- Pharmaceuticals

- Pharmacovigilance Market

Pharmacovigilance Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Pharmacovigilance Market by Reporting Type (Spontaneous Reporting, Intensified ADR Reporting, Targeted Spontaneous Reporting, Cohort Event Monitoring, EHR Mining), Deployment Mode (In-house, Contract Outsourcing), Product Life Cycle (Pre-clinical, Phase I, Phase II, Phase III, Phase IV), Therapeutic Area (Oncology, Neurology, Infectious Diseases, Cardiology, Respiratory Systems, Others), End-user, and Regional Analysis from 2026 to 2033

Pharmacovigilance Market Share and Trends Analysis

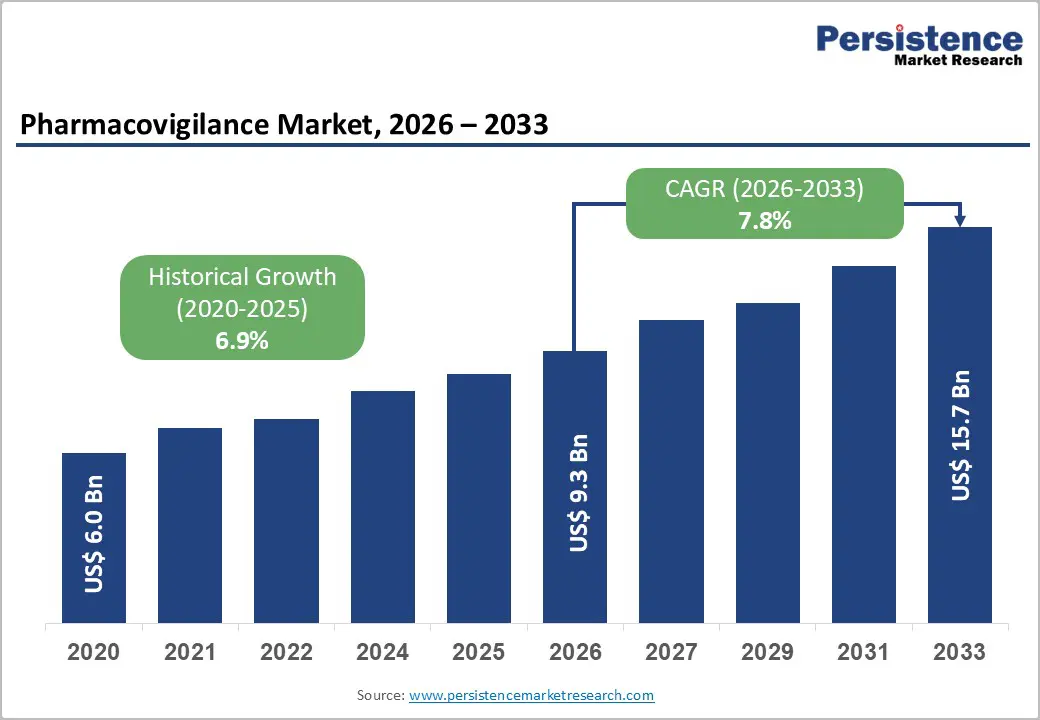

The global pharmacovigilance market size is estimated to reach US$ 9.3 billion in 2026 and reach US$ 15.7 billion by 2033, growing at a CAGR of 7.8% during the forecast period from 2026 to 2033. The global pharmacovigilance market is experiencing robust growth, driven by increasing adverse drug reaction reporting, stringent regulatory requirements, and rising drug approvals worldwide.

Expanding clinical trials, growing biologics pipelines, and outsourcing trends further fuel demand. North America leads due to advanced regulatory systems, while the Asia Pacific is expected to experience rapid growth amid expanding pharmaceutical manufacturing and clinical research activity.

