- Renewable Energy

- Pipeline Maintenance Service Market

Pipeline Maintenance Service Market Size, Share, and Growth Forecast, 2026 - 2033

Pipeline Maintenance Service Market by Service Type (Inspection & Testing, Repair & Rehabilitation, Others), Application (Oil & Gas Pipelines, Water & Wastewater, Others), Pipeline Location, and Regional Analysis for 2026 - 2033

Pipeline Maintenance Service Market Size and Trends Analysis

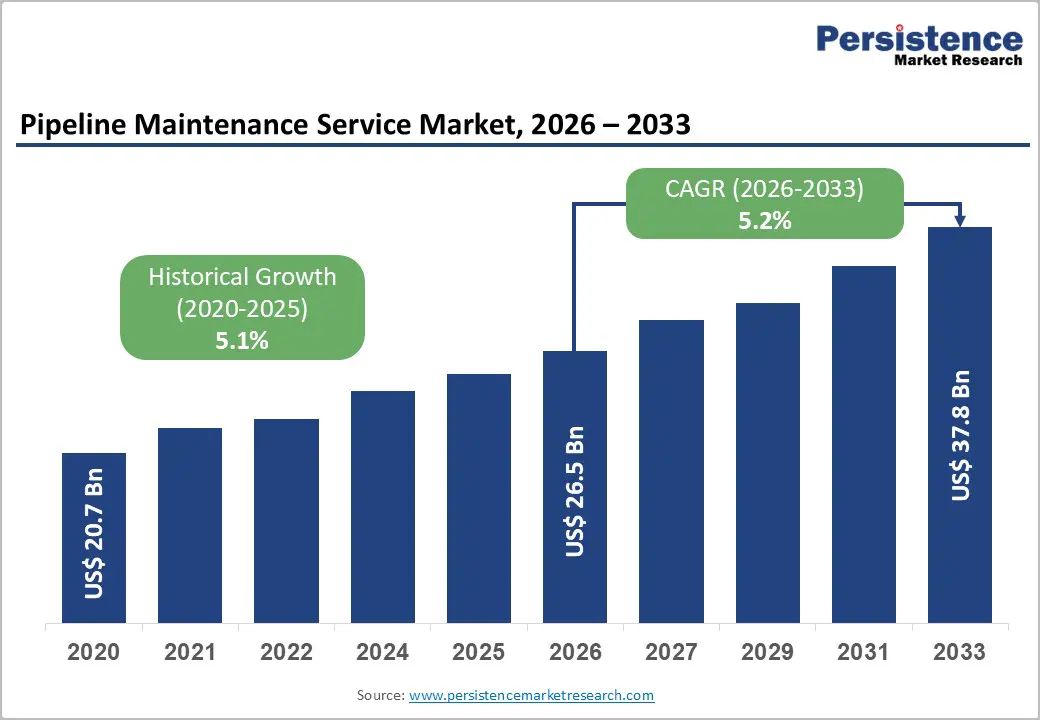

The global pipeline maintenance service market size is likely to be valued at US$ 26.5 billion in 2026 and is expected to reach US$ 37.8 billion by 2033, growing at a CAGR of 5.2% during the forecast period from 2026 to 2033, driven by rising investments in pipeline infrastructure, increasing regulatory focus on asset integrity, and the growing need to maintain aging pipeline networks worldwide.

Pipeline operators are prioritizing preventive maintenance and integrity management to avoid environmental incidents and operational disruptions. The adoption of advanced technologies such as inline inspection tools, robotics, remote monitoring systems, and predictive analytics is improving operational efficiency and expanding the scope of maintenance service contracts.

