- Electrical Equipment & Services

- Industrial Gauges Market

Industrial Gauges Market Size, Share, and Growth Forecast, 2026 - 2033

Industrial Gauges Market by Application (Hydraulic Systems, Pumps, Compressors, Boilers), End-User (Oil & Gas, Chemical, Water & Wastewater, Power Generation), Gauge Type (Pressure, Temperature, Level), and Regional Analysis for 2026-2033

Industrial Gauges Market Share and Trends Analysis

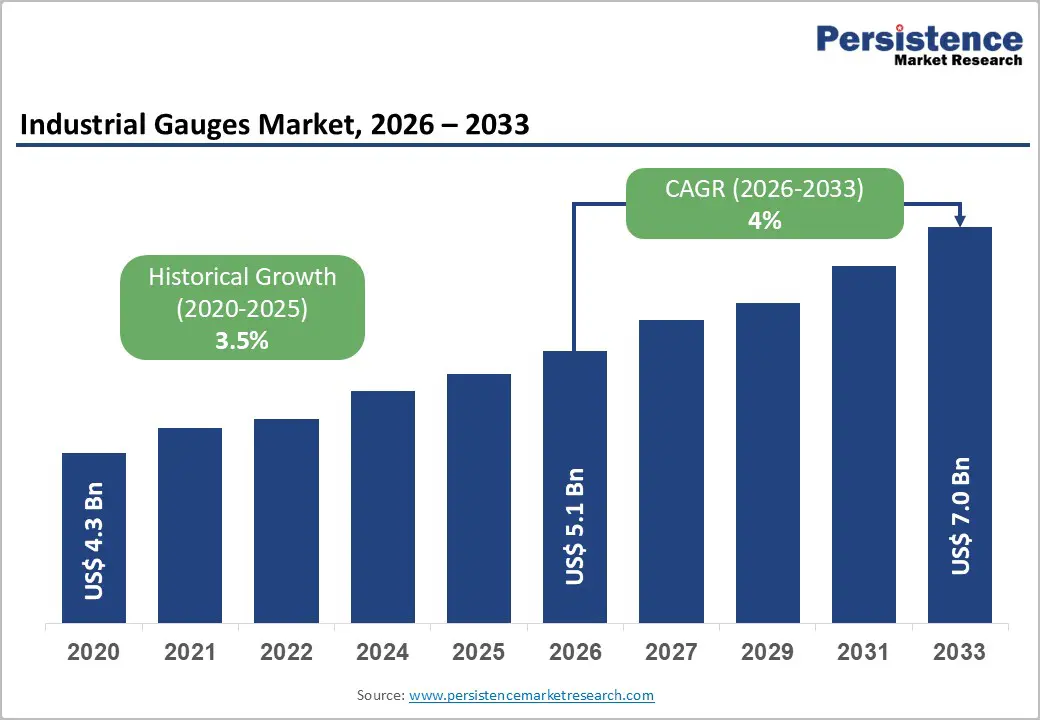

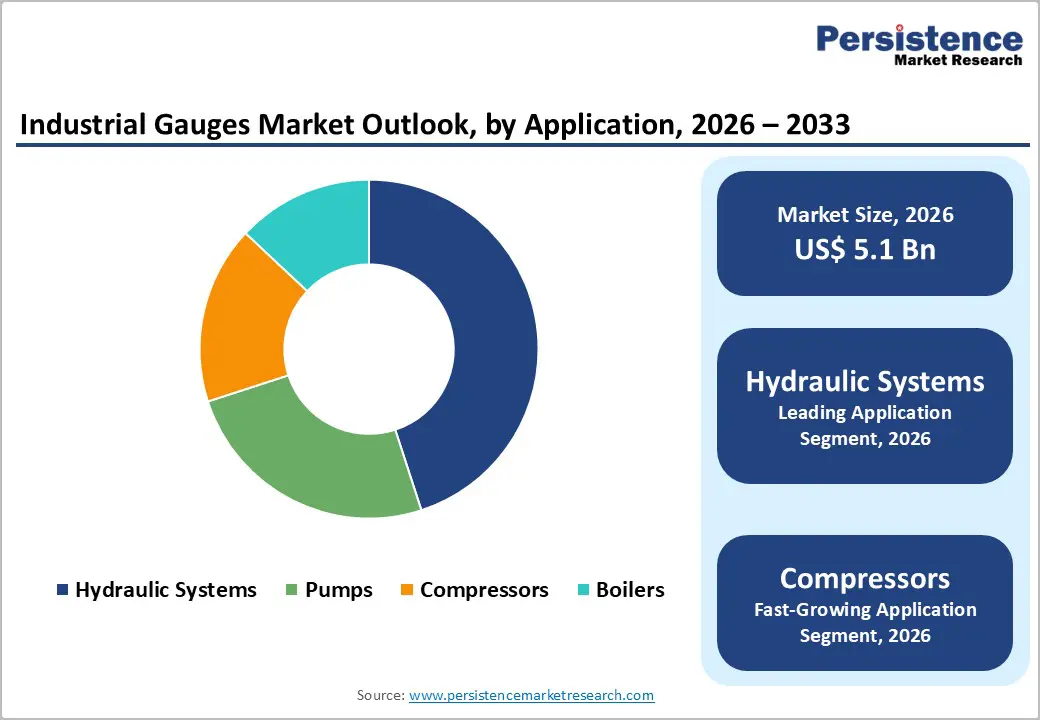

The global industrial gauges market size is likely to be valued at US$ 5.1 billion in 2026, and is projected to reach US$ 7.0 billion by 2033, growing at a CAGR of 4% during the forecast period 2026−2033.

Market growth is being supported by rising automation across manufacturing environments where precision measurement is becoming central to operational efficiency. Industrial facilities are integrating automated production lines that require accurate monitoring of pressure, temperature, flow, and level parameters. Regulatory standards issued by organizations such as the International Organization for Standardization (ISO) and the Occupational Safety and Health Administration (OSHA) are mandating strict quality control and safety compliance.