Key Industry Highlights:

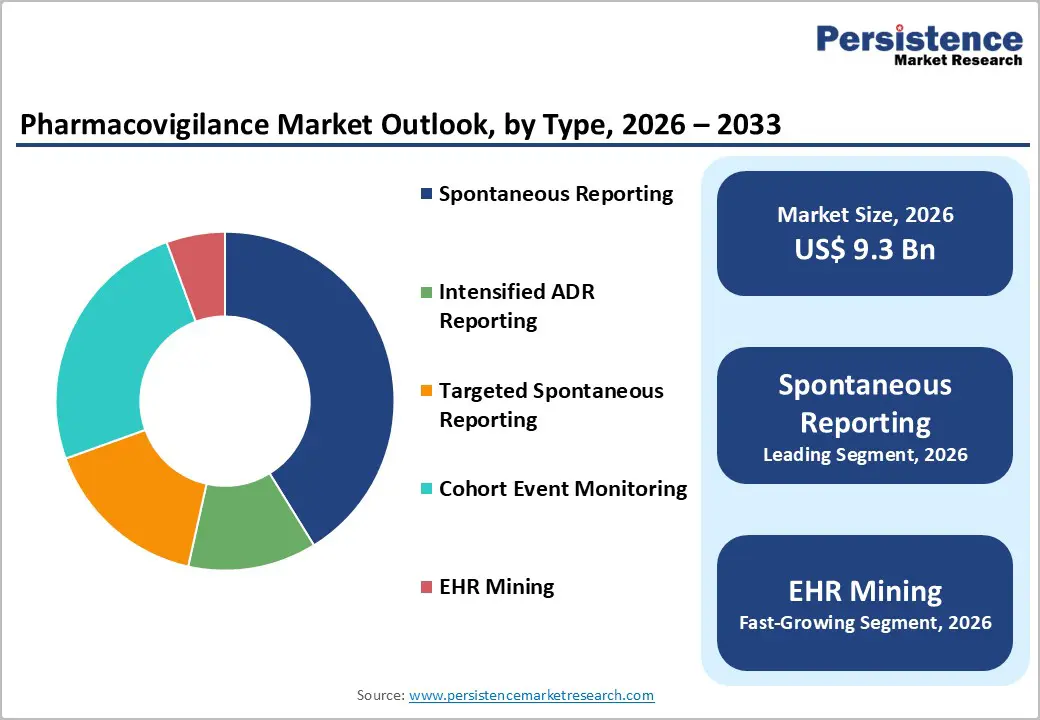

- Dominant Product: Spontaneous Reporting accounts for 41.2% of the pharmacovigilance market in 2025, driven by its central role in detecting adverse drug reactions and regulatory safety monitoring. Mandatory reporting requirements, broad participation by healthcare professionals, established global databases, and continuous post-marketing surveillance support widespread adoption across pharmaceutical and biotechnology companies worldwide.