Key Industry Highlights:

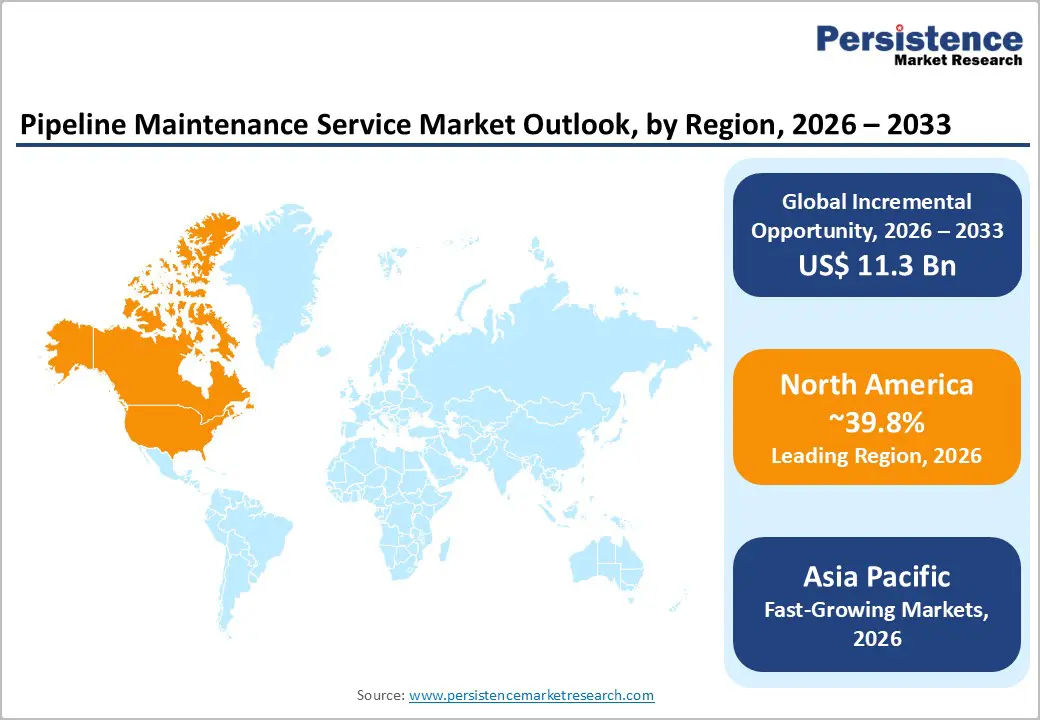

- Leading Region: North America is projected to lead the market, accounting for approximately 39.8% of market share, supported by extensive oil and gas pipeline networks in the U.S. and Canada and strict regulatory oversight from agencies such as the Pipeline and Hazardous Materials Safety Administration (PHMSA).

- Fastest-growing Region: Asia Pacific is the fastest-growing regional market, driven by large-scale pipeline infrastructure expansion projects in China and India, and rising industrial demand.

- Investment Plans: Governments and energy companies are investing heavily in pipeline modernization, hydrogen pipeline conversion, and water infrastructure upgrades, with several countries in Europe and Asia launching major energy transition pipeline projects. These initiatives are expected to drive maintenance service demand growth exceeding 5% annually during the forecast period.

