- Advanced Materials

- Investment Casting Market

Investment Casting Market Size, Share, and Growth Forecast 2026 - 2033

Investment Casting Market by Material Type (Alumina-based: Tabular Alumina, White Fused Alumina, Calcined Alumina, Others; Zirconia-based: Fused Silica-based, Other Oxides, Non-Oxides; Others), Application (Aerospace & Defense, Automotive, Oil & Gas, Medical, Mechanical Engineering, Automation, Transportation, Others), and Regional Analysis for 2026 - 2033

Investment Casting Market Size and Trend Analysis

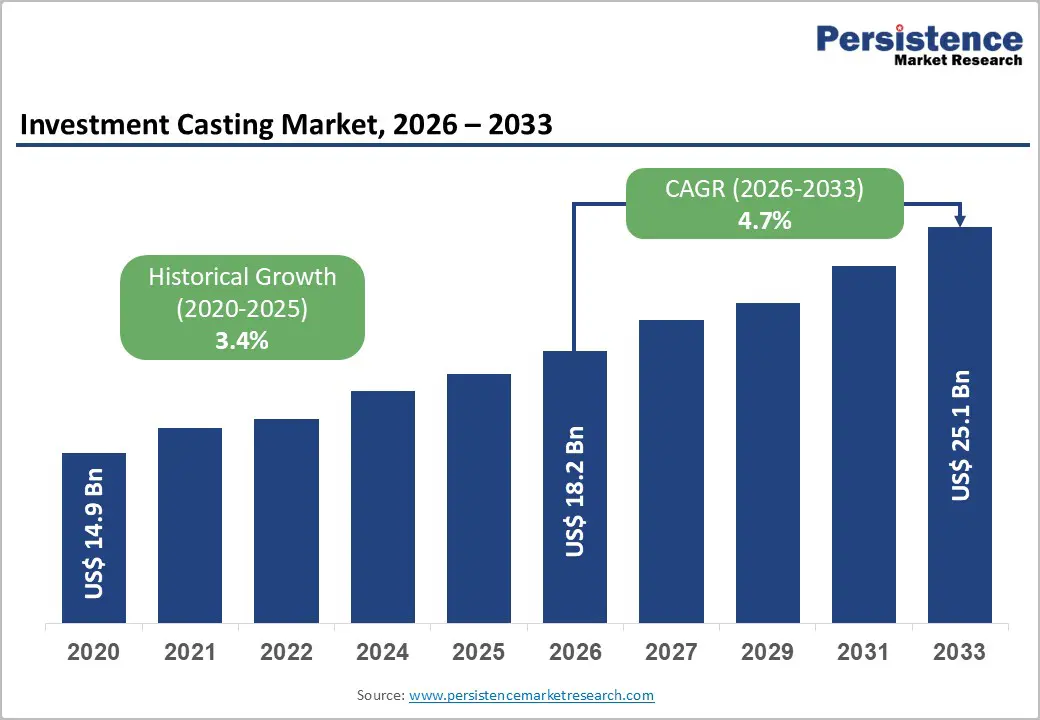

The global investment casting market size is valued at US$ 18.2 billion in 2026 and is projected to reach US$ 25.1 billion by 2033, growing at a CAGR of 4.7% between 2026 and 2033.

The market's steady expansion is primarily underpinned by accelerating aerospace fleet renewal programs and the automotive industry's transition to lightweight, precision-engineered components, both of which demand the unmatched geometric complexity and material versatility offered by the investment casting process. According to the Aerospace Industries Association (AIA), U.S. aerospace and defense exports totalled US$ 138.7 Bn between 2023 and 2024, signalling robust downstream procurement demand for investment cast parts.

Key Industry Highlights:

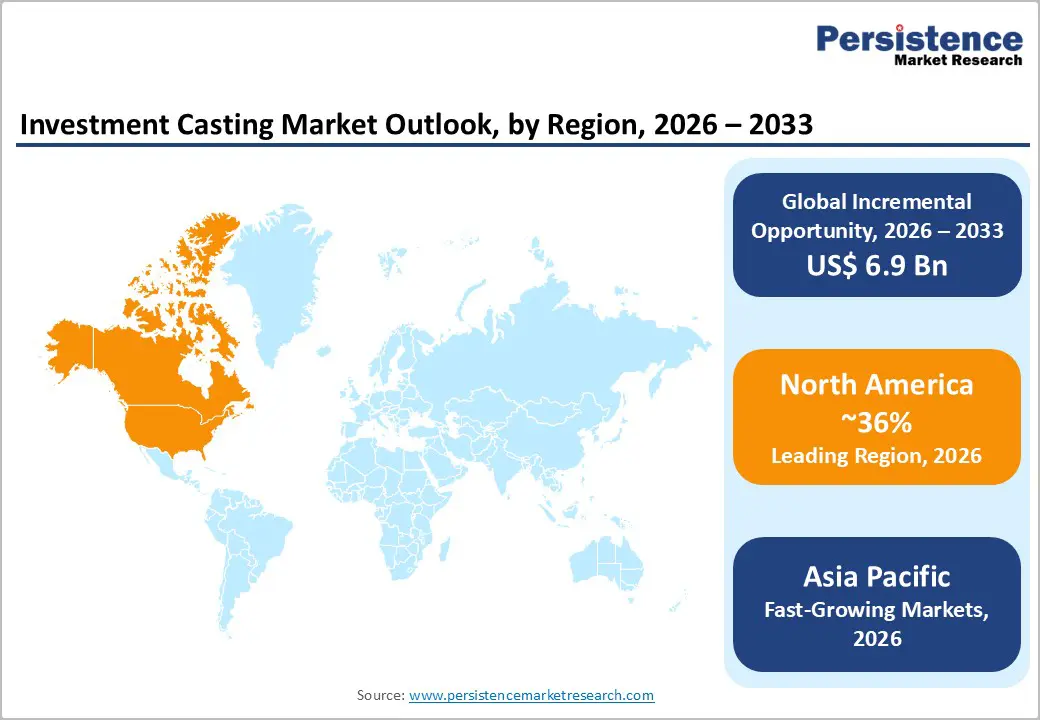

- Leading Region: North America leads the global Investment Casting market with approximately 36% share in 2025, underpinned by U.S. aerospace and defense exports of US$ 138.7 Bn and Precision Castparts Corp.'s dominant OEM supply position.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by China's 7.0% and India's defense budget expansion, the 'Make in India' initiative, and the region's 1,500+ active foundries scaling aerospace-grade casting capacity.

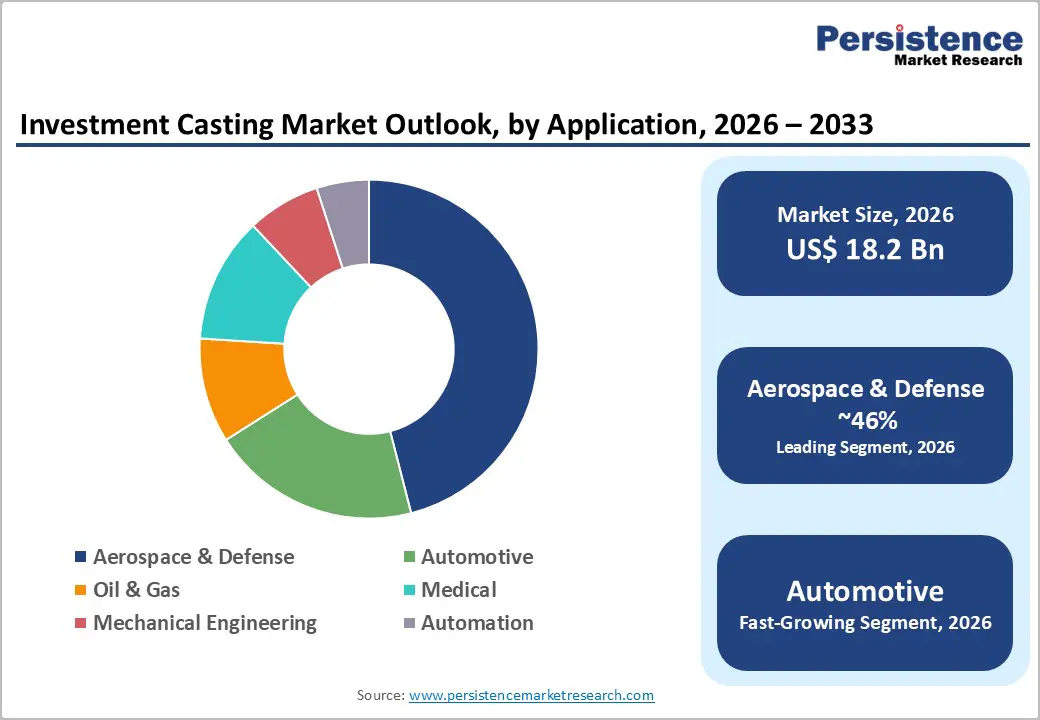

- Dominant Segment: Aerospace & Defense leads the Application category with approximately 46% revenue share, driven by mandatory use of investment casting for superalloy turbine blades and airfoil components across a global fleet of 28,400+ commercial aircraft.

