- Plastics, Polymers & Resins

- Plastic Pipe Market

Plastic Pipe Market Size, Share, and Growth Forecast, 2026 - 2033

Plastic Pipe Market by Material Type (Polyvinyl Chloride (PVC) (Chlorinated PVC (CPVC), Unplasticised PVC (PVC-U), Molecular Oriented PVC (PVC-O), Modified PVC (PVC-M, PVC-HI, PVC-A)), Polyethylene (PE) (HDPE, LDPE), Polypropylene (PP), Polybutylene (PB), Acrylonitrile Butadiene Styrene (ABS), Fibreglass, Misc., Application (Liquid Conduits, Gas Conduits, Others) Industry, and Regional Analysis for 2026 - 2033

Plastic Pipe Market Size and Trends Analysis

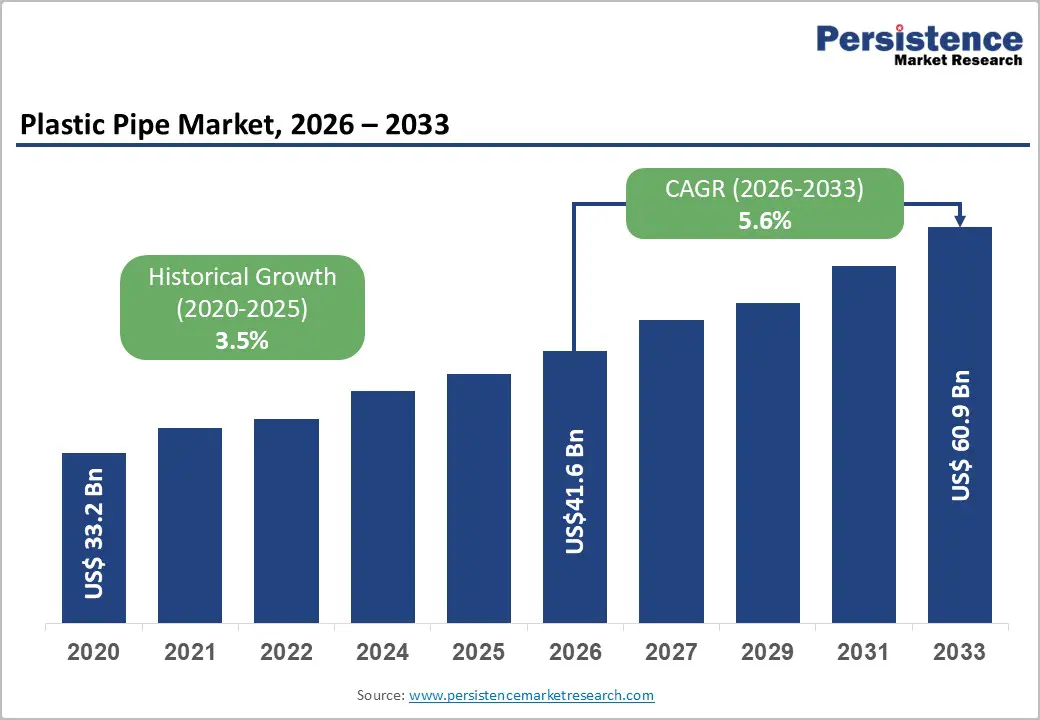

The global plastic pipe market size is likely to be valued at US$ 41.6 billion in 2026 and is projected to reach US$ 60.9 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033. Sustained government investment in water supply, wastewater management, urban housing, and agricultural irrigation infrastructure across both emerging and mature economies is the central force underpinning this trajectory.

Plastic pipes are widely adopted over conventional metal alternatives due to their superior corrosion resistance, lower installation and maintenance costs, and extended service life across diverse applications. A historical CAGR of 3.5% between 2020 and 2025 reflects the market's stable, foundational performance, with the accelerated forecast rate signalling structurally strengthening demand driven by policy-backed construction programs, the adoption of precision agriculture, and the expansion of digital infrastructure globally.

