- Automation & Robotics

- Non-Lethal Weapons Market

Non-Lethal Weapons Market Size, Share, and Growth Forecast 2026 - 2033

Non-Lethal Weapons Market by Product Type (Gases & Sprays, Ammunition, Area Denial, Explosives, Directed Energy, Electroshock, Other), Technology (Chemical, Acoustic, Electrical, Blunt Impact, Projectile), Range (Short, Medium, Long), Application (Crowd Control, Law Enforcement Operations, Border Security, Self-Defense, Other), End-user (Defense/Military, Law Enforcement, Civil & Commercial), and Regional Analysis for 2026 - 2033

Non-Lethal Weapons Market Size and Trend Analysis

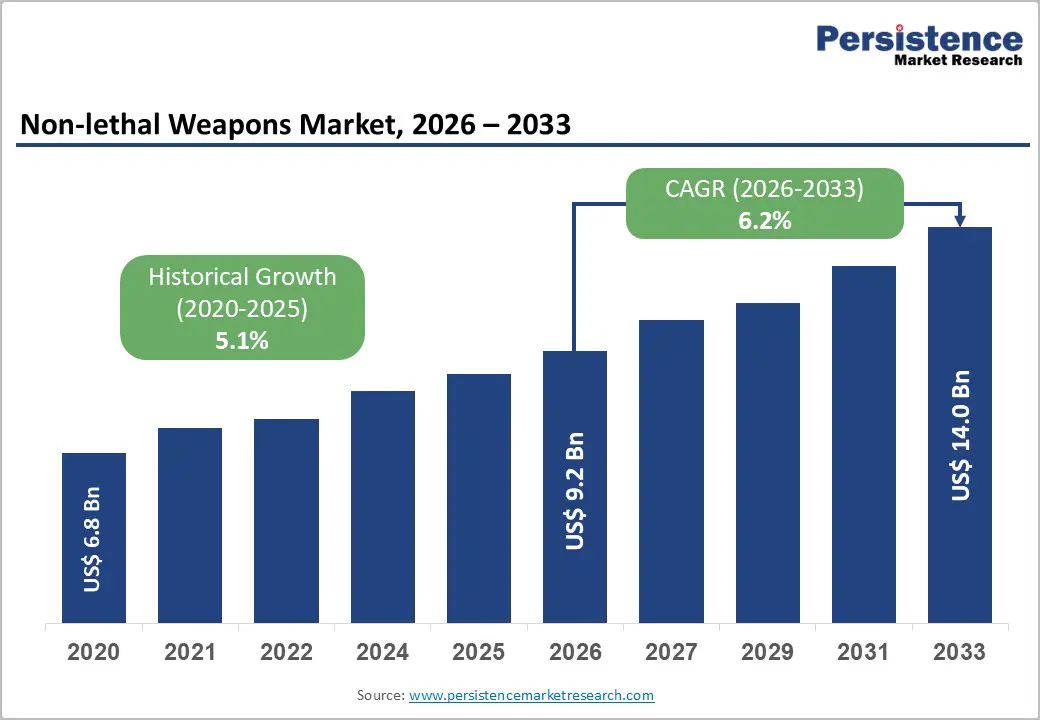

The global non-lethal weapons market is valued at US$ 9.2 billion in 2026 and is projected to reach US$ 14.0 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033. This growth is primarily driven by the escalating frequency of civil unrest and geopolitical conflicts worldwide, compelling governments and law enforcement agencies to seek effective yet humane crowd control solutions.

According to the Institute for Economics and Peace (IEP) Global Terrorism Index 2023, terrorism-related fatalities surged 22% to 8,352, the highest since 2017, intensifying the demand for non-lethal alternatives. Furthermore, mounting regulatory pressure on the proportional use of force, combined with continuous innovation in directed energy and acoustic technologies, is reinforcing sustained market expansion through the forecast horizon.

