- Home Appliances

- Intruder Alarms Market

Intruder Alarms Market Size, Share, and Growth Forecast, 2025 - 2032

Intruder Alarms Market By Product Type (Wired Alarm, Wireless Alarm, Hybrid Alarm), Component (Alarm Sensors, RTU, Central Monitoring Receiver, Others), Application and Regional Analysis for 2025 – 2032

Intruder Alarms Market Size and Trends Analysis

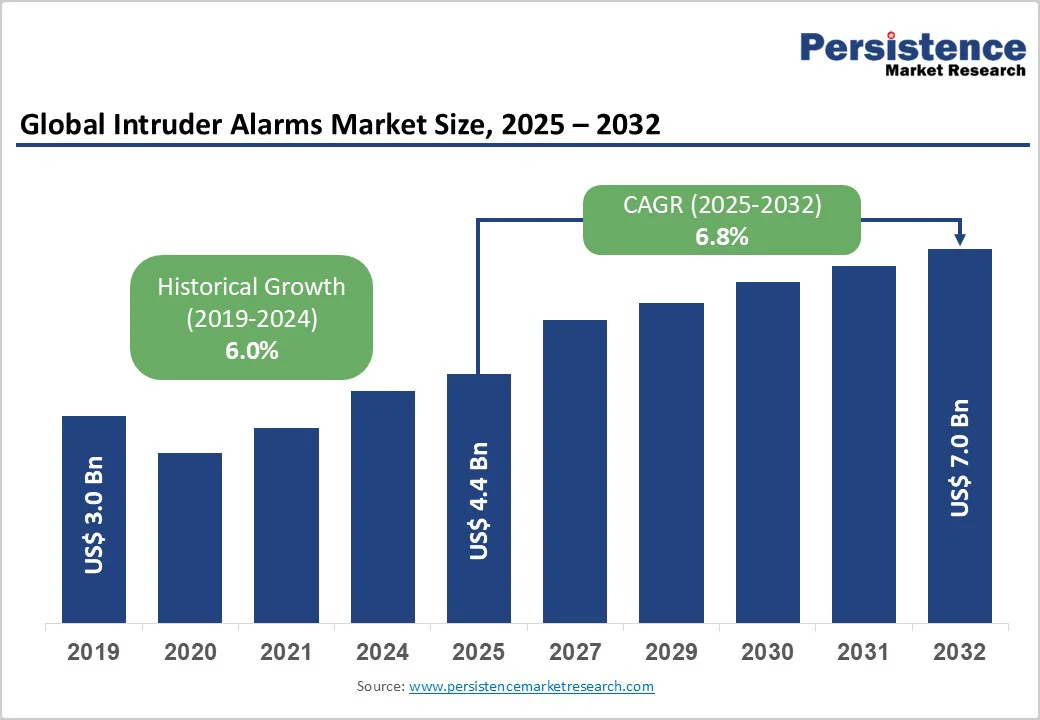

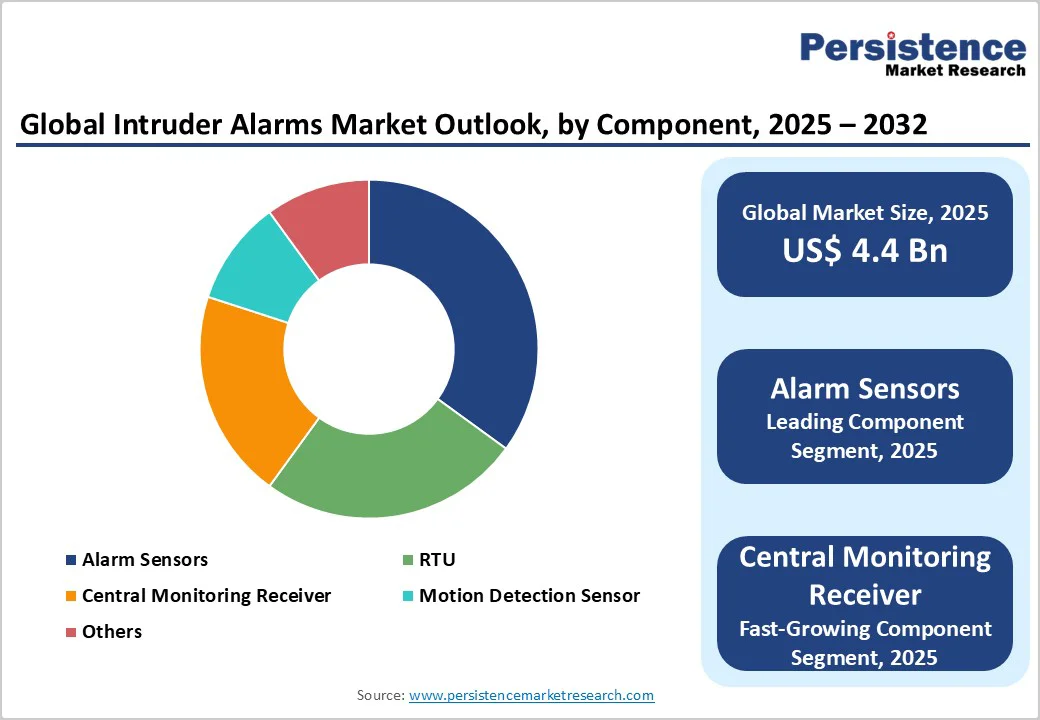

The global intruder alarms market size is likely to be valued US$4.4 Biliion in 2025, projected to reach US$7.0 Billion by 2032, growing at a CAGR of 6.8% during the forecast period from 2025 to 2032. The market is experiencing robust growth driven by increasing security concerns, rising adoption of smart home technologies, and advancements in wireless and hybrid alarm systems.

The market is further propelled by innovations in AI-integrated sensors and IoT-enabled monitoring, catering to preferences for seamless and remote-accessible security solutions. The growing acceptance of intruder alarms as essential components of modern safety ecosystems, especially with the integration of central monitoring receivers, is a key growth factor.