- Fastest Growing Segment: The Medical application segment is the fastest growing end-use, fueled by rising global demand for precision titanium orthopaedic implants and the US$ 595 Bn medical device market, requiring investment casting's biocompatible, complex-geometry capabilities.

- Key Market Opportunity: Integration of additive manufacturing (3D printing) in wax pattern production exemplified by 3D Systems' QuickCast Air offering up to 70% material reduction and 30-50% efficiency gains represent the most transformative near-term growth opportunity.

| Key Insights | Details |

|---|---|

| Investment Casting Market Size (2026E) | US$ 18.2 Bn |

| Market Value Forecast (2033F) | US$ 25.1 Bn |

| Projected Growth CAGR (2026 - 2033) | 4.7% |

| Historical Market Growth (2020 - 2025) | 3.4% |

Market Dynamics

Drivers - Resurgent Aerospace Fleet Renewal and Defense Procurement Programs

The aerospace sector is the single largest demand engine for the investment casting market, and its post-pandemic resurgence is generating multi-year order backlogs at precision foundries worldwide. The global commercial aircraft fleet, estimated at approximately 28,400 active airliners in 2024, is projected to grow by roughly 28% over the following decade, creating persistent demand for turbine blades, structural castings, and hot-section air foil components that are exclusively manufactured via the investment casting process due to superalloy compatibility requirements. Precision Castparts Corp. (PCC), the market's foremost aerospace casting supplier, reported revenues of US$ 10.4 Bn in 2024a 15% revenue increase in H1 2024 compared to the prior year, validating the industry-wide expansion driven by Boeing and Airbus production rate increases.

Automotive Lightweighting Imperative and Electric Vehicle Transition

The global automotive industry's accelerating transition toward lighter, more fuel-efficient powertrains, particularly driven by the rapid adoption of electric vehicles (EVs)is creating substantial new demand streams for investment cast aluminum and titanium components. Global EV production reached approximately 17 million units in 2024, driven by surging adoption in China, the U.S., and Europe. Investment casting enables automakers to produce structurally complex, thin-walled components such as battery case brackets, gearbox housings, and suspension knuckles with minimal material waste and near-net-shape dimensional accuracy. GF Casting Solutions AG invested more than US$ 184 Mn in a new manufacturing facility in Augusta, Georgia in May 2024 to manufacture cast aluminum parts for EV platforms, directly signalling strong industrial confidence in automotive investment casting demand trajectories through 2033.

Restraints - High Tooling Costs and Extended Lead Times for Traditional Wax Patterns

A significant constraint limiting the investment casting market's penetration particularly among small-to-medium manufacturers and rapid-prototype development programs is the high upfront cost and protracted lead times associated with traditional injection-molded wax pattern tooling. Conventional injection Molds for wax patterns carry development costs ranging from US$ 5,000 to US$ 25,000 per die, with lead times extending approximately eight weeks before the first casting pattern can be produced. These barriers delay new product introduction cycles and increase total project costs, particularly for aerospace and medical applications that require frequent design iterations. For low-volume or customized production orders, these tooling economics significantly erode investment casting's cost competitiveness relative to emerging precision manufacturing alternatives.

Raw Material Price Volatility and Energy-Intensive Process Economics

The investment casting process is inherently dependent on high-purity specialty materials including nickel superalloys, titanium alloys, and ceramic shell materials, whose pricing is highly sensitive to geopolitical supply disruptions and global commodity market fluctuations. Nickel, a critical input for aerospace-grade investment castings, experienced price swings of approximately 40% between 2022 and 2024 on the London Metal Exchange (LME), directly compressing foundry margins. In addition, the ceramic shelling, dewaxing, and heat-treatment stages of the investment casting process carry high thermal energy demands, exposing manufacturers to electricity and gas price volatility. This cost structure places constant margin pressure on foundries, limiting capacity expansion investment and slowing market penetration in emerging economies where energy costs are less predictable.