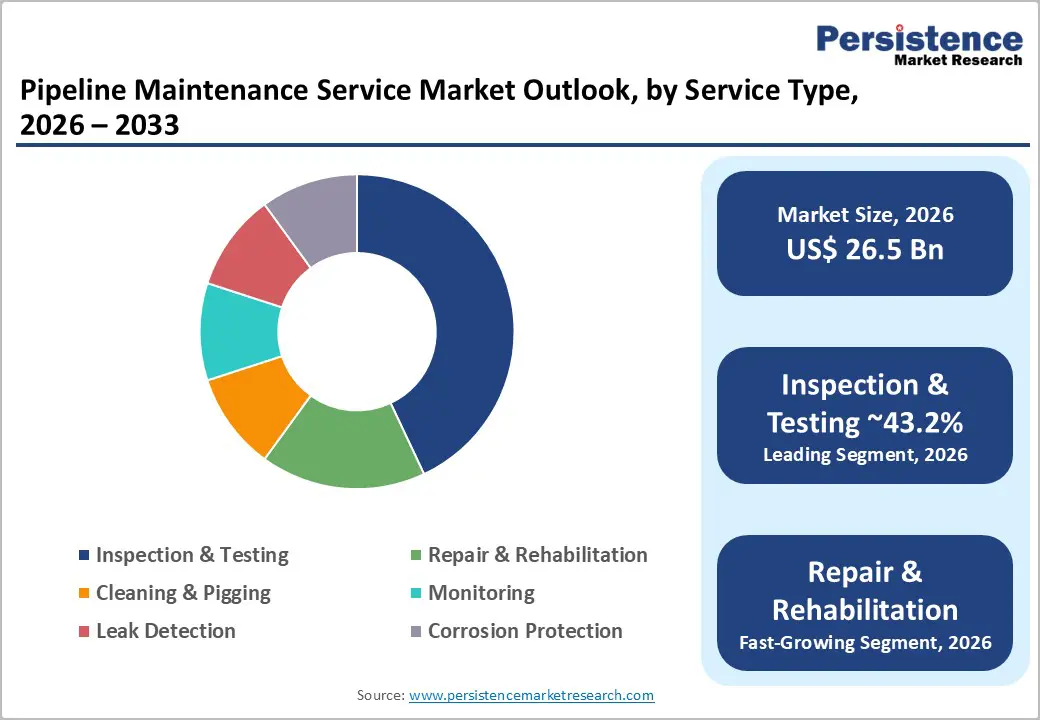

- Dominant Service Type: Inspection & testing services are anticipated to hold approximately 43.2% market share, as operators prioritize regular integrity inspections, corrosion monitoring, and smart pigging operations to meet regulatory compliance and prevent pipeline failures.

- Leading Application: Oil & gas pipeline is estimated to account for around 59.4% of market share, supported by extensive hydrocarbon transportation networks and the high operational value associated with energy pipeline infrastructure.

| Key Insights | Details |

|---|---|

| Pipeline Maintenance Service Market Size (2026E) | US$26.5 Bn |

| Market Value Forecast (2033F) | US$37.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expansion of Global Pipeline Infrastructure

The continuous expansion of global pipeline networks for oil, natural gas, and refined petroleum products is a major driver for the pipeline maintenance service market. Growing global energy demand has resulted in large-scale investments in pipeline infrastructure connecting production regions with consumption markets. As pipeline networks expand, operators must allocate substantial budgets toward inspection, pigging, corrosion protection, and monitoring to ensure operational safety and compliance with environmental standards. Maintenance services are essential throughout the pipeline lifecycle, from commissioning to long-term operation. As new pipelines are installed and older networks continue operating, the demand for specialized maintenance services increases consistently across both developed and emerging economies.

Aging Pipeline Infrastructure and Integrity Management Requirements

A significant portion of global pipeline infrastructure has been operational for several decades. Aging pipelines are more vulnerable to corrosion, metal fatigue, mechanical damage, and leakage incidents. Governments and regulatory authorities are strengthening integrity management regulations that require periodic inspections, testing, and maintenance of pipelines. Operators are therefore investing heavily in advanced inspection technologies such as inline inspection tools, ultrasonic testing, and corrosion monitoring systems. These efforts help prevent catastrophic failures, minimize environmental risks, and ensure regulatory compliance. As a result, pipeline integrity management programs are becoming a major source of recurring demand for maintenance service providers.

Adoption of Digital Monitoring and Robotics

Technological advancements are transforming pipeline maintenance services through automation and digital monitoring systems. Robotic inspection tools, autonomous underwater vehicles, and remotely operated vehicles are increasingly used to inspect pipelines located in challenging environments such as offshore fields or remote terrains. At the same time, digital monitoring platforms are enabling real-time data collection and predictive maintenance capabilities. These technologies allow service providers to detect corrosion, cracks, and leaks more accurately and at earlier stages. The shift toward data-driven maintenance strategies is improving operational efficiency, reducing downtime, and creating new revenue opportunities for service providers offering advanced monitoring and analytics solutions.

