- Executive Summary

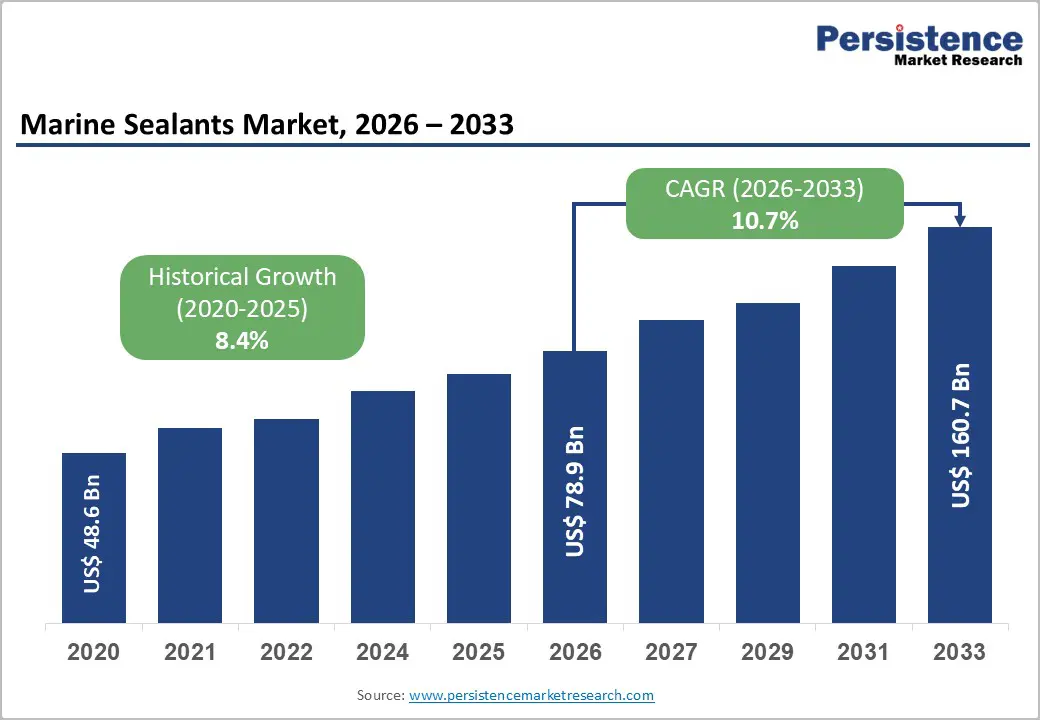

- Global Marine Sealants Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Marine Industry Overview

- Global Chemical Industry Overview

- Forecast Factors – Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 – 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Marine Sealants Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

