- Nutraceuticals & Functional Foods

- Lactose Market

Lactose Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Lactose Market is segmented by Product Type (Lactulose, Galactose, Lactose Monohydrate), by Form (Powder, Granule), by End Use (Food and Beverage, Infant Formula, Pharmaceuticals, Animal Feed, Others), and by Regional Analysis, 2026 - 2033

Lactose Market Share and Trends Analysis

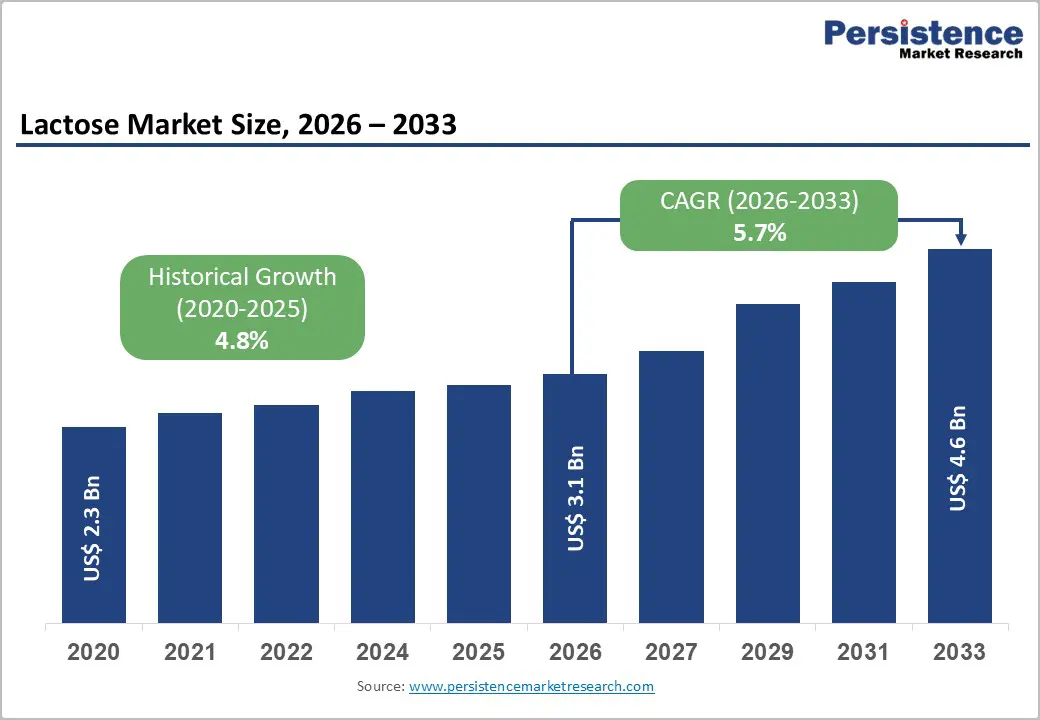

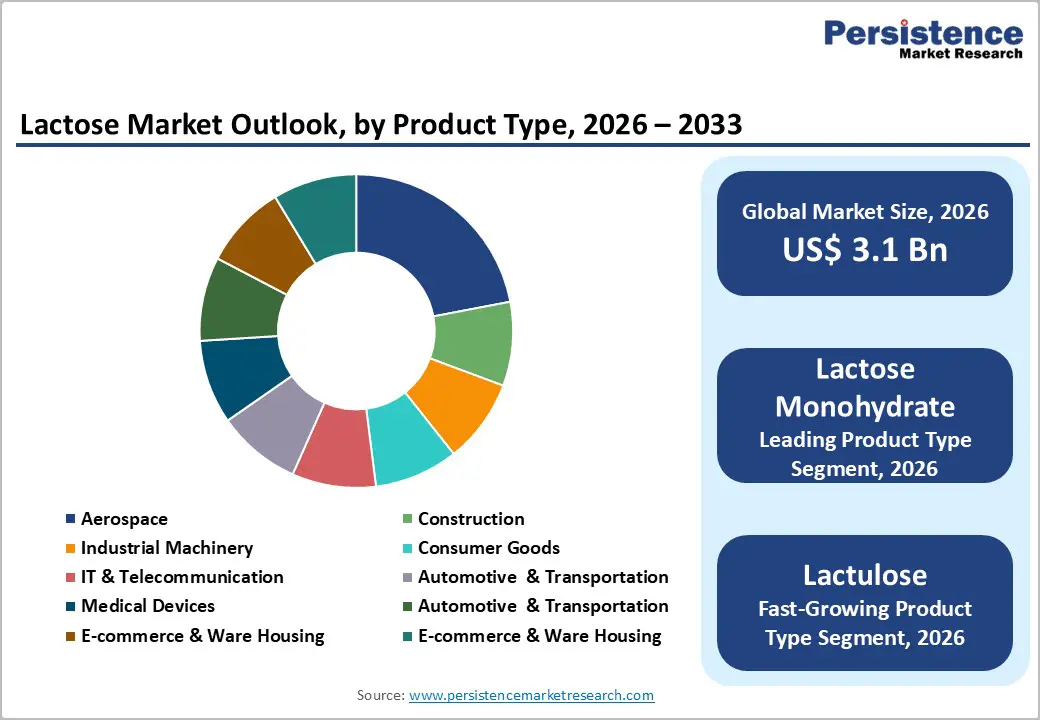

The global lactose market size is expected to be valued at US$ 3.1 billion in 2026 and projected to reach US$ 4.6 billion by 2033, growing at a CAGR of 5.7% between 2026 and 2033. The market expansion is primarily driven by the surging demand for refined lactose in the pharmaceutical sector as a critical excipient and the rising production of infant formula globally.