Key Industry Highlights:

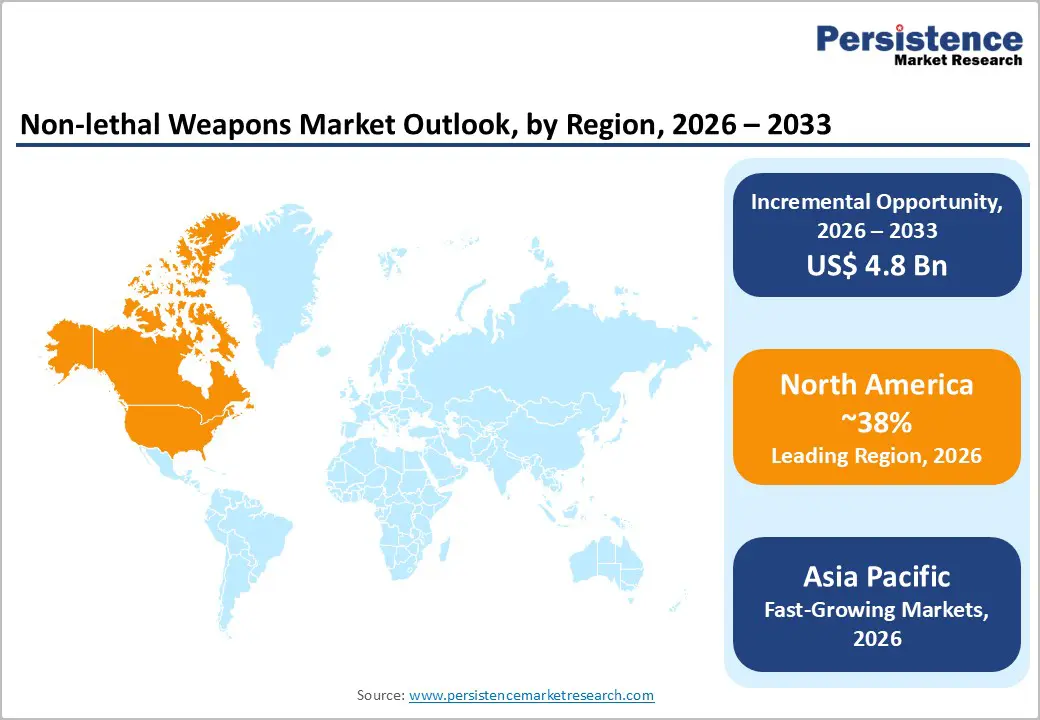

- Leading Region: North America leads the global non-lethal weapons market with approximately 38% revenue share, driven by advanced R&D infrastructure, substantial law enforcement budgets, and the presence of major manufacturers including Axon and Safariland.

- Fastest Growing Region: Asia Pacific is the fastest growing non-lethal weapons market, propelled by escalating defense spending in India and China, rapid urbanization, and government-mandated police modernization programs increasingly requiring less-lethal solutions.

- Dominant Segment: Gases & Sprays hold the largest product-type share, with 30%, in the non-lethal weapons market, valued for their cost-effectiveness, portability, and proven efficacy in crowd dispersal and riot control across institutional and civilian applications.

- Fastest Growing Segment: Directed Energy Weapons is the fastest growing segment in the non-lethal weapons market, forecast to register the highest CAGR through 2033, driven by precision targeting capability, AI integration, and zero-ammunition-cost operational benefits for security forces.

