- Specialty & Fine Chemicals

- Isobutyric Acid Market

Isobutyric Acid Market Size, Share, and Growth Forecast 2026 - 2033

Isobutyric Acid Market by Product Type (Synthetic, Renewable), End-user (Animal Feed, Chemical Intermediates, Food & Flavors, Pharmaceutical, Perfumes, Other), and Regional Analysis for 2026 - 2033

Isobutyric Acid Market Size and Trend Analysis

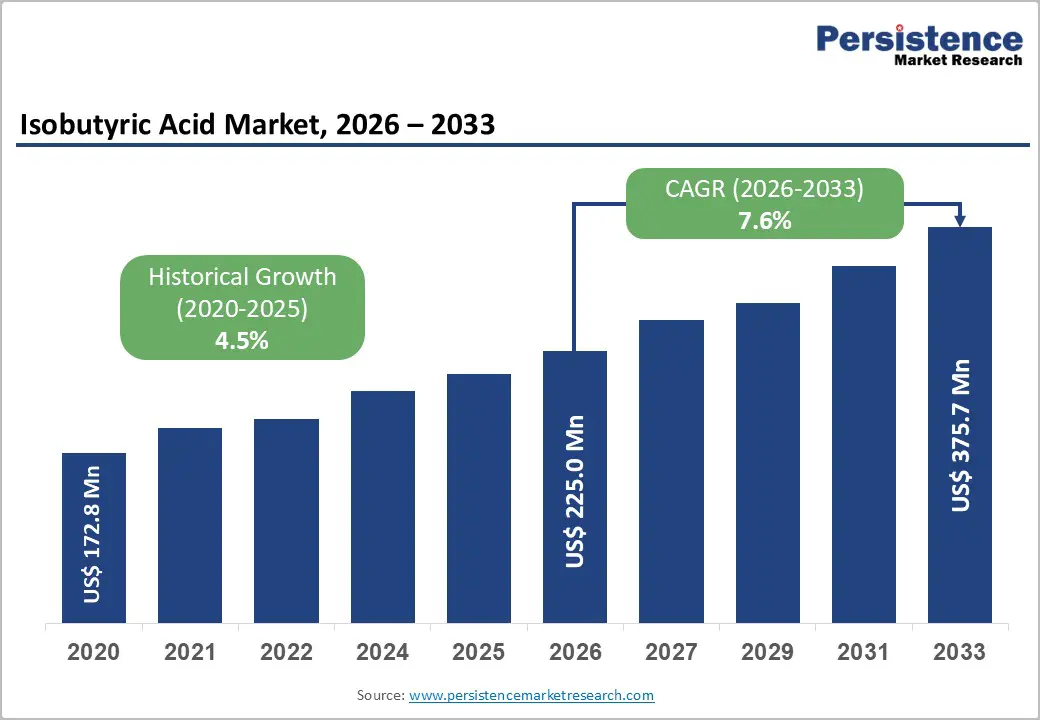

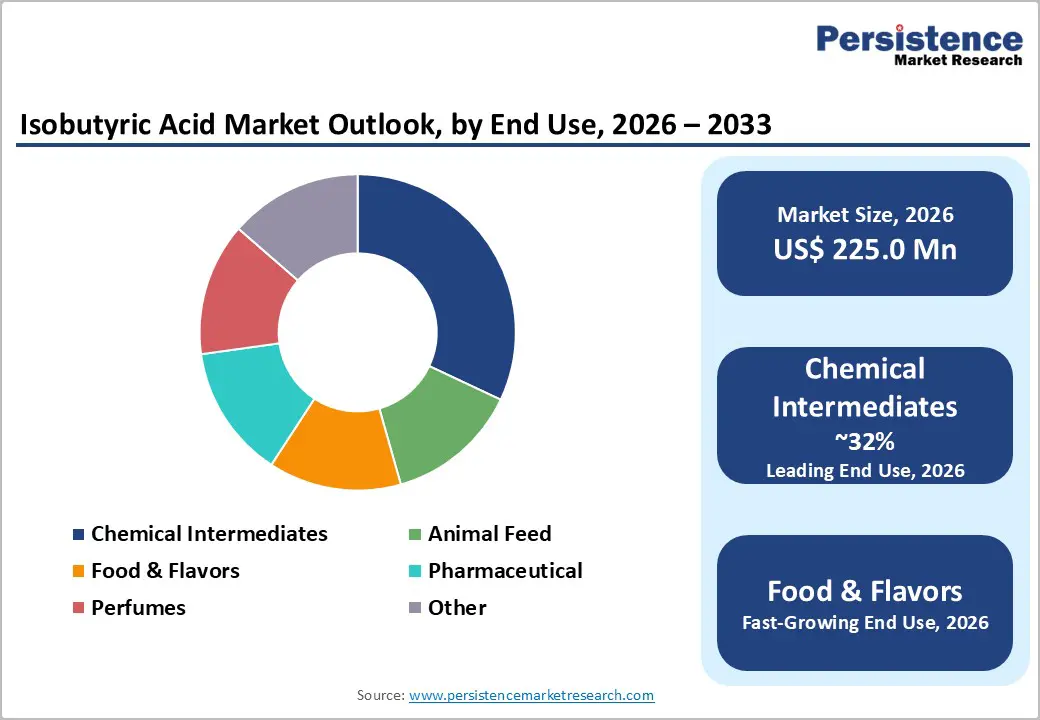

The global isobutyric acid market size is likely to be valued at US$ 225.0 million in 2026 and is projected to reach US$ 375.7 million by 2033, growing at a CAGR of 7.6% between 2026 and 2033.

The market expansion is primarily driven by rising adoption of bio-based chemicals in response to stringent environmental