Key Industry Highlights:

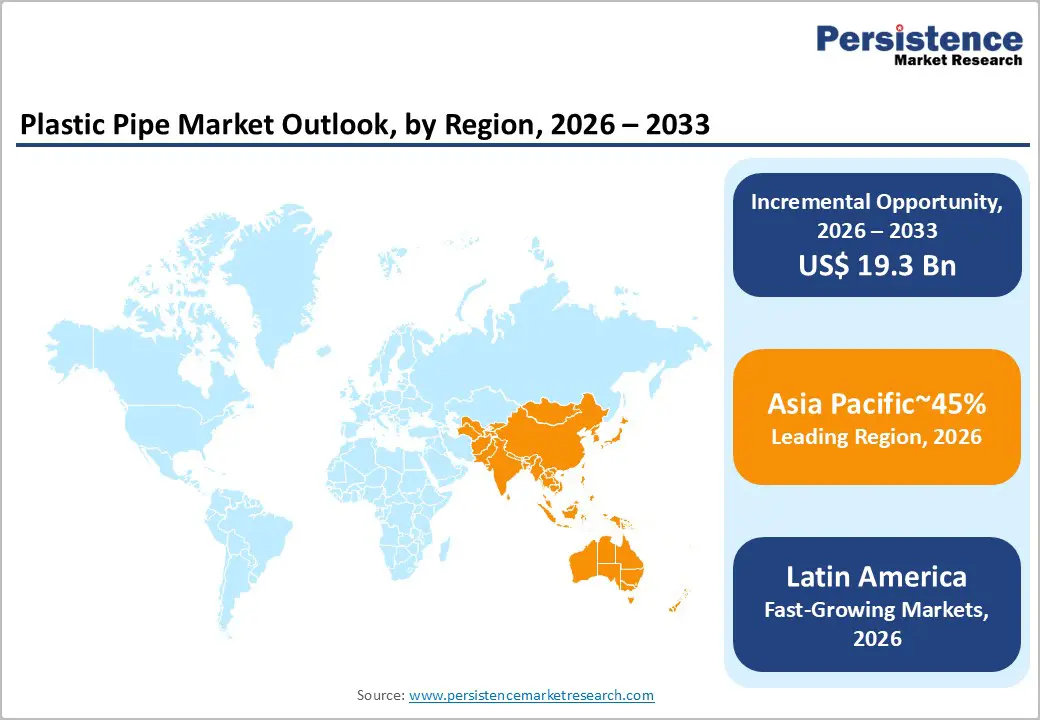

- Asia Pacific Market Leadership: Asia Pacific dominates the Plastic Pipe Market with approximately 45% share, driven by rapid urbanisation, government-led infrastructure spending, and large-scale water supply and irrigation projects across China and India.

- North America Strong Infrastructure Demand: North America accounts for nearly 23% market share, supported by high construction spending, municipal water infrastructure replacement programs, and strong adoption of PVC and HDPE pipes in the United States.

- Europe Regulatory-Driven Growth: Europe holds around 20% share of the global market, driven by strict water management regulations, wastewater treatment upgrades, and investments in modern gas and digital infrastructure networks.