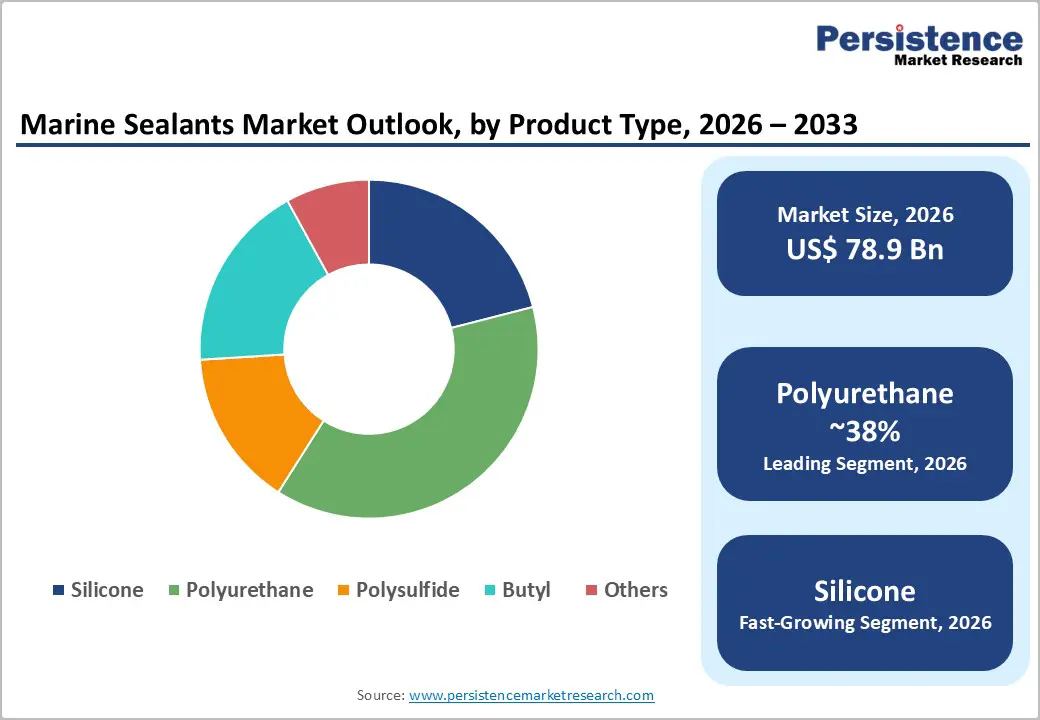

- Global Marine Sealants Market Outlook: By Product Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by By Product Type, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by By Product Type, 2026-2033

- Silicone

- Polyurethane

- Polysulfide

- Butyl

- Others

- Market Attractiveness Analysis: By Product Type

- Global Marine Sealants Market Outlook: By Application

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by By Application, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by By Application, 2026-2033

- Deck Sealing

- Hull Sealing

- Window and Door Sealing

- Others

- Market Attractiveness Analysis: By Application

- Global Marine Sealants Market Outlook: By End User

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by By End User, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by By End User, 2026-2033

- Commercial Vessels

- Recreational Boats

- Others

- Market Attractiveness Analysis: By End User

- Global Marine Sealants Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Marine Sealants Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by By Product Type, 2026-2033

- Silicone

- Polyurethane

- Polysulfide

- Butyl

- Others

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by By Application, 2026-2033

- Deck Sealing

- Hull Sealing

- Window and Door Sealing

- Others

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by By End User, 2026-2033

- Commercial Vessels

- Recreational Boats

- Others

- Europe Marine Sealants Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by By Product Type, 2026-2033

- Silicone

- Polyurethane

- Polysulfide

- Butyl

- Others

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by By Application, 2026-2033

- Deck Sealing

- Hull Sealing

- Window and Door Sealing

- Others

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by By End User, 2026-2033

- Commercial Vessels

- Recreational Boats

- Others

- East Asia Marine Sealants Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by By Product Type, 2026-2033

- Silicone

- Polyurethane

- Polysulfide

- Butyl

- Others

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by By Application, 2026-2033

- Deck Sealing

- Hull Sealing

- Window and Door Sealing

- Others

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by By End User, 2026-2033

- Commercial Vessels

- Recreational Boats

- Others

- South Asia & Oceania Marine Sealants Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by By Product Type, 2026-2033

- Silicone

- Polyurethane

- Polysulfide

- Butyl

- Others

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by By Application, 2026-2033

- Deck Sealing

- Hull Sealing

- Window and Door Sealing

- Others

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by By End User, 2026-2033

- Commercial Vessels

- Recreational Boats

- Others

- Latin America Marine Sealants Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by By Product Type, 2026-2033

- Silicone

- Polyurethane

- Polysulfide

- Butyl

- Others

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by By Application, 2026-2033

- Deck Sealing

- Hull Sealing

- Window and Door Sealing

- Others

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by By End User, 2026-2033

- Commercial Vessels

- Recreational Boats

- Others

- Middle East & Africa Marine Sealants Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by By Product Type, 2026-2033

- Silicone

- Polyurethane

- Polysulfide

- Butyl

- Others

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by By Application, 2026-2033

- Deck Sealing

- Hull Sealing

- Window and Door Sealing

- Others

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by By End User, 2026-2033

- Commercial Vessels

- Recreational Boats

- Others

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Dow Corning Corporation

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Henkel AG and Company, KGaA

- The 3M Company

- Bostik S.A.

