- Smart Packaging

- Micro Packaging Market

Micro Packaging Market Size, Share, and Growth Forecast, 2026 – 2033

Micro Packaging Market by Product Type (Films, Pouches, Bottles, Boxes & Cartons, Cans), Material (Paper & Paperboard, Glass, Metal, Plastic Copolymers), and Regional Analysis for 2026 – 2033

Micro Packaging Market Size and Trends Analysis

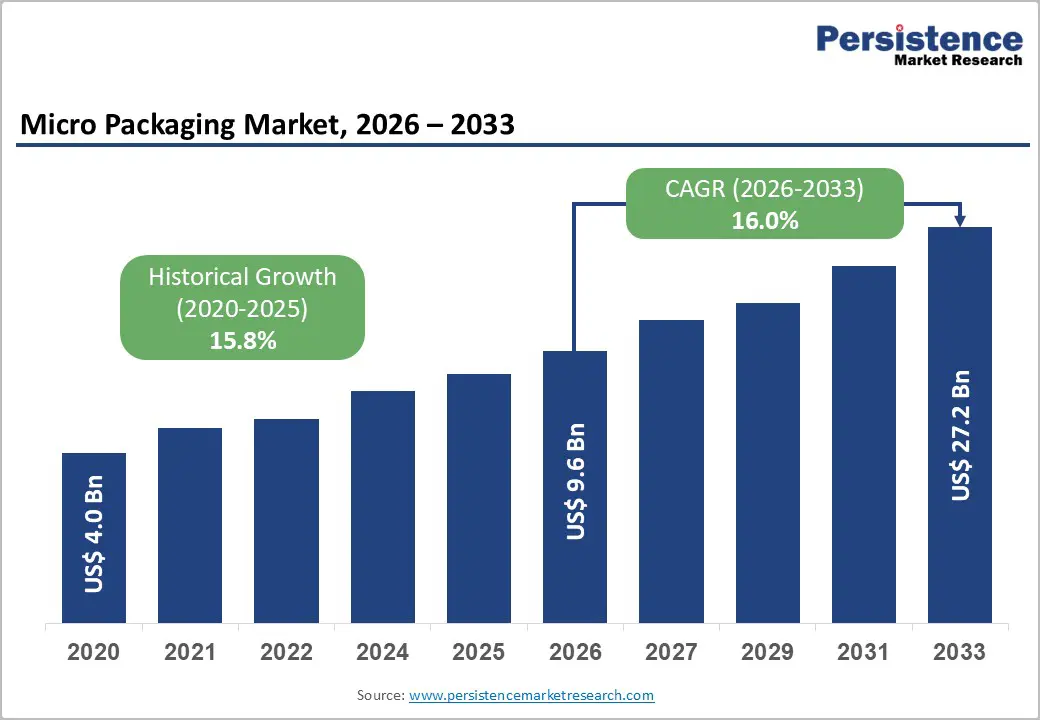

The global Micro Packaging market size is likely to be valued at US$9.6 billion in 2026 and is expected to reach US$27.2 billion by 2033, growing at a CAGR of 16.0% during the forecast period from 2026 to 2033, driven by structural shifts across pharmaceuticals, food & beverage, and advanced consumer goods packaging. Market growth is driven by nanotechnology-based barrier coatings, micro-perforation, and functional layers that improve protection while reducing material use. In pharma, micro formats ensure stability for biologics and high-potency drugs, while in food and beverage, they extend shelf life, cut waste, and support single-serve and e-commerce trends.