- Key Market Opportunity: Civil & Commercial end-user demand represents the highest-growth opportunity in the non-lethal weapons market, such as rising personal safety concerns, retail availability of compact devices, and favorable regulation drive mass-market adoption of less-lethal self-defense products.

| Key Insights | Details |

|---|---|

|

Non-Lethal Weapons Market Size (2026E) |

US$ 9.2 Bn |

|

Market Value Forecast (2033F) |

US$ 14.0 Bn |

|

Projected Growth CAGR (2026–2033) |

6.2% |

|

Historical Market Growth (2020–2025) |

5.1% |

DRO Analysis

Drivers - Rising Civil Unrest and Global Security Threats

The proliferation of civil unrest, political violence, and terrorism across both developed and developing nations is a primary catalyst for the non-lethal weapons market. The Armed Conflict Location and Event Data (ACLED) project recorded over 165,273 political violence events globally between July 2023 and June 2024, representing a 15% increase year-on-year and a staggering 64% increase since 2016. In response, the U.S. Department of Homeland Security (DHS) allocated US$ 45 Mn in 2024 specifically for advanced non-lethal weapons for riot control.

France's widespread 2024 pension-reform protests, which saw law enforcement deploy tear gas and water cannons extensively, and similar unrest scenarios across Latin America and South Asia, underscore the irreplaceable operational role of non-lethal systems in modern public-order management. As urban populations grow, so does the frequency and scale of such events, making non-lethal solutions structurally indispensable for security forces.

Military Modernization Programs and Peacekeeping Mandates

Defence budget expansions and military modernization initiatives globally are broadening the adoption of non-lethal weapons beyond law enforcement into active military deployment. NATO member states have progressively integrated less-lethal munitions into their rules of engagement for peacekeeping operations, while the United Nations Institute for Disarmament Research (UNIDIR) has documented growing incorporation of rubber bullets and stun grenades by UN peacekeeping forces to reduce civilian casualties in conflict zones.

The U.S. Air Force Security Forces Center (AFSFC) partnered with the Joint Intermediate Force Capabilities Office in May 2024 to deploy advanced non-lethal technologies across security force units. Simultaneously, rising defence budgets in Asia-Pacific nations, with India's defence allocation crossing US$ 75 Bn in fiscal year 2024–25, are generating substantial procurement opportunities for manufacturers offering scalable, compliant, and technologically advanced non-lethal solutions.

Restraints - Ethical and Legal Concerns Surrounding Deployment

Despite their classification as non-lethal, these weapons can inflict serious injuries or cause fatalities under certain conditions, generating persistent ethical and legal scrutiny. Organizations such as Amnesty International and Human Rights Watch have documented cases where rubber bullets and chemical agents caused permanent eye damage, respiratory harm, and even deaths. Inconsistent deployment standards, insufficient training protocols, and unclear proportionality thresholds across jurisdictions raise liability risks for procuring agencies. Legal uncertainty around the classification and export of certain directed-energy systems under frameworks such as the Wassenaar Arrangement further complicates cross-border trade, constraining international market expansion.

High Development Costs and Technological Readiness Gaps

Advanced non-lethal weapons, particularly directed-energy systems such as Active Denial Systems and Long-Range Acoustic Devices (LRADs), entail significant research, development, and production costs, restricting adoption primarily to well-funded defense establishments. Emerging economies with constrained defense budgets frequently rely on conventional, lower-technology alternatives, limiting market penetration for premium segments. Moreover, inconsistencies in field performance under adverse environmental conditions, such as wind dispersion affecting chemical agents or electronic interference impacting electroshock weapons, create reliability concerns that slow procurement decisions among critical end users.

Opportunities - Directed Energy Weapons are emerging as the Next Frontier in Crowd Control Technology

Directed energy weapons (DEWs) represent one of the highest-growth opportunity areas within the non-lethal weapons landscape. Systems such as millimeter-wave Active Denial Systems project energy to create a temporary, intense heating sensation on the skin, compelling dispersal without physical projectiles or chemical residue. In November 2024, China unveiled the WB-1 directed-energy non-lethal weapon at the Zhuhai Airshow, developed by Poly Group, with an effective range of up to 1 km, demonstrating sovereign interest in long-range crowd deterrence.