- Sika AG

- SABA

- Adshead Ratcliffe and Co Ltd.

- Wacker Chemie AG

- Momentive Performance Materials

- Evonik Industries AG

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Trelleborg AB

- ITW Performance Polymers

- Others

- Dow Corning Corporation

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Inks, Coatings, Adhesives & Sealants (ICAS)

- Marine Sealants Market

Marine Sealants Market Size, Share, and Growth Forecast 2026 - 2033

Marine Sealants Market by Product Type (Silicone, Polyurethane, Polysulfide, Butyl, Others), Application (Deck Sealing, Hull Sealing, Window and Door Sealing, Others), End-user (Commercial Vessels, Recreational Boats, Others), and Regional Analysis, 2026 - 2033

Marine Sealants Market Size and Trend Analysis

The global Marine Sealants market size is likely to be valued at US$ 78.9 billion in 2026 and is expected to reach US$ 160.7 billion by 2033, growing at a CAGR of 10.7% during the forecast period from 2026 to 2033.

The market's exceptionally robust and accelerating growth trajectory is anchored in the convergence of rapid global shipbuilding activity expansion, escalating vessel maintenance and refit expenditure driven by an aging global commercial fleet, and tightening international maritime environmental regulations that mandate higher-performance sealant and coating systems across vessel construction and refurbishment programs.

Key Industry Highlights:

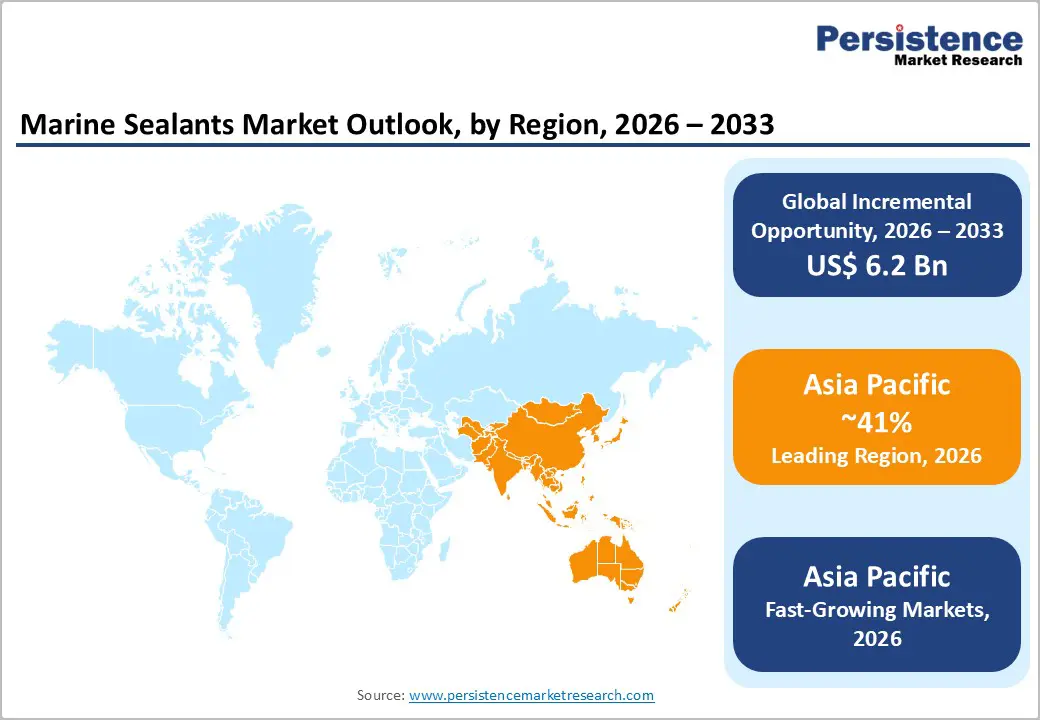

- Leading Region: Asia Pacific leads the global Marine Sealants market with 41% share, supported by South Korea’s strong shipbuilding orders, China’s large CSSC shipyard output, and the region’s dominant position in global commercial vessel construction.

