- Testing, Inspection, & Certification

- Manned Security Services Market

Manned Security Services Market Size, Share, and Growth Forecast, 2026 - 2033

Manned Security Services Market by Product Type (Service, Equipment, Others), End-user (Industrial Buildings/Facilities, Residential Buildings/Complexes, Others), Service Model, and Regional Analysis for 2026 - 2033

Manned Security Services Market Size and Trends Analysis

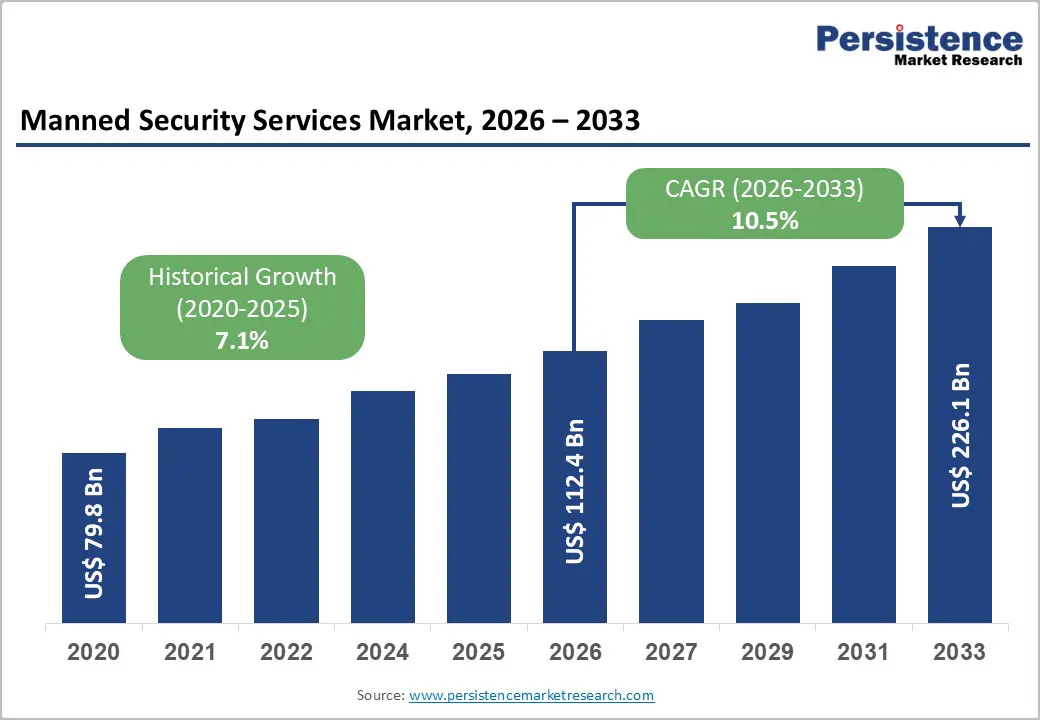

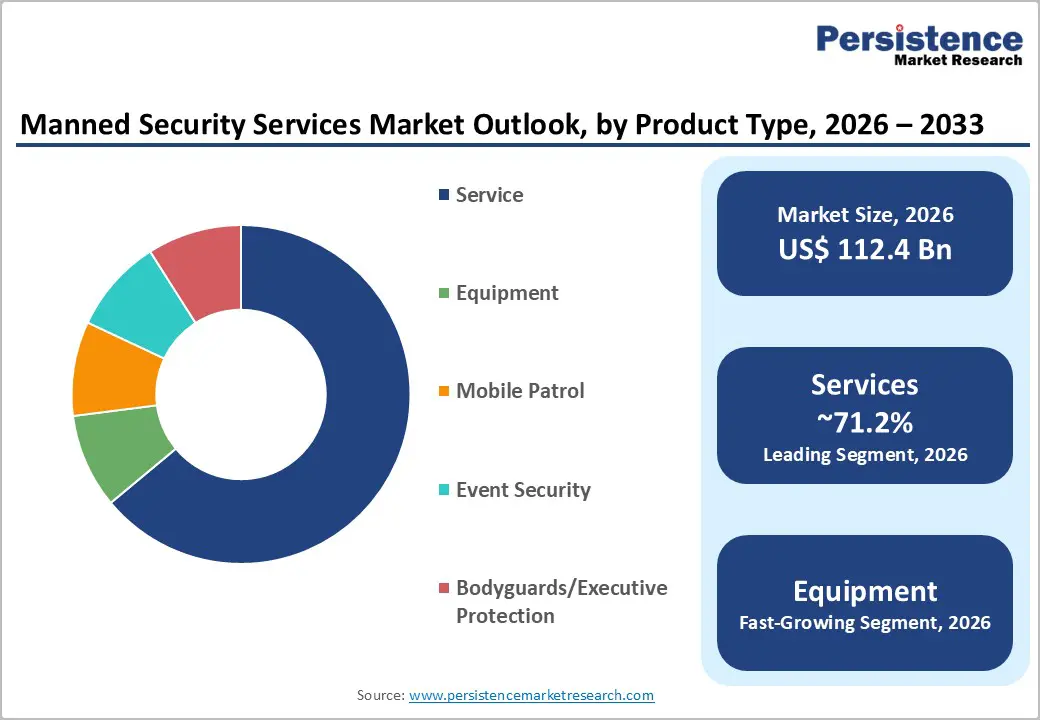

The global manned security services market size is likely to be valued at US$112.4 billion in 2026 and is expected to reach US$226.1 billion by 2033, growing at a CAGR of 10.5% between 2026 and 2033.

Urban expansion continues to drive the demand for physical security presence across commercial, industrial, and residential environments. Stricter regulatory frameworks in major economies are reinforcing the need for licensed, trained personnel. The market is also evolving through technology augmentation, where human security is complemented by surveillance systems, analytics, and remote monitoring, enhancing both efficiency and service value.