The DEW segment is forecast to grow at the fastest CAGR among all product categories through 2033, driven by its precision targeting, scalability, reduced collateral risk, and absence of consumable ammunition. Investment in AI-integrated targeting systems is further amplifying operational efficiency, making DEWs increasingly attractive for both law enforcement and military procurement agencies globally.

Expanding Civil and Commercial Self-Defense Market

The civil and commercial end-user segment, encompassing personal self-defense, private security firms, and corrections facilities, is emerging as the fastest-growing demand pocket in the non-lethal weapons market. Rising urban crime rates, growing personal safety awareness, and evolving retail availability of compact, less-lethal devices are reshaping consumer behavior. In February 2025, Byrna Technologies launched a CO2-powered non-lethal pistol in Franklin, Tennessee, targeting personal protection use cases without lethal force.

In January 2025, PepperBall introduced its BURST area-saturation device, which incorporates a 130-decibel auditory deterrent alongside advanced payload dispersal technology. Concurrently, regulatory frameworks across key markets are increasingly facilitating civilian ownership of less-lethal devices, thereby expanding the addressable market and creating attractive revenue opportunities for manufacturers seeking to diversify beyond institutional customers.

Category-wise Analysis

Product Type Insights

The gases and sprays represent the dominant product category within the global non-lethal weapons market, accounting for roughly 30% of total revenue in 2025. This position is supported by the extensive use of tear gas, pepper spray, and chemical irritant grenades across law enforcement, military, and civilian self-defense applications. Key attributes such as cost efficiency, operational simplicity, portability, and rapid crowd-dispersal capability, without intent to cause lasting injury, have firmly established gases and sprays as standard first-response measures for security forces worldwide.

Consistent institutional procurement by police departments and paramilitary organizations sustains stable demand, while rising consumer sales of pepper sprays and gels further bolster revenues in the civil segment. Long-standing operational use of CS gas and Oleoresin Capsicum sprays continues to reinforce institutional confidence. Meanwhile, the Directed Energy segment is anticipated to experience the most rapid growth over the forecast period.