Opportunities - Integration of Additive Manufacturing in Pattern Production

The growing convergence of additive manufacturing (AM) with traditional investment casting workflows represents one of the most transformative commercial opportunities in the market for the 2026-2033 forecast period. By replacing costly, time-consuming injection-molded wax patterns with 3D-printed photopolymer or castable wax patterns, foundries can eliminate tooling costs of US$ 5,000-US$ 25,000 per die and reduce pattern production lead times from weeks to hours. 3D Systems launched its QuickCast Air software tool in September 2024, enabling up to 70% reduction in pattern material consumption, significantly lowering burnout time and overall production cost. Industry data indicates that adoption of 3D-printed wax patterns can boost overall foundry efficiency by 30-50%.

Medical Device and Implant Manufacturing as a High-Growth End Market

The medical devices segment represents a rapidly expanding, premium-margin opportunity for investment casting manufacturers, driven by accelerating global demand for titanium orthopaedic implants, surgical instruments, and dental prosthetics that require both biocompatibility and intricate geometric precision. The global medical device market was valued at approximately US$ 595 Bn in 2025, according to the U.S. Food and Drug Administration (FDA) and industry census data, with orthopaedic implants representing one of the fastest-growing sub-segments. Investment casting offers unmatched compatibility with ASTM F1472-grade titanium alloys used in hip and knee implants, enabling complex porous surface geometries that promote osseointegration outcomes that are difficult to achieve through conventional machining. The aging demographics of North America, Western Europe, and Japan are ensuring compound annual growth in orthopaedic implant volumes, providing investment casting suppliers with durable, high-value demand independent of aerospace and automotive cyclicality.

Category-wise Analysis

Material Type Insights

The Alumina-based ceramic shell material segment dominates the investment casting material type category, accounting for approximately 58% of total market revenue. Alumina-based shells encompassing tabular alumina, white fused alumina, and calcined alumina are the industry standard for producing high-temperature investment casting Molds used in aerospace turbine airfoil and superalloy casting applications, owing to their exceptional refractoriness (melting points exceeding 2,000°C), high dimensional stability, and resistance to thermal shock during metal pouring. These properties are irreplaceable in the fabrication of jet engine hot-section components where shell dimensional accuracy directly impacts aerodynamic performance. Zirconia-based and fused silica-based materials are gaining traction in precision-tolerance medical and automotive casting applications that demand low thermal expansion coefficients and smoother cavity surfaces, representing the fastest-growing material sub-segment through 2033.

Application Insights

The Aerospace & Defense application segment is the clear market leader, commanding approximately 46% of the total investment casting market revenue. This dominance is structurally anchored by the aerospace industry's mandatory reliance on investment casting for producing turbine blades, structural fittings, and air foil components from nickel superalloys and titanium materials whose mechanical properties and microstructural integrity can only be achieved through the controlled solidification environment that investment casting provides. The global commercial aircraft fleet of approximately 28,400 active airliners in 2024, with projected 28% fleet expansion over the next decade, guarantees sustained multi-year procurement demand. Additionally, defense budget increases across NATO member states and the Indo-Pacific region are sustaining elevated procurement of investment cast engine and armament components, reinforcing the segment's leading position through the forecast period.

Regional Insights

North America Investment Casting Market Trends

North America holds the largest regional share of the global investment casting market, accounting for approximately 36% of total revenue, anchored by the world's most concentrated aerospace manufacturing ecosystem and robust defense spending. The U.S. aerospace and defense sector generated US$ 138.7 Bn in exports between 2023 and 2024 (Aerospace Industries Association), driving consistent demand for investment cast turbine blades, air foil castings, and structural components from foundries concentrated in Oregon, Connecticut, and Texas. Precision Castparts Corp.'s (PCC) revenue of US$ 10.4 Bn in 2024up 15% year-on-year in H1is the clearest single indicator of North America's investment casting demand leadership.

The innovation ecosystem is equally dynamic, with 3D Systems' introduction of the QuickCast Air digital pattern manufacturing tool in September 2024 and Form Technologies Inc.'s receipt of US$ 304 Mn in additional equity funding from Ares Management in January 2025 representing fresh capital flowing into U.S. precision casting capabilities.