Key Industry Highlights:

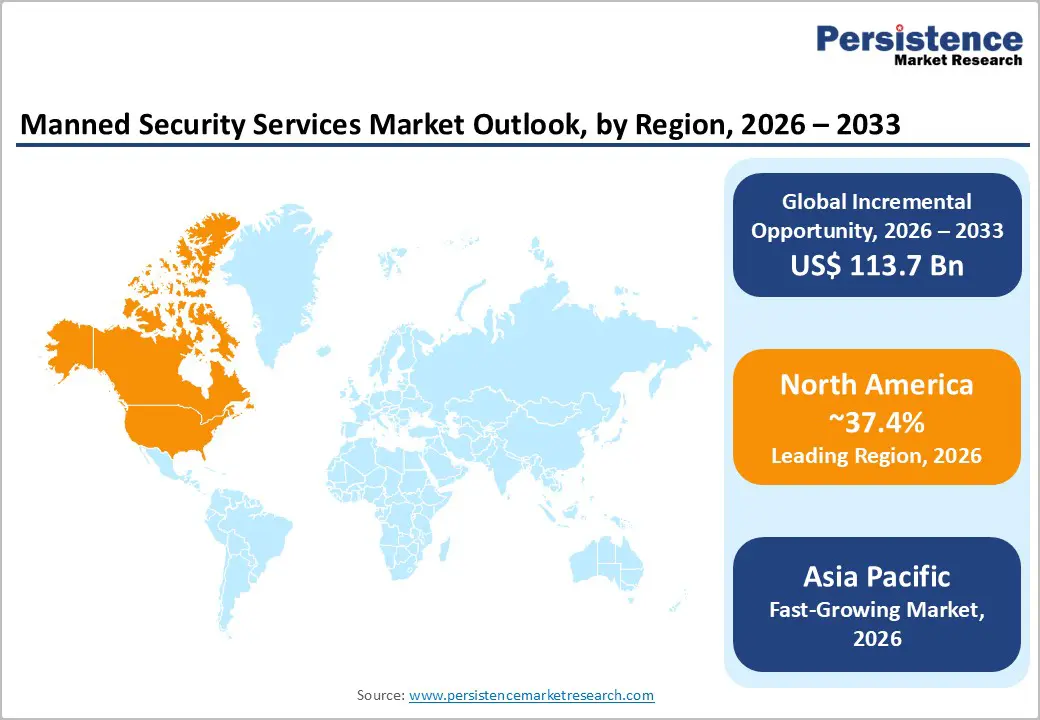

- Leading Region: North America is projected to account for approximately 37.4% of the market share, supported by strong demand across the corporate, industrial, and public infrastructure sectors, as well as high adoption of integrated security solutions.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, driven by rapid urbanization, infrastructure development, and increasing formalization of the private security sector.

- Investment Plans: Over 40% of large security service providers are prioritizing investments in AI-enabled surveillance, remote monitoring, and hybrid security models to enhance operational efficiency and transition to subscription-based revenue streams.

- Dominant Product Type: Services are anticipated to hold approximately 71.2% market share, driven by the continued reliance on human presence for critical functions such as access control, patrolling, surveillance, and emergency response.

