- Testing, Inspection, & Certification

- Industrial Radiography Equipment Market

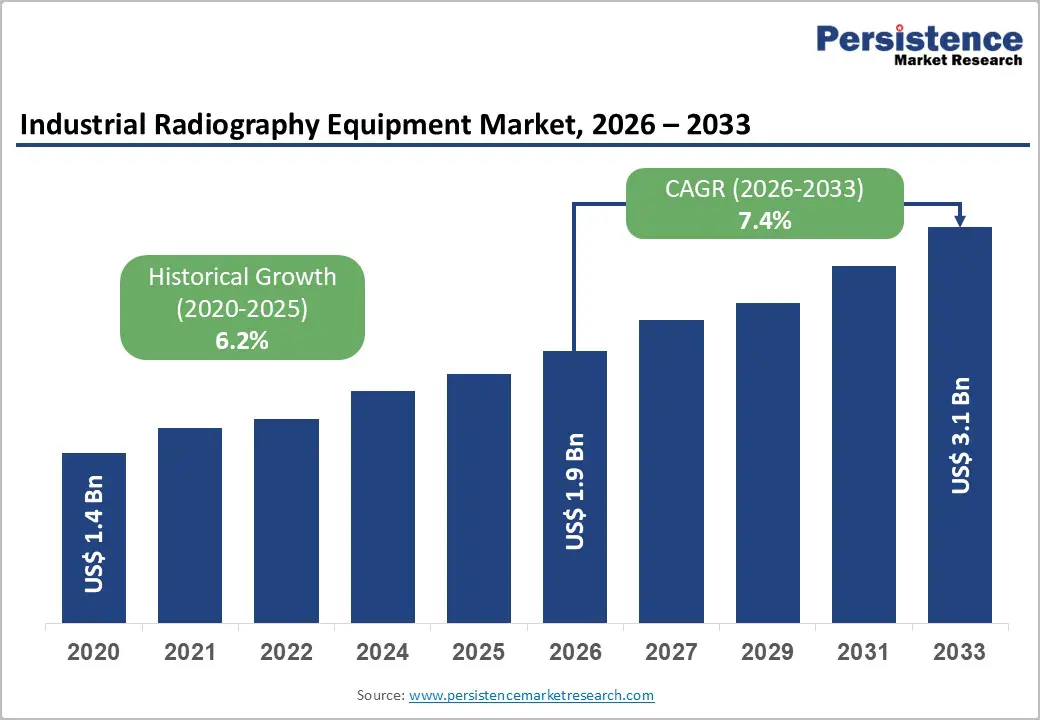

Industrial Radiography Equipment Market Size, Share, and Growth Forecast, 2026 - 2033

Industrial Radiography Equipment Market by Equipment Type (Detection & Imaging Devices, Radiation Sources, Others), End-user Industry (Automotive, Power Generation, Others), Imaging Technique, and Regional Analysis for 2026 - 2033

Industrial Radiography Equipment Market Size and Trends Analysis

The global industrial radiography equipment market size is likely to be valued at US$1.9 billion in 2026 and is expected to reach US$3.1 billion by 2033, growing at a CAGR of 7.4% between 2026 and 2033, driven by rising non-destructive testing (NDT) requirements across critical infrastructure and industrial manufacturing. Increasing regulatory oversight related to radiation safety and quality assurance is reinforcing adoption.

The transition toward digital radiography systems is improving inspection efficiency, while infrastructure development, electrification, and advanced manufacturing are sustaining long-term demand.

Key Industry Highlights:

- Leading Region: North America is projected to account for 35.9% of the market share, supported by advanced industrial infrastructure, strong regulatory frameworks, and early adoption of non-destructive testing technologies.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, driven by rapid industrialization, infrastructure development, and increasing demand from China and India.

- Investment Plans: Significant investments are being directed toward digital radiography systems, automated inspection technologies, and infrastructure expansion projects, particularly in power generation, electric vehicle manufacturing, and large-scale industrial development.

- Dominant Equipment Type: Detection & imaging devices dominate the equipment type segment, with an anticipated market share of 48.7%, driven by their critical role in capturing and analyzing inspection data across industries.

- Leading End-user Industry: The automotive sector leads with an anticipated share of 29.1%, supported by high production volumes and increasing demand for inspection of electric vehicle components and lightweight structures.

