- Inks, Coatings, Adhesives & Sealants (ICAS)

- Intumescent Coatings Market

Intumescent Coatings Market Size, Share, and Growth Forecast, 2026 - 2033

Intumescent Coatings Market by Product Type (Thin-Film, Thick-Film, Others), Substrate (Structural Steel & Cast Iron, Wood, Others), Composition, End-user, and Regional Analysis for 2026 - 2033

Intumescent Coatings Market Size and Trends Analysis

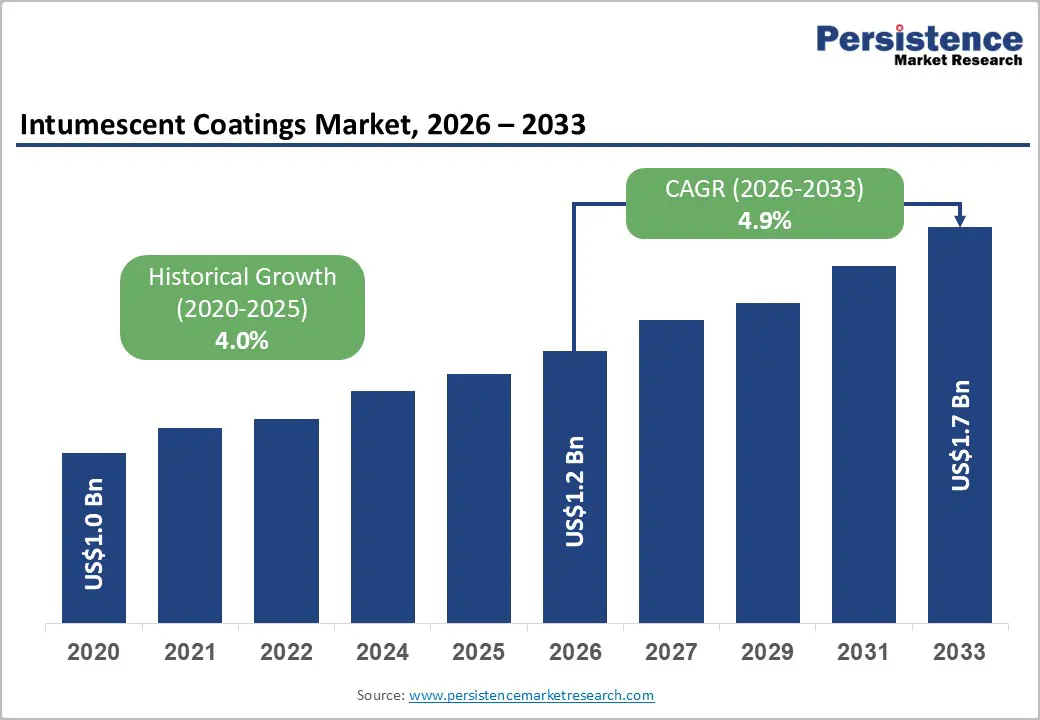

The global intumescent coatings market size is likely to be valued at US$ 1.2 billion in 2026 and is expected to reach US$ 1.7 billion by 2033, growing at a CAGR of 4.9% between 2026 and 2033, driven by stricter fire-safety regulations, increasing adoption of low-VOC formulations, and sustained demand for passive fire protection in steel-intensive construction and industrial assets. Growth remains steady and regulation-driven, with demand concentrated in projects requiring certified fire protection alongside aesthetic performance and efficient application.

Key Industry Highlights:

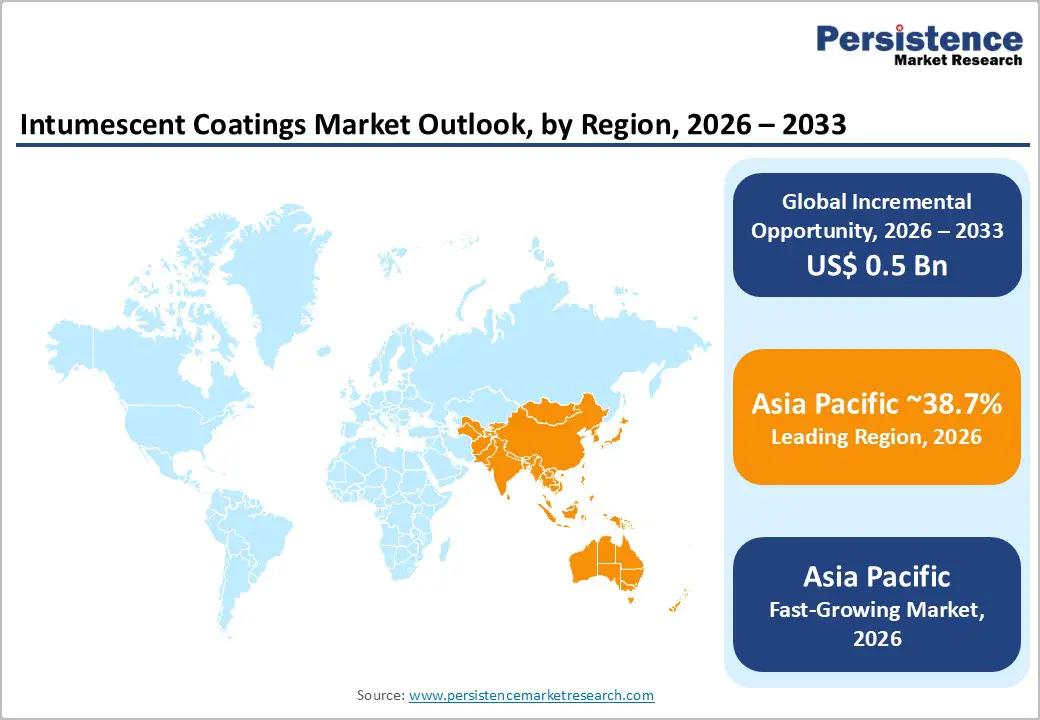

- Leading Region: Asia Pacific is projected to account for approximately 38.7% share, driven by large-scale infrastructure development, urbanization, and strong manufacturing capabilities across China, India, and Southeast Asia.

- Fastest-growing Region: Asia Pacific is also the fastest-growing region, supported by rapid industrialization, increasing construction of commercial and transportation infrastructure, and evolving fire-safety regulations that are accelerating adoption rates.

- Investment Plans: Industry investments are increasingly focused on low-VOC, water-based formulations and high-performance fire protection systems, with leading companies expanding product portfolios and regional manufacturing capabilities to support sustainable construction and energy infrastructure projects.

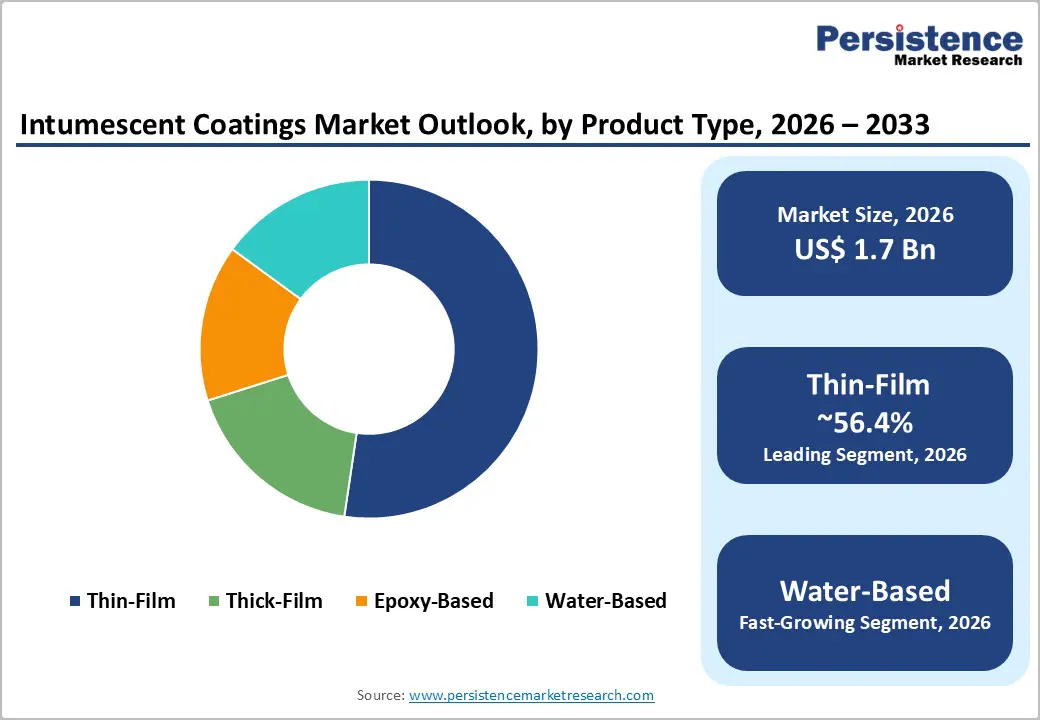

- Dominant Product Type: Thin-film coatings are anticipated to hold 56.4% market share, due to their ability to combine fire protection with aesthetic appeal and compatibility with modern architectural designs.