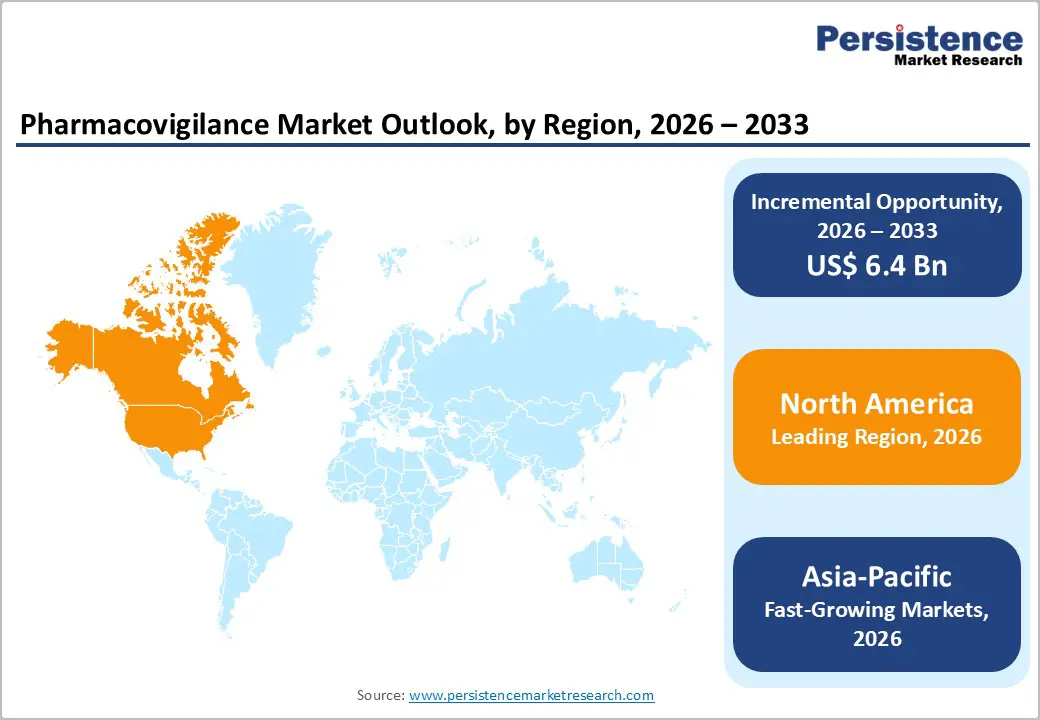

- Dominant Region: North America leads the pharmacovigilance market in 2025 with a 43.6% share, supported by stringent regulatory frameworks (FDA reporting requirements), high drug approval volumes, a strong biotech presence, and advanced adoption of safety analytics. The Asia-Pacific is the fastest-growing region, driven by expanding clinical trials, rising pharmaceutical manufacturing, and increasing outsourcing hubs in India and China.

- Growth Indicators: Rising adverse drug reaction (ADR) reporting, increasing drug approvals, expanding biologics and specialty drug pipelines, stringent global regulatory compliance requirements, growing clinical trial activity, and adoption of AI-driven signal detection technologies are key market growth drivers.

- Opportunity: Oppo/rtunities include AI-enabled automation of case processing, integration of real-world evidence (RWE) and EHR mining, expansion of pharmacovigilance services in emerging markets, development of cloud-based safety platforms, and strategic partnerships between CROs and pharmaceutical companies for end-to-end safety management.

| Key Insights | Details |

|---|---|

| Pharmacovigilance Market Size (2026E) | US$ 9.3 Bn |

| Market Value Forecast (2033F) | US$ 15.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.9% |

Market Dynamics

Driver: Increasing Drug Approvals and Expanding Biologics Pipeline

The volume of new therapeutic agents entering global markets has been steadily expanding, increasing the need for comprehensive pharmacovigilance systems to ensure safety monitoring throughout the drug lifecycle. According to the U.S. FDA’s Center for Drug Evaluation and Research (CDER) 2025 report, 46 novel drugs were approved, including 34 new molecular entities (NMEs) and 12 biologics, a significant contribution to the therapeutic pipeline that requires long-term safety surveillance after approval. Additionally, when accounting for approvals from both CDER and the Center for Biologics Evaluation and Research (CBER), 58 new therapies were approved in 2025.

The biologics subset alone remains a crucial driver for pharmacovigilance demand. On average over recent years, about 30% of FDA-approved new drugs were biologics, reflecting a consistent shift toward complex, high-risk therapeutic classes with diverse safety profiles that require vigorous post-market surveillance. This includes monoclonal antibodies and other advanced biologics with unique safety considerations. Globally, regulatory bodies, including EMA, PMDA (Japan), and CDSCO (India), emphasize lifecycle safety monitoring for both small molecules and biologics. Pharmaceutical sponsors must invest in expanded pharmacovigilance infrastructure to support market growth. This surge in approvals increases adverse event reporting volumes and necessitates larger safety databases, signal-detection tools, and specialized staffing, underscoring drug pipeline expansion as a principal growth driver.

Restraints: High Operational Costs of Pharmacovigilance Compliance

Maintaining a fully compliant pharmacovigilance system represents a significant financial burden for pharmaceutical companies, particularly when operations must meet stringent global regulatory requirements. In markets such as Europe, regulatory bodies require continuous post-marketing surveillance reporting to systems such as EudraVigilance, which necessitates validated safety databases and frequent audits, contributing to operational expenses.

