- Technology

- LED Driver ICs Market

LED Driver ICs Market Size, Share, and Growth Forecast, 2026 - 2033

LED Driver ICs Market by Power Conversion Type (AC-DC, DC-DC, Linear), Topology (Buck, Boost, Buck-Boost, Charge Pump, Others), End User (Residential, Commercial, Industrial, Automotive, Healthcare, Telecom, Aerospace & Defense, Others), and Regional Analysis for 2026 - 2033

LED Driver ICs Market Size and Trends

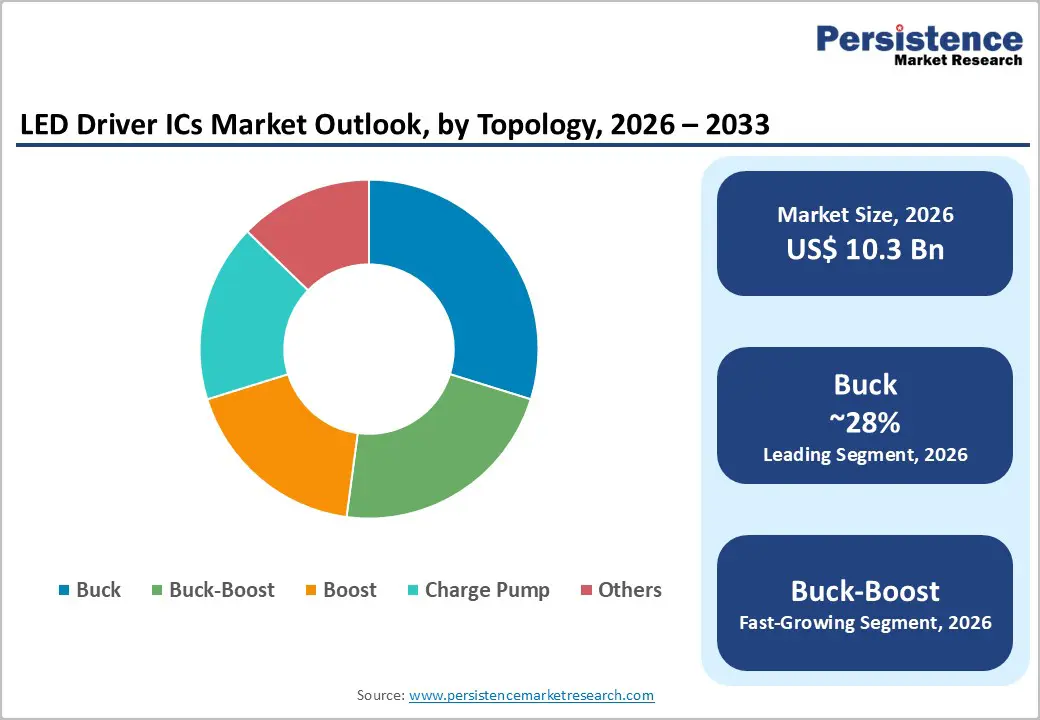

The global LED driver ICs market size is projected to rise from US$10.3 Bn in 2026 to US$22.9 Bn by 2033. It is anticipated that the market will grow at a CAGR of 12.1% from 2026 to 2033, driven by the global transition toward energy-efficient solid-state lighting solutions, intensifying government mandates to phase out conventional light sources, and the exponential proliferation of LED technology across sectors.

Regulations such as the European Union Ecodesign Directive and U.S. Department of Energy (DOE) efficiency standards are compelling manufacturers and end users to adopt advanced LED lighting systems, thereby directly fueling demand for sophisticated driver-integrated circuits (ICs) that regulate power delivery, enable dimming, and ensure the longevity of LED assemblies.

Key Industry Highlights:

- Leading Power Conversion Type: AC-DC dominates the market with over 54% share in 2026, valued at more than US$ 5.6 Bn, driven by large-scale grid-connected lighting systems, smart city deployments, and widespread LED retrofitting. DC-DC is the fastest-growing segment, driven by rising demand in automotive electronics, portable devices, and renewable energy-based lighting applications that require precise voltage regulation.