These requirements are increasing reliance on calibrated and traceable measurement instruments. As digital transformation initiatives continue advancing across industrial sectors, demand for reliable gauge systems is strengthening. Technological progress is reshaping product capabilities within the industrial gauges segment. Advanced sensor integration and Internet of Things (IoT) connectivity are enabling real-time data transmission and predictive maintenance applications. Connected gauge systems are supporting centralized monitoring dashboards and reducing unplanned downtime. Industrial operators are prioritizing measurement accuracy to improve asset performance and minimize process variability. Emerging economies in Asia Pacific are expanding manufacturing capacity across automotive, chemicals, energy, and infrastructure sectors, opening new avenues for market players.

Key Industry Highlights

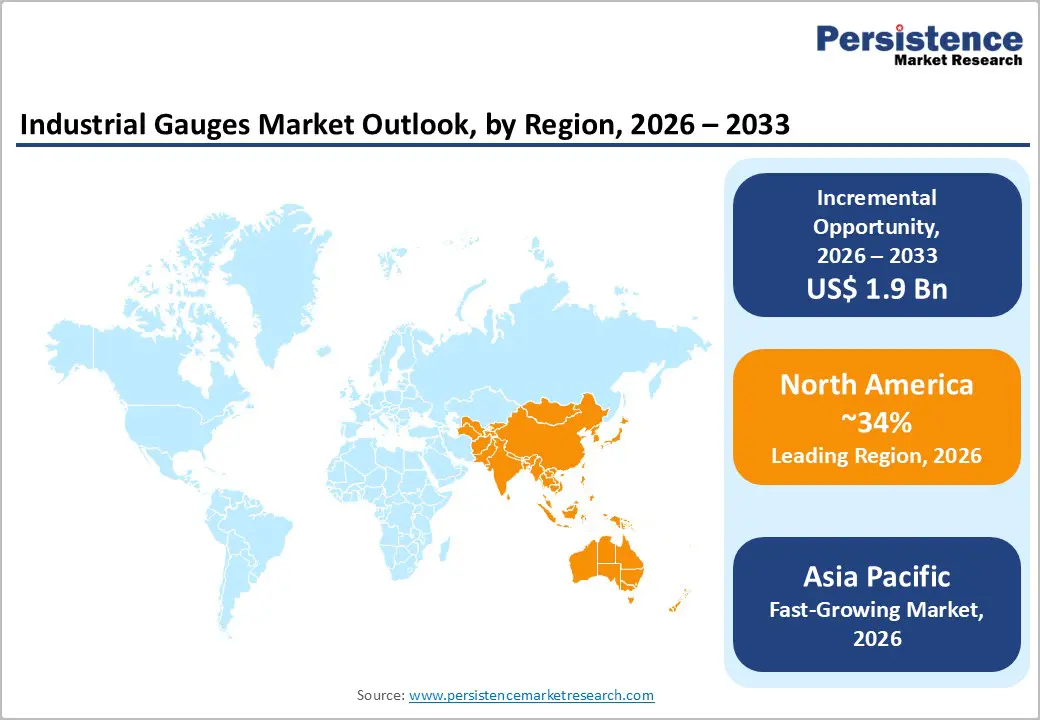

- Regional Dominance: The Asia Pacific market likely to lead as well as grow the fastest between 2026 and 2033, holding around 34% market share, supported by expansive petrochemical developments.