These costs arise from multiple sources: dedicated personnel for safety report review and medical assessment; investment in validated database infrastructure; software licenses for advanced case processing and signal detection systems; and routine compliance activities, including audit preparation, regulatory submissions, quality assurance, and training. Even large pharmaceutical companies allocate substantial budgets to meet these requirements, while small and mid-sized firms may struggle to absorb these costs without stretching other core R&D resources.

The complexity and fragmentation of global safety reporting requirements further exacerbate costs, as organizations must adapt workflows, documentation, and reporting formats to align with divergent regulatory expectations in key markets such as the U.S., Europe, and Asia. This results in duplication of processes and prevents economies of scale in safety operations. Consequently, the financial resources required to build, integrate, and maintain robust pharmacovigilance infrastructure remain a significant restraint on market adoption and expansion, particularly for resource-constrained companies.

Opportunity: Expansion of Pharmacovigilance Outsourcing in Emerging Markets

Rapid growth in emerging economies presents a substantial opportunity for the pharmacovigilance market, particularly through outsourcing arrangements in which specialized vendors provide drug safety services to global sponsors.

Emerging markets such as India, China, Brazil, and parts of Latin America are increasingly attractive destinations for outsourced pharmacovigilance work due to several advantages: cost-effective, skilled labor, expanding healthcare infrastructure, improving regulatory frameworks, and growing participation in multinational clinical research. For example, local regulatory authorities in India and Latin America have strengthened adverse event reporting requirements in recent years, creating demand for region-specific PV expertise.

Pharmaceutical and biotechnology companies seeking cost-efficient compliance solutions can leverage regional partners to manage adverse event case processing, signal detection, safety database management, and regulatory reporting. This allows sponsors to scale pharmacovigilance operations swiftly without building extensive internal teams. Additionally, outsourcing providers in emerging regions are adopting advanced technologies, including cloud-based safety platforms and AI-assisted analytics to enhance service quality, further broadening opportunities. Expansion into emerging markets thus represents both a strategic growth area and a competitive advantage for PV service providers seeking global reach and cost leadership.

Category-wise Analysis

By Reporting Type Insights

Spontaneous reporting accounts for 41.2% of the global market in 2025, as it is the foundational mechanism for detecting adverse drug reactions (ADRs) after a product enters the market. In the United States, the FDA Adverse Event Reporting System (FAERS) receives millions of reports annually from healthcare professionals and consumers. FAERS log files show well over 8 million individual case safety reports between 2004 and 2024. Similarly, the WHO’s VigiBase (maintained by the Uppsala Monitoring Centre) houses over 29 million global ADR reports, making spontaneous reporting the most extensively used method for real-world safety monitoring. These systems are mandated by regulatory authorities, with physicians, pharmacists, and patients required or encouraged to report suspected ADRs, which ensures high volume and broad coverage. Because it captures the largest share of real-world safety data and feeds global signal detection, spontaneous reporting remains the dominant pharmacovigilance method.

By Deployment Mode Insights

Contract outsourcing drives pharmacovigilance deployment, as sponsors increasingly rely on specialized external partners to manage complex safety functions at scale. Regulatory requirements in major markets like the U.S. and Europe demand continuous case processing, periodic reporting, and compliance with standards such as ICSR submission to EudraVigilance and FAERS, which has driven growth in outsourced safety operations. According to the U.S. FDA’s inspection data, multiple regulatory actions have highlighted compliance deficiencies in in-house safety systems, motivating pharmaceutical companies to engage CROs with dedicated expertise to mitigate risk. Outsourcing enables sponsors to tap into global safety networks, multilingual case intake, and efficient submission workflows without expanding internal headcount. Moreover, experienced CROs maintain validated safety databases and regulatory intelligence across regions, offering economies of scale. These factors collectively make outsourcing the dominant deployment choice for pharmacovigilance infrastructure.