- Leading Topology: Buck converters hold over 28% market share in 2026, due to their high efficiency, cost-effectiveness, and strong performance in step-down voltage LED applications across commercial and automotive lighting. Buck-Boost topology is the fastest-growing segment, driven by its ability to maintain stable LED performance under fluctuating input conditions in EVs, solar lighting systems, and adaptive smart lighting networks.

- Leading End-user: Commercial segment commands the largest share at over 35% in 2026, valued at more than US$ 3.6 Bn, supported by strong adoption across offices, retail spaces, hospitality, and smart building infrastructure. Automotive is the fastest-growing industry, with a CAGR of 15.6%, driven by rapid electrification, ADAS integration, and the increasing deployment of advanced LED-based lighting systems in modern vehicles.

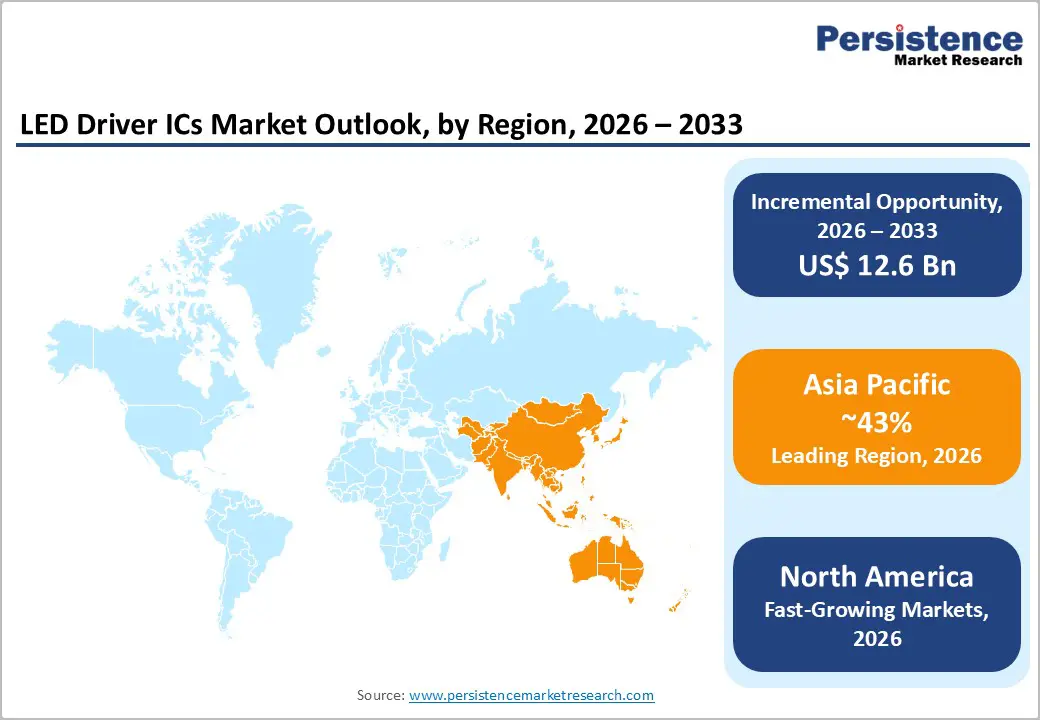

- Leading Region: Asia Pacific leads the global market with over 43% share in 2026, valued at around US$ 4.4 Bn, supported by strong semiconductor manufacturing ecosystems, large-scale LED production, and rapid smart city development. North America follows with over 27% share, driven by smart infrastructure upgrades and automotive adoption.

| Key Insights | Details |

|---|---|

| LED Driver ICs Market Size (2026E) | US$10.3 Bn |

| Market Value Forecast (2033F) | US$22.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 12.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 10.8% |

Market Dynamics

Driver - Surging Demand for Energy-Efficient Lighting and Stringent Regulatory Mandates

The LED Driver ICs market is intensifying global emphasis on energy conservation backed by binding regulatory frameworks. Lighting accounts for 10-15% of global electricity consumption; replacing conventional sources with LED solutions can reduce lighting energy use by 40-50%. Governments across the European Union, the United States, China, and India have enacted binding phase-out schedules for incandescent and halogen bulbs and have mandated minimum luminous efficacy thresholds.