As manufacturers focus on high-purity ingredients to meet stringent safety standards, the transition toward specialized lactose derivatives has intensified. This growth is further supported by the increasing utilization of lactose in the food processing industry for its browning properties and ability to carry flavors effectively, ensuring a steady demand across both developed and emerging economies.

Key Industry Highlights:

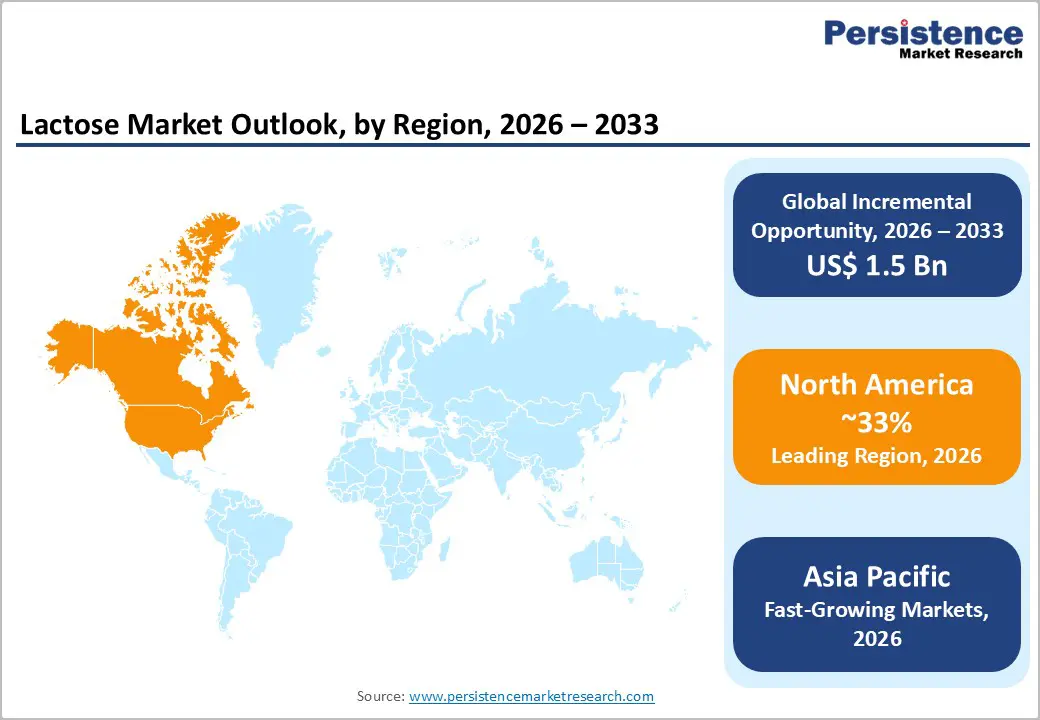

- Leading Region: North America, holding 33% market share, supported by advanced pharmaceutical manufacturing, well-established dairy processing infrastructure, and strong regulatory frameworks that encourage development of high-purity lactose excipients.

- Fastest-Growing Region: Asia Pacific, driven by expanding infant formula demand in China and India, rising pharmaceutical production capacity, increasing healthcare expenditure, and growing reliance on imported pharmaceutical-grade lactose.