Barrier Analysis - High Capital Requirements for Advanced Inspection Technologies

Pipeline maintenance operations often require sophisticated equipment such as inline inspection tools, remotely operated vehicles, advanced sensors, and corrosion monitoring systems. The acquisition and deployment of such technologies involve substantial capital investment and specialized technical expertise. Smaller service providers may face financial barriers when competing with established firms that possess advanced technological capabilities. In addition, maintenance projects involving offshore pipelines require specialized vessels and equipment, which significantly increases operational costs and limits participation by smaller contractors.

Complex Regulatory Compliance and Permitting Processes

Pipeline maintenance operations are subject to stringent regulatory oversight in many countries. Maintenance activities often require environmental permits, safety approvals, and coordination with multiple regulatory agencies. These compliance requirements can extend project timelines and increase administrative costs for pipeline operators and service providers. In urban areas or environmentally sensitive regions, maintenance projects may also face delays due to public consultations and environmental impact assessments. Such regulatory complexities can slow down project execution and limit the speed at which maintenance contracts are awarded.

Opportunity Analysis - Pipeline Repurposing for Low-Carbon Energy Transport

The global transition toward low-carbon energy systems is creating new opportunities for pipeline maintenance service providers. Existing pipelines are increasingly being evaluated for potential conversion to transport hydrogen, carbon dioxide, or other alternative energy carriers. Repurposing pipelines requires extensive testing, inspection, and retrofitting to ensure material compatibility and safety. Maintenance service companies can benefit from providing specialized services such as metallurgical assessments, weld inspection, corrosion protection upgrades, and leak detection. These activities create long-term service opportunities for companies that possess expertise in advanced pipeline integrity management.

Growth of Digital Monitoring and Predictive Maintenance Services

Pipeline operators are increasingly adopting digital monitoring platforms that integrate sensor networks, real-time analytics, and predictive maintenance algorithms. These technologies enable continuous monitoring of pipeline conditions, allowing operators to identify potential failures before they occur. Service providers that offer integrated solutions combining field inspections with digital monitoring platforms can establish long-term service agreements with pipeline operators. This shift toward subscription-based monitoring services is creating a more stable and recurring revenue stream for companies operating in the pipeline maintenance service market.

Expansion of Water and Wastewater Infrastructure

Rapid urbanization and population growth are driving investments in water distribution and wastewater treatment infrastructure around the world. Governments are launching large-scale programs to upgrade aging municipal pipeline networks and reduce water losses caused by leakage and infrastructure deterioration. These initiatives are increasing demand for pipeline cleaning, leak detection, rehabilitation, and monitoring services. Maintenance service providers that specialize in municipal infrastructure are expected to benefit significantly from these infrastructure investment programs, particularly in emerging economies across Asia Pacific and Latin America.

Category-wise Analysis

Service Type Analysis

Inspection & testing is anticipated to account for approximately 42.8-45% of the market share in 2026, making it the largest service category. Pipeline operators conduct routine inspections to evaluate structural integrity, detect corrosion, and identify potential leaks before they escalate into operational failures or environmental incidents. Inspection technologies commonly include inline inspection tools (commonly referred to as smart pigs), ultrasonic testing systems, magnetic flux leakage tools, and hydrostatic pressure testing. These technologies allow operators to detect anomalies such as cracks, metal loss, corrosion growth, and mechanical deformation within pipelines. Inspection and testing services play a critical role in regulatory compliance and long-term asset management strategies.

Many national safety authorities require periodic integrity assessments of pipelines transporting oil, gas, and hazardous materials. As a result, operators must implement structured integrity management programs that involve scheduled inspections and data analysis. The growing use of high-resolution inline inspection tools and advanced analytics platforms is enabling operators to obtain highly detailed pipeline condition data. For example, modern smart pigging technologies can map corrosion defects and crack growth with millimeter-level precision, helping operators plan preventive maintenance activities more effectively.