regulations and increasing demand from the pharmaceutical and food sectors. The U.S. FDA and USDA have been actively promoting renewable chemical production, creating favorable regulatory environments that encourage manufacturers to invest in sustainable isobutyric acid production technologies. Isobutyric acid serves as a vital feed additive that enhances the nutritional value and palatability of animal feed, thereby improving livestock productivity and feed conversion rates.

Key Industry Highlights:

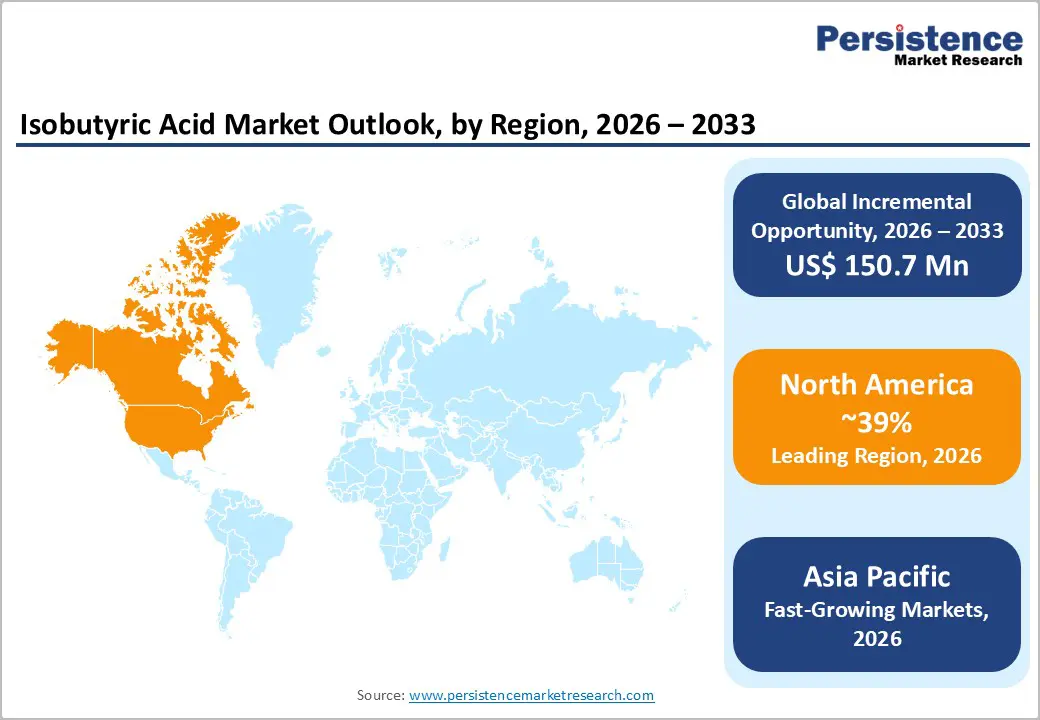

- Regional Leader: North America maintains market leadership, with 39% share, driven by the U.S.'s robust manufacturing infrastructure, supported by favorable FDA and USDA policies promoting renewable chemicals.