- Leading Product Type Segment: Lactose Monohydrate, accounting for around 59% share due to its excellent compressibility, chemical stability, and widespread application as a standard excipient in tablets, capsules, and infant nutrition formulations.

- Growth Indicator: Expanding pharmaceutical manufacturing and rising chronic disease prevalence are increasing demand for reliable excipients such as lactose that ensure drug stability, controlled delivery, and consistent tablet formulation.

- Market Opportunity: Growing application of lactose in animal nutrition and veterinary medicine, particularly in piglet starter diets and pet pharmaceuticals, is opening new revenue streams for dairy-derived carbohydrate ingredients.

- Key Developments: In February 2026, DFE Pharma launched EcoLact 2030 to provide verified sustainability transparency across its lactose ingredient portfolio. In July 2025, Lactalis USA announced an investment exceeding $75 million to expand production capacity at two New York dairy facilities.

| Key Insights | Details |

|---|---|

| Global Lactose Market Size (2026E) | US$ 3.1 Bn |

| Market Value Forecast (2033F) | US$ 4.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.8% |

Market Dynamics

Driver - Growing Demand for Pharmaceutical Grade Lactose as a Reliable Excipient

The primary driver for the lactose industry is its indispensable role as a filler and diluent in the production of solid dosage forms, such as tablets and capsules. Lactose monohydrate is one of the most widely used inactive ingredients due to its excellent compressibility, physical stability, and compatibility with a broad range of active pharmaceutical ingredients (APIs). As the global pharmaceutical industry expands to address chronic illnesses and an aging population, the demand for high-purity, spray-dried, and anhydrous lactose has spiked. This trend is particularly evident in the production of inhalation powders, where specifically engineered lactose particles are required to ensure consistent drug delivery to the lungs.

Restraints - Volatile Prices of Raw Material and Dependence on Cheese Production

The production of lactose is inextricably linked to the cheese manufacturing process, as it is a byproduct of whey. Consequently, the supply and pricing of lactose are highly sensitive to fluctuations in the global dairy market and cheese consumption patterns. When cheese production slows down or when there are disruptions in the milk supply chain due to environmental factors or animal diseases, the availability of whey permeates the primary raw material for lactose becomes limited. This supply chain dependency often leads to price volatility, making it challenging for end-users in the Pharmaceuticals and Infant Formula sectors to maintain stable procurement costs. Furthermore, the high energy costs associated with the evaporation and crystallization processes required to refine lactose further pressure the profit margins of manufacturers.

Opportunity - Expansion into the Animal Feed and Veterinary Medicine Sector

The utilization of lactose in animal nutrition represents a significant untapped potential, especially in the early-stage feeding of livestock. In the swine industry, lactose is frequently added to piglet starter diets to ease the transition from sow's milk to solid feed, as it provides a readily available energy source and improves gut health. Statistics from Persistence Market Research indicate a growing trend toward using dairy-derived carbohydrates to reduce mortality rates in young livestock. Furthermore, the veterinary pharmaceutical sector is increasingly adopting lactose as a carrier for various medications and nutritional supplements for pets. As the global demand for meat and dairy products rises, the animal feed industry's requirement for consistent, high-energy ingredients like lactose is expected to generate significant demand for lower-grade edible lactose.

Category-wise Analysis

Product Type Insights

Lactose Monohydrate segment is the leading segment in Category-1, accounting for a dominant 59% market share in 2026. Its leadership is justified by its widespread application as a primary excipient in the pharmaceutical industry and its foundational role in infant formula. The crystalline stability and long shelf life of monohydrate versions make them the industrial standard for large-scale manufacturing. Meanwhile, Lactulose is identified as the fastest-growing segment through 2033. This rapid growth is driven by the increasing clinical validation of its prebiotic benefits and its rising use in pharmaceutical laxatives. As consumer demand for digestive health solutions increases, the conversion of lactose into medicinal-grade lactulose is becoming a high-revenue strategy for key market players.

Form Insights

Powder segment currently holds the leading market share in 2025, favored for its ease of integration into dry-mix formulations and its superior solubility in liquid applications. Powdered lactose is the preferred form for Infant Formula and Pharmaceuticals, where precise measurements and uniform distribution of ingredients are critical. On the other hand, the Granule segment is emerging as a significant contributor, particularly in the production of direct-compression tablets. Granulated lactose offers better flowability and reduced dust during the manufacturing process, which are essential for high-speed pharmaceutical tableting machines. This form is expected to see steady growth as drug manufacturers seek to optimize their production efficiencies and reduce waste in the coming years.