Repair & rehabilitation is anticipated to be the fastest-growing service segment in the pipeline maintenance service market during the forecast period. A large portion of global pipeline infrastructure has been in operation for several decades and is now approaching advanced stages of its service life. As pipelines age, they become increasingly susceptible to corrosion, fatigue cracks, and structural degradation, creating the need for targeted repair and reinforcement solutions. Repair and rehabilitation services include pipeline welding repairs, composite wrap reinforcement, pipe section replacements, and internal pipe lining solutions.

Technologies such as composite wrap systems, trenchless rehabilitation methods, and cured-in-place pipe (CIPP) lining are gaining popularity because they allow operators to restore pipeline integrity without extensive excavation or complete pipeline replacement. For example, composite wrap systems are widely used in oil and gas transmission pipelines to reinforce weakened sections, while trenchless relining technologies are increasingly used to rehabilitate aging municipal water pipelines. Operators are prioritizing rehabilitation strategies because they provide cost-effective solutions for extending pipeline lifespans and minimizing operational disruptions.

Application Insights

Oil & gas pipelines are anticipated to account for approximately 59.4% of the market share in 2026, making them the dominant application segment. These pipelines form the backbone of global energy transportation systems, connecting production fields, processing facilities, storage terminals, and end-use markets. Oil and gas pipeline networks span thousands of kilometers across continents, requiring continuous monitoring and maintenance to ensure safe and uninterrupted energy transportation. Maintenance activities in this segment typically include pigging operations, corrosion monitoring, leak detection, pressure testing, and integrity inspections. Due to the high economic value and safety risks associated with hydrocarbon transportation, pipeline operators allocate substantial budgets toward maintenance and integrity management programs.

For example, long-distance crude oil pipelines in North America and natural gas transmission networks in Europe require frequent inspection cycles using inline inspection tools and advanced monitoring systems. Similarly, large offshore oil and gas pipelines in regions such as the North Sea and the Gulf of Mexico rely on subsea inspection technologies and remotely operated vehicles to maintain operational reliability. Strict regulatory standards governing hydrocarbon pipelines further reinforce the dominance of the oil and gas segment in the global pipeline maintenance service market.

Water & wastewater pipeline systems are anticipated to be the fastest-growing application segment in the pipeline maintenance service market. Many urban areas around the world are facing significant challenges related to aging water distribution networks, which often suffer from leakage, corrosion, and structural deterioration. In some regions, aging infrastructure results in high levels of non-revenue water losses due to undetected leaks and pipeline failures. Governments and municipal authorities are therefore investing heavily in infrastructure modernization programs aimed at upgrading water supply and wastewater management systems.

Maintenance activities in this sector include leak detection surveys, pipeline cleaning, trenchless rehabilitation, corrosion protection, and condition monitoring. Technologies such as acoustic leak detection sensors and smart monitoring systems are increasingly being deployed to identify leaks early and reduce water losses. For example, several major cities in Asia and Europe have launched large-scale pipeline rehabilitation programs using trenchless relining technologies to restore aging water pipelines without disrupting urban infrastructure. As population growth, urbanization, and water security concerns continue to intensify, maintenance services for water and wastewater pipeline networks are expected to experience strong and sustained growth.

Regional Insights

North America Pipeline Maintenance Service Market Trends - Aging Pipeline Infrastructure and Strict Integrity Regulations Driving Maintenance Demand

North America represents the largest regional market, accounting for approximately 39.8% of the market share in 2026. The region has an extensive network of oil and natural gas pipelines that transport energy resources across the U.S. and Canada. The U.S. dominates the regional market due to its large midstream energy sector and well-established pipeline infrastructure. Major operators such as Kinder Morgan, Enbridge Inc., and Williams Companies manage thousands of kilometers of crude oil and natural gas pipelines, creating sustained demand for inspection, pigging, and integrity management services.