Energy Star certifications, RoHS compliance, and IEC 61347 safety standards create a baseline requirement for high-performance driver ICs. As of 2025, more than 50% of global streetlight modernization projects specify digital driver ICs with power-factor correction and pulse-width modulation capabilities, underscoring the regulatory tailwind on the market.

Automotive Electrification and Smart Lighting Integration

The escalating adoption of electric vehicles (EVs) and advanced driver-assistance systems (ADAS) is emerging as a high-velocity demand catalyst. Global car production recorded a 3.5% increase in 2025 alone, underscoring the automotive sector's expanding role as an LED driver IC consumer.

Modern EV platforms deploy LED arrays for adaptive headlights, matrix beam systems, taillights, interior ambiance lighting, and LiDAR-adjacent optical systems, all requiring ruggedized, thermally stable driver ICs with precise PWM dimming and fault diagnostics. The smart lighting segment is gaining substantial traction, with driver ICs increasingly being integrated with Bluetooth, Wi-Fi, and NB-IoT wireless modules to enable remote control, dynamic dimming, and human-centric lighting (HCL) in smart building deployments.

Restraint - Semiconductor Supply Chain Vulnerabilities and Raw Material Price Volatility

The LED driver IC market remains structurally exposed to global semiconductor supply-chain disruptions. Shortages that began in 2020 continued to impact approximately 30-35% of LED driver IC suppliers by 2024, with around 20% of companies reporting measurable delays in wafer fabrication cycles. Price volatility of critical raw materials, including gallium nitride (GaN), silicon carbide (SiC), and specialized packaging components, creates unpredictable cost structures for manufacturers, squeezing profit margins and constraining timely product launches. Geopolitical tensions affecting export controls on advanced semiconductor materials further aggravate this restraint, complicating supply diversification efforts and increasing lead times for finished driver IC products.

Thermal Management Complexity and High Cost of Compliance

LED systems generate significant heat during operation, requiring driver ICs to incorporate sophisticated thermal management and protection circuitry. Designing ICs that maintain stable output current across wide temperature ranges while meeting stringent standards such as EN 61347, EN 55015 for EMC, and automotive-grade AEC-Q100 qualification substantially increases development costs and extends time-to-market.

For smaller and regional manufacturers, the dual burden of achieving regulatory compliance and managing heat dissipation in compact form factors presents a meaningful competitive disadvantage. These combined engineering and compliance costs impede market entry and restrain the pace of product diversification.

Opportunity - Smart City Infrastructure Development and IoT-Enabled Intelligent Lighting Systems

The rapid proliferation of smart city programs globally represents a transformative growth opportunity for manufacturers. Municipal governments in the United States and China are committing substantial capital to intelligent street lighting networks that integrate IoT-based control platforms. For example, New York State completed the replacement of 500,000 streetlights with smart LED fixtures under the Smart Street Lighting NY program three years ahead of schedule. In smart city projects across the Asia Pacific region, up to 30% of infrastructure budgets are now allocated to intelligent lighting, which relies on driver ICs that support dimming, color tuning, and wireless control. The growing adoption of IoT and AI-powered adaptive lighting is expected to drive demand for next-generation driver ICs with integrated wireless connectivity.

Mini-LED and Micro-LED Backlighting for Displays, AR/VR, and Smart Wearables

The proliferation of Mini-LED and Micro-LED display technologies in premium televisions, monitors, AR/VR headsets, and smart glasses is generating a technically demanding and rapidly growing sub-segment for specialized LED driver ICs. TCL Mini LED TV shipment increased by 33.6% YoY, directly amplifying downstream demand for high-precision, multi-channel driver ICs capable of managing thousands of independently dimmed local zones.