- Fastest Growing Region: Asia Pacific exhibits the highest growth trajectory with China and India, driven by rapid industrialization, expanding pharmaceutical API manufacturing, and government investment incentives.

- Leading Segment: Synthetic Product Type commands approximately 65% market share due to cost-efficiency, scalability, and consistent high-purity quality meeting pharmaceutical and chemical intermediate specifications.

- Fastest Growing Segment: Food and Flavors end-user represents the most rapidly expanding application, driven by consumer preferences for natural ingredients and clean-label products.

- Key Opportunity: Bio-Based Production Expansion presents substantial growth potential as Afyren achieved continuous production at AFYREN NEOXY biorefinery in 2025 using AFYNERIE® technology, supported by governmental R&D incentives, €21 million investment, and alignment with EU circular economy mandates promoting renewable chemical alternatives.

| Key Insights | Details |

|---|---|

|

Isobutyric Acid Market Size (2026E) |

US$ 225.0 Mn |

|

Market Value Forecast (2033F) |

US$ 375.7 Mn |

|

Projected Growth CAGR (2026-2033) |

7.6% |

|

Historical Market Growth (2020-2025) |

4.5% |

Market Dynamics

Drivers - Increasing Demand in the Animal Feed Sector

The animal feed industry is a rapidly growing application area for isobutyric acid, owing to its proven effectiveness as a feed acidifier and growth promoter in livestock nutrition. Research published in Frontiers in Veterinary Science indicates that dietary supplementation with 0.5% isobutyric acid significantly enhances intestinal mucosal barrier function, improves antioxidant capacity through elevated total antioxidant capacity (T-AOC) levels, and increases superoxide dismutase (SOD) activity in weaned piglets.

Furthermore, it contributes to superior meat quality by improving marbling, intramuscular fat (IMF), and triglyceride (TG) content. With rising demand for natural alternatives to antibiotic growth promoters, isobutyric acid offers multifunctional benefits, including antimicrobial properties that improve feed safety and shelf life. These attributes position it as an essential component in modern animal nutrition strategies.

Expansion in Pharmaceutical and Chemical Synthesis

Isobutyric acid is a key intermediate in the synthesis of active pharmaceutical ingredients (APIs) and drug formulations, driving strong demand within the global pharmaceutical sector. It is widely employed in producing analgesics, anti-inflammatory drugs, and stabilizers that enhance the sensory properties of oral medications while ensuring extended shelf life.

Asia Pacific has emerged as the fastest-growing market for pharmaceutical chemicals, with China leading in production volumes and India specializing in API manufacturing. Favorable government policies across the region are accelerating investments in pharmaceutical and nutraceutical additives through 2030. Enhanced regulatory frameworks aligned with ICH Q7 standards and infrastructure development further strengthen manufacturing capabilities, positioning pharmaceutical applications as a major growth driver.

Restraint - High Production Costs Associated with Bio-Based Manufacturing Processes

Although renewable isobutyric acid offers clear sustainability benefits, its bio-based production faces significant cost barriers that hinder widespread adoption. Bio-fermentation processes using non-genetically modified microorganisms require extensive R&D, with companies such as Afyren investing over two million laboratory hours to achieve commercial viability. The proprietary AFYNERIE® technology, protected by multiple global patents, involves complex raw material sourcing, advanced separation and purification steps, and substantial capital investment in biorefinery infrastructure.