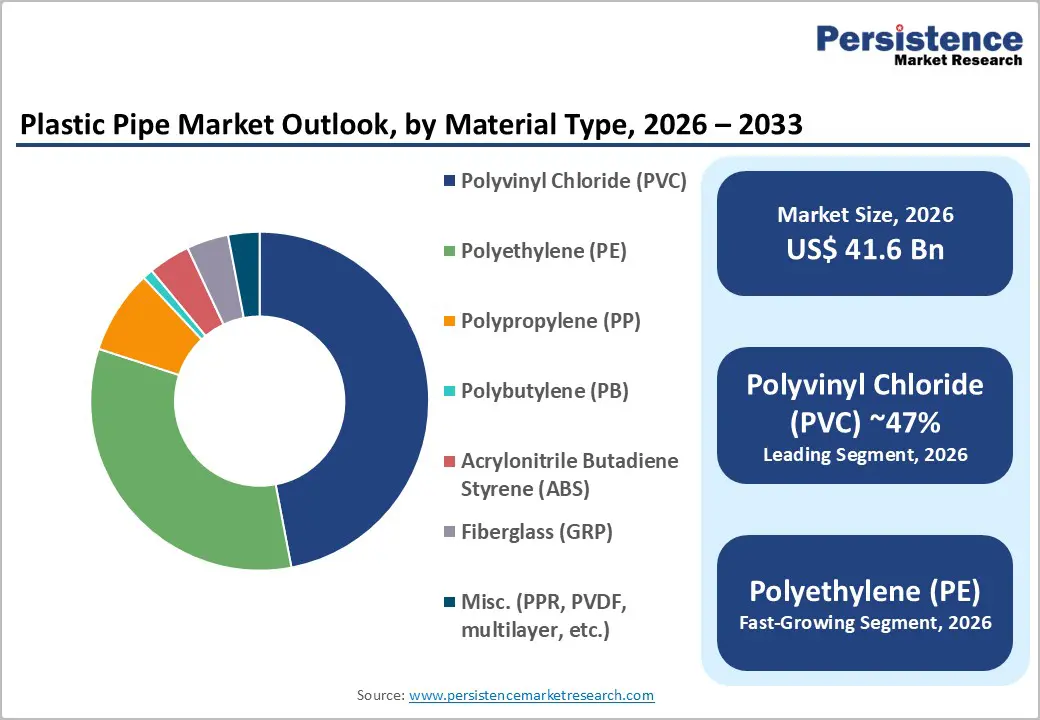

- PVC Leading Material Segment: Polyvinyl Chloride (PVC) leads the Plastic Pipe Market with nearly 47% share, owing to its cost efficiency, durability, and extensive usage across construction, water supply, drainage, and agricultural applications.

- Polyethylene Fastest-Growing Material: Polyethylene (PE), particularly HDPE, represents the fastest-growing material segment, supported by rising demand in gas distribution, water transmission pipelines, and modern irrigation systems.

- Building & Construction Dominant End-user: Building and construction accounts for about 39% of market demand, reflecting strong global activity in residential housing, commercial infrastructure, and urban utility networks.

| Key Insights | Details |

|---|---|

| Market Plastic Pipe Size (2026E) | US$ 41.6 Bn |

| Market Value Forecast (2033F) | US$ 60.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.5% |

Market Dynamics

Drivers - Government Infrastructure Expenditure and Urbanisation-Led Construction Demand

Escalating government capital investment in housing, urban infrastructure, and public works is one of the most durable structural drivers for the Plastic Pipe Market worldwide. In India, the central government raised capital expenditure by 11.1% to US$ 133 billion in FY 2024, equivalent to 3.4 per cent of GDP, directing substantial allocations toward water supply networks, sanitation infrastructure, and urban development. The Pradhan Mantri Awas Yojana Urban (PMAY-U) program has sanctioned 1.18 crore houses, with 86.6 lakh already completed, each requiring extensive plastic pipe networks for plumbing, drainage, and water conveyance.

In the United States, the construction sector recorded total annual spending of US$2.2 trillion in 2024, representing 4.5% of GDP, while 1.6 million new homes were built in a single year. The industry employs over 8.2 million people, reflecting a construction ecosystem of exceptional scale that generates high-volume, recurring demand for PVC and HDPE pipe systems across residential, commercial, and industrial segments. These converging public and private capital flows establish urbanisation-driven construction as the most consistent demand anchor for the global Plastic Pipe Market.