Key Industry Highlights:

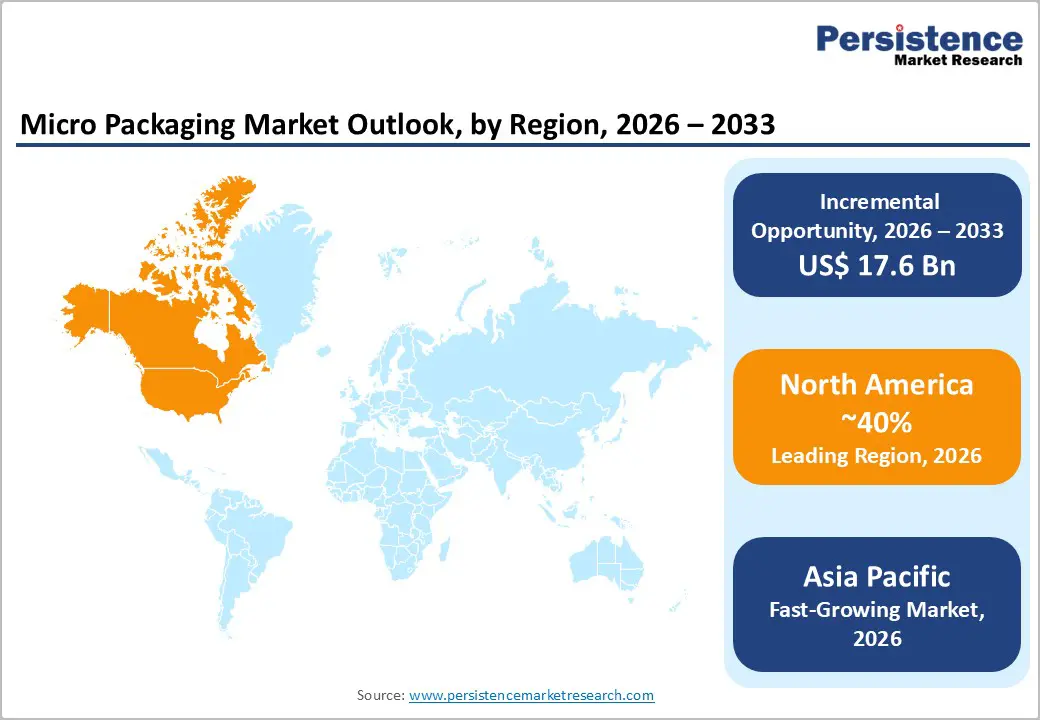

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by U.S. leadership in regulated pharmaceutical applications, advanced innovation ecosystems, and high-value precision packaging adoption.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by strong manufacturing advantages, rapid industrial scaling, and rising adoption across pharmaceuticals, electronics, and consumer goods.

