- Plastics, Polymers & Resins

- Packaging Resins Market

Packaging Resins Market Size, Share, and Growth Forecast 2026 - 2033

Packaging Resins Market by Product Type (Polyethylene, Polypropylene, Polyethylene Terephthalate, Polystyrene, PVC, Other), Application (Food & Beverage, Consumer Goods, Healthcare, Industrial, Other), and Regional Analysis for 2026 - 2033

Packaging Resins Market Size and Trend Analysis

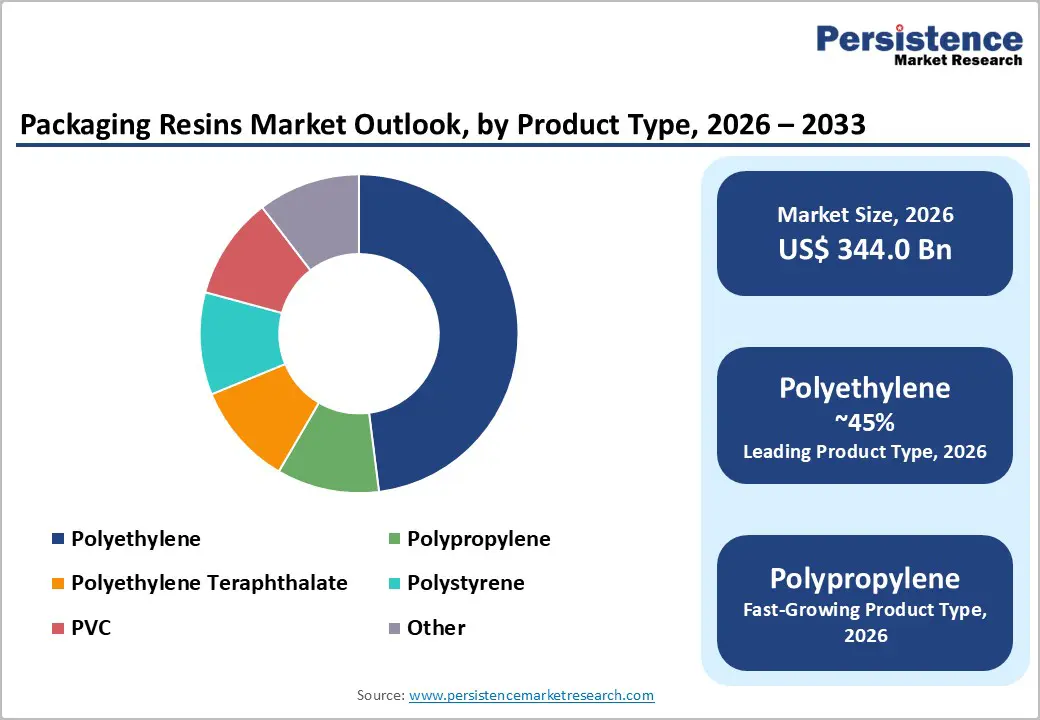

The global packaging resins market size is supposed to be valued at US$ 344.0 billion in 2026 and is projected to reach US$ 574.5 billion by 2033, growing at a CAGR of 7.6% between 2026 and 2033.

The market growth is driven by three primary factors: accelerating demand from the food and beverage industry, expanding e-commerce and retail sectors requiring protective packaging solutions, and rising consumer preferences for convenience-driven packaged products. The United Nations Industrial Development Organization (UNIDO) reported a 15% year-on-year increase in packaging production, driven by urbanization in the Asia-Pacific region.

Key Industry Highlights:

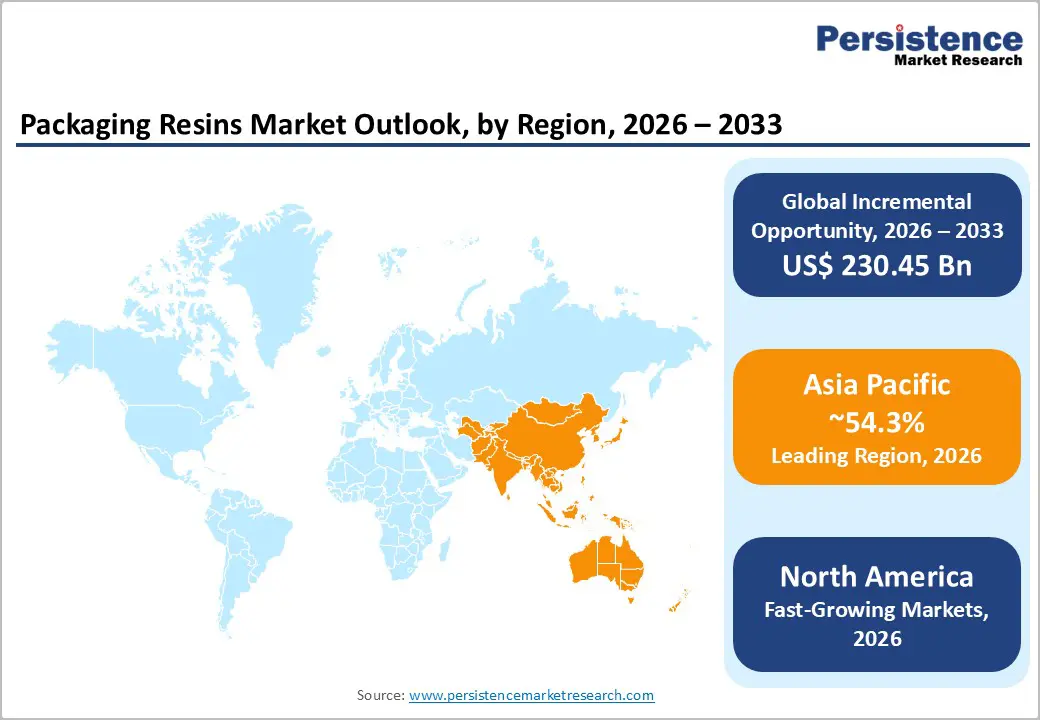

- Regional Leader: Asia-Pacific dominates the global packaging resins market with 54.3% share, driven by China's manufacturing dominance, India's infrastructure growth, and expanding consumer goods consumption.

- Fastest Growing Region: North America emerges as the fastest-growing region, driven by its mature food and beverage industry, strong pharmaceutical packaging demand, and advanced innovation ecosystem.

- Leading Segment: Polyethylene maintains market dominance with approximately 48% share of polyethylene applications, driven by exceptional durability, chemical resistance, recyclability, and unmatched cost-effectiveness.

- Fastest Growing Segment: Food & Beverages grows fastest in applications, fueled by ready-to-eat demand and shelf-life needs.

- Key Market Opportunity: Circular economy materials and smart packaging technology integration represent the most significant opportunity, with regulatory mandates requiring 30-65% recycled content by 2030-2040 across major markets, and smart packaging solutions.

| Key Insights | Details |

|---|---|

|

Packaging Resins Market Size (2026E) |

US$ 344.0 Bn |

|

Market Value Forecast (2033F) |

US$ 574.5 Bn |

|

Projected Growth CAGR (2026-2033) |

7.6% |

|

Historical Market Growth (2020-2025) |

6.1% |

Market Dynamics

Driver - Expansion of E-Commerce and Retail Logistics

The rapid expansion of e-commerce platforms has become a significant driver of the packaging resins market. By the end of 2023, global online shoppers reached approximately 2.64 billion, up 5% year on year. This growth necessitates packaging solutions that are lightweight yet durable, able to withstand shipping stresses while reducing transportation costs and environmental impact. Packaging resins provide the optimal combination of strength, flexibility, and cost-efficiency required for modern logistics.

The rise of leading platforms such as Alibaba and JD.com, alongside the global proliferation of retail chains, has sustained demand for versatile materials. Polyethylene and polypropylene resins are increasingly preferred for their adaptability across diverse applications, from protective wraps to branded containers. This trend is expected to intensify as consumer purchasing behavior continues to shift toward online channels, particularly in Asia-Pacific and North America.

Food and Beverage Industry Growth with Safety and Preservation Focus

The food and beverage sector dominates packaging resin applications with consistent year-on-year growth. Consumer demand for packaged, ready-to-eat, and convenience foods has intensified globally, driven by urbanization and changing lifestyle patterns, particularly in emerging economies. This dominance is attributed to polyethylene and polypropylene's exceptional barrier properties against moisture and oxygen, which significantly extend product shelf life and maintain freshness. High-Density Polyethylene (HDPE) is particularly favored for rigid containers and bottles due to its superior chemical resistance and durability, while low-density polyethylene (LDPE) is extensively used for flexible films and squeeze bottles.