- Leading End-user: Industrial buildings/facilities are estimated to account for approximately 39.7% of the market share, driven by continuous monitoring requirements, high-value assets, and the expansion of manufacturing and logistics infrastructure.

| Key Insights | Details |

|---|---|

| Manned Security Services Market Size (2026E) | US$112.4 Bn |

| Market Value Forecast (2033F) | US$226.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 10.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.1% |

DRO Analysis

Driver Analysis - Urbanization and Asset-Density Growth Expanding Demand

Rapid urbanization is significantly increasing the demand for manned security services. The expansion of urban centers has led to a higher concentration of commercial buildings, industrial facilities, residential complexes, and public infrastructure. As population density rises, so does the need for access control, surveillance, and incident response services. High-traffic environments such as transportation hubs, logistics centers, and mixed-use developments require continuous on-site security presence. This trend is particularly strong in the Asia Pacific and emerging economies, where infrastructure development and urban migration are accelerating. The increasing complexity of urban ecosystems is reinforcing the importance of visible human security as a deterrent and response mechanism.

Regulatory Tightening Driving Formal Security Adoption

Governments across the key markets are strengthening regulatory oversight of private security services. Licensing requirements, training standards, and compliance frameworks are becoming more stringent, ensuring higher service quality and accountability. In regions such as Europe and India, security personnel must meet defined certification standards, while operational audits and compliance checks are increasingly common. These regulatory developments are pushing organizations toward professional, licensed security providers, reducing reliance on informal or unregulated services. As a result, established companies with strong compliance capabilities are gaining a competitive advantage and achieving higher contract values.

Technology Integration: Enhancing Service Capabilities

The integration of advanced technologies is expanding the scope and effectiveness of manned security services. While automation and AI-driven surveillance systems are becoming more prevalent, they primarily augment rather than replace human personnel. Security providers are deploying smart screening systems, AI-powered video analytics, and remote monitoring platforms to improve threat detection and response times. This convergence of human expertise and technology enables more proactive security management. Organizations are increasingly adopting hybrid solutions that combine physical guarding with digital tools, resulting in greater service differentiation and improved operational efficiency.

Restraint Analysis - Labor-Intensive Cost Structure Impacting Margins

Manned security services rely heavily on human resources, making labor costs a significant component of operational expenditure. Expenses related to recruitment, training, wages, and retention continue to rise, particularly in developed markets. Compliance requirements further increase costs through mandatory training programs and certification processes. While demand remains strong, service providers often face challenges passing on rising costs to clients amid competitive pricing pressures. This creates margin constraints, especially in large-scale guarding contracts with high pricing sensitivity.

Market Fragmentation and Pricing Pressure

The market remains highly fragmented, with a large number of regional and local players operating alongside global firms. While entry barriers are increasing, they still allow smaller providers to compete in localized markets. This fragmentation leads to intense price competition, particularly in commoditized service segments such as static guarding. Clients frequently prioritize cost efficiency, resulting in competitive bidding environments that limit pricing power. Consequently, service providers must focus on differentiation through quality, technology integration, and specialized services to maintain profitability.

Opportunity Analysis - Hybrid Security Models Creating Premium Service Segments

The adoption of hybrid security solutions represents a major structural growth opportunity within the manned security services market. Organizations are increasingly transitioning from standalone guarding contracts to integrated security ecosystems that combine on-site personnel with remote monitoring, AI-enabled surveillance, data analytics, and risk intelligence platforms. This shift is being driven by the need for real-time situational awareness, faster incident response, and improved threat prediction capabilities. Hybrid solutions are particularly valuable for high-risk and high-value environments such as data centers, corporate headquarters, logistics hubs, airports, and critical infrastructure facilities. For example, large data center operators are deploying manned guards supported by biometric access systems, centralized command centers, and AI-based anomaly-detection tools to minimize breach risk. Similarly, corporate campuses are integrating visitor management systems with guard oversight to streamline access while maintaining security. From a commercial perspective, hybrid models enable service providers to move beyond labor-based pricing toward subscription-based and outcome-driven revenue models.

Expansion in Emerging Markets and Urban Infrastructure Driving Volume Growth

Emerging economies, particularly in the Asia-Pacific region, offer substantial growth opportunities driven by ongoing urbanization, industrialization, and infrastructure expansion. Rapid population growth and migration to urban centers are driving the development of smart cities, industrial corridors, transportation networks, and large-scale residential complexes, all of which require robust security frameworks. For instance, the expansion of manufacturing hubs and logistics parks in countries such as India, Vietnam, and Indonesia is creating sustained demand for perimeter security, access control, and asset protection services. Similarly, the rise of integrated townships and high-rise residential developments is driving the adoption of professional security services, including 24/7 guarding, visitor management, and surveillance. Government initiatives aimed at formalizing the private security sector are further strengthening market potential.