- Leading Substrate: Structural steel and cast iron dominate, accounting for an anticipated 57.9% share, as these materials require certified fire protection to maintain structural integrity in commercial buildings, industrial facilities, and infrastructure projects.

| Key Insights | Details |

|---|---|

| Intumescent Coatings Market Size (2026E) | US$1.2 Bn |

| Market Value Forecast (2033F) | US$1.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.0% |

Market Factors - Driver, Restraint, and Opportunity Analysis

Driver Analysis - Fire-Safety Regulations Driving Mandatory Adoption

Fire-safety regulations are transforming intumescent coatings from optional solutions into mandatory components in construction and industrial projects. Regulatory frameworks across developed markets emphasize fire resistance in structural materials, particularly steel, which loses strength rapidly under high temperatures. Standardized fire testing protocols such as UL 263, ASTM E119, and EN 13381-8 have become critical benchmarks for product approval and specification. This regulatory tightening directly expands market demand, as coatings are now integrated at the design stage rather than applied post-construction. Compliance-driven adoption is particularly strong in commercial buildings, transportation infrastructure, and industrial facilities. As regulatory enforcement intensifies globally, manufacturers with certified, tested, and compliant systems are gaining a competitive advantage.

Growing Demand for Low-VOC and Water-Based Coatings

Environmental regulations targeting volatile organic compound (VOC) emissions are accelerating the transition toward water-based and low-emission intumescent coatings. Regulatory limits on VOC content in architectural coatings are pushing manufacturers to reformulate products without compromising fire performance. Water-based systems are gaining traction due to their ease of application, lower environmental impact, and suitability for indoor use. These coatings also support faster project timelines by enabling simplified logistics and reduced health and safety concerns during application. The shift is particularly evident in urban construction and refurbishment projects, where sustainability standards and indoor air quality considerations are increasingly prioritized.

Expansion of Construction and Industrial Infrastructure

Global urbanization and infrastructure development continue to drive demand for intumescent coatings. Increasing investments in commercial buildings, transport hubs, industrial plants, and energy infrastructure are expanding the installed base of steel structures requiring passive fire protection. Large-scale infrastructure projects, including airports, metro systems, and high-rise developments, rely heavily on structural steel, making fire protection essential for regulatory compliance and safety assurance. Industrial sectors such as oil & gas and power generation further contribute to demand, as asset protection and risk mitigation remain critical priorities. This sustained expansion of construction and industrial activity provides a consistent demand pipeline for intumescent coatings.

Restraint Analysis - High Installation and System Costs

The cost of intumescent coatings remains a key barrier, particularly in price-sensitive markets. These systems require multiple layers, including primers, intumescent coatings, and topcoats, along with certified application processes and skilled labor. This increases total project costs compared to alternative fireproofing solutions such as cementitious coatings or fire-resistant boards. Cost sensitivity is especially pronounced in smaller construction projects and retrofit applications, where budget constraints may lead to the selection of lower-cost alternatives. While intumescent coatings offer superior aesthetics and performance, their higher upfront cost can limit adoption in certain segments.

Complex Certification and Testing Requirements

The performance of intumescent coatings depends on precise application thickness, substrate compatibility, and environmental conditions. As a result, extensive testing and certification are required to validate fire resistance under different scenarios. This complexity can delay project timelines, as coatings must meet specific regulatory standards and pass rigorous testing procedures. Variations in regional certification requirements further increase the burden on manufacturers, who must adapt formulations and testing protocols for different markets. These challenges increase operational costs and create barriers for new entrants.

Opportunity Analysis - Growth in Oil & Gas and Petrochemical Applications

Hydrocarbon fire protection represents a high-value opportunity within the intumescent coatings market. Industrial environments such as oil refineries, offshore platforms, and petrochemical plants require specialized coatings capable of withstanding rapid temperature increases associated with hydrocarbon fires. These applications demand high-performance coatings with advanced certification, allowing manufacturers to command premium pricing. Continued investments in energy infrastructure, including LNG facilities and petrochemical complexes, are expected to sustain demand for hydrocarbon-resistant intumescent coatings.

Development of High-Efficiency Application Systems

Advancements in coating technology are enabling reduced film thickness, faster drying times, and simplified application processes. These innovations help reduce labor costs, shorten project timelines, and improve overall efficiency. Contractors increasingly prioritize coatings that can be applied using standard equipment and require fewer layers or rework. This shift creates opportunities for manufacturers to differentiate through performance efficiency rather than price alone. Products that deliver both fire protection and installation efficiency are likely to gain strong market traction.