- Fastest-Growing Region: Asia Pacific is also the fastest-growing region with a 12.3% CAGR, driven by China’s recreational boating growth, India’s Sagarmala shipbuilding expansion, and increasing ship repair and maintenance activity across Southeast Asia.

- Leading Segment: Polyurethane leads the product type segment with about 38% share in 2026, supported by strong brand presence from 3M and Sika, and its superior flexibility, adhesion, and resistance to seawater exposure.

- Fastest-Growing Segment: Silicone sealants represent the fastest-growing segment with a CAGR of 13.4%, driven by strong demand in deck and superstructure sealing applications due to their high-temperature resistance, UV durability, and compatibility with painted surfaces.

- Key Opportunity: IMO decarbonization targets and EU maritime emission regulations are encouraging shipowners to upgrade hull sealing systems, creating strong opportunities for advanced marine sealants that improve vessel efficiency, durability, and environmental compliance.

| Key Insights | Details |

|---|---|

|

Marine Sealants Market Size (2026E) |

US$ 78.9 Billion |

|

Market Value Forecast (2033F) |

US$ 160.7 Billion |

|

Projected Growth CAGR (2026–2033) |

10.7% |

|

Historical Market Growth (2020–2025) |

8.4% |

Market Dynamics

Drivers - Global Shipbuilding Industry Expansion and Commercial Fleet Renewal Driving Large-Volume Marine Sealant Demand

The global shipbuilding industry continues to operate at high activity levels, mainly supported by commercial fleet renewal programs aimed at replacing aging vessels, expanding global container shipping capacity, increasing LNG carrier fleets, and growing demand for offshore energy infrastructure vessels. These developments are generating consistent and large-scale demand for marine sealants used in hull construction, deck sealing, superstructure jointing, and below-waterline penetration sealing applications. Industry organizations such as the Korean Register of Shipping and Lloyd's Register have reported a sustained global orderbook build-up. According to the Korean Shipbuilders' and Offshore Plant Industry Association (KOSHIPA), South Korean shipyards received new orders totaling 25.7 million compensated gross tons (CGT) in 2023, representing the highest order intake in more than a decade.

China State Shipbuilding Corporation (CSSC) is executing large vessel construction programs covering container ships, bulk carriers, tankers, and naval vessels. Each of these vessels requires certified marine sealant systems supplied by companies such as Sika AG, Henkel AG, and 3M to ensure watertight structural integrity. In addition, the IMO’s Common Structural Rules (CSR) for bulk carriers and oil tankers specify performance standards for sealant systems used in ballast tanks and void spaces, further driving marine sealant procurement in new ship construction projects worldwide.

IMO Environmental Regulations and Green Shipping Initiatives Accelerating Transition to High-Performance Sealant Systems

The International Maritime Organization is strengthening its environmental regulations, which is increasing demand for advanced marine sealant technologies. The IMO’s 2023 GHG Strategy aims to reduce shipping carbon intensity by at least 40% by 2030 and achieve net-zero greenhouse gas emissions by around 2050. These targets are encouraging the adoption of high-performance sealants that improve vessel efficiency, durability, and long-term operational performance. Modern polyurethane and polysulfide sealants provide strong adhesion, long-term flexibility, and smoother hull-to-water joints, which help reduce hydrodynamic drag and improve fuel efficiency.