Key Industry Highlights:

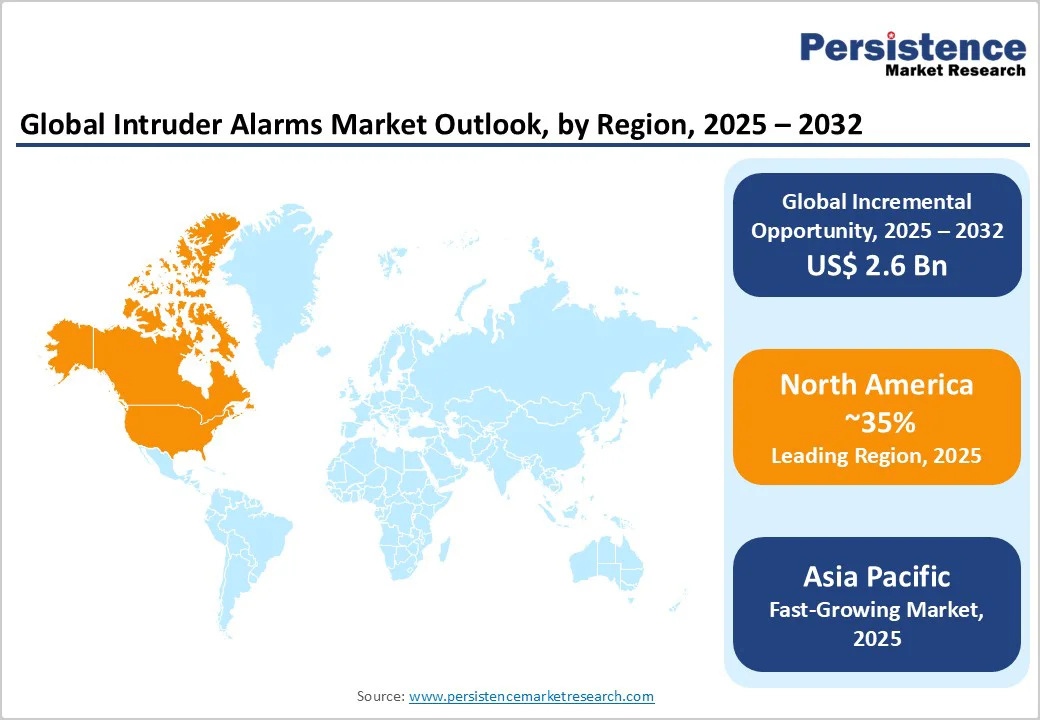

- Leading Region: North America, commanding a 35% market share in 2025, driven by advanced smart home adoption and stringent security regulations in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by rapid urbanization, rising crime rates, and infrastructure development in China and India.

- Dominant Product Type: Wireless Alarm, holding approximately 40% of the market share, due to its ease of installation and flexibility in modern homes.

- Leading Component: Alarm Sensors, accounting for over 30% of market revenue, driven by demand for motion detection and perimeter security.

- Leading Application: Residential, contributing nearly 45% of market revenue, owing to homeowners focus on personal safety.

- Key Market Driver: Increasing incidents of theft, burglary, and property crime are driving the adoption of advanced intruder alarm systems across residential, commercial, and industrial sectors.