- Application Primacy: Hydraulic systems are slated to capture approximately 32% revenue share in 2026, while compressors are expected to be the fastest-growing segment over the 2026-2033 forecast period.

- End-User Leadership: The oil and gas segment is poised to lead with an approximate 39% revenue share in 2026, whereas the chemical industry is projected to record the highest CAGR through 2033.

- Driver & Opportunity: The accelerating adoption of Industry 4.0 technologies is reshaping demand patterns for industrial gauges, while technological innovations in wireless communication and energy harvesting are opening fresh market opportunities.

| Key Insights | Details |

|---|---|

| Industrial Gauges Market Size (2026E) | US$5.1 Bn |

| Market Value Forecast (2033F) | US$7.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Industrial Automation and Industry 4.0 Adoption

The accelerating adoption of Industry 4.0 technologies is reshaping demand for industrial gauges across manufacturing sectors. Companies are installing automated production systems that rely on precise digital pressure gauges, temperature sensors, and flow meters to maintain process stability. Smart factory environments are deploying IoT–enabled devices to support predictive maintenance strategies that reduce equipment downtime and improve asset utilization. The transition from analog instrumentation to digital measurement platforms is strengthening operational visibility and process control. Manufacturers are increasingly selecting gauges equipped with data logging functions, wireless communication modules, and integration capabilities with supervisory control and data acquisition (SCADA) systems. These features are enabling real-time performance monitoring and centralized data management across production facilities.

Industrial operators are prioritizing advanced measurement systems that align with automation objectives and long-term efficiency targets. Strategic suppliers are responding by designing customized gauge solutions that integrate with enterprise resource planning (ERP) systems and artificial intelligence (AI) analytics platforms. This technological convergence is generating additional revenue opportunities through remote diagnostics, predictive analytics, and subscription-based monitoring services. Executives should evaluate existing instrumentation portfolios against digital performance benchmarks to determine modernization priorities. Proactive investment in connected gauge technologies will strengthen competitiveness and ensure operational resilience as industrial digitization continues advancing.

High Initial Investment and Calibration Costs

Small & medium-sized enterprises (SMEs) are encountering capital expenditure constraints when considering premium industrial gauge systems. Digital and IoT–enabled instruments are requiring higher upfront investment compared with conventional analog models. Companies must also allocate funds for supporting network infrastructure, cybersecurity safeguards, and system integration. Routine calibration services conducted by accredited laboratories are adding recurring operational costs to maintain measurement accuracy and regulatory compliance. Facilities operating numerous monitoring points are experiencing cumulative expenditure pressure. During periods of economic uncertainty, cost-sensitive operators are often postponing modernization initiatives and extending the lifecycle of existing equipment.

Wireless gauge solutions are introducing additional lifecycle expenses, including battery replacement cycles, communication gateway maintenance, and software subscription fees. These cumulative costs are influencing purchasing decisions in resource-constrained environments, particularly across emerging markets. Many organizations are continuing to rely on durable analog devices to control short-term spending. However, this cautious approach may limit long-term efficiency gains associated with digital monitoring and predictive analytics. Executives should conduct comprehensive total cost of ownership assessments that compare long-term operational savings with initial capital outlays. Suppliers can strengthen market penetration by offering tiered product portfolios, flexible financing structures, and modular upgrade pathways. Such strategies enable gradual digital adoption while preserving cash flow stability and minimizing operational disruption.