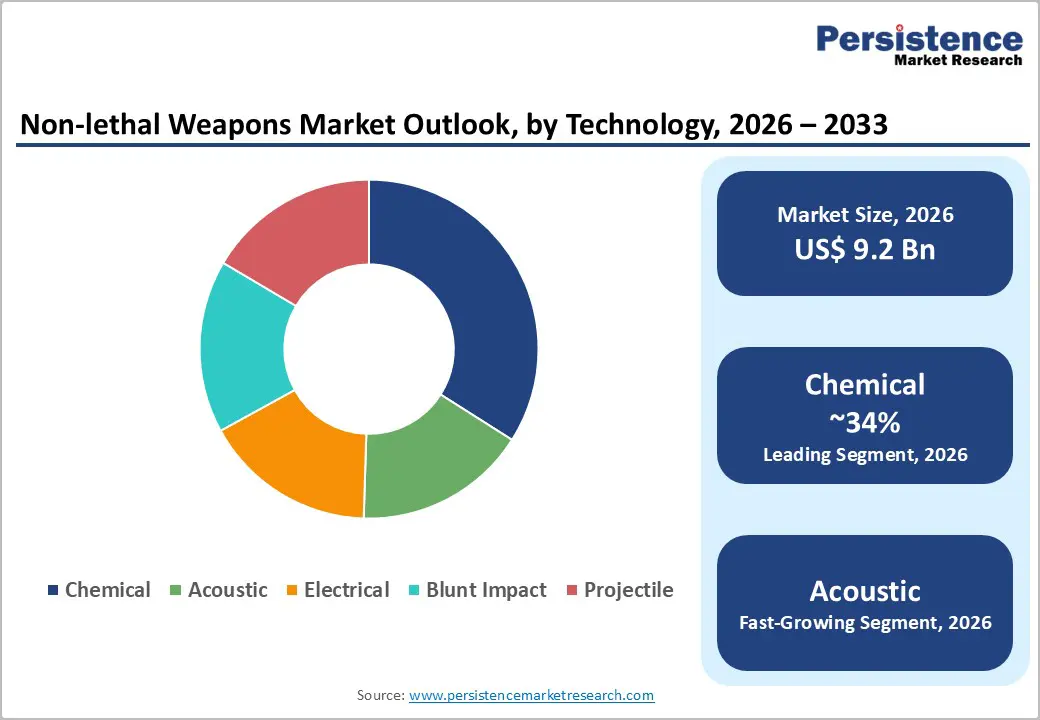

Technology Analysis

The chemical technology segment holds the largest share of the global non-lethal weapons market by technology, accounting for approximately 34% of total revenue. This dominance is attributed to the widespread adoption of chemical-based systems, including riot control agents such as CS gas, Oleoresin Capsicum (OC), and CN gas, which are valued for their operational versatility, rapid incapacitation effectiveness, and the limited risk of permanent physiological harm when deployed in accordance with established protocols.

The bunt impact technology comprising rubber bullets, bean bag rounds, and other kinetic projectiles, represents the second-largest contributor. Meanwhile, Acoustic technologies, such as Long-Range Acoustic Devices and sound cannons, are gaining increased adoption in naval, border security, and anti-piracy applications due to their extended engagement range and non-contact deterrence capabilities.

Range Analysis

The medium range (30 to 100 meters) segment dominates the non-lethal weapons market by operational range, holding approximately 46% of total revenue. This leadership reflects the segment's practical versatility in the most common operational contexts, crowd control, urban law enforcement, and civil disturbance management, where engagement distances are typically within this band. Medium-range systems such as rubber bullets, bean bag rounds, and acoustic hailing devices provide an effective balance between operational safety distance and incapacitation efficacy.

In August 2023, Byrna Technologies Inc. announced broad adoption of its Byrna HD Launcher by law enforcement agencies across the U.S. for precisely this range profile. The Long Range (above 100 meters) segment is projected to register the fastest CAGR through 2033, driven by technology innovations in directed energy and advanced acoustic systems that extend engagement envelopes while preserving mission-critical non-lethality standards.

Application Insights

The crowd control application segment constitutes the largest share of the global non-lethal weapons market, accounting for approximately 38% of total revenue. This leadership is driven by the increasing frequency and scale of protests, civil disturbances, and mass demonstrations worldwide, which have elevated crowd management to a critical operational priority for security agencies. Law enforcement authorities across regions continue to formalize the use of tear gas, rubber bullets, water cannons, and stun grenades as standard components of crowd control arsenals.

Furthermore, the Border Security application is emerging as a high-growth segment, as authorities seek to address illegal migration and cross-border security challenges while minimizing fatalities. The deployment of acoustic hailing devices by the Republic of Singapore Navy in 2023 exemplifies the expanding application of non-lethal systems across maritime, naval, and border enforcement operations.

End-user Insights

The defense/military segment is the dominant end user in the non-lethal weapons market, contributing approximately 68% of total revenue. This dominance is driven by the scale of institutional procurement by national armed forces, paramilitary units, and peacekeeping contingents, which require non-lethal capabilities across a wider range of operational environments than law enforcement. Compliance with International Humanitarian Law (IHL) and UN peacekeeping mandates that emphasize casualty minimization reinforces this structural demand.

The Law Enforcement segment is the second-largest contributor, with widespread adoption of tasers, pepper sprays, and less-lethal munitions by police departments globally. In May 2023, Axon Enterprise Inc. secured a US$ 5 Mn contract with the Baltimore Police Department for advanced non-lethal weapon systems with enhanced control systems. The Civil & Commercial segment is the fastest growing, propelled by rising personal safety awareness and consumer demand.