Rising Demand for Aesthetic Fire Protection Solutions

Architectural trends favor exposed structural elements, particularly in commercial and public buildings. Intumescent coatings enable fire protection without compromising visual appeal, making them ideal for applications where design and safety must coexist. This trend is driving demand for thin-film coatings that maintain smooth finishes and support decorative applications. As modular construction and prefabrication gain momentum, coatings that combine aesthetics, certification, and ease of application will play a critical role in project specifications.

Category-wise Analysis

Product Type Insights

Thin-film coatings are expected to dominate the market, accounting for an anticipated 56.4% share in 2026. Their popularity stems from their ability to provide effective fire protection while maintaining the visual appearance of structural steel. These coatings are widely used in commercial buildings, transport infrastructure, airports, and high-rise construction, where aesthetics are important. Their compatibility with modern architectural designs, such as exposed steel frameworks in office towers, stadiums, and transit terminals, combined with relatively lower application thickness, supports their widespread adoption. In practice, thin-film systems are often specified in premium commercial projects where both fire ratings and architectural finishes must be achieved without adding bulk or weight to the structure.

Water-based coatings are likely to be the fastest-growing segment, with an anticipated above-market growth rate. This growth is driven by tightening environmental regulations and rising demand for sustainable construction materials. These systems offer low VOC emissions, improved indoor air quality, and easier handling during application, making them particularly suitable for enclosed environments such as offices, hospitals, and data centers. For example, water-based intumescent coatings are increasingly used in urban redevelopment and refurbishment projects where ventilation constraints and safety standards are strict. As green building certifications and sustainability targets become central to procurement decisions, water-based systems are expected to gain a progressively larger share of the market.

Substrate Insights

Structural steel and cast iron are anticipated to remain the dominant substrates, accounting for an anticipated 57.9% market share in 2026. Steel structures require fire protection to maintain load-bearing capacity during fire exposure, making intumescent coatings a critical component in construction and industrial applications. Their widespread use in commercial buildings, bridges, industrial plants, and transport infrastructure reinforces their leading position. For instance, intumescent coatings are routinely applied to steel beams and columns in high-rise office buildings, airports, and metro rail systems to meet fire-resistance ratings while preserving structural integrity. The continued expansion of steel-intensive infrastructure globally ensures sustained demand in this segment.

Wood substrates are emerging as a fast-growing segment, with an anticipated above-average growth rate. This trend is driven by the increasing adoption of engineered timber, including cross-laminated timber (CLT), in modern construction. Intumescent coatings enable wood to meet fire-safety standards while maintaining its natural appearance, making them ideal for applications such as hotels, schools, heritage restorations, and premium residential interiors. For example, timber-based commercial buildings and modular housing projects increasingly incorporate intumescent coatings to comply with fire regulations without compromising design aesthetics. The shift toward sustainable and low-carbon building materials is expected to further accelerate growth in this segment.

Regional Insights

North America Intumescent Coatings Market Trends - Certification-Driven Demand & Low-VOC Innovation in Structural Fire Protection

North America accounts for a significant share of the global market, supported by strong construction activity and stringent fire-safety regulations. The U.S. leads the region, with a well-established regulatory framework and high adoption of certified fire protection systems. Standards such as UL 263 and ASTM E119 are widely enforced, ensuring that only rigorously tested intumescent coatings are specified in major projects. This regulatory consistency has created a mature and quality-driven market environment where performance and certification are key purchasing criteria.

Demand is driven by commercial construction, industrial facilities, and infrastructure upgrades. The region also benefits from a strong focus on testing standards and product certification, which supports the adoption of high-performance coatings. Recent developments highlight this trend, for example, PPG launched Steelguard 652 in 2026, a water-based intumescent coating tailored for interior structural steel, reinforcing the shift toward low-VOC and easy-to-apply systems. Similarly, The Sherwin-Williams Company continues expanding its FIRETEX range, focusing on faster curing and reduced film thickness to improve application efficiency. Retrofit projects, data centers, and logistics hubs are emerging as key growth areas, as asset owners prioritize fire safety, compliance, and operational continuity in high-value infrastructure.

Europe Intumescent Coatings Market Trends - CPR-Regulated Market with Sustainability-Led Coating Innovation

Europe is characterized by a highly regulated environment and a strong emphasis on environmental sustainability. The region demonstrates steady growth, supported by harmonized construction standards and strict fire-safety requirements under frameworks such as the Construction Products Regulation (CPR). This regulatory alignment ensures consistent product performance standards across countries, making Europe one of the most technically advanced markets for intumescent coatings.

