large-scale remediation projects. Companies are expanding manufacturing capacity and service networks to capitalize on growing long-term demand.

Europe Point of Entry PFAS Treatment Systems Market Trends

Europe accounted for approximately 36.3% of the market share in 2026, making it the leading regional market. Growth is supported by stringent environmental regulations, advanced water infrastructure, and increasing public awareness of PFAS-related health and environmental concerns. Harmonized regulatory frameworks across European countries are creating a consistent approach to PFAS monitoring, reporting, and remediation.

Germany Point of Entry PFAS Treatment Systems Market Trends

Germany represents one of Europe's largest markets due to its strong industrial base and proactive environmental policies. Municipal utilities and industrial facilities are investing in advanced PFAS treatment technologies to meet increasingly stringent water quality requirements. The country's emphasis on environmental sustainability continues to support long-term market growth.

U.K. Point of Entry PFAS Treatment Systems Market Trends

The U.K. is strengthening PFAS monitoring and drinking water management practices through enhanced regulatory oversight. Water utilities and commercial facility operators are investing in treatment infrastructure to ensure compliance and protect public health. Growing focus on water quality resilience is expected to create sustained demand for POE treatment systems.

France Point of Entry PFAS Treatment Systems Market Trends

France is actively addressing PFAS contamination through expanded monitoring programs and environmental protection initiatives. Municipal authorities are modernizing water treatment facilities, while industrial operators are implementing source-control strategies to reduce PFAS emissions and contamination risks.

Spain Point of Entry PFAS Treatment Systems Market Trends

Spain's market growth is supported by increasing investments in water infrastructure modernization and sustainable water management programs. The country is prioritizing treatment technologies that improve drinking water quality while addressing emerging contaminants, including PFAS compounds.

Across Europe, investment activity remains focused on advanced treatment technologies, infrastructure upgrades, and service-based compliance solutions. Companies with localized manufacturing capabilities and comprehensive lifecycle support services are well-positioned to benefit from market expansion.

Asia Pacific Point of Entry PFAS Treatment Systems Market Trends

Asia Pacific is emerging as a significant growth market for point-of-entry PFAS treatment systems. Rapid industrialization, urbanization, and rising investments in water infrastructure are creating favorable conditions for market expansion. While regulatory frameworks are still evolving in many countries, increasing environmental awareness and industrial compliance requirements are encouraging the adoption of advanced treatment technologies.

China Point of Entry PFAS Treatment Systems Market Trends

China represents the largest market in Asia Pacific, supported by its extensive manufacturing base and growing emphasis on environmental management. Government initiatives focused on water quality improvement and industrial pollution control are driving investments in PFAS monitoring and treatment infrastructure. Industrial facilities remain the primary source of demand.

Japan Point of Entry PFAS Treatment Systems Market Trends

Japan continues to invest in advanced water treatment technologies and environmental protection programs. The country's strong technological capabilities and focus on high-quality water infrastructure support the adoption of sophisticated PFAS treatment solutions across municipal and commercial applications.

India Point of Entry PFAS Treatment Systems Market Trends

India is gradually expanding water quality monitoring programs and strengthening investments in drinking water infrastructure. Rapid urbanization, industrial growth, and increasing awareness of emerging contaminants are creating opportunities for PFAS treatment technology providers. Demand is expected to be concentrated in industrial facilities, educational campuses, healthcare institutions, and commercial developments.

Competitive Landscape

The global point of entry PFAS treatment systems market is characterized by a fragmented competitive landscape comprising multinational water technology companies, specialized filtration providers, media manufacturers, and regional service providers. Competition is based primarily on treatment performance, regulatory compliance capabilities, lifecycle cost optimization, technological innovation, and after-sales service support.

Leading companies are prioritizing technological innovation, service integration, geographic expansion, and regulatory expertise. Organizations increasingly offer comprehensive solutions encompassing testing, treatment, monitoring, maintenance, and waste management. The transition toward recurring service revenue models and compliance-focused offerings is becoming a defining trend across the competitive landscape.

Key Industry Developments

- In June 2025, Veolia announced the European launch of its patented Drop® technology for PFAS destruction.

- In May 2025, Culligan International launched its new Culligan with ZeroWater Technology product line, featuring advanced five-stage filtration certified to remove total PFAS and other emerging contaminants.

Companies Covered in Point of Entry PFAS Treatment Systems Market

- Veolia Water Technologies

- Pentair plc

- Calgon Carbon Corporation

- DuPont Water Solutions

- Culligan International

- Xylem Inc.

- O. Smith Corporation

- Watts Water Technologies, Inc.

- BWT AG

- EcoWater Systems LLC

- Evoqua Water Technologies LLC

- Newterra Ltd.

- Kuraray Co., Ltd.

- Purolite Corporation

- Aquasana, Inc.

- 3M Company

Frequently Asked Questions

The global point-of-entry (POE) PFAS treatment systems market is anticipated to be valued at US$205.4 million in 2026.

The projected point-of-entry PFAS treatment systems market is expected to reach approximately US$254.3 million by 2033.

Key market trends include increasing PFAS regulatory enforcement, growing adoption of reverse osmosis and hybrid treatment systems, rising demand for service-based compliance solutions, expansion of industrial PFAS source-control programs, and advancements in PFAS destruction technologies.

Separation and concentration technologies lead the market, accounting for an anticipated 74.5% market share, driven by the widespread adoption of activated carbon, membrane filtration, ion exchange, and foam fractionation systems.

The point-of-entry PFAS treatment systems market is projected to expand at a CAGR of 3.1% between 2026 and 2033.

Major companies include Veolia Water Technologies, Pentair plc, Calgon Carbon Corporation, DuPont Water Solutions, and Xylem Inc.