Regional Insights

North America Non-Lethal Weapons Trends

North America represents the largest regional market for non-lethal weapons, accounting for an estimated 38% of global revenue in 2025. Federal commitment to the sector is reflected in the Department of Homeland Security’s US$45 million allocation for non-lethal weapons in 2024, as well as the U.S. Air Force Security Forces Center’s partnership with the Joint Intermediate Force Capabilities Office to advance next-generation deployments.

Additionally, regulatory frameworks, including the Department of Defense’s Directive 3000.3E and evolving Department of Justice use-of-force guidelines, continue to steer procurement toward less-lethal alternatives. Canada also supports market growth through federal public safety investments, albeit at a smaller scale, while innovation hubs in states such as Arizona and Florida sustain a robust regional R&D ecosystem.

Europe Non-Lethal Weapons Trends

Europe represents the second-largest regional market for non-lethal weapons, driven by rising levels of civil unrest, anti-government demonstrations, and persistent terrorism-related security concerns across member states. Germany, France, the United Kingdom, and Spain constitute the principal markets in the region. France’s 2024 pension reform protests, marked by extensive use of tear gas and water cannons, have reinforced ongoing procurement commitments by law enforcement authorities.

The European Defence Agency has increasingly recognized non-lethal capabilities as integral to the European Union’s common security and defence policy. Concurrently, regulatory harmonization under EU law enforcement cooperation frameworks, along with geopolitical spillovers from international tensions, is encouraging European governments to strengthen border security capabilities. Ongoing updates to the UK Home Office’s approved equipment lists and the growing presence of specialized European startups contribute to a moderately fragmented competitive landscape.

Asia Pacific Non-Lethal Weapons Trends

Asia Pacific is the fastest-growing region in the global non-lethal weapons market, propelled by rising defense expenditures, accelerated urbanization, and increasingly complex internal security challenges. China continues to invest heavily in indigenous non-lethal technologies, exemplified by the unveiling of the WB-1 millimeter-wave directed-energy weapon in November 2024, aimed at managing large urban populations and reinforcing domestic stability.

India’s multifaceted internal security environment, coupled with a defense budget exceeding US$75 billion in FY2024–25, is driving structured procurement of advanced crowd control munitions and non-lethal border security systems. Japan’s strategic stance against fully autonomous weapons is indirectly supporting the integration of non-lethal systems within its defense doctrine. Across the ASEAN region, heightened border security and counter-terrorism imperatives are accelerating the adoption of acoustic systems, chemical agents, and kinetic less-lethal munitions.

Competitive Landscape

The global non-lethal weapons market is moderately fragmented, characterized by the coexistence of large integrated defense contractors and highly specialized less-lethal manufacturers. Leading players leverage scale, established government relationships, and broad product portfolios. Axon Enterprise and Rheinmetall AG represent the technology-intensive tier, investing heavily in AI-integrated systems and directed energy. Strategic M&A, notably EDGE Group's acquisition of a majority stake in Condor Non-Lethal Technologies (April 2024), signals consolidation aimed at geographic expansion. Smaller specialists such as Byrna Technologies and NonLethal Technologies, Inc. are gaining traction in the civilian and law enforcement sub-segments through product innovation and direct-to-consumer channels. R&D investment in smart projectiles, autonomous drones, and acoustic deterrents is reshaping competitive differentiation.

Key Developments:

- February 2026: Vector announced a strategic partnership with Nammo Defense Systems to develop kinetically integrated unmanned aerial systems (UAS) combining drone platforms with advanced munitions capabilities. The collaboration focuses on producing small, American-made UAS platforms integrated with allied-manufactured munitions.

- February 2026: The Philippine National Police - Police Regional Office Bangsamoro Autonomous Region (PRO BARMM) has invited bids for the supply and delivery of a large number of non-lethal weapons for FY2026. The evaluation process will adhere to the "lowest calculated responsive bid" criteria, ensuring the equipment complies with the PNP's operational standards for crowd control and tactical operations while maintaining cost efficiency.