The global rise in processed food consumption, driven by hectic work-life schedules and urbanization, continues to amplify demand for reliable, cost-effective packaging solutions. Major beverage manufacturers are increasingly adopting multi-material and multilayer resin structures to enhance product protection and meet stringent regulatory requirements for food contact safety established by the U.S. Food and Drug Administration (FDA) and European Food Safety Authority (EFSA).

Restraints - Stringent Regulatory Compliance and Compliance Costs

The packaging resins industry is increasingly challenged by stringent regulatory frameworks across major markets. The European Union’s REACH regulation imposes comprehensive standards on chemical substances used in packaging, resulting in prolonged product development cycles and significant compliance costs. Similarly, mandates from the U.S. Consumer Product Safety Commission and equivalent authorities in other regions require extensive testing and documentation, particularly for food-contact applications.

Leading companies, such as BASF SE, report that compliance with these regulations can delay product launches by several months and substantially increase operational expenses. Smaller manufacturers, lacking specialized regulatory expertise, face even greater barriers to entry. Consequently, these compliance obligations compel established players to allocate considerable resources to regulatory management rather than to innovation and market expansion, thereby limiting the overall industry's growth potential.

Consumer Pushback Against Plastic Waste and Alternative Materials Competition

Increasing consumer environmental awareness has created significant challenges for traditional plastic-based packaging resins. Regulatory measures, including single-use plastic bans across multiple jurisdictions such as the European Union, have curtailed demand for conventional resin applications. Consumer preferences are shifting toward sustainable alternatives like paper-based packaging, glass, and biodegradable materials, intensifying competitive pressures on resin manufacturers.

Furthermore, heightened visibility of plastic pollution in oceans and landfills has driven major brands to reduce plastic content in their packaging portfolios. This sentiment, reinforced by environmental advocacy groups, has prompted retailers and consumer goods companies to explore alternative materials, directly impacting resin market growth. The uncertainty surrounding plastic’s long-term viability is compelling brand owners to diversify packaging strategies, reducing reliance on traditional resins and contributing to volatility in demand.

Opportunity - Recycled Content Mandates and Circular Economy Materials Demand

Extended Producer Responsibility (EPR) regulations across multiple jurisdictions are creating substantial opportunities for manufacturers investing in recycled resin technologies. The European Union's Packaging and Packaging Waste Regulation (PPWR) mandates that single-use plastic beverage bottles contain at least 30% recycled content by 2030, escalating to 65% by 2040, creating considerable demand for high-quality recycled resin materials. India's Extended Producer Responsibility rules require 30% recycled content in 2024-2025, escalating to 60% by 2027-2028, representing substantial growth potential in the Asia-Pacific region. The Global Recycled Standard (GRS) certification and Recycled Claimed Standard (RCS) certification have established clear traceability frameworks, enabling manufacturers to differentiate products through sustainability credentials.

Major companies, including Dow Inc., have launched innovations such as the INNATE™ TF 220 Precision Packaging Resin and REVOLOOP™ Post-Consumer Recycled Resin, demonstrating the commercial viability of advanced recycled content solutions. This regulatory momentum creates competitive advantages for companies developing scalable recycling infrastructure and recycled resin production capabilities, positioning them to capture growing demand from brand owners committed to sustainability targets.

Smart Packaging Technology Integration and Supply Chain Transparency

The integration of digital technologies with packaging presents a substantial growth opportunity. Smart packaging solutions incorporating RFID tags, QR codes, and NFC technology are transforming product traceability and consumer engagement, particularly in the food and beverage sector. These innovations enable real-time supply chain tracking, facilitate rapid product recalls, authenticate goods, and monitor shelf life, addressing critical needs in pharmaceutical and perishable goods markets.

Adoption of smart packaging is accelerating globally, driven by regulatory mandates such as the EU’s Falsified Medicines Directive (FMD) and rising consumer demand for transparency on product origin and sustainability. Flexible plastic packaging resins serve as ideal substrates for these technologies, offering cost-effectiveness and performance. Manufacturers developing resin formulations compatible with printing, lamination, and digital integration are well-positioned to capture growing demand from brand owners and compliance-driven applications.