DRO Analysis

Driver - Mandatory Quality Assurance across Critical Infrastructure to Expand Radiography Usage

Industrial radiography is a foundational inspection method for ensuring the structural integrity of pipelines, storage tanks, pressure vessels, and welded assemblies. Regulatory bodies across major economies mandate strict inspection standards for safety-critical assets, particularly in sectors such as oil & gas, power generation, and transportation infrastructure. Industrial radiography enables internal defect detection without damaging the material, making it essential for compliance-driven industries.

Radiation safety regulations and licensing requirements have formalized inspection protocols, creating a structured demand environment. This regulatory enforcement leads to recurring expenditure on equipment calibration, certification, and replacement cycles. As infrastructure ages and safety expectations increase, inspection frequency rises, directly supporting sustained demand for radiography equipment and associated services.

Electrification, Grid Expansion, and Industrial Digitization are widening the Inspection Base.

Global electrification trends and rising energy demand are accelerating investments in power generation and grid infrastructure. Emerging economies, particularly in Asia, are experiencing rapid growth in electricity demand, driving expansion in thermal, renewable, and nuclear energy systems. These developments require extensive inspection of turbines, boilers, transmission components, and structural welds. Industrial radiography plays a critical role in validating these assets during both construction and maintenance phases.

Simultaneously, industrial digitization is transforming manufacturing processes, increasing the need for high-precision quality control in automotive, aerospace, and heavy engineering sectors. The combination of infrastructure expansion and advanced manufacturing is significantly broadening the application base for industrial radiography equipment, creating stable and diversified demand across multiple industries.

Restraint - Safety Compliance, Source Handling, and Operational Complexity Increase Total Cost of Ownership

Industrial radiography systems, particularly those using radioactive sources, require strict safety controls, trained personnel, and specialized infrastructure. These requirements increase capital expenditure and operational costs for end users. Equipment handling involves shielding, controlled environments, and regulatory documentation, which can be resource-intensive for small and mid-sized inspection providers. Licensing procedures and compliance audits also introduce administrative complexity.

As a result, organizations may delay upgrading legacy systems, especially when existing film-based setups remain functional. This slows the adoption of advanced digital solutions despite their operational advantages. The high total cost of ownership, combined with regulatory burden, remains a structural constraint that limits faster market penetration in cost-sensitive regions.

Opportunity - Asia Pacific Presents Strong Volume Growth Driven by Industrialization and Infrastructure Expansion

Asia Pacific is emerging as the most dynamic regional market, driven by rapid industrialization, urbanization, and infrastructure development. Countries such as China and India are investing heavily in transportation networks, power generation, and manufacturing capacity. These developments create significant demand for inspection technologies across pipelines, structural components, and industrial machinery. The region’s expanding automotive and energy sectors further underscore the need for reliable NDT solutions.

Increasing localization of manufacturing and supply chains also drives demand for portable and cost-effective radiography systems. Vendors that establish regional service networks and offer scalable solutions are well-positioned to capture growth opportunities in this high-demand environment.

Transition from Film-Based To Digital Radiography Is Unlocking System and Software Upgrades

The shift toward digital radiography represents a major transformation in the industrial inspection landscape. Digital systems offer faster image acquisition, improved defect detection accuracy, and seamless data integration compared to traditional film-based methods. This transition is creating opportunities not only for equipment sales but also for software platforms, analytics tools, and remote inspection services. Organizations are increasingly adopting digital workflows to enhance productivity and reduce inspection turnaround times.

Integration with automation and Industry 4.0 frameworks further increases the value proposition of digital systems. Vendors that provide end-to-end solutions, combining hardware, software, and lifecycle services, are likely to benefit from this ongoing technology upgrade cycle.

Category-wise Analysis

Equipment Type Insights

Detection and imaging devices are anticipated to represent the leading segment, accounting for 48.7% of market share in 2026. This category includes digital detectors, computed radiography (CR) systems, flat-panel detectors, and traditional radiographic film, all of which form the backbone of the imaging process. The dominance of this segment is driven by its essential role in capturing high-resolution inspection data across applications such as weld inspection, casting validation, and structural integrity assessment.

Industries such as automotive, aerospace, and oil & gas rely heavily on advanced imaging systems to detect internal defects in engine blocks, turbine blades, and pipeline welds. For example, automotive manufacturers use flat-panel digital detectors to inspect aluminum castings and EV battery housings for porosity and cracks, while aerospace companies apply high-resolution imaging for composite structures and critical airframe components. Continuous advancements in detector sensitivity, resolution, and processing speed are enhancing defect detection capabilities.