AR/VR headsets and smart glasses, such as those powered by ams OSRAM's VEGALED ultra-compact RGGB LED arrays, require driver ICs with nanoscale precision, ultralow power consumption, and thermal stability to sustain wearable form factors. As the global smart wearables and immersive display market accelerates, companies developing compact, highly integrated LED driver ICs with sub-microsecond PWM dimming resolution and multi-topology flexibility are positioned to unlock a premium, rapidly expanding revenue pocket.

Category-wise Analysis

Power Conversion Type Insights

AC-DC dominates the market, capturing more than 54% market share in 2026, with a value exceeding US$ 5.6 Bn, driven by the widespread need for direct conversion of grid AC power to a stable DC output for LED systems. Increasing urban infrastructure development and large-scale smart lighting deployments further strengthen demand. AC-DC solutions are preferred for their high efficiency, safety compliance, and support for constant-current control. Growing retrofitting of traditional lighting systems with LED technology also boosts their usage. Their compatibility with a wide range of voltage conditions makes them the most widely deployed segment.

DC-DC is expected to grow rapidly due to rising deployment in battery-powered and low-voltage LED systems. Their importance is increasing in automotive lighting, portable devices, and renewable energy-based lighting setups. These drivers ensure precise voltage regulation, which is essential for energy-efficient and long-life LED performance. Expansion of electric vehicles and solar-powered lighting systems is significantly boosting demand. They are also favored in smart lighting applications requiring flexible dimming and control. The shift toward compact, energy-efficient electronics is a key factor accelerating their adoption.

Topology Insights

Buck holds over 28% market share in 2026 due to its simple design and high efficiency in stepping down voltage for LED applications. It is widely used in applications where input voltage is consistently higher than LED operating voltage, such as commercial lighting and automotive interiors. The demand is driven by its cost-effectiveness, low power loss, and reliable thermal performance. Buck converters also support stable current regulation, which is critical for LED lifespan and brightness consistency. The rise in adoption of smart bulbs and LED drivers for appliances further supports its dominance.

Buck-Boost is expected to grow rapidly due to its ability to handle fluctuating input voltages, making it ideal for modern lighting systems. The flexibility to both step up and step down voltage ensures consistent LED performance under varying conditions. Rising integration in electric vehicles and portable lighting systems is a major growth driver. It is also increasingly used in smart grids and off-grid solar lighting solutions. Its versatility makes it essential for next-generation adaptive lighting systems.

End-user Insights

Commercial holds the largest market share at over 35% in 2026, with a value exceeding US$ 3.6 Bn, driven by the extensive deployment of LED lighting in offices, retail spaces, hospitality, and public infrastructure. The shift toward energy-efficient buildings and smart lighting systems is a major driver. Commercial spaces require high-performance lighting with dimming, automation, and long operational life, boosting LED driver IC adoption. Government regulations promoting energy savings further accelerate installation. Large-scale infrastructure modernization and smart city projects are also increasing demand. The need to reduce long-term energy costs supports this segment’s dominance.

The automotive industry is expected to grow at a CAGR of 15.6% due to the increasing adoption of advanced lighting systems. Modern vehicles use LED driver ICs for headlights, tail lights, interior ambient lighting, and adaptive lighting systems. The rise of electric vehicles is a major growth catalyst, as they require efficient power management for extended battery life. Integration of ADAS and smart lighting features further increases demand. Automakers are focusing on energy-efficient and lightweight electronic components, boosting LED driver IC usage. Continuous innovation in vehicle design and safety features is expected to sustain strong growth momentum.

Regional Insights

North America LED Driver ICs Market Trends

North America holds over 27% share in 2026, reaching US$ 2.8 Bn value, led primarily by the United States. Growth is driven by strong LED retrofit adoption across commercial, industrial, and public infrastructure, supported by efficiency programs from the U.S. Department of Energy (DOE) and certifications such as Energy Star, which continue to promote high-efficiency lighting systems.