Agricultural Modernization and Irrigation Infrastructure Development

The global imperative to improve water-use efficiency in food production is driving sustained, policy-backed procurement demand for plastic pipe systems, particularly HDPE and PVC irrigation pipes. According to the Food and Agriculture Organisation (FAO), agriculture accounts for approximately 70% of total global freshwater withdrawals, creating urgent government pressure to transition from flood-based irrigation to drip and sprinkler systems that rely on plastic pipe networks.

India's Pradhan Mantri Krishi Sinchayee Yojana (PMKSY) program allocated US$ 7.7 billion to expand irrigated farmland, directly accelerating PVC and HDPE pipe adoption across high-volume agricultural states. India's Jal Jeevan Mission targeting tap water connectivity for all rural households generated a 28% uplift in polyethylene pipe demand between 2020 and 2023 driven by the material's leak-proof design and suitability for installation in rugged terrain. In Southeast Asia, governments in Thailand, Vietnam, and Indonesia are mandating the adoption of modern irrigation technology to improve crop yields, with plastic pipes preferred for their lightweight handling, chemical resistance, and cost-effectiveness. This convergence of water scarcity pressures, food security mandates, and the adoption of precision agriculture is embedding agricultural demand as a structurally significant driver of the Plastic Pipe Market through the forecast horizon.

Telecommunications and Digital Infrastructure Conduit Demand

The rapid global expansion of digital connectivity infrastructure is creating a high-value demand stream for plastic conduit pipes used in fibre-optic cable protection, 5G antenna groundworks, and data centre cable management. According to the International Telecommunication Union (ITU), global internet usage reached approximately 6 billion users, representing 74% of the world's population in 2025, up from 60 percent in 2020, with nearly 1.3 billion new users coming online during these five years.

In India, gross telecom revenue reached US$43.42 billion in FY25, with broadband subscribers reaching 979 million connections. Cumulative FDI inflows into India's telecom sector reached US$40.07 billion between April 2000 and March 2025, making it the fourth-largest FDI destination nationally. Large-scale 5G rollouts and the BharatNet fibre expansion program create a recurring procurement pipeline for plastic conduit pipes in rural and urban deployment zones.

At the European Union level, the information and communication services sector comprised approximately 1.4 million enterprises employing nearly 7.2 million people, generating approximately EUR 667 billion in value added, with Germany alone accounting for 22.8 percent of the EU sectoral value added. This scale of digital infrastructure investment across major economies positions telecom conduit as a structurally significant, rapidly accelerating demand segment within the Plastic Pipe Market.

Restraint - Raw Material Price Volatility and Energy Cost Pressures

The primary raw materials used in plastic pipe production, including PVC resin, polyethylene, and polypropylene, are petroleum-derived and subject to significant price volatility tied to global crude oil dynamics. According to the International Energy Agency (IEA), global oil production capacity is set to expand by 4.6 mb/d through non-OPEC+ producers. Yet, structural market transitions and geopolitical tensions continue to generate feedstock price unpredictability.

Plastics Europe explicitly identified soaring energy and feedstock prices as a persistent threat to industry competitiveness, complicating long-term pricing strategies for plastic pipe manufacturers and limiting margin stability, particularly for mid-tier producers.

Opportunity - Middle East Giga-Project Pipeline and Gulf Diversification Programs

The Gulf Cooperation Council region's unprecedented concentration of giga-scale construction programs represents a structurally funded, long-duration commercial opportunity for global plastic pipe manufacturers. Saudi Arabia's Vision 2030 program encompasses landmark infrastructure and real estate projects, including NEOM, The Line, King Salman Park, and Diriyah Gate, alongside preparations for EXPO 2030 and the 2034 FIFA World Cup. These developments collectively constitute some of the most capital-intensive construction programs in modern history, each requiring massive volumes of plastic pipes for water distribution, drainage, fire protection, and HVAC systems. Office construction costs in Riyadh average US$ 2,266 per m², while Dubai's high-rise residential sector averages US$ 1,334 per m², reflecting sustained procurement capacity.