- September 2025: Genasys Inc. announced that it secured a USD 9 million order from the United States Army for its Long Range Acoustic Device (LRAD) systems. These systems will be integrated into the Common Remotely Operated Weapon Stations (CROWS II) under a technical refresh program.

Top Companies in Non-Lethal Weapons

Axon Enterprise, Inc. (Scottsdale, USA) is the market-defining leader in electroshock weapons and integrated law enforcement technology. Its TASER product line is the most widely adopted electroshock weapon globally, deployed by police agencies across over 100 countries. The company's acquisition of Dedrone in May 2024 underscores its strategy to extend into counter-drone and airspace security, broadening its non-lethal solutions portfolio significantly beyond traditional products.

Rheinmetall AG (Düsseldorf, Germany) is Europe's premier defense manufacturer with a comprehensive non-lethal weapons portfolio spanning acoustic hailing devices, less-lethal munitions, and directed-energy crowd control systems. Its September 2023 successful test of a long-range acoustic hailing device capable of dispersal at over 1,000 meters illustrates its leadership in advancing non-lethal system range and technology. The company serves NATO military establishments and allied law enforcement agencies across over 40 nations.

Safariland, LLC (Jacksonville, USA) is one of the most established full-portfolio non-lethal weapons manufacturers in the world, with products spanning chemical aerosols, kinetic munitions, and batons for law enforcement. The company's partnership with 3DLOOK for AI-driven body scanning in tactical armor and its extensive global distribution network underscore its commitment to technology integration and broad market reach across institutional end users.

Companies Covered in Non-Lethal Weapons Market

- Axon Enterprise

- Safariland

- Rheinmetall AG

- Combined Systems

- Genasys Inc.

- Nammo AS

- Ultra Electronics

- Byrna Technologies

- Condor

- NonLethal Technologies

- Zarc International

- Armament Systems and Procedures

- PepperBall Technologies

- AMTEC

- FN Herstal

- Lamperd Less Lethal

- Fiocchi Munizioni

Frequently Asked Questions

The global Non-Lethal Weapons market is valued at approximately US$ 9.2 Bn in 2026 and is projected to reach US$ 14.0 Bn by 2033, expanding at a CAGR of 6.2%. Historically, the market grew at a CAGR of 5.1% between 2020 and 2025, supported by rising security concerns and increasing law enforcement budgets globally.

Primary demand drivers include the escalating frequency of civil unrest and political violence, with the ACLED reporting over 165,273 political violence events globally between July 2023 and June 2024, combined with mandatory shifts in law enforcement use-of-force policies, military peacekeeping mandates from the United Nations, and continuous innovation in directed energy and acoustic technologies.

The Gases & Sprays segment is the dominant product category, accounting for approximately 30% of total revenue. These include tear gas, pepper spray, and chemical aerosols, widely adopted for their cost-effectiveness, ease of deployment, portability, and proven efficacy in crowd dispersal across law enforcement, military, and civilian applications.

North America is the leading region, accounting for approximately 38% of global market revenue. The United States drives regional dominance through high defense and law enforcement spending, presence of leading manufacturers, and strong R&D investment in non-lethal technologies. The DHS's US$ 45 Mn non-lethal weapons allocation in 2024 exemplifies ongoing federal commitment.

The Civil & Commercial end-user segment and the Directed Energy Weapons product segment represent the most compelling growth opportunities. The former is driven by rising personal safety awareness and expanding retail availability, while the latter benefits from precision targeting, AI integration, and increasing government procurement for advanced, sustainable crowd-control solutions, with the DEW segment forecast to achieve the highest product-level CAGR through 2033.

Leading companies in the global non-lethal weapons market include Axon Enterprise, Inc., Rheinmetall AG, Safariland, LLC, Combined Systems, Inc., Byrna Technologies Inc., Condor Non-Lethal Technologies, Genasys Inc., Nammo AS, and NonLethal Technologies, Inc., among others.