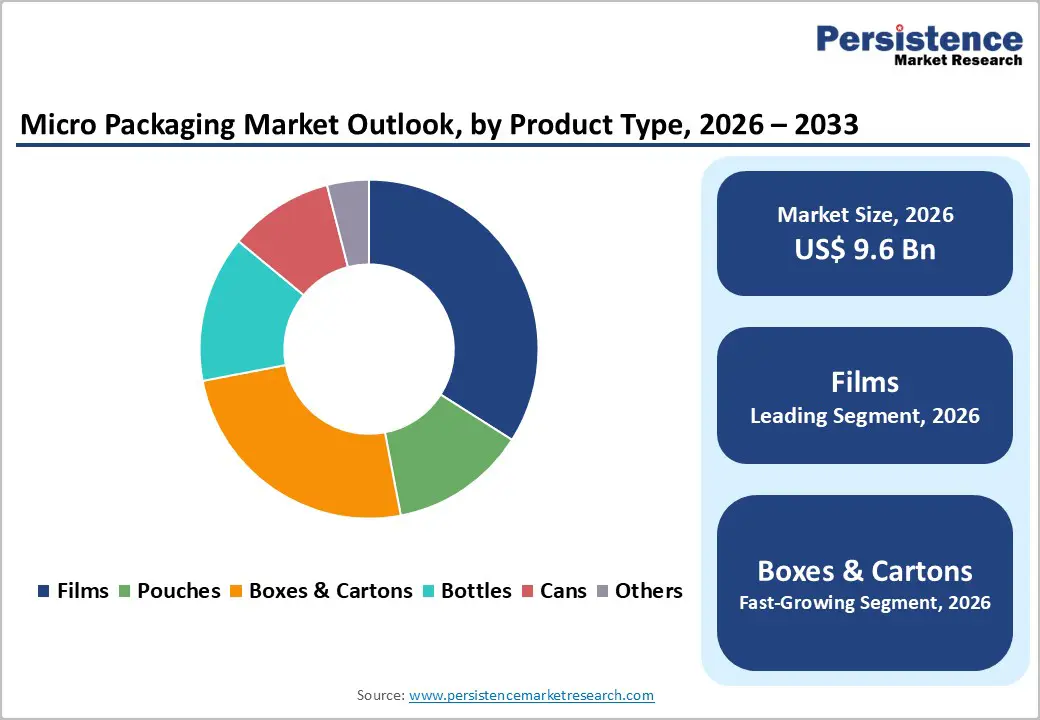

- Leading Product Type: Films are projected to represent the leading product type in 2026, accounting for 55% of the revenue share, driven by widespread use in high-barrier, micro-engineered flexible packaging applications.

- Leading Material Type: Plastic copolymers are anticipated to be the leading material type, accounting for over 55% of the revenue share in 2026, supported by their flexibility, lightweight nature, and compatibility with high-barrier nano-technologies.

| Report Attribute | Details |

|---|---|

|

Micro Packaging Market Size (2026E) |

US$9.6 Bn |

|

Market Value Forecast (2033F) |

US$27.2 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

16.0% |

|

Historical Market Growth (CAGR 2020 to 2025) |

15.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Advancements in Nanotechnology for Enhanced Barrier and Functional Properties

Nanotechnology has become a foundational driver of the micro packaging market by enabling ultra-thin, high-performance barrier layers that significantly improve resistance to oxygen, moisture, light, and microbial contamination. Nano-coatings and nano-composites allow packaging to achieve superior protection while using less material, aligning with lightweighting and sustainability goals. These technologies are particularly valuable in pharmaceutical and food applications where shelf-life extension, product integrity, and contamination control are critical. The ability to engineer functionality at the molecular level enhances packaging efficiency without increasing bulk or cost.

Beyond barrier enhancement, nanotechnology enables functional features such as antimicrobial activity, oxygen scavenging, and controlled permeability. These properties support active packaging formats that respond dynamically to environmental conditions, improving product safety and quality. In micro packaging, nanomaterials integrate seamlessly with films, pouches, and bottles, enabling scalable adoption across flexible and rigid formats. Continuous R&D investment and falling production costs are accelerating commercialization, positioning nanotechnology as a long-term growth engine that differentiates advanced micro packaging solutions from conventional alternatives.

Expansion of Biologics and Personalized Medicine Requiring Micro-Dose Formats

The rapid expansion of biologics, injectables, and personalized medicine is driving demand for micro packaging formats that enable precise dosing, sterility, and chemical stability. These therapies are highly sensitive to environmental exposure and require packaging solutions that ensure exact dose delivery while preventing degradation. Micro-dose packaging formats such as unit-dose containers, micro-vials, and high-barrier films are increasingly essential to meet these needs. Regulatory emphasis on patient safety and dosing accuracy reinforces adoption across pharmaceutical supply chains.

Personalized medicine also necessitates flexible, small-batch packaging that can accommodate varied formulations and dosage regimens. Micro packaging supports this shift by offering scalable precision without compromising compliance or performance. The ability to integrate traceability, tamper evidence, and compatibility with automated filling lines strengthens its role in advanced drug delivery systems. Pharmaceutical pipelines increasingly focus on biologics and niche therapies, and micro packaging becomes a critical enabler of innovation and commercialization.

Barrier Analysis - Emerging Microplastic, PFAS, and Single-Use Plastic Legislation

Increasing scrutiny of microplastics, PFAS compounds, and single-use plastics presents a significant restraint for the micro packaging market, particularly for polymer-based solutions. Governments and regulatory bodies are introducing stricter rules targeting material composition, recyclability, and environmental persistence. These evolving regulations create compliance uncertainty for manufacturers, especially those relying on advanced polymers and functional coatings. Navigating fragmented regional policies increases development costs and lengthens approval timelines, slowing market penetration in regulated end-use sectors.