According to the International Monetary Fund (IMF), Middle East GDP is projected to grow by 4.2% in 2025, outpacing many emerging-market peers. Falling central bank interest rates and strong state-backed capital deployment are accelerating residential, hospitality, leisure, and data center construction across the UAE and Saudi Arabia. For participants in the Plastic Pipe Market seeking geographic diversification beyond saturated markets, the Middle East represents a government-priority, legally funded demand source with multi-year procurement cycles and a growing base of international contractors with established preferences for plastic pipe specifications.

Plastic Circularity and Sustainable Material Innovation

The convergence of tightening environmental regulations and growing institutional ESG investment frameworks is creating a meaningful commercial opportunity for Plastic Pipe Market participants that advance circular-economy-aligned product development. The World Bank (IBRD) introduced a seven-year US$100 million principal-protected bond to finance plastic waste reduction projects in Ghana and Indonesia, linking investor returns to Plastic Waste Collection Credits, Plastic Waste Recycling Credits, and Verified Carbon Units. This innovative financing model establishes a replicable template for scaling investment in circular plastic infrastructure across developing economies.

Plastics Europe confirmed that chemical recycling is essential to complement mechanical recycling, as demand for recyclates currently exceeds supply, and that non-fossil-based plastics already represented 12.4% of European production, aligning with the EU's 20% non-fossil carbon target for 2030. Advanced Drainage Systems (ADS) demonstrated the commercial viability of this approach by purchasing 540 million pounds of recycled material in fiscal 2024, with a stated goal of reaching 1 billion pounds annually, establishing recycled content as both a cost-competitive and sustainability-differentiating strategy.

Companies in the Plastic Pipe Market investing in recycled-content pipe formulations and certified low-carbon products are positioned to capture premium specification mandates from public-sector and multinational private-sector procurement programs globally.

Category-wise Analysis

Material Type Insights

Polyvinyl Chloride PVC commands a dominant 47% share of the plastic pipe market by material type, a position sustained by its unmatched combination of product versatility, cost-effectiveness, and proven performance across a broad spectrum of end-use applications. PVC encompasses multiple advanced sub-variants, with Chlorinated PVC (CPVC) serving high-temperature hot water systems, Unplasticised PVC or PVC-U addressing pressure water mains and drainage networks, Molecular Oriented PVC or PVC-O providing high-strength performance for transmission main applications, and Modified PVC variants including PVC-M, PVC-HI, and PVC-A delivering enhanced impact and chemical resistance.

Continuous advancements in PVC formulations have improved flexibility and broadened application suitability across diverse soil and water chemistry environments. India alone imported 3.2 million metric tons of PVC from global sources, with construction and agricultural applications accounting for the dominant share of this volume, reflecting PVC's irreplaceable role in supplying high-growth emerging markets where cost-efficiency and infrastructure development speed are overriding specifications.

Polyethylene PE pipes, encompassing High-Density Polyethylene (HDPE) and Low-Density Polyethylene (LDPE) grades, represent the fastest-growing material segment in the Plastic Pipe Market, driven by expanding adoption across water supply, gas distribution, sewage conveyance, and agricultural irrigation applications. HDPE's superior high-pressure resistance, flexibility, and performance across extreme temperature ranges make it the preferred specification for gas distribution networks, large-diameter water transmission mains, and trenchless rehabilitation projects where minimising civil disruption is essential. In agricultural contexts, HDPE is the dominant pipe material in drip and sprinkler irrigation systems deployed by governments across India, Southeast Asia, and South America. India's Jal Jeevan Mission generated a 28% uplift in polyethylene pipe demand between 2020 and 2023, with the material's leak-proof design performance in rugged terrains driving specification preference.

Industry Insights

Building and construction commands the leading end-use position with 39% of the Global Plastic Pipe Market, reflecting the fundamental and irreplaceable role of plastic pipe systems in residential plumbing, commercial HVAC networks, drainage, fire suppression, and electrical conduit applications across global construction activity.