Category-wise Analysis

Product Type Insights

Polyethylene resins hold a dominant position in the packaging resins market, with 48% of the market share, driven by their versatility and performance. High-Density Polyethylene (HDPE) accounts for approximately 52.4% of polyethylene applications, owing to its superior durability, chemical resistance, and recyclability, qualities essential for beverage bottles, food containers, and household packaging. Low-Density Polyethylene (LDPE) accounts for around 29% of polyethylene revenue, supported by strong demand for its flexibility, transparency, and moisture resistance, making it ideal for films, bags, and pouches across the food, medical, and industrial sectors.

This leadership reflects polyethylene’s unmatched balance of cost-effectiveness, functionality, and established manufacturing infrastructure. Growing consumer preference for lightweight, recyclable packaging and ongoing investments in recycling technologies and barrier-enhanced grades further reinforce polyethylene’s competitive advantage across diverse applications.

Application Insights

The food & beverages segment is the largest application category for packaging resins, accounting for approximately 47% of global market share, significantly surpassing consumer goods, healthcare, and industrial sectors. This dominance is driven by polyethylene and polypropylene’s superior properties, including moisture resistance, chemical inertness, light-blocking capability, and cost efficiency, which meet critical requirements for perishable products. HDPE is widely used in rigid containers for juices, dairy, and condiments, while LDPE and LLDPE films serve flexible formats such as bags, pouches, and laminates for snacks and confectionery.

UNIDO reports a 15% annual growth in food packaging production, fueled by urbanization and rising living standards in the Asia-Pacific, particularly China, India, and Southeast Asia. PET is increasingly favored for premium beverages due to its clarity, transparency, and recyclability, with its market projected to grow from US$ 52.94 billion in 2024 to US$ 109.63 billion by 2032 at a 9.5% CAGR. Regulatory compliance with FDA, EFSA, and emerging PFAS restrictions continues to drive innovation in food-grade resin formulations and advanced barrier technologies.

Regional Insights

North America Packaging Resins Trends

North America commands a substantial share of the global packaging resins market, supported by its mature food and beverage industry, strong pharmaceutical packaging demand, and advanced innovation ecosystem. The U.S. market, valued at approximately US$ 14.34 billion in 2025, benefits from robust manufacturing infrastructure, significant investments in sustainable packaging technologies, and efficient supply chain networks. High-Density Polyethylene (HDPE) remains the dominant material, widely used in beverage bottles, food containers, and chemical-resistant applications.

Regulatory pressures from the FDA and state-level plastic reduction mandates are accelerating the shift toward recyclable and sustainable resin solutions. Additionally, rapid e-commerce growth and rising consumer preference for lightweight, convenient packaging continue to drive demand for polyethylene and polypropylene. Investments in design-for-recyclability and circular economy initiatives position North American manufacturers as leaders in sustainable packaging innovation.

Europe Packaging Resins Market Trends

Europe is a highly regulated yet innovation-driven market for packaging resins, shaped by the European Union’s Packaging and Packaging Waste Regulation (PPWR) and the Single-Use Plastics (SUP) Directive, which are steering the industry toward circular-economy solutions. These regulations mandate 77% separate collection of plastic bottles by 2025, rising to 90% by 2029, creating strong demand for advanced recycling infrastructure and recycled resin materials. Europe leads globally in recycled PET adoption, with 39% of locally produced recycled PET re-entering bottle applications in 2024, reflecting significant progress in circularity.

Major consumption hubs include Germany, the U.K., France, and Spain, with Germany and France at the forefront of sustainable packaging innovation and chemical recycling technologies. Manufacturers are accelerating investments in bio-based resins and design-for-recyclability principles, leveraging extended producer responsibility schemes to gain competitive advantages through premium-grade recycled materials and innovative packaging solutions aligned with sustainability goals.

Asia Pacific Packaging Resins Trends

Asia Pacific remains the dominant region in global packaging resin consumption, accounting for approximately 54.3% of the market share. This leadership is driven by rapid industrialization, urbanization, and strong growth in consumer goods and pharmaceutical sectors. China leads as the world’s manufacturing hub, with e-commerce expansion and sustainability initiatives under “Double Carbon” goals accelerating the adoption of recyclable materials.

India’s market is expanding through infrastructure investments and rising food and beverage demand, supported by major players like Reliance Industries. Japan and South Korea spearhead sustainable packaging innovations and specialized resin applications for electronics and pharmaceuticals. The region’s cost competitiveness, manufacturing scale, and growing consumer base ensure sustained momentum, while increasing adoption of flexible plastic packaging and smart technologies positions Asia-Pacific as the fastest-growing market through the forecast period.