In contrast, synthetic isobutyric acid continues to dominate the market due to its cost efficiency, high purity, and consistent quality, exemplified by Eastman Chemical’s 12% output increase in 2023 through established petrochemical routes. Limited scalability of renewable methods compared to conventional production creates price disparities, constraining broader adoption despite rising environmental awareness.

Stringent Regulatory Compliance Requirements for Multiple Applications

Isobutyric acid manufacturers face complex regulatory landscapes across diverse end-use sectors, imposing significant compliance burdens that impact market operations. In pharmaceutical applications, intermediates must meet strict standards for purity, quality, and consistency as mandated by the European Directorate for the Quality of Medicines (EDQM) in the EU and the FDA in the U.S., requiring comprehensive documentation, process validation, and quality control protocols. The European Chemicals Agency (ECHA) requires intermediates to be registered under REACH regulations, necessitating extensive substance evaluation and safety data compilation.

Food-grade isobutyric acid for flavoring applications must comply with FDA food additive regulations and undergo rigorous safety assessments. The European Union's circular economy action plan and bio-based industry policies impose additional requirements on sustainable chemical production. These multi-jurisdictional regulatory frameworks create barriers to entry for new market participants and increase operational costs for existing manufacturers.

Opportunity - Expansion of Bio-Based Production Through Fermentation Technologies

The transition toward renewable and bio-based isobutyric acid production presents substantial growth opportunities aligned with global sustainability goals and environmental regulations. Governmental legislation and policies supporting renewable resources, including R&D incentives and renewable energy programs, are encouraging the development of bio-based alternatives to petroleum-derived chemicals. Afyren has achieved significant milestones with its AFYREN NEOXY biorefinery, reaching continuous production capacity in 2025 and accelerating the commercialization of carboxylic acids from second-generation biomass co-products using a zero-waste approach. Its proprietary fermentation platform converts sugars from diverse biomass sources into seven-carbon acids for applications in cosmetics, flavors, fragrances, nutrition, and fine chemicals. Recent capital raises, including €21 million led by Sofinnova Partners and Valquest Partners, underscore investor confidence. Furthermore, rising demand from the Biodegradable Polymer Market positions isobutyric acid as a sustainable intermediate, enabling direct “drop-in” replacement of petrochemical molecules.

Rising Demand from the Food and Flavors Industry for Natural Ingredients

The food and flavors segment is the fastest-growing application area for isobutyric acid, driven by rising consumer demand for natural ingredients and clean-label products. Its distinctive aroma and taste make it highly valuable as a flavoring agent in confectionery, baked goods, beverages, and savory snacks, creating fruity and creamy profiles. In Q2 2024, Eastman Chemical Company introduced a high-purity grade tailored for food and flavor applications, underscoring industry recognition of this trend.

Esters derived from isobutyric acid are widely used in dairy products, soft drinks, and snack foods, where desirable odor and flavor characteristics are critical. Additionally, the compound functions as a preservative, enhancing food safety and shelf life. Growing regulatory approvals for natural flavoring agents and consumer preference for transparency enable manufacturers using renewable feedstocks to command premium pricing, fostering market expansion aligned with sustainability mandates.

Category-wise Analysis

Product Type Insights

The synthetic segment holds a dominant position in the global isobutyric acid market, accounting for approximately 65% of the total share. This leadership is attributed to its well-established production infrastructure, cost efficiency, and ability to meet stringent industry specifications. Synthetic isobutyric acid, produced via oxo synthesis using petroleum-based feedstocks, ensures high purity and consistent quality for pharmaceutical, chemical intermediate, and industrial applications.

The synthetic route offers scalability for large-volume uses such as plasticizers, solvents, and intermediates, supported by Eastman’s 12% output increase in 2023. While renewable isobutyric acid is gaining traction through biomimetic fermentation technologies, its adoption remains limited due to higher costs and restricted commercial-scale capacity. However, ongoing investments and favorable sustainability regulations signal strong future growth potential for the renewable segment.

End-user Insights

Chemical intermediates constitute the leading end-use segment, accounting for nearly 32% of global isobutyric acid consumption. This dominance is driven by its extensive use in producing value-added derivatives, particularly esters, which serve critical roles in protective coatings, plasticizers, and specialty solvents requiring precise performance characteristics. The pharmaceutical industry significantly contributes to this segment, utilizing isobutyric acid in the synthesis of APIs, analgesics, anti-inflammatory compounds, and stabilizers.