Strong regulatory frameworks require pipeline operators to implement comprehensive integrity management programs. Agencies such as the Pipeline and Hazardous Materials Safety Administration enforce strict safety regulations that mandate regular inspections, leak detection systems, and maintenance procedures to prevent environmental incidents. For example, PHMSA expanded rules for gas transmission pipeline integrity management in recent years, requiring operators to conduct more frequent inline inspections and corrosion monitoring. These regulatory requirements compel operators to allocate significant budgets toward pipeline monitoring, inspection, and repair services.

Technological innovation also plays an important role in the region’s market leadership. Service providers such as Baker Hughes and T.D. Williamson is actively developing advanced inline inspection tools, robotic inspection systems, and digital monitoring platforms that enhance pipeline integrity management. For example, Baker Hughes has introduced high-resolution magnetic flux leakage inspection tools designed to detect early-stage corrosion defects, while T.D. Williamson has expanded its intelligent pigging technologies to improve crack detection accuracy in long-distance transmission pipelines. The growing adoption of predictive maintenance platforms and digital twin technology is enabling operators to reduce operational risks and optimize maintenance schedules.

Investment in pipeline modernization and replacement projects further supports the growth of maintenance services in North America. Many existing pipelines were built decades ago and now require rehabilitation or replacement. Infrastructure operators are therefore increasing investments in pipeline upgrades and modernization programs. For instance, projects such as the Line 3 Replacement Program involved replacing large segments of aging crude oil pipelines across the U.S., which have created long-term opportunities for maintenance and integrity monitoring services. Growing investments in carbon capture infrastructure and hydrogen transport pipelines are also expected to generate new demand for specialized inspection and monitoring technologies across the region.

Europe Pipeline Maintenance Service Market Trends - Hydrogen Pipeline Conversion and Offshore North Sea Maintenance Opportunities

Europe represents a significant market for pipeline maintenance services due to its extensive energy transportation networks and strong regulatory standards governing pipeline safety. Countries such as Germany, the U.K., France, and Spain play leading roles in the regional market. Major pipeline infrastructure operators, including Gascade Gastransport and National Grid, maintain large natural gas pipeline networks that require continuous inspection, corrosion monitoring, and maintenance programs.

European regulatory frameworks emphasize environmental protection and infrastructure safety, which encourages regular pipeline inspection and maintenance activities. Regulatory agencies across the European Union enforce strict safety standards for pipeline integrity management. Organizations such as the European Union Agency for the Cooperation of Energy Regulators support regulatory harmonization and oversight of cross-border energy infrastructure. These frameworks require operators to implement leak detection systems, corrosion monitoring programs, and periodic pipeline inspections, which creates consistent demand for specialized maintenance service providers.

Several European countries are exploring the conversion of existing natural gas pipelines to transport hydrogen as part of long-term decarbonization strategies. For example, the European Hydrogen Backbone initiative aims to repurpose thousands of kilometers of natural gas pipelines to support hydrogen transport across Europe. Such projects require extensive inspection, testing, and retrofitting services to ensure pipeline compatibility with hydrogen transportation, thereby creating new opportunities for pipeline maintenance companies.

In addition, offshore pipeline infrastructure in the North Sea remains a key market segment. Maintenance services for subsea pipelines, including inspection, repair, and integrity monitoring, are critical for maintaining offshore oil and gas operations. Energy companies such as Equinor and BP operate major offshore pipeline systems connected to North Sea production fields. These assets require specialized subsea inspection technologies, remotely operated vehicles, and corrosion monitoring systems. The combination of aging infrastructure and energy transition investments continues to drive demand for pipeline maintenance services across Europe.