Restrictions on PFAS and plastic additives challenge the performance advantages traditionally offered by micro packaging materials. Reformulating products without compromising barrier or functional properties requires substantial R&D investments. Smaller converters face disproportionate pressure due to limited technical resources, while larger players must balance innovation with regulatory risk. This environment favors established incumbents but constrains rapid experimentation, acting as a temporary brake on market expansion despite strong underlying demand.

Regulatory and Safety Concerns Regarding Nanoparticle Migration and Environmental Impact

Concerns over nanoparticle migration into food, pharmaceuticals, and the environment pose a critical restraint for nanotechnology-enabled micro packaging. Regulatory agencies require extensive safety validation to ensure nanoparticles do not leach into products or cause long-term health risks. This uncertainty delays approvals and increases testing costs, particularly in food-contact and pharmaceutical applications where safety thresholds are stringent. Lack of harmonized standards complicates commercialization across multiple regions.

Environmental impact considerations also influence adoption, as the long-term behavior of nanoparticles in waste streams remains under evaluation. Stakeholders face pressure to demonstrate lifecycle safety and recyclability, especially as sustainability reporting becomes mandatory. These challenges slow adoption among risk-averse brand owners and regulators, even as technological benefits are clear. Until clearer regulatory frameworks and standardized testing protocols emerge, safety concerns will continue to restrain full-scale deployment.

Opportunity Analysis - Integration of Smart and Active Technologies

The integration of smart and active technologies represents a major opportunity for the micro packaging market, enabling functionality beyond passive containment. Smart features such as freshness indicators, temperature sensors, and track-and-trace elements enhance product visibility and supply chain transparency. These capabilities are particularly valuable in pharmaceuticals, biologics, and perishable foods, where monitoring conditions directly impacts safety and efficacy. Micro packaging provides the ideal platform for embedding these technologies due to its precision and material efficiency.

Active packaging technologies, including antimicrobial layers and oxygen scavengers, expand value creation by extending shelf life and reducing waste. As digitalization and industry adoption accelerate, smart micro packaging aligns with automation, data analytics, and compliance monitoring. Brands increasingly view these solutions as differentiation tools rather than cost centers, opening high-margin opportunities for converters and technology providers across premium and regulated markets.

Development of Bio-Based and Edible Micro-Packaging Solutions

The development of bio-based and edible micro packaging solutions presents a transformative opportunity aligned with sustainability and regulatory priorities. Fiber-based materials, biopolymers, and edible coatings enable micro packaging to deliver required performance while minimizing environmental impact. Advances in bio-barrier coatings now allow these materials to achieve moisture and oxygen resistance comparable to traditional plastics. This evolution supports circular economy goals and attracts eco-conscious consumers and brand owners.

Edible and compostable micro packaging formats are particularly attractive for single-serve food, nutraceuticals, and pharmaceutical supplements. These solutions reduce waste while maintaining functionality, opening new application areas where disposal concerns previously limited adoption. Investment in bio-material R&D and scalable manufacturing positions early adopters to capture premium demand. As regulations tighten around plastic use, bio-based micro packaging is poised to shift from niche innovation to mainstream growth driver.

Category-wise Analysis

Product Type Insights

Films are expected to lead the micro packaging market, accounting for approximately 55% of revenue in 2026, driven by their adaptability, high barrier efficiency, and compatibility with nanotechnology-driven enhancements. Micro packaging films are widely used in food and pharmaceutical applications where impermeability to oxygen, moisture, and contaminants is critical. Their thin structure allows for nano-coatings, micro-perforation, and active layers without increasing material consumption, supporting lightweighting initiatives. For example, the use of micro-perforated barrier films in fresh food packaging, where controlled gas exchange extends shelf life while maintaining product freshness.