Europe Investment Casting Market Trends

Europe represents the second-largest regional market for investment casting, with Germany, the United Kingdom, and France collectively forming the region's demand core. The European market benefits from a mature aerospace supply chain built around Airbus and Rolls-Royce engine programs that maintain consistent long-term procurement contracts with domestic investment casting foundries. ZOLLERN GmbH & Co. KG, headquartered in Germany, exemplifies the region's premium-grade casting capability for precision mechanical engineering, energy, and automotive applications.

European foundries are actively investing in additive-assisted pattern production and digital process control to align with EU Industrial Strategy 2030 sustainability and digital transformation mandates. The European Green Deal is additionally pushing foundries toward low-emission melting technologies and near-net-shape production strategies that inherently reduce waste, positioning investment casting favorably compared to machining-intensive alternatives.

Asia Pacific Investment Casting Trends

Asia Pacific is the fastest-growing regional market for investment casting and is simultaneously the largest by volume share accounting for approximately 30% of global revenue in 2025, underpinned by China's unparalleled foundry infrastructure of over 1,500 casting facilities serving automotive, aerospace, and industrial machinery customers. China and India registered defense budget increases of 7.0% and 1.6%, respectively, in 2024 (SIPRI), while India's 'Make in India' initiative is accelerating domestic precision manufacturing capacity building across aerospace, medical, and defense sectors.

Japan and South Korea are advancing high-technology casting niches including additive-assisted pattern creation and superalloy recycling, widening the region's technological depth. Impro Precision Industries reported increased aerospace and energy end-market revenue growth in its 2024 annual results, with capacity expansion underway at Mexico and China plants.

Competitive Landscape

The global investment casting market is moderately fragmented, with the top five players Precision Castparts Corp., Alcoa Corporation, Impro Precision Industries, MetalTek International, and ZOLLERN GmbH collectively accounting for an estimated 40% of global revenue. Market leaders differentiate through NADCAP and aerospace qualification certifications, proprietary superalloy formulations, and long-term OEM supply agreements. A large base of regional foundries particularly in China, India, and Eastern Europe competes on cost and throughput for automotive and general industrial volumes.

Key Developments:

- In December 2025, Hitchiner Manufacturing opened a new 57,000-square-foot Shared Services Operations facility at its Elm Street Campus in Milford, NH, expanding finishing and value-stream capabilities for aerospace, automotive, and defense investment casting customers.

- In September 2024, 3D Systems introduced QuickCast Air, an advanced software tool that reduces investment casting pattern material by up to 70%, cutting production costs and build time, particularly for large-format aerospace and defense casting patterns.

Companies Covered in Investment Casting Market

- Alcoa Corporation

- CIREX

- Dongying Giayoung Precision Metal Co., Ltd.

- Impro Precision Industries Limited

- JW CASTING

- MetalTek International

- Milwaukee Precision Casting

- Precision Castparts Corp.

- RLM Industries, Inc.

- Uni Deritend Ltd

- WANGUAN

- ZOLLERN GmbH & Co. KG

Frequently Asked Questions

The global Investment Casting market is valued at US$ 18.2 Bn in 2026 and is projected to reach US$ 25.1 Bn by 2033, expanding at a CAGR of 4.7%.

The key demand drivers include the resurgence of commercial aerospace fleet expansion with the global fleet of approximately 28,400 airliners projected to grow by 28% over the next decade combined with the rapid global transition to electric vehicles (17 million EV units produced in 2024) requiring lightweight precision aluminum and titanium castings.

The Aerospace & Defense segment is the dominant application, representing approximately 46% of total market revenue. Its leadership is structurally driven by the mandatory use of investment casting for superalloy turbine blades, airfoil castings, and structural fittings components that require the near-net-shape precision and high-temperature alloy compatibility that only investment casting delivers reliably at scale.

North America holds the largest regional share, accounting for approximately 36% of global revenue in 2025.

The key market participants include Precision Castparts Corp. (PCC), Alcoa Corporation, Impro Precision Industries Limited, MetalTek International, ZOLLERN GmbH & Co. KG, CIREX, Dongying Giayoung Precision Metal Co., Ltd., Milwaukee Precision Casting, RLM Industries, Inc., Uni Deritend Ltd, WANGUAN, JW CASTING, and regional leaders such as Hitchiner Manufacturing, Form Technologies, and GF Casting Solutions AG, among others.