Regulatory frameworks that mandate licensing, training, and operational standards are encouraging the shift from informal security arrangements to organized service providers. This transition is improving service quality while creating opportunities for companies with strong compliance capabilities. In addition, partnerships with real estate developers, infrastructure companies, and government bodies can provide access to long-term contracts and recurring revenue streams.

Category-wise Analysis

Product Type Insights

Service is anticipated to remain the leading product type, accounting for approximately 71.2% of the market share throughout the forecast period. This dominance is driven by the continued reliance on human presence for critical functions such as access control, patrolling, surveillance, and emergency response. Within services, guarding/security guards represent the largest sub-segment due to their extensive deployment across industries such as manufacturing plants, retail chains, healthcare facilities, airports, and logistics hubs. For instance, large industrial parks and shopping malls typically deploy multiple layers of on-site guards to manage entry points, monitor visitor movement, and ensure compliance with safety protocols. The adaptability of trained personnel in handling dynamic situations ensures that human-led services remain indispensable, even as digital solutions evolve.

Equipment is anticipated to be the fastest-growing segment, supported by rapid advancements in surveillance systems, biometric authentication, and AI-based monitoring platforms. Organizations are increasingly investing in integrated security ecosystems that combine CCTV analytics, facial recognition systems, and automated access control to enhance operational efficiency and reduce response time.

For example, corporate campuses and data centers are deploying smart screening systems alongside manned guards to strengthen threat detection. Among service sub-segments, Bodyguards/Executive Protection is expected to grow the fastest, driven by increasing demand from high-net-worth individuals, senior executives, diplomats, and public figures. This segment is also expanding in emerging markets where wealth concentration and geopolitical risks are rising, leading to higher adoption of personalized and intelligence-led protection services.

End-user Insights

Industrial buildings/facilities are anticipated to remain the largest end-user segment, accounting for approximately 39.7% of the market share over the forecast period. These facilities require continuous monitoring due to the presence of high-value assets, critical operations, and large workforces operating in shifts. Security services in this segment typically include perimeter fencing surveillance, gate access management, cargo inspection, and internal patrols. For example, manufacturing plants, oil & gas facilities, and large warehouses deploy multi-layered security systems combining guards, surveillance cameras, and access control checkpoints. The expansion of global supply chains and logistics infrastructure further strengthens demand, as companies prioritize loss prevention and operational continuity.

Residential buildings/complexes are anticipated to be the fastest-growing segment, driven by rapid urbanization, rising disposable incomes, and increasing awareness of personal and community safety. Gated communities, high-rise residential towers, and integrated townships are increasingly adopting professional security services that combine manned guarding with digital access systems and visitor management solutions. For instance, modern residential societies are implementing guard-assisted digital entry systems and 24/7 surveillance to enhance resident safety and convenience.

Regional Insights

North America Manned Security Services Market Trends - AI-Integrated Guarding and Critical Infrastructure Protection Demand

North America is projected to lead the global market, holding approximately 37.4% of the market share. The region’s dominance is driven by strong demand across corporate, industrial, and public sectors, with the U.S. acting as the primary revenue contributor due to its extensive infrastructure base, mature security ecosystem, and high awareness of risk management practices. Key growth drivers include protecting critical infrastructure, increasing investments in data centers, and rising demand for security services across healthcare and educational institutions.

For instance, major operators such as Allied Universal have expanded their integrated service offerings across U.S. campuses, healthcare systems, and enterprise facilities, combining manned guarding with surveillance and risk analytics. Similarly, Securitas AB has strengthened its North American presence through technology-enabled services, particularly in data center security and remote monitoring. Regulatory compliance frameworks across U.S. states ensure high service standards, further encouraging the adoption of licensed and professional providers.

Investment trends indicate strong growth in AI-enabled surveillance and hybrid security solutions. Companies such as GardaWorld have introduced AI-driven monitoring platforms (e.g., ECAM), enhancing real-time threat detection and response capabilities. This shift toward technology integration is enabling service providers to move beyond traditional guarding into risk intelligence and consulting services. The market is expected to maintain steady growth, supported by innovation, large-scale contracts, and increasing demand for integrated, multi-site security solutions.

Europe Manned Security Services Market Trends - Regulated Market with Intelligence-Led Hybrid Security Adoption

Europe represents a mature yet highly regulated market, characterized by strict compliance standards and well-established operational frameworks. Key contributors include the U.K., Germany, France, and Spain, where demand is supported by industrial activity, public infrastructure, and urban security requirements. Regulatory harmonization across the region ensures consistent service quality, particularly in licensing, training, and operational oversight.