Large-scale smart city initiatives and infrastructure modernization under federal programs such as the Bipartisan Infrastructure Law are further accelerating demand for smart, IoT-enabled lighting and advanced driver ICs. The region also shows strong automotive adoption, with widespread integration of LED lighting systems in passenger and commercial vehicles, supported by leading semiconductor design companies.

Asia Pacific LED Driver ICs Market Trends

Asia Pacific holds over 43% share in 2026, reaching US$ 4.4 Bn value, supported by strong semiconductor manufacturing and large-scale LED production ecosystems. China is the largest contributor, accounting for a major portion of regional output due to its extensive electronics and lighting manufacturing base. Rapid urbanization and government-led smart city programs across the region are increasing demand for energy-efficient lighting infrastructure.

India is witnessing a strong growth through initiatives such as UJALA and SLNP, which have driven large-scale LED streetlight deployments, while Japan and South Korea lead in advanced automotive and display lighting technologies. The region benefits from integrated supply chains and cost-efficient manufacturing, making it the global hub for LED driver IC production and export.

Europe LED Driver ICs Market Trends

Europe is expected to account for more than 20% of the market share by 2026, driven by stringent energy-efficiency regulations and sustainability goals under the European Union Ecodesign framework. The phase-out of inefficient lighting technologies has accelerated widespread LED adoption across residential, commercial, and industrial sectors, particularly in countries such as Germany, the United Kingdom, and France.

The region’s commitment to Net Zero by 2050 is further increasing demand for advanced LED driver ICs with improved power efficiency, power-factor correction, and thermal performance. Smart public lighting and infrastructure upgrades across countries such as Spain, the Netherlands, and Nordic nations are supporting the adoption of IoT-enabled lighting systems, thereby strengthening long-term market growth.

Competitive Landscape

The global LED driver IC market is moderately consolidated at the top tier, with the leading players controlling over 40% of market share, while the broader general lighting segment remains more fragmented. Market leaders focusing on broad topology coverage, advanced dimming capabilities, integration of GaN and SiC wide-bandgap materials, and compliance with automotive safety standards such as AEC-Q100.

Emerging business models include silicon IP licensing, co-development partnerships with lighting OEMs, and distributor-centric channel models targeting cost-sensitive Asia Pacific markets. M&A activity remains robust as companies seek to fill portfolio gaps and expand geographic reach.

Key Developments:

- In March 2025, Lumissil Microsystems introduced the IS31FL3758 LED driver IC, a 48-channel constant-current driver designed for high-density LED matrix displays. The IC supports up to a 40×9 (360-LED) configuration and is targeted at applications such as display panels, appliance HMIs, and gaming systems.

- In February 2025, Macroblock introduced its DaVinci Series LED Driver ICs, targeting high-end LED display applications. The new series focuses on improving visual performance, low-gray uniformity, flicker reduction, and power efficiency through advanced technologies such as Adaptive Refresh and 19-bit grayscale. These ICs are designed for premium displays used in virtual production, XR, broadcast, and high-resolution LED screens, aiming to deliver smoother image quality and better energy efficiency.

Companies Covered in LED Driver ICs Market

- Texas Instruments

- Analog Devices

- Infineon Technologies

- ON Semiconductor

- STMicroelectronics

- NXP Semiconductors

- ROHM Semiconductor

- Renesas Electronics

- Microchip Technology

- Toshiba

- Skyworks Solutions

- Diodes Incorporated

- Others

Frequently Asked Questions

The global LED driver ICs market is projected to be valued at US$10.3 Bn in 2026.

The rising adoption of energy-efficient LED lighting, supported by global energy-saving regulations and smart lighting integration are key driver of the market.

The LED Driver ICs market is expected to witness a CAGR of 12.1% from 2026 to 2033.

The expansion of smart city infrastructure, IoT-enabled connected devices, and the growth of mini and micro-LED displays are creating strong growth opportunities.

Texas Instruments, Analog Devices, Infineon Technologies, ON Semiconductor, STMicroelectronics, NXP Semiconductors, ROHM Semiconductor, Renesas Electronics, and Microchip Technology are among the leading key players.