Wireless and Battery-Free Gauge Technologies

Technological progress in wireless communication and energy harvesting is creating new growth pathways within the industrial gauges market. Advanced wireless pressure transmitters are adopting communication standards such as Wireless Highway Addressable Remote Transducer (WirelessHART) and International Society of Automation 100 (ISA100), which enable secure data transmission in complex industrial environments. These solutions are functioning effectively in remote or hazardous locations without extensive cabling, thereby reducing installation time and infrastructure costs. Energy harvesting technologies, including thermoelectric generators, photovoltaic solar cells, and vibration-based power systems, are supplying autonomous energy to measurement devices. This capability is eliminating frequent battery replacement requirements and improving suitability in safety-sensitive zones such as chemical processing plants and offshore platforms.

The Industrial IoT (IIoT) is accelerating deployment of wireless gauge networks that support predictive maintenance strategies and digital twin modeling. Low-power communication protocols such as Bluetooth Low Energy (BLE) and Long Range Wide Area Network (LoRaWAN) are enabling cost-effective monitoring across distributed assets. Emerging applications include leak detection, steam trap performance assessment, and compressed air system optimization. Executives should prioritize partnerships with vendors demonstrating validated wireless integration expertise and cybersecurity compliance. Hybrid architectures that combine wired reliability with wireless flexibility are strengthening scalability and operational continuity. Early investment in connected measurement ecosystems will enhance asset visibility, reduce maintenance costs, and improve long-term operational resilience.

Category-wise Analysis

Application Insights

Hydraulic systems are projected to account for approximately 32% of the industrial gauges market revenue share in 2026. These systems form the operational foundation for heavy equipment used in automotive, construction, and manufacturing industries. Accurate pressure monitoring is ensuring safe and reliable performance in high-load environments. Hydraulic mechanisms are supporting essential functions such as braking, power steering, suspension control, and transmission actuation. Rising global vehicle production, particularly across emerging economies, is sustaining demand for precise measurement solutions within automotive hydraulics. Manufacturers are incorporating lightweight materials such as aluminum alloys to improve fuel efficiency and durability, which is increasing the need for calibrated pressure instrumentation. Integration with electronic stability control and anti-lock braking systems is further reinforcing the critical role of hydraulic monitoring in modern industrial and transportation systems.

Compressor applications are expected to be the fastest-growing between 2026 and 2033. Growth is being driven by expanding gas processing operations and increasing industrial automation. Investments in energy infrastructure are accelerating adoption of compressor systems for efficient air and gas handling across power generation and petrochemical facilities. Integration with Industry 4.0 technologies, including IoT sensors and data analytics platforms, is enabling real-time condition tracking and predictive maintenance. These digital capabilities are optimizing operational efficiency and reducing downtime in high-capacity environments. Rapid infrastructure development and manufacturing expansion in Asia Pacific are further increasing compressor installation rates. Scalable system designs that support modular upgrades are enhancing flexibility and long-term performance optimization across diverse industrial settings.

End-User Insights

The oil and gas sector is anticipated to capture an estimated 39% of the industrial gauges market share in 2026. Operations across drilling, production, transportation, and refining depend on accurate monitoring of pressure, temperature, and flow parameters to ensure operational continuity and safety. Regulatory frameworks established by organizations such as the American Petroleum Institute (API) are mandating certified instrumentation capable of operating in hazardous environments. High downtime costs associated with unplanned shutdowns are compelling operators to invest in rugged, high-accuracy gauges that preserve process integrity. Expanding offshore exploration and shale resource development are increasing measurement requirements. Integration of IoT devices and AI analytics is enabling real-time asset monitoring and predictive maintenance across upstream and downstream operations.

The chemical industry is likely to post the highest CAGR between 2026 and 2033. Chemical manufacturing processes require precise control of pressure, temperature, level, and flow variables to maintain product quality and ensure safety in reactive environments. High-precision instrumentation is essential where volatile reactions demand continuous oversight and rapid adjustment. Expansion of specialty chemical production is driving installation of advanced measurement systems, particularly in emerging markets investing in new processing facilities. Operators are incorporating IoT-enabled sensors to support predictive analytics and automated process optimization. Sustainability initiatives are encouraging adoption of energy-efficient gauge systems that reduce material waste and lower emissions. As digitalization and environmental compliance become central to chemical production strategies, demand for intelligent measurement solutions is expected to accelerate.