Competitive Landscape

The packaging resins market demonstrates moderate consolidation, with leading integrated chemical companies such as Dow Inc., BASF SE, ExxonMobil Corporation, and LyondellBasell Industries N.V. holding significant production capacity and technological expertise globally. These players differentiate through specialized resin grades, investments in sustainable formulations, and strategic partnerships across the packaging value chain. Emerging competitors, particularly in Asia-Pacific, are expanding regional production and offering cost-effective solutions for price-sensitive segments. Consolidation trends include acquisitions, joint ventures for recycling infrastructure, and collaborations with brands committed to sustainability. Key competitive advantages include advanced polymer chemistry, global distribution networks, technical support capabilities, and investments in circular economy technologies such as advanced recycling and bio-based resin production.

Key Market Developments

- June 2025: Dow Inc. announced the commercial launch of INNATE™ TF 220 Precision Packaging Resin, a high-density polyethylene innovation specifically designed to enable design-for-recyclability in flexible packaging applications

- June 2025: Dow Inc. established a strategic collaboration with the Chinese laundry detergent brand Liby, integrating 10% REVOLOOP™ Post-Consumer Recycled (PCR) Resin into the Floral Era detergent series packaging.

- January 2024: LyondellBasell Industries Holdings B.V. executed an agreement to acquire 35% stake in Saudi Arabia-based National Petrochemical Industrial Company (Natpet) from Alujain Corporation for approximately USD 500 million, expanding polypropylene production capacity and strengthening integrated operations in Middle Eastern petrochemical complexes.

Top Companies in the Packaging Resins Market

Dow Inc. (Midland, U.S.), a leading materials science company, commands a significant market presence through advanced polyethylene and polypropylene resin portfolios, a strategic focus on sustainable packaging solutions, including recycled-content formulations, and investments in circular-economy technologies.

BASF SE (Ludwigshafen, Germany) operates as one of the world's largest chemical manufacturers, offering comprehensive thermoplastic and specialty resin portfolios, including polyolefins, polyesters, and engineering plastics serving packaging and industrial applications. The company's extensive research and development capabilities, global distribution networks, and commitment to sustainable material innovation enable broad market presence across North America, Europe, and the Asia-Pacific regions, supporting diverse customer requirements in rigid and flexible packaging applications.

LyondellBasell Industries N.V. (Houston, Netherlands) maintains a leadership position through integrated polyolefins production, advanced polypropylene technology platforms, and strategic investments in recycling infrastructure and advanced polymers. The company's proprietary Spheripol polypropylene technology and expanding geographic footprint enable competitive positioning across major market segments, supporting customers' sustainability objectives through recycled content formulations and advanced barrier resin solutions.

Companies Covered in Packaging Resins Market

- Dow Inc.

- BASF SE

- ExxonMobil Corporation

- LyondellBasell Industries N.V.

- INEOS

- PetroChina Companies Ltd.

- Reliance Industries

- Sinopec

- SABIC

- Braskem

- Indorama Ventures Public Company Limited

- China Petroleum & Chemical Corporation

- Borealis AG

- Formosa Plastics Corporation

Frequently Asked Questions

The global packaging resins market is valued at US$ 344.0 billion in 2026 and projected to reach US$ 574.5 billion by 2033, representing substantial expansion at a 7.6% CAGR driven by e-commerce growth, food and beverage industry expansion, and sustainability regulatory mandates.

Primary growth drivers include explosive e-commerce expansion reaching 2.64 billion online shoppers, rising food and beverage industry demand, particularly in emerging markets urbanizing rapidly, stringent regulatory mandates requiring 30-65% recycled content in packaging by 2030-2040, and consumer preference for lightweight, convenient packaging solutions supporting operational efficiency.

Polyethylene resins command market dominance, with 48% of the market share, driven by superior durability, chemical resistance, recyclability, and cost-effectiveness in beverage bottles and food containers essential for consumer goods packaging.

Asia Pacific dominates with 54.3% global market share, driven by China's manufacturing dominance, India's infrastructure expansion, and rapid e-commerce growth.

Circular economy materials incorporating recycled content and smart packaging technology integration represent the most significant opportunities, with regulatory mandates requiring 30-65% recycled content by 2030-2040, creating substantial demand for advanced recycling infrastructure.