Asia Pacific is the primary consumption region, with China leading production and India specializing in API manufacturing, supported by favorable government policies. Research highlights the importance of isobutyric acid derivatives in vitamin precursors and complex pharmaceutical compounds. Rapid growth in generics, improved regulatory frameworks, and infrastructure investments across China, India, and South Korea further reinforce the segment’s strong market position.

Regional Insights

North America Isobutyric Acid Market Trends

North America remains the leading region in the isobutyric acid market, with 39% of the global market share, primarily supported by the United States’ advanced manufacturing infrastructure and well-established chemical production ecosystem. Eastman Chemical Company, headquartered in Tennessee, operates the largest production capacity in the region through facilities in Kingsport and Longview, Texas. A major capacity expansion completed in 2018 doubled output, following a 2013 debottlenecking project that added 11 million pounds of butyric acid capacity to meet rising demand.

Regulatory frameworks in the U.S. significantly shape market dynamics, with the FDA and USDA promoting renewable chemical production through favorable policies and incentive programs. Furthermore, the region benefits from a mature pharmaceutical industry requiring high-purity chemical intermediates compliant with FDA Good Manufacturing Practice standards for API production.

Europe Isobutyric Acid Market Trends

Europe demonstrates distinctive market characteristics shaped by stringent sustainability regulations and circular economy mandates, driving bio-based chemical adoption. The EU's bioeconomy policies, including the Circular Economy Action Plan and renewed EU Industrial Policy Strategy, prioritize products wholly or partly produced from biomass as central to industrial transformation. The Circular Bio-based Europe Joint Undertaking, established between the EU and Bio-based Industry Consortium, accelerates innovation and market uptake of bio-based solutions while ensuring environmental performance.

France-based Afyren represents regional leadership in renewable isobutyric acid production, achieving continuous production at its AFYREN NEOXY biorefinery in 2025 using the proprietary AFYNERIE® technology protected by 10 patent families. The company raised €21 million in financing led by Sofinnova Partners and Valquest Partners to commercialize carboxylic acids from second-generation biomass, targeting cosmetics, flavors, fragrances, and nutrition markets. The region's emphasis on zero-waste approaches and short supply chains creates competitive advantages for bio-based producers developing sustainable isobutyric acid alternatives.

Asia Pacific Isobutyric Acid Market Trends

Asia Pacific is the fastest-growing regional market for isobutyric acid, driven by rapid industrialization and expansion in the pharmaceutical and specialty chemical sectors. The IMF projects annual GDP growth of 6.5% for India and 5.0% for Indonesia through 2028, far exceeding the G7 average of 1.3%, fueling strong demand for specialty chemicals. China and India dominate the market, together accounting for two-thirds of regional specialty chemical value by 2030.

Pharmaceutical chemicals show robust growth, with China leading in production and India specializing in APIs. Regional advantages include cost-efficient manufacturing, improved regulatory frameworks, and government incentives. ASEAN nations add further demand from food processing and agriculture, adopting isobutyric acid-based feed additives to enhance livestock productivity.

Competitive Landscape

The global isobutyric acid market exhibits a moderately concentrated competitive structure with several established chemical manufacturers controlling significant market shares alongside emerging bio-based producers. Leading players including Eastman Chemical Company, Oxea (OQ Chemicals GmbH), Evonik Industries AG, and Dow Inc. leverage vertical integration strategies and extensive distribution networks to maintain competitive positions in synthetic production. Emerging business model trends feature partnerships between traditional chemical producers and biotechnology companies to commercialize renewable isobutyric acid, exemplified by Afyren's fundraising success and achievement of continuous production at its biorefinery. The competitive landscape is also characterized by geographic expansion strategies targeting high-growth Asia Pacific markets where pharmaceutical and specialty chemical demand is accelerating.

Key Market Developments

- June 2025: Afyren announced its AFYREN NEOXY biorefinery achieved continuous production capacity, marking a significant phase in its industrial strategy and accelerating the commercialization of renewable carboxylic acids, including isobutyric acid from biomass co-products.