- Growth Opportunity: Expansion in hybrid systems with AI for predictive threat detection, enhancing commercial applications.

| Key Insights | Details |

|---|---|

|

Intruder Alarms Market Size (2025E) |

US$4.4 Bn |

|

Market Value Forecast (2032F) |

US$7.0 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Increasing Security Concerns and Smart Home Integration

Increasing security concerns and the rapid adoption of smart home technologies are major factors driving growth in the intruder alarms market. Rising incidents of burglary, theft, and property damage have heightened awareness about personal and asset protection, prompting both homeowners and businesses to invest in reliable alarm systems. Consumers now seek intelligent security solutions that not only detect intrusions but also offer real-time alerts, remote monitoring, and automated responses to potential threats.

Smart home integration has further transformed the landscape by making intruder alarms more accessible, connected, and user-friendly. Modern systems can seamlessly connect with IoT devices such as smart locks, cameras, and lighting systems through mobile apps or voice assistants. This interconnected ecosystem enables users to monitor their property remotely, receive instant notifications, and control their security setup effortlessly. Advancements in AI and cloud-based technologies enhance system efficiency by reducing false alarms and improving predictive threat analysis.

High Installation and Maintenance Costs

High installation and maintenance costs remain a major challenge in the intruder alarms market, limiting adoption, particularly among small businesses and price-sensitive consumers. Advanced alarm systems, especially those integrated with AI, Internet of Things (IoT), and hybrid technologies, often require specialized equipment, professional installation, and complex wiring. These factors significantly increase upfront expenses compared to conventional security systems. Additionally, the need for skilled technicians to ensure proper configuration and integration with other devices further adds to costs.

Maintenance expenses also contribute to the overall burden, as systems require regular software updates, battery replacements, and performance testing to maintain reliability and prevent false alarms. In commercial and industrial settings, large-scale installations may involve additional costs for centralized monitoring, data storage, and system upgrades.

Expansion in AI and IoT-Enabled Hybrid Systems

The intruder alarms market is witnessing significant expansion through the integration of AI and IoT-enabled hybrid systems, reflecting a shift toward intelligent, connected security solutions. AI technologies enhance alarm systems by enabling advanced threat detection, behavioral analysis, and predictive monitoring. These systems can differentiate between false alarms and genuine security breaches, allowing for more accurate and timely alerts. AI also facilitates automated decision-making, such as triggering cameras, contacting security personnel, or notifying homeowners in real time, improving overall responsiveness, and reducing human intervention.

IoT-enabled hybrid systems combine the reliability of traditional wired alarms with the flexibility of wireless devices, creating a versatile security network suitable for both residential and commercial applications. By connecting sensors, cameras, control panels, and mobile applications, these systems allow remote monitoring, data sharing, and centralized management. Users can access real-time security updates from anywhere, control devices through smartphones, and integrate alarms with broader smart home or building automation platforms.

Category-wise Analysis

Product Type Insights

Wireless Alarm dominates the market, accounting for 40% of the share in 2025. Their popularity stems from easy installation, flexible scalability, and seamless integration with smart home systems. Homeowners and businesses favor wireless solutions for their convenience, adaptability, and ability to expand coverage without extensive wiring, making them a preferred choice for modern, technology-driven security setups.

Hybrid Alarm is the fastest-growing segment, driven by rising demand for integrated wired and wireless solutions. These systems offer flexibility, scalability, and seamless connectivity, allowing users to combine the reliability of wired setups with the convenience of wireless technology. Their adaptability makes them ideal for both new installations and retrofitting existing security systems.

Component Insights

Alarm sensors lead with 30% share, driven by the growing need for perimeter and motion detection in residential security. Homeowners increasingly rely on these sensors to detect unauthorized entry, monitor vulnerable areas, and trigger timely alerts. Their effectiveness, ease of installation, and compatibility with smart home systems make them a preferred choice for safeguarding properties.

Central monitoring receiver is the fastest-growing, driven by the demand for remote access and professional surveillance in commercial settings. Businesses increasingly rely on centralized monitoring to oversee multiple sites, receive real-time alerts, and coordinate rapid responses. This ensures enhanced security, operational efficiency, and seamless integration with advanced alarm and surveillance systems.

Application Insights

Residential holds nearly 45% share, fueled by homeowners increasingly adopting DIY alarm systems and app-controlled solutions that offer convenience, affordability, and real-time monitoring. Rising awareness of home security, coupled with smart home integration, encourages users to install flexible, easy-to-manage systems, making residential spaces safer and more connected.

Commercial & Industrial is the fastest-growing, driven by enterprises upgrading security infrastructure to protect assets, sensitive data, and personnel. Rising concerns over theft, vandalism, and workplace safety are prompting businesses to adopt advanced alarm systems, including AI-enabled monitoring and integrated solutions, ensuring robust, scalable, and real-time protection across large facilities and complex operations.