Gauge Type Insights

Pressure measurement devices are foreseen to command roughly 62% of the industrial gauges market revenues in 2026. These instruments are serving critical functions across oil and gas, chemical manufacturing, and power generation facilities where precise pressure control is essential for safety and efficiency. Accurate monitoring is preventing equipment failure, reducing leak risks, and ensuring stable process conditions in high-risk environments. Digital pressure gauges are gaining adoption due to enhanced measurement precision, integrated data logging capabilities, and intuitive display interfaces. Their compatibility with automated control systems is supporting seamless integration into advanced manufacturing environments. As regulatory requirements and operational risk management standards continue tightening, manufacturers are prioritizing innovation in pressure monitoring technologies to meet stringent performance expectations.

Temperature measurement systems are expected to register the fastest growth over the 2026-2033 forecast period. Wireless temperature sensors are increasingly deployed in cold chain logistics, pharmaceutical production, and food processing operations where continuous documentation is mandated by authorities such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA). Infrared thermometers and thermal imaging technologies are expanding use in high-temperature industrial processes that require non-contact measurement. Resistance temperature detectors (RTDs) and thermocouples are maintaining strong relevance in laboratory environments and semiconductor fabrication facilities that demand accuracy levels near ±0.1 degrees Celsius. As compliance requirements and quality assurance protocols strengthen across industries, temperature monitoring solutions are becoming integral to operational integrity and regulatory adherence.

Regional Insights

Asia Pacific Industrial Gauges Market Trends

Asia Pacific is slated to be both the leading and fastest-growing regional market for industrial gauges in 2026, accounting for approximately 34% of global revenue. China is driving regional leadership through large-scale petrochemical investments and expansion of advanced manufacturing clusters. India is strengthening demand through its growing pharmaceutical production base, where strict calibration standards are required for sterile processing environments. Japan is sustaining steady consumption through precision-driven sectors such as semiconductor fabrication and robotics manufacturing. Southeast Asian economies including Vietnam, Thailand, and Indonesia are attracting foreign direct investment into industrial corridors, which is increasing installation of measurement systems. Competitive manufacturing costs are supporting local production of mechanical gauges, particularly among Chinese suppliers. Government-backed infrastructure programs and regional trade agreements are further stimulating industrial expansion.

Regulatory modernization is reinforcing quality assurance standards across the region. China is aligning calibration practices with ISO guidelines, while India is enforcing compliance under the Legal Metrology Act of 2009. Multinational instrumentation providers are localizing production facilities to reduce supply chain risk and improve response times. Establishing regional manufacturing and service hubs is enabling faster delivery and enhanced technical support. Executives should assess collaboration opportunities with established local distributors to strengthen regulatory navigation and market penetration. Hybrid gauge systems that combine analog durability with digital monitoring enhancements are gaining traction as industrial operators seek gradual modernization. Strategic alignment with regional industrialization trends will position companies to capture sustained growth in Asia Pacific.

Europe Industrial Gauges Market Trends

Europe maintains a strong position in the global market for industrial gauges due to its advanced manufacturing ecosystem and established industrial standards. Germany is leading regional demand through its robust chemical, automotive, and machinery production sectors, all of which require high-precision measurement systems. The United Kingdom and France are contributing significantly through pharmaceutical manufacturing and food processing industries where validated instrumentation is essential for regulatory compliance. Spain is emerging as a growth contributor, particularly through renewable energy investments such as concentrated solar power installations that require specialized high-temperature monitoring solutions.

Harmonized regulatory frameworks are reinforcing market stability and cross-border trade efficiency. The Pressure Equipment Directive (PED) and directives related to explosive atmospheres under ATEX certification are standardizing compliance requirements across member states. These regulations are favoring manufacturers with strong testing capabilities and documented quality systems. European companies such as Endress+Hauser Group, WIKA Alexander Wiegand SE & Co. KG, and JUMO GmbH & Co. KG are leveraging localized service networks and close client engagement to maintain competitive advantage. Investment in wireless sensor technologies, cybersecurity protection, and digital integration is supporting Industry 4.0 alignment. Executives should consider partnerships with established regional suppliers to strengthen compliance positioning and accelerate system upgrades. Retrofit initiatives that improve energy efficiency and digital connectivity are enabling companies to align sustainability objectives with long-term industrial modernization strategies.

North America Industrial Gauges Market Trends

North America possess a strong regional position in the market for industrial gauges owing to its established industrial base and advanced operational standards. The United States is driving demand through large-scale chemical processing, petroleum refining, and power generation activities that require continuous monitoring of pressure, temperature, and flow parameters. Shale oil and gas development is increasing the need for high-pressure instrumentation capable of withstanding hydraulic fracturing environments. Mexico is contributing additional growth through expanding automotive and aerospace manufacturing clusters that depend on precise quality control systems. Early adoption of Industry 4.0 frameworks across North American facilities is accelerating integration of smart sensors and connected measurement devices within automated production lines.