- July 2024: Afyren's fermentation laboratory reached 2 million hours of operational experience, identifying new raw materials to fuel industrial expansion and secure diverse biomass sources for replicating profitable production models in multiple geographical regions.

- May 2024: OQ Chemicals GmbH (now Oxea) lifted force majeure declarations at its German carboxylic acid production facilities, fully restoring its isobutyric acid supply capabilities. This development strengthened supply chain stability and reinforced the company's commitment to meeting rising European demand for specialty chemicals.

Top Companies in the Isobutyric Acid Market

Eastman Chemical Company (Kingsport, Tennessee, U.S.) ranks as the global market leader in synthetic isobutyric acid production, operating major manufacturing facilities in Kingsport and Longview, Texas, with combined capacity doubled through a 2018 expansion project. The company recorded 12% output increase at its Tennessee facility in 2023 to meet pharmaceutical and chemical intermediate demand, while launching high-purity grades for food and flavor applications in 2024. Eastman's vertically integrated operations, extensive technical service capabilities, and strong customer relationships across pharmaceutical, food, and industrial sectors position it as the primary supplier for applications requiring consistent quality and regulatory compliance.

Oxea (Oberhausen, Germany) operates as a leading global manufacturer of oxo intermediates and derivatives, including isobutyric acid, serving chemical intermediates, coatings, and specialty applications markets. The company, part of OQ Chemicals, leverages advanced oxo synthesis technology and European production infrastructure to supply pharmaceutical and industrial customers with high-purity isobutyric acid meeting stringent REACH and EDQM specifications. Oxea's investment in sustainable production methods and process optimization enhances its competitive position in environmentally conscious European markets aligned with circular economy mandates.

Afyren (Clermont-Ferrand, France) emerges as the innovation leader in renewable bio-based isobutyric acid production utilizing proprietary AFYNERIE® technology protected by 10 patent families worldwide. The company achieved continuous production at its AFYREN NEOXY biorefinery in 2025, supported by €21 million in funding from Sofinnova Partners and Valquest Partners, positioning it to commercialize sustainable carboxylic acids for cosmetics, flavors, fragrances, nutrition, and fine chemicals markets. Afyren's zero-waste biomimetic fermentation process and expertise in converting second-generation biomass co-products into industry-specification products address growing market demand for environmentally sustainable chemical alternatives.

Companies Covered in Isobutyric Acid Market

- Oxea

- Eastman Chemical Company

- Tokyo Chemical Industry Co., Ltd.

- Evonik Industries AG

- Shanghai Aladdin Biochemical Technology Co., Ltd.

- Snowco

- Nanjing Chemical Material Corp.

- Afyren

- Lygos Inc.

- Dow Inc.

- Yufeng International Group Co., Ltd.

- Jiangsu Dynamic Chemical Co., Ltd.

Frequently Asked Questions

The global isobutyric acid market is valued at US$ 225.0 Mn in 2026 and is projected to reach US$ 375.7 Mn by 2033, growing at a CAGR of 7.6% during the forecast period, driven by pharmaceutical, food and flavors, and chemical intermediate applications.

Key demand drivers include increasing pharmaceutical API production requiring high-purity chemical intermediates, growing adoption in animal feed as nutritional enhancers improving intestinal health in weaned piglets with demonstrated 0.5% supplementation efficacy, and rising consumer preferences for natural flavoring agents in food and beverage applications.

The synthetic segment leads with approximately 65% market share due to cost-efficiency, established production infrastructure, scalability for large-volume applications, and consistent high-purity quality.

North America maintains market leadership driven primarily by the U.S.’s robust chemical manufacturing ecosystem, supported by favorable FDA and USDA renewable chemical policies.

Significant opportunities include bio-based production expansion through fermentation technologies, with Afyren achieving continuous production at AFYREN NEOXY biorefinery in 2025, supported by €21 million funding and EU circular economy mandates, alongside the fastest-growing food and flavors segment demanding natural ingredients, with Eastman launching high-purity grades in 2024.