Asia Pacific Pipeline Maintenance Service Market Trends - Rapid Pipeline Network Expansion Driven by Industrialization and Energy Demand

Asia Pacific is the fastest-growing regional market for pipeline maintenance services. Rapid industrialization, urbanization, and increasing energy demand are driving the expansion of pipeline infrastructure across the region. Governments are investing heavily in pipeline networks for energy transportation, water supply systems, and industrial infrastructure. China leads the regional market with significant investments in oil, natural gas, and industrial pipeline networks. State-owned enterprises such as China National Petroleum Corporation and PipeChina are expanding long-distance pipeline systems connecting energy production regions in western China with major consumption centers in eastern provinces. Large infrastructure projects such as the West-East Gas Pipeline Project have created extensive pipeline networks requiring continuous inspection, monitoring, and maintenance services throughout their lifecycle.

India is also experiencing strong growth in pipeline infrastructure development. Government initiatives aimed at expanding natural gas distribution networks and improving water supply infrastructure are increasing demand for pipeline inspection, cleaning, and monitoring services. Organizations such as GAIL India Limited are expanding national gas pipeline networks under initiatives like the Pradhan Mantri Urja Ganga Pipeline Project. These projects involve thousands of kilometers of pipeline installations, creating long-term demand for maintenance and integrity management services.

Japan remains a technologically advanced market with strong expertise in offshore maintenance technologies and infrastructure monitoring systems. Companies such as Mitsubishi Heavy Industries and JGC Holdings Corporation provide advanced inspection technologies and engineering services for pipeline systems and offshore energy infrastructure. Meanwhile, Southeast Asian countries, including Indonesia, Malaysia, and Vietnam, are expanding pipeline infrastructure to support growing industrial and energy demand.

Competitive Landscape

The global pipeline maintenance service market consists of a combination of global engineering service companies, inspection specialists, and regional contractors. While large multinational companies dominate high-value offshore and technologically complex projects, regional service providers play an important role in onshore pipeline maintenance activities. The market structure can be characterized as moderately fragmented, with competition driven by technological capabilities, regulatory certifications, and geographic presence.

Leading companies focus on technology innovation, digital monitoring platforms, and global service expansion to strengthen their competitive positions. Strategic investments in robotics, inspection technologies, and predictive maintenance solutions are enabling service providers to deliver higher-value integrity management services to pipeline operators.

Key Industry Developments:

- In March 2025, Baker Hughes announced a technology development agreement with Petrobras to develop next-generation flexible pipe systems designed to mitigate stress corrosion cracking in high-CO2 offshore environments. The initiative focuses on extending pipeline service life to nearly 30 years, improving long-term pipeline integrity, and supporting offshore oil and gas operations in Brazil’s pre-salt fields.

- In July 2025, Baker Hughes secured a multi-year agreement with Genesis Energy to supply drag-reducing agents and digital optimization solutions for major offshore crude pipelines in the U.S. Gulf Coast. The project is designed to increase pipeline throughput and improve operational efficiency for the Cameron Highway and Poseidon pipeline systems.

Companies Covered in Pipeline Maintenance Service Market

- Baker Hughes

- ROSEN Group

- T.D. Williamson

- Intertek Group plc

- SGS SA

- NDT Global

- Applus+

- Dacon Inspection Services

- Enduro Pipeline Services

- Quest Integrity Group

- LIN SCAN

- Pure Technologies

- STATS Group

- EnerMech

- Halfwave AS

- IKM Gruppen

Frequently Asked Questions

The global pipeline maintenance service market is estimated to be valued at US$26.5 billion in 2026.

The pipeline maintenance service market is projected to reach US$37.8 billion by 2033.

Key trends include the adoption of advanced inline inspection technologies (smart pigging), predictive maintenance platforms, robotic inspection systems, and digital monitoring tools.

Inspection & testing services represent the leading segment, accounting for approximately 43.2% of the market share, as pipeline operators prioritize routine inspections and integrity management programs to comply with safety regulations and prevent operational failures.

The pipeline maintenance service market is expected to grow at a CAGR of 5.2% between 2026 and 2033.

Some of the major companies include Baker Hughes, ROSEN Group, and T.D. Williamson, Intertek Group plc, and SGS SA.