- Industrial Machinery

- Industrial Brakes Market

Industrial Brakes Market Size, Share, and Growth Forecast 2026 - 2033

Industrial Brakes Market by Brake Type (Disc, Drum), Actuation (Hydraulic Braking System, Mechanical Braking System, Electrical Braking System, Pneumatic Braking System, Others), Application (Manufacturing, Metal and Mining, Marine and Shipping, Construction, Oil & Gas, Others), and Regional Analysis for 2026 - 2033

Industrial Brakes Market Size and Trend Analysis

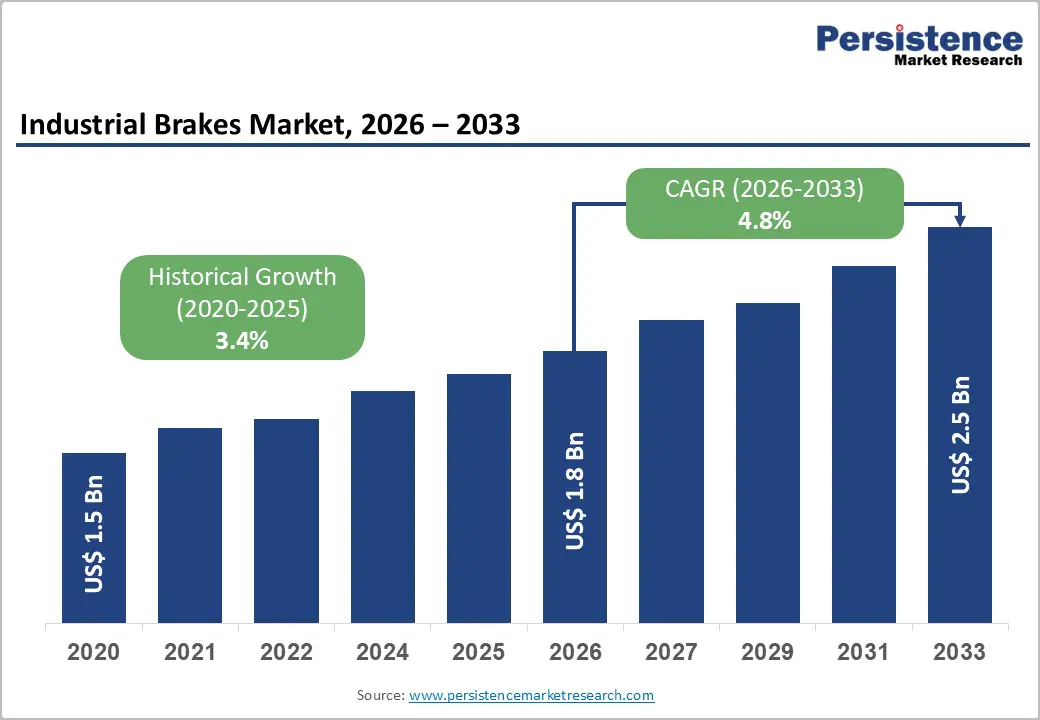

The global industrial brakes market size is valued at US$ 1.8 Bn in 2026 and is projected to reach US$ 2.5 Bn by 2033, growing at a CAGR of 4.8% between 2026 and 2033. This growth is primarily driven by accelerating industrial automation, expanding heavy-industry infrastructure investments, and increasingly stringent workplace safety regulations across key end-use sectors.

The rising deployment of automated manufacturing systems and the expansion of mining, construction, and marine operations worldwide are driving sustained demand for high-performance braking solutions.