Key markets include Germany, the U.K., France, and Spain, where construction activity and regulatory enforcement remain strong. The adoption of water-based coatings is particularly high, driven by environmental regulations and sustainability initiatives. Recent product innovation reflects this shift, for instance, AkzoNobel introduced Chartek ONE in 2025, a next-generation hydrocarbon fire protection coating designed to improve durability while reducing environmental impact. Similarly, Hempel launched Hempafire Extreme 550, targeting both performance efficiency and compliance with evolving fire standards. Investment trends increasingly focus on certified systems, off-site application methods, and solutions that reduce labor costs and improve installation speed, particularly in complex infrastructure and commercial developments.

Asia Pacific Intumescent Coatings Market Trends - Infrastructure-Led Growth & Rapid Adoption in Steel-Intensive Construction

Asia Pacific is projected to lead the market with approximately 38.7% share in 2026, and is the fastest-growing region. Rapid urbanization, large-scale infrastructure projects, and expanding industrial activity drive demand across China, India, Japan, and Southeast Asia. Governments across the region are investing heavily in transport networks, smart cities, and industrial corridors, all of which rely on steel-intensive construction requiring passive fire protection.

The region benefits from strong manufacturing capabilities and cost advantages, enabling large-scale production and adoption of intumescent coatings. Growth is supported by increasing construction of commercial buildings, transportation infrastructure, and industrial facilities. For example, Jotun expanded its fire protection portfolio with Jotachar 1709 XT in 2025, targeting oil & gas and energy infrastructure projects across Asia, where hydrocarbon fire risks are significant. Kansai Paint continues to strengthen its presence in industrial and protective coatings, supporting regional demand through localized production and distribution. As regulatory frameworks continue to evolve, particularly in India and Southeast Asia, there is a growing emphasis on certified fire protection systems, which is expected to further accelerate adoption and reinforce the region’s leadership position.

Competitive Landscape

The global intumescent coatings market is moderately fragmented, with a mix of global leaders and regional players. A group of multinational companies dominates the premium segment, offering certified, high-performance solutions supported by technical expertise and strong distribution networks. Smaller players and niche manufacturers compete in regional markets and specialized applications. Competitive positioning is largely determined by product certification, performance reliability, and technical support capabilities. Barriers to entry remain high due to stringent testing requirements and regulatory compliance. Key players are focusing on innovation, regulatory compliance, and application efficiency. Strategies include developing low-VOC formulations, expanding product portfolios, and enhancing technical service capabilities. Companies are also investing in faster application technologies and integrated solutions to improve project economics and strengthen competitive positioning.

Key Industry Developments

- In March 2025, Hempel A/S announced the launch of Hempafire Extreme 550, an advanced epoxy-based passive fire protection coating designed for structural steel exposed to cellulosic fire conditions, aimed at improving fire resistance performance in commercial and infrastructure applications.

- In July 2025, AkzoNobel introduced Chartek ONE, a next-generation boron-free intumescent coating developed for hydrocarbon fire protection in oil & gas and petrochemical facilities, strengthening its sustainable product portfolio while enhancing durability and performance in extreme environments.

- In November 2025, Jotun launched Jotachar 1709 XT, a high-performance intumescent coating optimized for hydrocarbon fire scenarios in oil & gas assets, focusing on improved application efficiency, reduced material usage, and enhanced fire protection reliability.

Companies Covered in Intumescent Coatings Market

- The Sherwin-Williams Company

- PPG Industries, Inc.

- Akzo Nobel N.V.

- Jotun Group

- Hempel A/S

- Carboline Company

- Sika AG

- Promat International (Etex Group)

- Teknos Group Oy

- Kansai Paint Co., Ltd.

- Isolatek International

- Nullifire (Tremco CPG Europe)

- Albi Protective Coatings

- Flame Control Coatings, LLC

- No-Burn, Inc.

- Contego International Inc.

Frequently Asked Questions

The global intumescent coatings market is estimated to be valued at US$1.2 billion in 2026.

The market is projected to reach US$1.7 billion by 2033.

Key trends include the growing adoption of low-VOC and water-based coatings, increasing integration of fire protection in early-stage building design, and rising demand for aesthetic thin-film coatings in modern infrastructure projects.

Thin-film coatings lead the intumescent coatings market, accounting for an anticipated 56.4% share, driven by their ability to combine fire protection with architectural aesthetics.

The intumescent coatings market is expected to grow at a CAGR of 4.9% from 2026 to 2033.

Major players include The Sherwin-Williams Company, PPG Industries, Inc., Akzo Nobel N.V., Jotun Group, and Hempel A/S.