Pouches are likely to represent the fastest-growing segment in 2026, supported by demand for convenience, portion control, and e-commerce compatibility. Their resaleable designs, space efficiency, and ability to incorporate smart and active features make them ideal for modern consumption patterns. Micro packaging pouches support advanced laminates that enhance shelf life while reducing material usage compared to rigid alternatives. For example, the adoption of micro-dose pouches for nutritional supplements, which combine precise portioning with high-barrier protection.

Material Type Insights

Plastic copolymers are projected to lead the market, capturing around 55% of the revenue share in 2026, supported by their unmatched versatility, lightweight characteristics, and ability to integrate seamlessly with nanotechnology-enabled barrier enhancements. Their dominance is especially evident in flexible micro packaging formats such as films and pouches, where high oxygen and moisture resistance is essential without adding bulk. Plastic copolymers support micro-perforation, nano-coatings, and functional additives that enable shelf-life extension and contamination prevention in food and pharmaceutical applications. For example, the use of multilayer plastic copolymer films in unit-dose pharmaceutical sachets, where precision, barrier performance, and regulatory compliance are critical.

The paper and paperboard segment is likely to be the fastest-growing material type, driven by sustainability regulations, brand commitments to fiber-based materials, and consumer preference for recyclable packaging. Advances in micro-scale barrier coatings and functional surface treatments now allow paper-based materials to achieve moisture and grease resistance previously limited to plastics. This evolution enables their use in micro packaging formats without compromising recyclability or circular economy alignment. For example, coated paperboard is used in portion-controlled food cartons that incorporate thin barrier layers while remaining recyclable within existing paper streams.

Regional Insights

North America Micro Packaging Market Trends

North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by strong demand intensifying for high-performance, compliance-driven solutions across pharmaceuticals, food & beverage, and advanced electronics. Sustainability has also emerged as a key trend, with brands seeking lightweight, recyclable, or fiber-based micro packaging formats to meet state-level plastic reduction mandates and corporate ESG commitments. For example, Amcor’s development of advanced barrier films and recyclable micro laminate structures illustrates how converters leverage material science innovation to balance high protection with recyclability.

The acceleration of automation and digital manufacturing within North America’s micro packaging ecosystem. As converters and material producers invest in robotics, AI-enabled process controls, and inline inspection systems, production lines achieve higher precision, faster throughput, and better quality assurance for micro-engineered packaging formats. This is especially critical for regulated sectors such as biologics and micro-dose pharmaceuticals, where tight tolerances and contamination control are nonnegotiable.

Europe Micro Packaging Market Trends

Europe is likely to be a significant market for micro packaging in 2026, due to sustainability regulations and circular economy mandates that favor recyclable, fiber-based, and low-impact materials. The emphasis on environmental performance is also prompting investments in life cycle assessments (LCAs) and sustainable material labeling that resonate with eco-conscious consumers. For example, Mondi Group’s development of recyclable high-barrier paper packaging for fresh foods, which demonstrates how European players are aligning micro packaging performance with stringent sustainability goals.

Innovation in smart, active, and traceable packaging technologies is accelerating the adoption of micro packaging across regulated segments such as pharmaceuticals and nutraceuticals. European regulators are emphasizing product safety, tamper evidence, and supply-chain transparency, prompting brand owners to integrate features such as QR-based traceability, freshness indicators, and anti-counterfeit seals within micro formats. The demand for precision dosing and contamination protection in biologics and high-value therapeutics drives investments in advanced forming, micro-coating, and inspection systems.

Asia Pacific Micro Packaging Market Trends

The Asia Pacific region is likely to be the fastest-growing region in the micro packaging market in 2026, driven by rapid industrial growth, expanding manufacturing capacity, and cost-efficiency advantages that appeal to brands and regional converters alike. Regional governments are offering incentives and subsidies for packaging modernization, and supply-chain integration across Asia Pacific reduces lead times and logistics costs for multinational companies. For example, Uflex Ltd.’s expansion of its advanced film and flexible micro packaging portfolio in India and Southeast Asia, where innovations in barrier films and sustainable laminates are helping brand owners meet performance and regulatory expectations.