Region-wise Insights

North America Lactose Market Trends and Insights

North America is the leading region in the global lactose market, holding a 33% market share in 2025. The region's dominance is underpinned by a highly advanced pharmaceutical sector and a robust dairy processing infrastructure in the United States. The presence of leading organizations such as Hilmar Ingredients and Leprino Foods ensures a steady supply of high-grade lactose. The U.S. regulatory framework, governed by the FDA, provides a stable environment for the use of lactose in both medical and food applications, fostering an innovation ecosystem where companies are developing specialized lactose grades for advanced drug delivery systems.

Key trends in this region include a significant focus on high-oleic and specialty lactose products for the sports nutrition market. American consumers are increasingly seeking transparent labeling and non-GMO ingredients, which has led to a rise in demand for cleaner lactose extraction processes. Furthermore, the collaboration between dairy producers and pharmaceutical researchers in the U.S. has resulted in the development of anhydrous lactose forms that are ideal for moisture-sensitive medication. The region's mature market status means that growth is primarily driven by value-added products rather than volume alone, with a strong emphasis on meeting the precise technical specifications of the high-end medical industry.

Asia Pacific Lactose Market Trends and Insights

Asia Pacific is identified as the fastest-growing segment for the lactose market through 2033. This rapid growth is primarily fueled by the massive demand for infant formula in China, India, and the ASEAN nations. As disposable incomes rise and urbanization increases, more parents are turning to premium, lactose-enriched infant milk powders. China's manufacturing advantages and its status as a global pharmaceutical manufacturing hub are also driving the demand for excipient-grade lactose. Local production is increasing, but the region still relies heavily on imports from North America and Oceania for high-purity variants.

Growth dynamics in India are particularly noteworthy due to the country's status as the world's largest milk producer and its burgeoning generic drug industry. The Indian government's push for self-reliance in pharmaceutical ingredients is encouraging local dairy companies to invest in lactose refining facilities. In Japan, the focus is on the functional food market, where lactose-derived prebiotics are highly popular. The overall region benefits from a young population and a booming healthcare sector, which are expected to maintain a high demand for lactose in both food and medicine. The expansion of modern retail and e-commerce further facilitates the distribution of lactose-containing products across this diverse geographical area.

Competitive Landscape

The Lactose Market exhibits a consolidated structure, where a few global dairy giants and specialized pharmaceutical ingredient companies hold a significant share. Companies like Royal FrieslandCampina NV, Fonterra Co-Operative Group Limited, and Kerry Group plc dominate the supply chain due to their control over raw milk and whey permeate sources. Their strategy often involves vertical integration, allowing them to oversee the entire process from dairy farming to the final crystallization of pharmaceutical-grade lactose. Key differentiators employed by market leaders include the development of proprietary spray-drying techniques and the attainment of global quality certifications. Emerging business model trends show a shift toward co-innovation partnerships with pharmaceutical firms to create customized excipients for specific drug formulations. Research and development focus is increasingly directed toward improving the purity and consistency of lactose particles to enhance the stability of life-saving medications.

Key Developments:

- In February 2026, DFE Pharma launched EcoLact 2030, an initiative aimed at improving transparency and providing verified sustainability data across its lactose ingredient portfolio.

- In July 2025, Lactalis USA announced an investment of over $75 million to expand production capacity at its two dairy processing facilities in New York.

Companies Covered in Lactose Market

- Fonterra Co-Operative Group Limited

- Arla Foods amba

- Royal FrieslandCampina NV

- Kerry Group plc

- Saputo Inc.

- Lactalis Ingredients

- DMK Group

- Agropur

- Leprino Foods

- Hilmar Ingredients

- Others

Frequently Asked Questions

The global Lactose market is projected to be valued at US$ 3.1 Bn in 2026.

Growing Demand for Pharmaceutical-Grade Lactose as a Reliable Excipient is a major factor driving the global Lactose market.

The Global Lactose market is poised to witness a CAGR of 5.8% between 2026 and 2033.

Expansion into the Animal Feed and Veterinary Medicine Sector is a significant opportunity in the Lactose market.

Major players in the Global Lactose market include Fonterra Co-Operative Group Limited, Arla Foods amba, Royal FrieslandCampina NV, Kerry Group plc, Saputo Inc., Lactalis Ingredients, and others.