- Industrial Machinery

- Industrial Motor Market

Industrial Motor Market Size, Share, and Growth Forecast 2026 - 2033

Industrial Motor Market by Motor Type (AC Motors (Induction Motors, Synchronous Motors), DC Motors (Brushed DC Motors, Brushless DC Motors (BLDC)), Servo Motors, Stepper Motors), by Voltage (Low Voltage Motors (<1 kV), Medium Voltage Motors (1 kV - 6.6 kV), High Voltage Motors (>6.6 kV)), by Power Output, by End-Use Industry, by Regional Analysis, 2026 - 2033

Industrial Motor Market Size and Trend Analysis

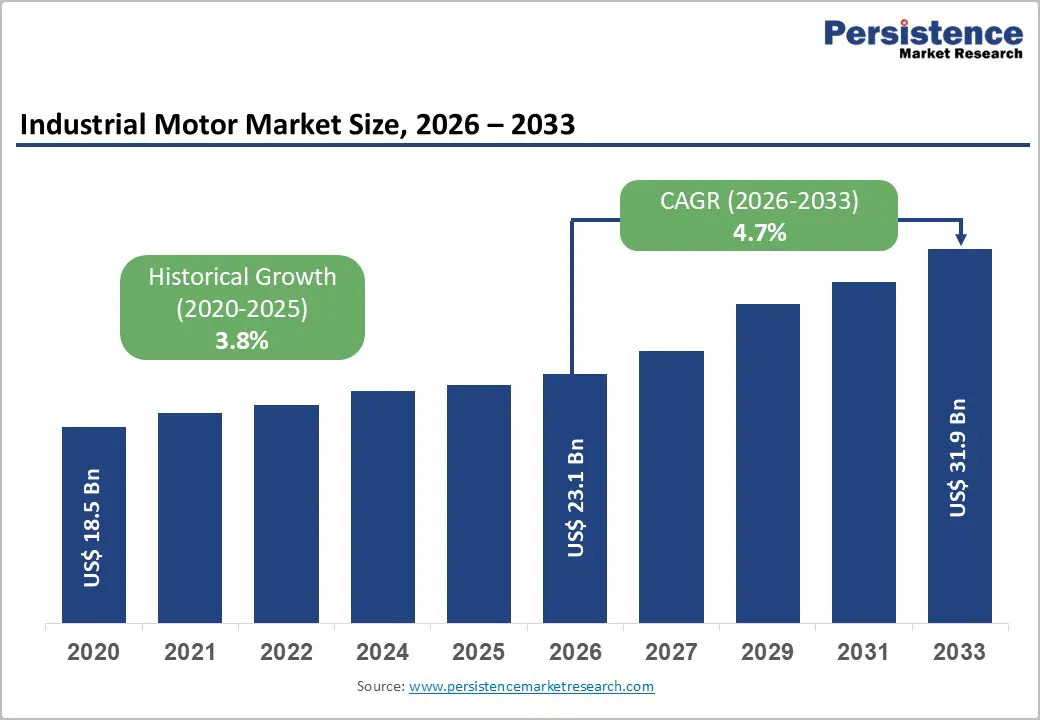

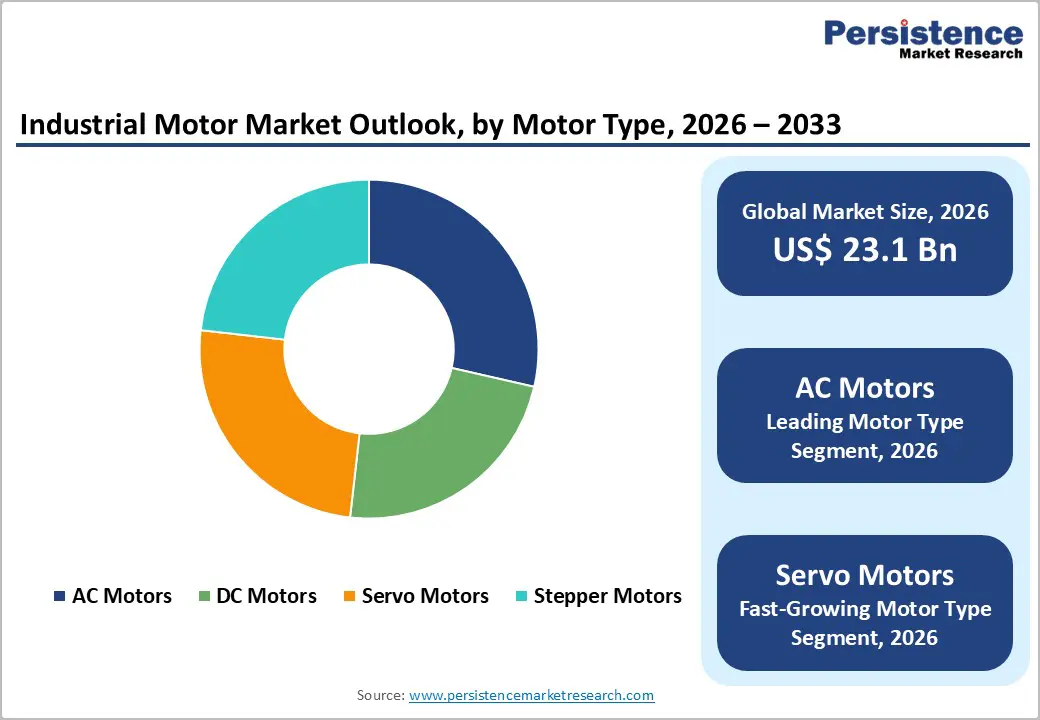

The global industrial motor market size is expected to be valued at US$ 23.1 billion in 2026 and projected to reach US$ 31.9 billion by 2033, growing at a CAGR of 4.7% between 2026 and 2033. Industrial motors are witnessing strong demand driven by rapid industrialization and the growing emphasis on energy efficiency across sectors.

Rising manufacturing activities and strict energy regulations are accelerating the adoption of high-efficiency motors. Electric motors account for nearly half of global electricity consumption, encouraging industries to upgrade systems. Additionally, increasing automation and adoption of Industry 4.0 are boosting demand for smart, connected motor solutions.

Key Industry Highlights:

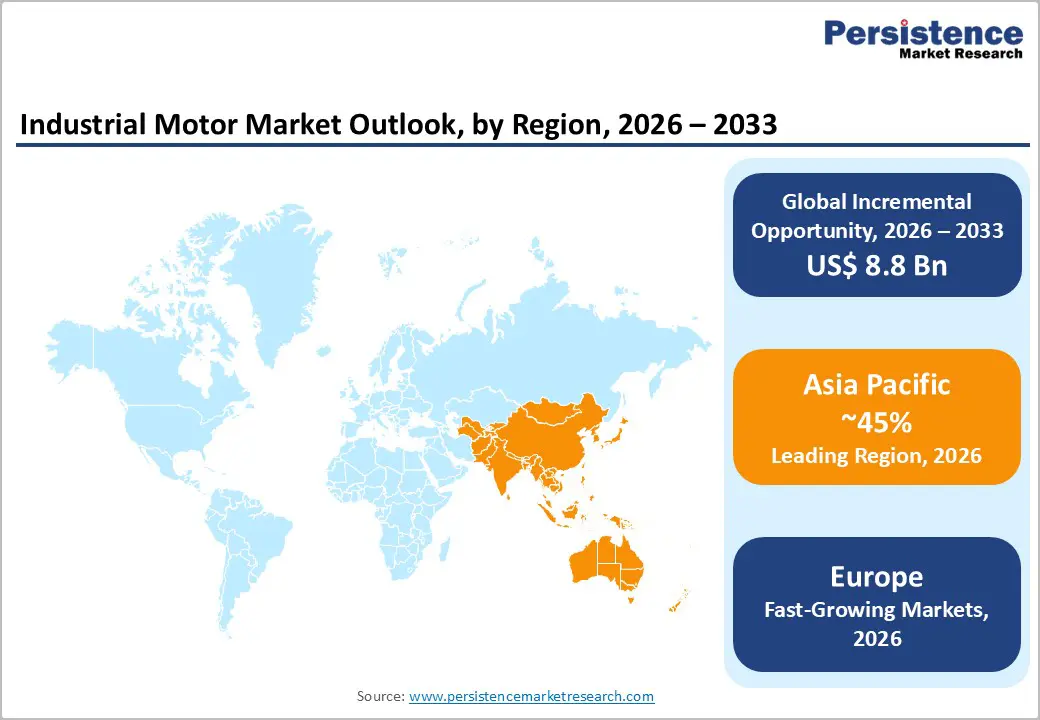

- Leading Region: Asia Pacific leads the market with a 45% share in 2025, driven by strong manufacturing activity across China and India.

- Fastest Growing Region: Europe emerges as the fastest-growing region, supported by stringent energy efficiency regulations and industrial modernization.

- Leading Category: AC Motors dominate with a 65% share, owing to their reliability and widespread use in industrial applications.

- Fastest Growing Category: Servo Motors are the fastest-growing segment, driven by rising demand for precision and automation across industries.

- Key Market Opportunity: Smart IoT-enabled motors present a major opportunity by enabling predictive maintenance and improving operational efficiency.

| Key Insights | Details |

|---|---|

| Industrial Motor Size (2026E) | US$ 23.1 billion |

| Market Value Forecast (2033F) | US$ 31.9 billion |

| Projected Growth CAGR (2026 - 2033) | 4.7% |

| Historical Market Growth (2020 - 2025) | 3.8% |

DRO Analysis

Drivers - Rising Demand for Energy-Efficient Motors

The growing focus on energy efficiency is a major driver for the industrial motor market, supported by strict global regulations and cost optimization needs. Electric motors consume nearly half of global electricity, encouraging industries to shift toward high-efficiency IE3 and IE4 motors. This transition helps reduce operational costs and improve energy performance across industrial applications.

Additionally, upgrading to energy-efficient motors significantly lowers carbon emissions, supporting sustainability goals. Regulatory frameworks such as minimum efficiency standards are accelerating replacement of legacy systems. Industries are achieving notable energy savings, often up to 10%, which enhances long-term profitability while aligning with environmental compliance requirements.

Industrial Automation and Robotics Expansion

The rapid expansion of industrial automation is driving strong demand for advanced motor technologies such as servo and stepper motors. Increasing deployment of industrial robots across manufacturing sectors is boosting the need for precise and high-performance motion control systems. These motors play a critical role in ensuring accuracy, speed, and operational efficiency.

Furthermore, Industry 4.0 adoption involves integrating motors with smart technologies such as IoT for predictive maintenance and real-time monitoring. This enhances productivity and reduces downtime in automated systems. Sectors such as automotive and electronics are witnessing significant efficiency gains, strengthening the long-term growth of the industrial motor market.

Restraints - High Initial Costs of Advanced Motors

The high upfront cost of premium efficiency motors, such as IE4 and IE5, remains a key restraint in the industrial motor market. These motors can cost significantly more than standard models, limiting adoption, especially among cost-sensitive industries and small enterprises with constrained capital budgets.

Additionally, longer payback periods make investments less attractive despite long-term energy savings. Fluctuations in raw material prices, including copper and rare earth elements, further increase overall costs. These factors slow down replacement of older systems, particularly in emerging markets where affordability remains a major concern.

Stringent Regulatory Compliance Burdens

Complex and region-specific regulatory standards pose a significant challenge for industrial motor manufacturers. Compliance with multiple efficiency and safety frameworks increases operational complexity and adds to certification and testing costs, especially for companies operating in global markets.