In the United States, the construction sector spent US$2.2 trillion in 2024, employed over 8.2 million workers, and delivered 1.6 million new homes. In the European Union, construction output demonstrated measurable resilience, with Spain recording annual construction output growth of 11.2%, Czechia at 9.7 percent, and Slovakia at 5.8% in 2024. India's government-driven housing push through PMAY-U, combined with the country's real estate market trajectory toward US$5.8 trillion by 2047, with logistics and warehousing infrastructure expected to require 159 million square feet of new space, firmly positions construction demand as the defining procurement anchor for the Plastic Pipe Market globally through the forecast period.

Agriculture is the fastest-growing end-use segment for plastic pipes, propelled by global policy-level intensification of irrigation modernisation and precision water management programs across major food-producing nations. The FAO confirms agriculture consumes approximately 70% of global freshwater withdrawals, creating urgent pressure for governments to mandate a transition from flood-based irrigation toward drip and sprinkler systems that depend entirely on plastic pipe networks.

Regional Insights and Trends

Asia Pacific Plastic Pipe Market Trends

Asia Pacific accounts for approximately 45% of the global market, establishing the region as the world's largest and most strategically significant plastic pipe consumption base. China maintains the highest country-level share, serving as both the world's leading manufacturer and the largest consumer of plastic pipes, with strong domestic demand anchored by urbanisation, infrastructure investment, and construction-sector activity, projected to sustain China's regional leadership through the forecast horizon. India represents one of the region's highest-growth individual markets, driven by government capital expenditure of US$ 133 Billion in FY 2024 to 25. India imported 3.2 million metric tons of PVC from global sources, with demand concentrated across construction and agricultural pipe applications.

The country's Jal Jeevan Mission generated a 28% increase in polyethene pipe demand, while the Indian plastic pipe market is projected to register a CAGR of 7.2% in the forecast period. Japan represents a technically mature, stable market sustaining replacement activity across ageing water and gas distribution networks, projected to register a regional CAGR of 5.9%. South Korea continues to invest in smart city infrastructure and advanced water management systems, creating demand for high-performance specifications. The region's manufacturing cost advantages, demographic-driven construction demand, and overlapping government water and agricultural infrastructure programs create a structurally reinforced foundation for sustained market leadership through 2033.

North America Plastic Pipe Market Trends

North America commands approximately 23% of the Global Plastic Pipe Market, with the United States representing the dominant national driver. Total U.S. construction sector spending reached US$ 2.2 trillion in 2024, equivalent to 4.5 per cent of GDP, with the industry employing over 8.2 million workers and delivering 1.6 million new homes in a single year, generating a sustained high-volume baseline demand for PVC, HDPE, and CPVC pipe systems.

Federal mandates accelerating lead service line replacement across municipal water utilities are creating a significant and legally defined procurement wave for corrosion-resistant plastic pipes, with large-diameter PVC-U and PVC-O pipe specifications gaining specification traction for transmission main applications across state and municipal programs. The integration of smart water network technologies within U.S. utilities is driving specification upgrades requiring NSF-certified plastic pipe products, elevating average transaction values for market participants. Advanced Drainage Systems (ADS) issued its fiscal 2024 sustainability report, confirming it purchased 540 million pounds of recycled plastic material, making it one of North America's largest plastic recyclers, and reinforcing the region's position as a center of sustainable pipe product development. Canada's remote community clean water programs further support demand in off-grid and rural contexts, rounding out North America's broad and structurally stable plastic pipe market profile.

Europe Plastic Pipe Market Trends

Europe accounts for approximately 20% of the Global Plastic Pipe Market, characterised by strong regulatory frameworks, elevated infrastructure quality standards, and increasing investment in water, wastewater, and digital connectivity systems. According to Eurostat, EU construction output in 2024 showed measurable activity divergence, reflecting meaningful geographic variation in regional demand dynamics, while Poland and Romania experienced short-term pullbacks.