Radiation sources are projected to be the fastest-growing segment, driven by increasing demand for flexible, efficient, and safer inspection systems. The market is gradually shifting from traditional gamma-ray sources (such as Iridium-192 and Cobalt-60) toward X-ray-based solutions, which offer superior operational control, portability, and safety advantages. Modern inspection environments prioritize systems that can be easily deployed in field conditions or integrated into automated production lines.

For instance, portable X-ray generators are increasingly used for on-site pipeline inspections in oil & gas projects, while high-energy X-ray systems are deployed in manufacturing plants for real-time inspection of thick metal components. The ability to power X-ray systems on and off reduces radiation exposure risks and simplifies compliance with safety regulations.

End-user Industry Insights

The automotive sector is expected to lead the market, accounting for 29.1% of the market in 2026, driven by high production volumes and stringent quality assurance requirements. Industrial radiography is extensively used to inspect engine components, castings, welds, and battery systems, ensuring structural integrity and compliance with safety standards. For example, manufacturers use digital radiography to detect internal porosity in aluminum engine blocks and transmission housings, while EV producers rely on X-ray systems to inspect lithium-ion battery packs and weld seams in battery enclosures.

The shift toward electric vehicles is further increasing demand for inspection of lightweight materials and complex assemblies. Automated radiography systems are being integrated directly into production lines, enabling real-time quality control without disrupting throughput. Given the scale of automotive manufacturing, even marginal improvements in inspection efficiency translate into significant cost savings and reduced defect rates, reinforcing the segment’s leadership position.

Power generation is likely to be the fastest-growing end-user segment, supported by rising global energy demand and significant infrastructure investments. This sector requires rigorous inspection of critical components, including turbines, boilers, heat exchangers, and pressure vessels, to ensure operational safety and reliability.

For instance, radiography is widely used in thermal power plants to inspect weld joints in high-pressure steam pipelines, while nuclear facilities rely on advanced imaging to evaluate reactor components and containment structures. In renewable energy, wind turbine components and structural welds in hydroelectric installations also require detailed inspection. Aging infrastructure in developed regions further drives demand for maintenance and periodic inspection services. Industrial radiography plays a key role in preventing equipment failures and minimizing downtime, making it indispensable for energy-sector operations.

Regional Insights

North America Industrial Radiography Equipment Market Trends

North America is projected to lead the market with a 35.9% share in 2026, reflecting its advanced industrial base and early adoption of non-destructive testing (NDT) technologies. The region is projected to grow steadily, supported by strong demand from the aerospace, oil & gas, and automotive industries. Regulatory frameworks governing radiation safety and inspection standards continue to sustain demand, with high compliance requirements driving continuous investment in certified equipment and trained personnel.

U.S. Industrial Radiography Equipment Market Trends

The U.S. is expected to contribute approximately 67.8% of North America’s revenue in 2026, reinforcing its dominance. The U.S. market is characterized by a highly mature inspection ecosystem and strong technological innovation. Companies such as Waygate Technologies and Varex Imaging Corporation are actively advancing digital radiography and computed tomography solutions. A notable development is Baker Hughes' strategic divestment of Waygate Technologies to Hexagon AB in 2026, reflecting increasing consolidation and a focus on precision inspection technologies.

Growing investments in electric vehicle (EV) manufacturing and battery production facilities, particularly in states such as Texas and Michigan, are driving demand for high-resolution X-ray inspection systems to ensure battery safety and performance. Aerospace manufacturers are also integrating automated radiography systems into production lines, thereby improving inspection speed and traceability. These developments highlight a shift toward digital, automated, and analytics-driven inspection workflows, strengthening North America’s leadership position.

Europe Industrial Radiography Equipment Market Trends

Europe represents a significant market, supported by strong regulatory oversight and advanced manufacturing capabilities. The region demonstrates steady growth, driven by industries such as automotive, aerospace, and industrial engineering. Countries including Germany, the U.K., and France play a central role in shaping regional demand due to their well-established industrial bases.

Germany Industrial Radiography Equipment Market Trends

Germany remains the largest contributor within Europe, supported by its strong automotive and industrial manufacturing sectors. Companies such as ZEISS Group and Dürr NDT GmbH are leading innovations in automated X-ray inspection systems. For instance, ZEISS has introduced advanced automated 2D X-ray solutions for high-volume automotive casting inspection, particularly for EV battery housings and lightweight components. These developments are accelerating the adoption of fully automated inspection systems in German manufacturing facilities, thereby improving throughput and consistency in quality.