Moreover, frequent regulatory updates require continuous product modifications and additional investments. Non-compliance can lead to financial penalties and restricted market access, creating barriers for new entrants. These regulatory pressures can delay product launches and increase manufacturers' time-to-market.

Opportunities - Adoption of Smart and IoT-Enabled Motors

The integration of IoT and smart technologies into industrial motors presents a significant growth opportunity. Smart motors enable real-time monitoring, predictive maintenance, and improved operational efficiency, reducing downtime and maintenance costs across industrial applications. This is increasingly important as industries shift toward data-driven decision-making.

Furthermore, the rise of smart manufacturing and automation is accelerating the adoption of connected motor systems. These solutions enhance productivity and asset performance, especially in high-growth sectors like robotics and advanced manufacturing. Continuous technological advancements are creating strong opportunities for manufacturers to develop intelligent, value-added motor solutions.

Growth in Renewable Energy and EV Integration

The rapid expansion of renewable energy and electric vehicle industries is creating strong demand for specialized industrial motors. Applications such as wind turbines, solar tracking systems, and EV manufacturing rely heavily on high-performance and energy-efficient motors. This is driving innovation in motor design and efficiency.

Additionally, increasing EV production is boosting demand for brushless DC motors and high-voltage motor systems. Government incentives and investments in clean energy infrastructure are further supporting this growth. These trends offer significant opportunities for manufacturers to expand into high-growth, sustainability-focused application areas.

Category-wise Analysis

Motor Type Insights

AC motors, particularly induction motors, dominate the industrial motor market with a 65% share in 2025 due to their reliability, cost-effectiveness, and wide applicability. Their ability to operate efficiently in harsh industrial environments and support diverse power requirements makes them the preferred choice across applications such as pumps, compressors, and conveyors. Their high durability and minimal maintenance needs further strengthen their widespread adoption.

Servo motors are emerging as the fastest-growing segment, driven by increasing demand for precision and automation. Their superior control, accuracy, and responsiveness make them ideal for robotics and advanced manufacturing systems. As industries adopt smart technologies and automated processes, the demand for high-performance motion control solutions continues to rise.

Voltage Insights

Low-voltage motors (<1 kV) lead the market, with a 55% share in 2025, primarily due to their safety, ease of installation, and suitability for standard industrial applications. They are widely used across manufacturing facilities and are highly compatible with variable frequency drives, improving energy efficiency and operational flexibility. Their lower risk profile further supports their strong adoption.

Medium-voltage motors are the fastest-growing segment, driven by increasing demand in heavy industrial applications. These motors are gaining traction in sectors such as mining, oil and gas, and power generation, where higher power capacity and operational efficiency are essential. Their ability to handle demanding workloads is driving their growing adoption.

Power Output Insights

Integral horsepower (IHP) motors dominate the market with a 70% share in 2025, driven by their extensive use in heavy-duty industrial operations. These motors are essential for high-load applications such as compressors, pumps, and large machinery. Their durability and ability to operate continuously under demanding conditions make them critical across power-intensive industries.

Fractional horsepower (FHP) motors are the fastest-growing segment, supported by rising demand in light industrial and precision applications. They are increasingly used in small equipment and automation systems where compactness and efficiency are important. Growth in sectors like electronics and small machinery is driving their adoption.

Industry Insights

Power generation leads the industrial motor market with a 25% share in 2025, driven by the need for reliable and efficient operations in power plants. Industrial motors play a critical role in turbines, cooling systems, and auxiliary equipment, ensuring continuous energy production. Their high energy consumption in power facilities further reinforces the demand for efficient motor systems.

Water and wastewater treatment is the fastest-growing end-use segment, driven by increasing infrastructure development and environmental regulations. Rising demand for efficient water management systems is boosting the need for industrial motors in pumping and treatment processes. Global investments in sustainable and smart water infrastructure support this trend.