The European Union's Urban Wastewater Treatment Directive recast and the revised Drinking Water Directive are mandating systemic water network upgrades across member states, generating regulated procurement demand for certified plastic pipe systems. The United Kingdom is actively investing in wastewater network development and gas distribution infrastructure, with growing plastic pipe specification for HDPE and PVC systems.

Competitive Landscape

The global plastic pipe market is moderately fragmented, with a mix of large multinational manufacturers and numerous regional producers competing across construction, water infrastructure, irrigation, and industrial applications. A few global players maintain strong technological capabilities, extensive product portfolios, and broad distribution networks, allowing them to influence pricing, innovation, and large infrastructure projects. Key companies shaping the competitive environment include JM Eagle, Aliaxis, Sekisui Chemical Co., Ltd., China Lesso Group Holdings Limited, and Advanced Drainage Systems. In addition, companies such as Wienerberger AG are strengthening their positions through acquisitions and infrastructure-focused solutions.

Competition in the market is largely driven by product innovation in PVC, HDPE, and PEX pipes, by the expansion of manufacturing capacities, and by strategic mergers and acquisitions to strengthen regional presence. As infrastructure investments and water management projects increase globally, leading players are also focusing on sustainable materials and advanced pipe technologies to maintain a competitive advantage.

Key Developments:

- In July 2025, Sekisui Chemical Co., Ltd. announced progress in developing PFAS-free plastic pipe materials for ultrapure water applications in advanced semiconductor manufacturing, introducing a special olefin resin pipe technology that can reduce CO2 emissions during manufacturing by about 80% compared to conventional fluorocarbon resin pipes.

- In June 2025, Wienerberger AG announced the acquisition of MFP Sales Ltd to strengthen its presence in the Irish and UK markets, expanding its drainage, ducting, and PVC piping solutions portfolio for construction and infrastructure applications.

- In June 2023, Aliaxis completed the acquisition of the manufacturing division of Valencia Pipe Company, integrating it into its North American IPEX business to expand its U.S. manufacturing footprint and strengthen its portfolio of ABS, PVC, and MDPE plastic pipe systems.

Companies Covered in Plastic Pipe Market

- Aliaxis Group

- Sekisui Chemical Co., Ltd.

- Wienerberger AG

- Orbia (formerly Mexichem SAB de CV)

- JM Eagle, Inc.

- Astral Limited (Astral Poly Technik Ltd.)

- China Lesso Group Holdings Ltd.

- Geberit AG

- Nan Ya Plastics Corporation

- Finolex Industries Ltd.

- Georg Fischer Ltd.

- Advanced Drainage Systems, Inc.

- Supreme Industries Ltd.

- Genuit Group plc (formerly Polypipe Group plc)

- AGRU Kunststofftechnik GmbH

Frequently Asked Questions

The global Plastic Pipe Market is projected to be valued at US$ 41.6 Bn in 2026.

The Polyvinyl Chloride (PVC) Pipe segment is expected to account for approximately 47% of the Global Plastic Pipe Market by Material Type in 2026.

The market is expected to witness a CAGR of 5.6% from 2026 to 2033.

The Global Plastic Pipe Market growth is driven by rising government infrastructure and housing investments, expanding irrigation and agricultural modernisation programs, and the rapid deployment of telecom and digital connectivity infrastructure worldwide.

Key opportunities in the Plastic Pipe Market include large-scale Middle East infrastructure mega-projects and growing demand for sustainable, recycled-content plastic pipe solutions driven by circular economy and ESG initiatives.

Key players in the Plastic Pipe Market include JM Eagle, Aliaxis, Sekisui Chemical Co., Ltd., China Lesso Group Holdings Limited, and Advanced Drainage Systems and Wienerberger AG.