This is particularly important for shipowners facing compliance pressure from the IMO’s Carbon Intensity Indicator (CII) requirements. Additionally, the European Union’s Fit for 55 legislative package, including the FuelEU Maritime Regulation and the extension of the EU Emissions Trading System (ETS) to shipping from 2024 is pushing European shipowners to upgrade vessel efficiency. As a result, companies such as Sika AG and Henkel are actively developing low-VOC and solvent-free marine sealant formulations that meet environmental compliance requirements while maintaining high performance standards.

Restraints - Volatile Raw Material Prices for Silicone and Polyurethane Precursors Impacting Marine Sealant Manufacturer Margins

The marine sealants industry continues to face pressure from volatile raw material prices, particularly for silicone intermediates such as methylchlorosilanes and polydimethylsiloxane, as well as polyols and isocyanates used in polyurethane formulations. Polysulfide polymer feedstocks also contribute to cost variability in sealant manufacturing. These materials are largely derived from petrochemical processes and require energy-intensive production, making them highly sensitive to fluctuations in global energy prices and feedstock availability. The International Energy Agency has reported significant energy price volatility between 2022 and 2024 due to geopolitical tensions and ongoing energy transition challenges.

Such fluctuations directly increase production costs for sealant manufacturers. Smaller and mid-sized marine sealant companies are particularly vulnerable to these changes because they often lack long-term supplier contracts or backward integration into raw material production. As a result, rising input costs can compress operating margins and reduce pricing flexibility. This situation makes it difficult for smaller producers to compete with large multinational companies such as Dow and Wacker Chemie AG, which benefit from stronger supply chain control and scale advantages.

Stringent Environmental and Health Regulations on Solvent-Based and Isocyanate-Containing Sealant Formulations

Increasingly strict environmental and occupational safety regulations are creating challenges for marine sealant manufacturers worldwide. Governments and regulatory bodies are introducing tighter controls on solvent-based sealant formulations due to concerns about volatile organic compound emissions and workplace health risks. For example, the European Union’s REACH regulation limits the use of hazardous chemicals, while the U.S. Environmental Protection Agency’s Architectural and Industrial Maintenance Coatings Rule sets restrictions on VOC emissions. In addition, occupational safety regulations are becoming stricter regarding exposure to isocyanates used in polyurethane sealant production.

The European Chemicals Agency has also expanded its list of Substances of Very High Concern, which includes several chemicals historically used in marine adhesive and sealant formulations. As a result, manufacturers must reformulate products, secure regulatory authorizations, or develop alternative chemistries that meet both regulatory standards and performance requirements. These compliance efforts require significant research, testing, and certification investments, placing a greater financial burden on smaller marine sealant manufacturers compared with large multinational companies that already maintain dedicated regulatory and compliance teams.

Opportunity - Commercial Vessel Retrofit and Maintenance, Repair, and Overhaul Market Generating Recurring High-Volume Demand

The global commercial shipping fleet requires continuous maintenance, repair, and overhaul activities, which creates recurring demand for marine sealants. Most commercial vessels must undergo scheduled dry-docking approximately every five years as mandated by the International Maritime Organization and classification societies such as Lloyd’s Register, Bureau Veritas, DNV, and the American Bureau of Shipping. During these maintenance cycles, marine sealants are replaced or reapplied across critical areas including deck fittings, hull penetrations, cargo hatch covers, superstructure windows, and accommodation joints.

According to the UNCTAD Review of Maritime Transport 2023, the global commercial fleet consists of more than 105,000 vessels with a combined capacity of approximately 2.2 billion deadweight tons. A large share of this fleet is more than 15 years old, which increases the need for regular maintenance and sealant replacement to maintain safety standards and classification certifications. Major dry-dock facilities in Singapore, South Korea, and China process thousands of vessel maintenance cycles each year. Companies such as PPG Industries and The Sherwin-Williams Company are well positioned to benefit from this stable and recurring demand.