Sustainability and regulatory convergence with norms are shaping market adoption in the region. While environmental policies vary widely across Asia Pacific, there is a clear push toward recyclable materials, reduced plastic waste, and compliance with international food safety standards, particularly in export-oriented economies. Paper-based and bio-derived materials are gaining attention in micro packaging applications as converters respond to both consumer preferences and impending regulatory frameworks aimed at reducing single-use plastic footprints.

Competitive Landscape

The global micro packaging market exhibits a moderately fragmented structure, driven by the coexistence of large multinational converters and numerous regional players investing in advanced materials, smart functionalities, and sustainable formats. Investments in nanotechnology-enabled barrier films, recyclable structures, and smart packaging solutions are central to product roadmaps, while automation and digital manufacturing improve quality and cost competitiveness.

With key leaders including Amcor plc, Sealed Air Corporation, Berry Inc., and Avery Dennison, the competitive terrain reflects both historical strength and innovation emphasis across pharmaceutical, food & beverage, and specialty industrial segments. These players compete through strategic initiatives focusing on technological innovation, sustainability, and operational scale to differentiate offerings and capture market share.

Key Industry Developments:

- In January 2026, Agrileaf announced the launch of biodegradable, sturdy, and microwave-safe food delivery boxes made from naturally fallen arecanut (areca palm) leaves, reinforcing the shift away from single-use plastic packaging. The new packaging solutions are designed to meet the growing demand from food delivery platforms, restaurants, and cloud kitchens for sustainable alternatives that do not compromise on strength, heat resistance, or food safety. Manufactured using agricultural waste without chemical additives, the boxes are fully compostable and align with tightening plastic regulations and sustainability mandates across India and export markets.

- In October 2025, Amcor introduced its AmSecure™ recyclable thermoformed trays and rollstock as part of its HealthCare portfolio, strengthening its focus on sustainable pharmaceutical packaging solutions. Designed for pharma applications, AmSecure is made from amorphous PET (APET) and delivers comparable mechanical strength, clarity, durability, and sterilization performance to traditional PETG, while offering improved dimensional stability and lower cost. The innovation provides a more environmentally sustainable alternative aligned with recyclability goals, earning Design for Recyclability Recognition from the Association of Plastic Recyclers (APR).

- In September 2025, Fujifilm Corporation announced the launch of an advanced packaging CMP slurry designed to support hybrid bonding technology, a critical enabler for next-generation AI semiconductor performance. The newly introduced CMP slurry has been adopted by a major semiconductor device manufacturer to achieve the ultra-high planarization accuracy required for bonding multiple chips into a single package. Optimized from Fujifilm’s front-end copper interconnect CMP slurry, the solution delivers high polishing efficiency and precision across complex surfaces where copper and oxide films coexist.

Companies Covered in Micro Packaging Market

- 3M

- Amcor

- Amerplast

- Avery Dennison

- Berry Global

- Bollore

- CCL Industries

- Cosmo Films

- Coveris Holdings

- Dai Nippon Printing

- Dunmore

- DuPont

- Graham Packaging

- International Paper

- Mondi Group

- MTD Micro Molding

- PPC Flex

- Sealed Air

Frequently Asked Questions

The global micro packaging market is projected to reach US$9.6 billion in 2026.

Growing demand for high-barrier, precision packaging in pharmaceuticals and food is supported by advances in nanotechnology, sustainability regulations, and smart packaging adoption.

The micro packaging market is expected to grow at a CAGR of 16.0% from 2026 to 2033.

Key market opportunities in micro packaging lie in smart and active packaging integration, bio-based and recyclable material development, and precision formats for biologics, e-commerce, and single-serve applications.

3M, Amcor, Amerplast, Avery Dennison, Berry Global, Bollore, CCL Industries, Cosmo Films, and Coveris Holdings are the leading players.