U.K. Industrial Radiography Equipment Market Trends

The U.K. is experiencing steady growth, supported by aerospace maintenance, repair, and overhaul (MRO) activities and industrial inspection services. Companies such as Nikon Metrology are expanding their X-ray and CT inspection capabilities, particularly in aerospace and advanced manufacturing. Increased investments in nuclear energy projects are also driving demand for radiography systems used in inspecting reactor components and pressure vessels, reinforcing the country’s role in high-value inspection applications.

Asia Pacific Industrial Radiography Equipment Market Trends

Asia Pacific is set to be the fastest-growing region, expanding at a CAGR of 9.9%. Rapid industrialization, infrastructure development, and manufacturing expansion are the primary drivers of growth. China holds a substantial share due to its large industrial base, while India is emerging as the fastest-growing market.

China Industrial Radiography Equipment Market Trends

China dominates the regional market due to its extensive manufacturing ecosystem and large-scale infrastructure projects. The country has seen significant adoption of advanced X-ray inspection systems in automotive and electronics manufacturing. Companies such as Comet Group and Hitachi High-Tech Corporation have expanded their presence in China, offering high-energy X-ray and CT systems tailored for industrial applications. The rapid growth of electric vehicle production in China has further increased demand for battery inspection systems that use radiography to detect internal defects in battery cells and modules. These developments are driving the transition toward automated and high-throughput inspection technologies.

India Industrial Radiography Equipment Market Trends

India is the fastest-growing market in the region, supported by investments in infrastructure, energy, and manufacturing. Domestic companies such as Parth Systems India Pvt. Ltd. are contributing to the localized production of industrial X-ray systems, improving accessibility and cost efficiency. Government initiatives focused on manufacturing expansion and infrastructure development are increasing demand for inspection technologies across railways, power plants, and construction projects. The growth of renewable energy and thermal power capacity is also driving the need for radiography in turbine and pipeline inspections. These factors are positioning India as a key growth engine within Asia Pacific.

Competitive Landscape

The global industrial radiography equipment market is moderately fragmented, with a mix of global and regional players competing across different segments. Leading companies maintain strong positions in specific areas such as detectors, radiation sources, or software solutions. The competitive landscape is characterized by continuous innovation and product differentiation. While top players dominate the premium segment, smaller firms cater to niche applications and regional markets, creating a diverse and competitive ecosystem.

Recent industry developments highlight a strong focus on innovation and consolidation. New product launches are centered on advanced X-ray and computed tomography systems designed for high-precision inspection. Automation and AI integration are becoming key differentiators, particularly in automotive and battery manufacturing applications. Strategic partnerships are emerging to enhance multi-modal inspection capabilities and expand technological expertise. Mergers and acquisitions are also shaping the market, with companies restructuring portfolios to strengthen their core competencies and expand their global footprint.

Key Industry Developments:

- In April 2026, Hexagon AB announced the acquisition of Waygate Technologies from Baker Hughes for approximately US$1.45 billion, aiming to expand its capabilities in non-destructive testing by integrating radiography, CT, and inspection software into a unified precision measurement portfolio.

- In July 2025, ZEISS Group launched the OMNIA GC 220-180 automated X-ray inspection system, designed for high-volume inspection of large castings and EV battery components, strengthening its position in automotive and e-mobility applications.

- In May 2025, ZEISS Group introduced the METROTOM 800 320 kV CT system, enhancing high-energy computed tomography capabilities for complex industrial components, particularly in aerospace and heavy manufacturing.

Companies Covered in Industrial Radiography Equipment Market

- Waygate Technologies

- Varex Imaging Corporation

- Nikon Metrology

- Comet Group

- ZEISS Group

- FUJIFILM Holdings Corporation

- Dürr NDT GmbH

- Vidisco Ltd.

- North Star Imaging

- Hitachi High-Tech Corporation

- Mettler-Toledo International Inc.

- Teledyne Technologies Incorporated

- Rigaku Corporation

- Bosello High Technology srl

- Carestream Health

- YXLON International GmbH

Frequently Asked Questions

The global industrial radiography equipment market is projected to be valued at US$1.9 billion in 2026.

The industrial radiography equipment market is expected to reach US$3.1 billion by 2033.

Key trends include the shift from film-based to digital radiography, increasing adoption of automated and AI-enabled inspection systems, growing demand from electric vehicle and battery manufacturing, and rising investments in infrastructure and power generation projects.

The detection & imaging devices segment is the leading category, accounting for an anticipated share of 48.7%, due to its critical role in capturing inspection data across all applications.

The industrial radiography equipment market is expected to grow at a CAGR of 7.4% from 2026 to 2033.

Major companies include Waygate Technologies, Varex Imaging Corporation, Nikon Metrology, Comet Group, and ZEISS Group.