Recreational Boating Industry Expansion and Premium Boat Manufacturing Growth Creating High-Value Sealant Application Segments

The global recreational boating industry is experiencing steady expansion, driven by rising consumer spending, lifestyle changes, and increased interest in marine tourism and outdoor leisure activities. Markets in North America, Western Europe, Australia, and emerging Asia Pacific economies are witnessing strong growth in boat ownership and marina infrastructure development. According to the National Marine Manufacturers Association, recreational boating in the United States generated over US$ 51 billion in economic impact in 2023.

Each newly manufactured recreational vessel requires marine sealant applications in multiple areas, including deck-to-hull joints, hardware bedding, portlight frames, through-hull fittings, and interior wood structures. Compared with commercial vessels, recreational boats often demand higher aesthetic and performance standards, allowing manufacturers to command premium prices for sealant products. Well-known marine sealant products such as 3M’s Marine Adhesive/Sealant 5200 and 4200 series and ITW Performance Polymers’ Devcon marine sealant range are widely used in this segment. Similarly, Bostik S.A. offers specialized bonding and sealing solutions targeted at premium recreational boat manufacturing and refurbishment applications.

Category-wise Analysis

By Product Type Insights

Polyurethane marine sealants lead the global Marine Sealants market by product type, accounting for approximately 38% of total segment revenue in 2026. This strong position reflects polyurethane’s balanced combination of permanent flexibility, excellent adhesion to multiple marine substrates such as fiberglass reinforced plastic, aluminum, steel, teak, and GRP laminates, and strong resistance to seawater immersion, UV exposure, and temperature fluctuations. These qualities make polyurethane the most versatile and widely used sealant chemistry across both commercial and recreational marine applications.

Well-known polyurethane systems such as 3M’s Marine Adhesive/Sealant 5200 and 4200FC illustrate the product’s leadership in the recreational boating segment, while Sika AG’s Sikaflex marine polyurethane range and Henkel’s LOCTITE polyurethane marine sealants are widely used in global shipbuilding and repair activities. Silicone sealants hold the second-largest share at around 28%, valued for their high-temperature resistance, UV stability, and paint compatibility in deck and superstructure applications. Meanwhile, polysulfide sealants maintain strong demand in below-waterline uses, fuel tanks, and portlight bedding, where their superior resistance to fuels and chemicals provides performance advantages.

By Application Insights

Hull sealing is the leading application segment in the global marine sealants market, accounting for approximately 42% of total application revenue in 2026. This leadership reflects the critical role hull sealing plays in maintaining vessel waterproofing, structural integrity, and operational safety across all marine vessels. Certified sealant systems are mandatory for below-waterline hull penetrations, keel-to-hull joints, appendage connections, and corrosion protection under International Maritime Organization and classification society standards. Hull sealing operates in some of the most demanding marine conditions, including continuous saltwater exposure, biofouling, interactions with cathodic protection systems, and dynamic hull movement. As a result, shipbuilders and repair yards rely on premium sealant formulations that offer long service life, strong adhesion, and reliable performance in permanently submerged environments.

Polysulfide and polyurethane hull sealants from companies such as PPG Industries, Sika AG, and Trelleborg AB are widely used in commercial vessels. Deck sealing represents the second-largest application segment, covering teak deck caulking, hardware bedding, non-skid panel sealing, and deck penetration waterproofing, with companies like Bostik S.A. and ITW Performance Polymers serving this high-volume application market.

By End-user Insights

The Commercial Vessels segment leads the global Marine Sealants market by end user, accounting for approximately 55% of total segment revenue in 2026. This leadership is supported by the global commercial shipping fleet of more than 105,000 vessels, as reported by UNCTAD, and the mandatory five-year dry-docking cycle required by classification societies such as Lloyd’s Register, DNV, and ABS. Commercial vessels require large volumes of sealants across multiple applications including hull construction, ballast tank sealing, cargo hatch waterproofing, engine room penetrations, and accommodation module joints.