Regional Insights

North America Industrial Motor Market Trends

North America is experiencing steady growth, supported by strong industrial policies and efficiency mandates. The U.S. remains the dominant contributor, with widespread adoption of premium efficiency motors and increasing deployment across manufacturing and energy sectors. The region benefits from advanced infrastructure and a high level of technological integration in industrial operations. The market is projected to grow at a CAGR of around 5.5% during the forecast period, driven by investments in grid modernization and industrial automation. Increasing focus on smart motor systems and predictive maintenance is enhancing operational efficiency. Continuous innovation and government-backed infrastructure programs are further accelerating demand.

Europe Industrial Motor Market Trends

Europe holds a significant 25% share in the industrial motor market, driven by strong regulatory frameworks and early adoption of energy-efficient technologies. Countries like Germany, the U.K., and France lead in implementing advanced manufacturing practices and efficiency standards, ensuring consistent demand for high-performance industrial motors.

The region is witnessing steady growth supported by sustainability initiatives and industrial modernization. The increasing adoption of Industry 4.0 and the focus on reducing carbon emissions are driving demand for advanced motor systems. Retrofitting existing infrastructure with energy-efficient solutions remains a key driver of growth across industries.

Asia Pacific Industrial Motor Market Trends

Asia Pacific leads the global industrial motor market with a dominant 45% share in 2025, driven by strong manufacturing activity and expanding industrial bases. China plays a central role with large-scale production, while countries like Japan contribute through advanced precision technologies and established industrial standards.

The region is also the fastest-growing, supported by rapid urbanization and industrial expansion in emerging economies such as India and Southeast Asian countries. Government initiatives promoting domestic manufacturing and infrastructure development are boosting demand. Cost advantages and increasing investments in the power and automation sectors continue to drive growth.

Competitive Landscape

The industrial motor market is moderately consolidated, with leading players focusing on technological innovation and large-scale production capabilities to maintain competitiveness. Continuous investment in research and development is driving advancements in energy efficiency, including the adoption of advanced materials and motor designs. Companies are also strengthening their market position through strategic partnerships, acquisitions, and expansion into high-growth regions.

Key competitive differentiation is increasingly centered on digital integration and customization. Manufacturers are incorporating IoT-enabled features for predictive maintenance and performance optimization. Additionally, emerging business models such as equipment-as-a-service are gaining traction, allowing end users to reduce upfront costs while improving operational flexibility and lifecycle management.

Key Developments:

- In June 2025, ABB introduced its Ability Smart Sensor platform to strengthen predictive maintenance capabilities in industrial motors. The solution enables real-time condition monitoring and analytics, helping operators reduce unexpected failures and extend motor lifespan by nearly 20% through proactive servicing.

- In March 2024, Siemens launched the Simotics S-1FK2 motor series designed specifically for high-precision robotics and automated systems. The new motors deliver improved torque density, compact design, and enhanced dynamic response, supporting faster and more accurate motion control in advanced manufacturing environments.

- In November 2023, Nidec expanded its manufacturing footprint in the United States to increase production capacity for electric vehicle and industrial motors. The move was aimed at leveraging domestic incentives and strengthening regional supply chains while meeting rising demand for electrification technologies.

Companies Covered in Industrial Motor Market

- ABB

- Siemens

- WEG

- Nidec Corporation

- Toshiba

- Mitsubishi Electric

- Regal Rexnord

- Schneider Electric

- General Electric

- Hitachi

- Rockwell Automation

- Emerson Electric

- TECO Electric & Machinery

- Wolong Electric Group

- Franklin Electric

Frequently Asked Questions

The industrial motor market is expected to reach US$ 23.1 billion in 2026, growing steadily driven by industrial expansion and energy efficiency adoption.

Energy efficiency regulations and automation trends are primary drivers, accelerating the adoption of high-efficiency motors across industries.

Asia Pacific leads the market with a 45% share in 2025, supported by strong manufacturing growth and industrialization.

IoT-enabled smart motors present a key opportunity, enabling predictive maintenance and improved operational efficiency under Industry 4.0.

Leading companies include ABB, Siemens, Nidec, and WEG, focusing on innovation and advanced motor technologies.