Regional Insights

North America Pharmacovigilance Market Trends

North America dominates the pharmacovigilance market with 43.6% share due to its advanced regulatory infrastructure, extensive ADR reporting systems, and strong pharmaceutical R&D ecosystem. In the U.S., the FDA’s FAERS database processes millions of adverse event reports annually, while mandatory electronic submissions under E2B(R3) standards have accelerated the adoption of robust safety monitoring platforms. The region also benefits from high clinical trial activity and widespread electronic health record (EHR) integration, enabling comprehensive real-world safety data capture and advanced signal detection. Significant investment in artificial intelligence, automation, and data analytics further strengthens pharmacovigilance capabilities. These structural advantages, stringent regulatory oversight, and technological sophistication sustain North America’s leadership in global drug-safety surveillance and compliance frameworks.

Europe Pharmacovigilance Market Trends

Europe is critical to the global pharmacovigilance landscape due to unified safety reporting frameworks and stringent regulatory standards under the European Medicines Agency (EMA). The EMA’s EudraVigilance system receives well over 1.7 million ADR reports annually, facilitating standardized safety surveillance across the European Economic Area. Reporting is mandatory for marketing authorization holders and clinical trial sponsors, ensuring comprehensive drug-safety data collection. European countries also emphasize the integration of real-world evidence and cross-border collaboration in pharmacovigilance, reinforcing harmonized surveillance. National authorities such as Germany’s BfArM and the UK’s MHRA also contribute through structured ADR monitoring and regulatory inspections. This robust regulatory integration, combined with a large pharmaceutical industry and mature post-marketing surveillance culture, makes Europe a key contributor and influencer in global pharmacovigilance practices.

Asia-Pacific Pharmacovigilance Market Trends

Asia-Pacific is the fastest-growing region in pharmacovigilance, driven by rapid expansion in clinical research, pharmaceutical manufacturing, and regulatory modernization. Countries such as India and China have seen strong growth in ADR database development and reporting activity. India’s national pharmacovigilance programme reports hundreds of thousands of ADRs annually with rising awareness among healthcare professionals. The region also hosts large numbers of pharmaceutical manufacturers (e.g., China with over 4,500 manufacturers), thereby fostering demand for safety-monitoring infrastructure compliant with international standards such as ICH. Regulatory authorities in Japan (PMDA) and China (NMPA) have updated reporting requirements and electronic submission mandates, accelerating adoption of pharmacovigilance systems. Outsourcing to Asia-Pacific CROs and service providers is increasing due to lower operational costs and greater availability of skilled talent, driving the region’s rapid market growth.

Competitive Landscape

The pharmacovigilance market's competitive landscape features key players focusing on product innovation, quality differentiation, and strategic partnerships. Leading manufacturers invest in tailored peptone formulations and expand production capacity to meet rising demand across biotech, pharmaceutical, and food fermentation sectors. Competitive strategies include sustainability initiatives, global distribution networks, and collaborations to enhance market presence and technological capabilities.

Key Industry Developments:

- In February 2026, ArisGlobal announced the launch of XDI NavaX Data Intelligence, along with three new intelligent agents and the NavaX Translation capability, strengthening its AI-driven pharmacovigilance portfolio. The company stated that the new XDI (Extended Data Intelligence) module was designed to enhance advanced data aggregation, signal detection, and regulatory decision support across safety ecosystems.

- In January 2026, The role of Local Qualified Persons for Pharmacovigilance (LQPPVs) gained significant strategic importance as pharmaceutical companies accelerated the adoption of AI-enabled safety systems. Organizations increasingly relied on LQPPVs not only for statutory compliance but also for oversight of automated signal detection, electronic case processing, and AI-driven risk management frameworks.

Frequently Asked Questions

The global pharmacovigilance market is projected to be valued at US$ 9.3 Bn in 2026.

Rising drug approvals, stricter regulations, growing ADR volumes, and expanding biologics pipeline.

The global pharmacovigilance market is poised to witness a CAGR of 7.8% between 2026 and 2033.

Outsourcing expansion, AI-driven automation, emerging markets growth, and real-world data integration.

Wipro, IQVIA, ICON plc., ArisGlobal, Accenture, ClinChoice (formerly FMD K&L).