Vessel types such as container ships, bulk carriers, oil and chemical tankers, and LNG carriers often require thousands of individual sealant joints during both new construction and scheduled maintenance cycles. Because sealant failure can directly affect vessel safety and seaworthiness, shipowners and shipyards typically specify high-performance products. Recreational boats represent the second-largest segment with about 32% revenue share. Growth in this segment is supported by the US$51 billion U.S. recreational boating economy and expanding leisure marine markets in Europe and Asia Pacific, where premium aesthetics and performance requirements increase average sealant prices.

Regional Insights

North America Marine Sealants Market Trends

North America remains a leading regional market for marine sealants, primarily driven by the United States, which has the world’s largest recreational boating economy. According to the National Marine Manufacturers Association, the U.S. recreational boating sector generates more than US$51 billion in annual economic impact and includes approximately 12 million registered boats nationwide. Strict vessel safety inspections conducted by the U.S. Coast Guard and classification requirements from the American Bureau of Shipping create strong demand for high-performance marine sealants in both commercial and recreational vessels.

Well-known products such as 3M’s Marine Adhesive/Sealant 5200 and ITW Performance Polymers’ Devcon marine product lines have strong brand recognition across the U.S. marine retail network, including West Marine stores and major distributors. Additionally, the Gulf of Mexico offshore energy industry, including oil and gas platforms and offshore wind installations, generates steady sealant demand. The U.S. Navy’s fleet maintenance programs, managed by Naval Sea Systems Command, also represent an important government procurement channel for manufacturers meeting strict military sealant performance standards.

Europe Marine Sealants Market Trends

Europe represents a technologically advanced and commercially important regional market for marine sealants, supported by its strong shipbuilding sector and globally recognized luxury yacht manufacturing industry. Major shipbuilding hubs in Germany, Italy, and Finland produce technically sophisticated vessels that require high-performance sealing systems. Europe is also home to leading yacht manufacturers such as Ferretti and Azimut-Benetti in Italy, Bénéteau Group in France, and Damen Shipyards in the Netherlands. Germany’s maritime sector, including shipyards such as Meyer Werft and Flensburger Schiffbau-Gesellschaft, generates consistent demand for premium sealants, especially in the cruise ship segment where thousands of cabin portlights, deck penetrations, and balcony installations require reliable sealing solutions.

European suppliers such as Sika AG and Henkel AG & Co. KGaA are among the region’s dominant sealant manufacturers. In addition, the European Union’s environmental initiatives, including the Fit for 55 package and FuelEU Maritime regulations, encourage shipowners to adopt more efficient vessel technologies, including improved hull sealing systems. The United Kingdom’s active sailing community and boating maintenance sector also support steady demand for high-quality marine sealants.

Asia Pacific Marine Sealants Market Trends

Asia Pacific is the largest and fastest-growing regional market for marine sealants, supported by the region’s dominance in global shipbuilding and increasing recreational boating activity. China and South Korea are the world’s two largest shipbuilding nations, while Japan continues to produce technologically advanced commercial and specialty vessels. South Korean shipyards such as HD Hyundai Heavy Industries, Samsung Heavy Industries, and Hanwha Ocean maintain one of the largest global shipbuilding order books, with KOSHIPA reporting over 25.7 million compensated gross tons (CGT) of new orders in 2023.

Each vessel constructed requires large volumes of sealants for hull, deck, and structural sealing applications. China’s state-owned CSSC group operates multiple large shipyards across Shanghai, Guangzhou, and Wuhan, producing thousands of vessels annually and generating the highest global demand for marine sealants at the shipyard level. In addition, China’s recreational boating market is expanding as coastal tourism develops in regions such as Hainan and Qingdao. India’s growing shipbuilding sector, supported by the Sagarmala maritime development program and naval modernization projects, is also increasing demand for marine sealant products.