Key Industry Highlights:

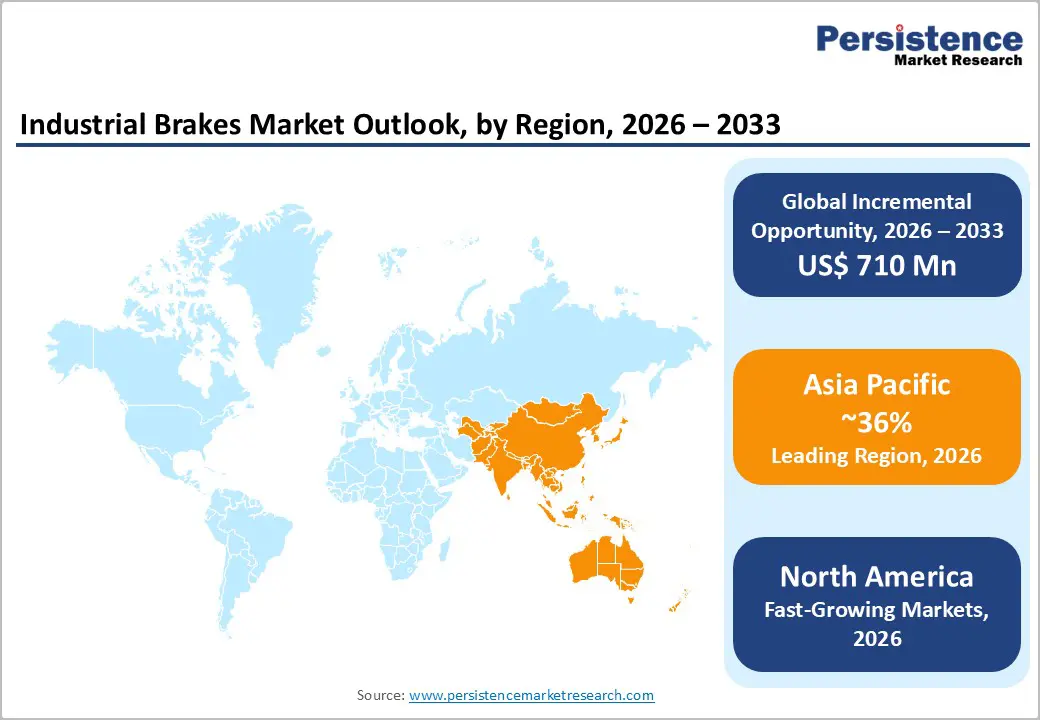

- Leading Region: Asia Pacific leads the industrial brakes Market, accounting for 37% of global revenue in 2026, driven by China's manufacturing modernization (RMB 500 Bn plan), India's National Infrastructure Pipeline (INR 111 trillion), and expanding mining activity across ASEAN economies.

- Fastest Growing Region: North America is the fastest-growing region, driven by stringent OSHA workplace safety mandates, strong manufacturing and oil & gas sector demand, and significant federal infrastructure investments totaling US$ 1.2 trillion under the Infrastructure Investment and Jobs Act.

- Dominant Segment: Disc brakes dominate the Brake Type segment with approximately 55% revenue share, owing to superior heat dissipation, reliability under continuous heavy-duty operation, and ease of visual inspection that minimizes unplanned downtime in manufacturing and crane applications.