Regulatory oversight is shaping procurement and upgrade decisions throughout the region. The OSHA Process Safety Management standard is governing facility risk management practices, while the Environmental Protection Agency (EPA) Leak Detection and Repair program is enforcing strict emission monitoring requirements. Pipeline safety regulations administered by the United States Department of Transportation are mandating routine pressure verification across transmission networks. Industrial operators are adopting wireless monitoring systems and cloud-based calibration platforms to enhance compliance tracking and maintenance efficiency. Executives should conduct systematic audits of legacy instrumentation against these regulatory benchmarks. Suppliers offering retrofit solutions and digital integration kits are enabling cost-effective modernization. Strategic expansion into Mexico’s manufacturing corridors is also providing opportunities to diversify supply chains and strengthen regional resilience.

Competitive Landscape

The global industrial gauges market structure is moderately concentrated, with Emerson Electric, Honeywell International, Siemens, ABB, and OMEGA Engineering holding a significant share of total revenue. These companies are leveraging established global distribution networks, engineering expertise, and diversified industrial portfolios to maintain competitive positioning. At the same time, regional manufacturers and specialized instrumentation firms are actively competing by targeting niche applications and offering cost-optimized alternatives. Market rivalry is intensifying as customers demand higher measurement accuracy, digital connectivity, and integration with automated control environments. This competitive environment is encouraging continuous product refinement and operational efficiency improvements across the supply chain.

Technological differentiation is becoming a primary competitive lever. Leading firms are advancing smart gauge systems that incorporate IoT connectivity and AI–enabled analytics to support predictive maintenance and real-time performance monitoring. These capabilities are enhancing asset visibility and enabling proactive operational adjustments. Manufacturers are also optimizing production processes to improve cost competitiveness without compromising calibration standards or durability. Customization, system interoperability, and rapid responsiveness to Industry 4.0 requirements are defining successful market strategies. Companies that align innovation pipelines with automation trends and regulatory compliance demands are strengthening long-term resilience in this evolving industrial instrumentation landscape.

Key Industry Developments

- In November 2025, ABB launched the MTG Box Gauge for precise single-side measurement of aluminum strip thickness below 8 mm during the final stages of hot rolling mills. The gauge features IP66 sealing for emulsion protection, optimized airflow reducing coil temperature by up to 40°C, pulsed eddy current technology, and simplified installation where underside access is limited.

- In September 2025, ABB launched its P-300 series versatile pressure transmitters in the US market, offering 0.055% accuracy across a wide range from 0.05 kPa differential pressure to 105 MPa gauge pressure for applications in petrochemical, chemical, power, pulp & paper, and other industries. Key features include a high-contrast backlit HMI display, QR-code-enabled Digital Advanced Diagnostics for instant documentation access, and FM-approved hazardous area certification.

- In March 2025, Renesas introduced R-BMS F, a complete battery management system with pre-validated firmware for its lithium-ion fuel gauge ICs, targeting consumer applications such as e-bikes, vacuum cleaners, robotics, and drones. The firmware handles essential functions such as state-of-charge/health monitoring, cell balancing, current/voltage/temperature control, and fault detection across configurations.

Companies Covered in Industrial Gauges Market

- Emerson Electric Co.

- Honeywell International Inc.

- Siemens AG

- ABB Ltd.

- Yokogawa Electric Corporation

- WIKA Instruments

- Endress+Hauser Group

- Ashcroft Inc.

- OMEGA Engineering Inc.

- Dwyer Instruments Inc.

- Kobold Messring GmbH

- NOSHOK Inc.

- Baumer Group

- JUMO GmbH & Co. KG

- Anderson-Negele

Frequently Asked Questions

The global industrial gauges market is projected to reach US$ 5.1 billion in 2026.

The market is driven by industrial automation, stringent safety regulations, and renewable energy expansion.

The market is poised to witness a CAGR of 4% from 2026 to 2033.

Major opportunities lie in industrialization of emerging economies, IoT convergence, and sustainability-driven upgrades.

Emerson Electric Co., Honeywell International Inc., Siemens AG, ABB Ltd., and OMEGA Engineering Inc. are some of the key players in the market.