Regional Insights

North America Intruder Alarms Market Trends

North America accounts for 35% in 2025, driven by the high penetration of smart home technologies in the U.S., where homeowners increasingly adopt connected devices, including intruder alarms, to enhance residential security. Rising property crime rates across urban and suburban areas further accelerate demand for reliable and responsive security systems. Smart intruder alarms, integrated with mobile apps, AI-based monitoring, and IoT-enabled devices, allow users to detect unauthorized entry, receive real-time alerts, and control security systems remotely, making them a preferred choice among consumers.

While the U.K. is part of Europe, its market dynamics resemble North American trends. Wireless alarm systems in the U.K. are witnessing robust growth, expanding at around 25%, driven by Home Office initiatives promoting safer residential and commercial environments. Additionally, the urban population’s preference for flexible, hybrid alarm systems combining wireless and wired solutions supports the adoption of advanced security technologies.

Europe Intruder Alarms Market Trends

Europe holds about 30% market share, led by driven by stringent regulatory frameworks, high technological adoption, and a mature security ecosystem across the continent. Germany and France are leading contributors, owing to their well-established infrastructure, high urbanization, and strong emphasis on safety and security standards. EU data protection regulations, such as the General Data Protection Regulation (GDPR), play a crucial role by encouraging the adoption of secure, reliable alarm systems that ensure compliance while protecting sensitive data.

Commercial buildings in Europe increasingly rely on centralized monitoring systems, which integrate intruder alarms with video surveillance, access control, and other security solutions. This integration allows facility managers to monitor multiple sites in real time, respond promptly to incidents, and optimize security operations efficiently. High consumer awareness, advanced technological penetration, and the preference for premium security solutions further strengthen the region’s market position.

Asia Pacific Intruder Alarms Market Trends

Asia Pacific commands around 25% share and is the fastest-growing region, driven by a combination of technological initiatives, urbanization, and increasing security awareness across both residential and commercial sectors. In China, large-scale smart city projects are playing a pivotal role in boosting demand for advanced security systems, including intruder alarms. These initiatives aim to integrate IoT, AI, and cloud-based monitoring solutions, creating intelligent urban environments where safety and surveillance are critical priorities.

Meanwhile, India is witnessing rapid urban migration, with millions moving to cities in search of better employment and lifestyle opportunities. This surge in urban population has increased the need for cost-effective and easily deployable security solutions, making intruder alarms a necessity for both new residential complexes and commercial establishments. The rising concerns around property theft, burglary, and workplace security further amplify the demand.

Competitive Landscape

The global intruder alarms market is highly competitive, with key players focusing on AI integration, hybrid solutions, and e-commerce expansion to meet security demands. This AI integration not only improves system accuracy but also enables real-time alerts and remote monitoring, making security management more efficient. Another significant trend is the development of hybrid solutions that combine traditional wired systems with wireless technologies. These hybrid systems offer flexibility, scalability, and easier installation, appealing to both new installations and retrofit projects.

Hybrid solutions can integrate with other smart home or building management systems, providing a comprehensive security ecosystem. To expand market reach, leading companies are also investing heavily in e-commerce platforms, enabling faster and wider distribution of alarm systems globally. Online channels facilitate direct engagement with end-users, reduce reliance on intermediaries, and offer convenient purchasing options.

Key Developments

- In June 2025, Honeywell announced the launch of Honeywell Connected Solutions, an AI-powered platform that integrates critical building software and technologies into a single interface to help enable more efficient operations. The platform's early adopters – Verizon Communications Inc. and Vanderbilt University have already begun using the solution in their buildings.

- In May 2025, ADT launched its ADT+ platform featuring deeper integration with Google Nest devices, a new hardware line, and the Trusted Neighbor™ feature. Also introduced is the ADT Self-Setup system for DIY customers, combining ADT's monitoring with Google Nest smart home products.

Companies Covered in Intruder Alarms Market

- Godrej & Boyce Mfg. Co. Ltd

- Johnson Controls

- Robert Bosch GmbH

- Honeywell International Inc.

- ADT

- Assa Abloy Group

- Hangzhou Hikvision Digital Technology Co., Ltd.

- Banham Group

- Securitas AB

- Risco Group

- Napco Security Technologies

- Others

Frequently Asked Questions

The global intruder alarms market is projected to reach US$4.4 Bn in 2025, driven by rising security concerns and smart home integration.

The market is driven by 30% rise in urban burglaries and smart home growth to 1 biilion devices by 2030, necessitating advanced intruder alarms.

The market is poised to witness a CAGR of 6.8% from 2025 to 2032, supported by AI and IoT innovations.

Expansion in AI-hybrid intruder alarms for predictive security offers opportunities in commercial and residential sectors.

Honeywell, Johnson Controls, Bosch, ADT, and Hikvision lead through Intruder Alarms innovations in wireless and AI systems.