Competitive Landscape

The global marine sealants market is moderately consolidated, with a group of major specialty chemical and adhesive manufacturers holding strong positions worldwide. Companies such as Sika AG, Henkel AG & Co. KGaA, 3M, Dow, and PPG Industries maintain competitive advantages through broad product portfolios, global distribution networks, and long-term partnerships with shipbuilders and boat manufacturers. Key factors that differentiate leading suppliers include ISO 9001-certified manufacturing processes, approvals from classification societies such as Lloyd’s Register, DNV, ABS, and Bureau Veritas, and advanced formulation technologies designed to meet strict marine performance standards.

Many manufacturers are also investing in low-VOC and environmentally friendly sealant formulations to align with global sustainability regulations. Competitive strategies increasingly include integrated coating and sealant product systems, strong technical service support for shipyards, and expanded e-commerce distribution for recreational marine markets. Companies such as Bostik S.A. and Evonik Industries AG are further investing in next-generation reactive hot-melt and bio-based adhesive technologies aimed at high-value yacht and premium marine construction segments.

Key Developments:

- In February 2025: Sika AG expanded its Sikafle Marine Pro polyurethane sealant portfolio to support sustainable shipbuilding and regulatory compliance in Europe. The range features low-VOC formulations, strong adhesion to marine substrates, and durability for shipbuilding and repair applications aligned with emerging maritime environmental standards. Source: Sika Marine Solutions

- In October 2024: Henkel AG & Co. KGaA strengthened its marine presence by expanding the LOCTITE sealant distribution network across Southeast Asia, partnering with ship repair yards in Singapore, Vietnam, and the Philippines to serve growing dry-dock maintenance demand from the expanding Asia Pacific commercial fleet.

- In March 2024: 3M launched an upgraded Marine Adhesive/Sealant 5200 Fast Cure formulation designed to reduce tack-free time by about 50%. The innovation helps boat manufacturers accelerate assembly processes and improve production efficiency amid rising recreational boat demand in North America and Europe.

Companies Covered in Marine Sealants Market

- Dow Corning Corporation

- Henkel AG & Co. KGaA

- The 3M Company

- Bostik S.A.

- Sika AG

- SABA

- Adshead Ratcliffe and Co. Ltd.

- Wacker Chemie AG

- Momentive Performance Materials

- Evonik Industries AG

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Trelleborg AB

- ITW Performance Polymers

- Chugoku Marine Paints Ltd.

- Jotun A/S

- Master Bond Inc.

Frequently Asked Questions

The global Marine Sealants market is valued at US$78.9 billion in 2026 and projected to reach US$160.7 billion by 2033, registering a 10.7% CAGR, supported by shipbuilding growth and rising fleet maintenance demand.

Key drivers include expanding global shipbuilding activity, a growing commercial fleet requiring regular dry-docking maintenance, and stricter environmental regulations encouraging shipowners to adopt advanced sealant systems for improved vessel durability and efficiency.

Polyurethane marine sealants lead the market with about 38% revenue share in 2026, supported by strong adhesion, long-term seawater resistance, and flexibility, making them widely used across commercial vessels and recreational boat sealing applications.

Asia Pacific leads the global Marine Sealants market due to strong shipbuilding activity in China, South Korea, and Japan, where large commercial vessel construction programs generate high demand for marine sealants.

A major opportunity lies in vessel retrofit programs driven by stricter maritime emission regulations, encouraging shipowners to upgrade hull sealing systems that enhance fuel efficiency, durability, and compliance with global environmental standards.

Major companies include Sika AG, Henkel AG & Co. KGaA, 3M, PPG Industries, Dow, Bostik, Wacker Chemie, Momentive Performance Materials, Trelleborg, Evonik, Sherwin-Williams, ITW Performance Polymers, and Jotun.