Demand is driven by industrial facilities, transportation networks, and government institutions, alongside heightened concerns around terrorism, cyber threats, and organized crime. Companies such as Prosegur have expanded their hybrid security model across European markets, integrating manned guarding with advanced surveillance and data-driven monitoring systems. In the UK, Mitie has strengthened its security division by integrating digital solutions, such as intelligent CCTV and access control systems, into traditional guarding contracts, particularly on public-sector and infrastructure projects. The region is witnessing increased adoption of intelligence-led and hybrid security services, supported by investments in AI-based analytics and centralized monitoring platforms.

For example, Securitas AB has enhanced its European operations through acquisitions and partnerships focused on risk intelligence and electronic security. While overall market growth remains moderate compared to emerging regions, the shift toward high-value, technology-integrated services is creating new revenue streams and improving service margins for leading providers.

Asia Pacific Manned Security Services Market Trends - Urbanization-Driven Demand and Scalable Hybrid Security Expansion

Asia Pacific is expected to be the fastest-growing region, driven by rapid urbanization, industrial expansion, and large-scale infrastructure development. Key markets include China, India, Japan, and Southeast Asia, where demand for security services is increasing across manufacturing, logistics, residential, and commercial sectors. Growth is fueled by the expansion of industrial corridors, smart cities, transportation hubs, and high-density residential developments.

In India, the formalization of the private security sector under regulatory frameworks has encouraged the growth of organized players such as SIS Limited, which has expanded its footprint across facility management and security services. Meanwhile, global firms such as G4S (now part of Allied Universal) continue to strengthen their presence in Asia by securing contracts in airports, embassies, and large infrastructure projects. In Southeast Asia, companies are increasingly deploying integrated security solutions in industrial parks and special economic zones to support foreign investments.

Investment opportunities are particularly strong in industrial security, residential protection, and hybrid monitoring solutions. For example, urban residential complexes in cities such as Mumbai, Singapore, and Jakarta are adopting guard-assisted digital entry systems and 24/7 surveillance models. The region’s large workforce and cost advantages enable scalable operations, making it attractive for both domestic and international providers. Asia Pacific is expected to remain the primary growth engine for the global market, with increasing emphasis on technology integration, regulatory compliance, and service standardization.

Competitive Landscape

The global manned security services market is fragmented yet gradually consolidating, with a mix of global leaders and regional players. Large companies dominate multi-site and high-value contracts, leveraging scale, technology integration, and brand reputation. However, smaller providers continue to operate in localized markets, maintaining competitive diversity. The competitive landscape is characterized by price competition, service differentiation, and increasing adoption of technology-driven solutions.

Recent developments highlight a strong focus on expansion, technology integration, and strategic acquisitions. Companies are investing in AI-driven surveillance platforms and intelligent monitoring systems to enhance service offerings. Mergers and acquisitions are being used to expand geographic presence and strengthen capabilities in emerging markets. Partnerships with technology providers are enabling the integration of advanced analytics and automation into traditional security services. These developments reflect the industry’s shift toward comprehensive, technology-enabled security solutions.

Key strategies include technology integration, geographic expansion, and service diversification. Market leaders are focusing on hybrid security models, compliance excellence, and long-term contracts. Differentiation is achieved through advanced analytics, operational efficiency, and the ability to deliver integrated security solutions across multiple locations.

Key Industry Developments:

- In March 2026, GardaWorld announced a strategic partnership between Crisis24 and Dataminr to advance AI-powered global risk management, enabling organizations to detect threats earlier and enhance real-time decision-making capabilities.

Companies Covered in Manned Security Services Market

- Allied Universal

- Securitas AB

- GardaWorld

- Prosegur

- G4S Limited

- SIS Limited

- Brink’s Incorporated

- ADT Inc.

- Allied Barton Security Services

- ICTS International

- Transguard Group

- TOPSGRUP

- ISS A/S

- Control Risks

- Andrews International

- DynCorp International

Frequently Asked Questions

The global manned security services market is estimated to be valued at US$ 112.4 billion in 2026.

The manned security services market is expected to reach approximately US$ 226.1 billion by 2033.

Key trends include the adoption of hybrid security models, integration of AI-enabled surveillance systems, increasing demand for risk intelligence services, and growing emphasis on technology-driven, subscription-based security solutions.

The service segment, particularly guarding/security guards, remains the leading segment, accounting for the majority share due to its widespread use across industries such as manufacturing, retail, and infrastructure.

The manned security services market is projected to grow at a CAGR of 10.5% from 2026 to 2033.

Some of the major players include Allied Universal, Securitas AB, GardaWorld, Prosegur, and SIS Limited.