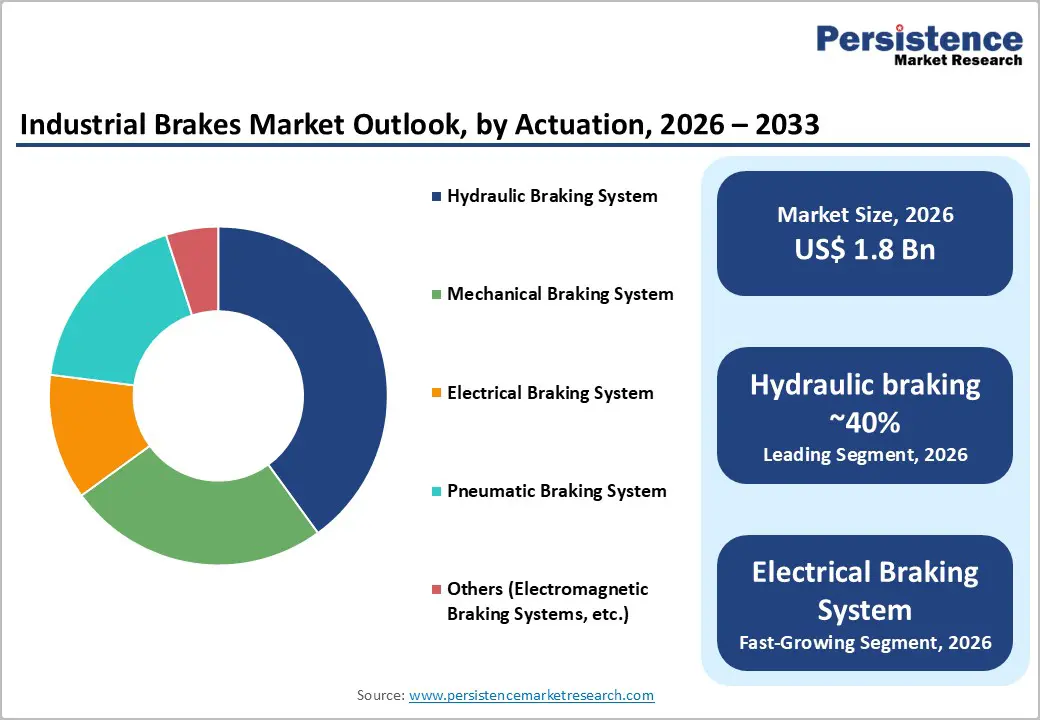

- Fastest Growing Segment: Electrical and electromagnetic braking systems are the fastest-growing actuation segment, driven by seamless integration with Industry 4.0 platforms, AGV and robotic system deployments, and growing demand for regenerative, low-maintenance braking in automated industrial environments.

- Key Market Opportunity: Wind energy infrastructure expansion represents the key market opportunity, with global wind capacity additions reaching 116 GW in 2023 and projected to double by 2030 per IEA forecasts, driving structural demand for specialized main shaft, yaw, and emergency stop braking systems.

| Key Insights | Details |

|---|---|

| Industrial Brakes Market Size (2026E) | US$ 1.8 Bn |

| Market Value Forecast (2033F) | US$ 2.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.4% |

DRO Analysis

Drivers - Industrial Automation and Machinery Safety Mandates

The rapid global expansion of industrial automation is the foremost structural driver of the industrial brakes market. Across the manufacturing, mining, and construction sectors, the adoption of computer-controlled machinery, robotic systems, and automated material-handling equipment requires high-reliability braking components that can operate continuously under demanding load and temperature conditions.

According to the International Federation of Robotics (IFR), global industrial robot installations reached a record 541,000 units in 2022 and have continued to rise, with each new robot installation representing a potential demand node for precision braking systems. Furthermore, the U.S. Occupational Safety and Health Administration (OSHA) increased the maximum penalty for serious safety violations to US$ 165,514 per incident in 2025, compelling industrial operators to invest proactively in certified braking and motion-control solutions across factory floors.

Expansion of Mining, Construction, and Heavy Industrial Operations

The global expansion of mining operations, large-scale infrastructure construction, and heavy industrial manufacturing is generating substantial incremental demand for robust industrial braking systems. The Indian government's National Infrastructure Pipeline commits approximately INR 111 trillion (≈ US$ 1.3 trillion) for infrastructure development through 2030, directly driving procurement of heavy machinery equipped with high-capacity hydraulic and disc braking systems.

Similarly, the Chinese Ministry of Industry and Information Technology's 14th Five-Year Plan allocated RMB 500 billion to manufacturing modernization, with Chinese steel production facilities alone consuming an estimated 180,000 brake units annually for rolling mill and material-handling operations. Globally, the expansion of offshore oil and gas platforms and container port infrastructure further amplifies demand for specialized marine and industrial braking solutions.

Restraints - High Initial Investment and Total Cost of Ownership

The high upfront capital expenditure associated with advanced industrial braking systems, particularly hydraulic disc and electromagnetic configurations, presents a significant adoption barrier, especially for small and medium enterprises (SMEs) in emerging economies. High-performance braking systems for heavy cranes, offshore platforms, or mining conveyors can require substantial capital investment, including installation, commissioning, and integration with automation control systems.

The complexity of maintenance and the need for specialized technical personnel further elevate the total cost of ownership, deterring budget-constrained operators from upgrading aging mechanical brake systems. In sectors where downtime is financially prohibitive, these costs can significantly delay procurement decisions, slowing the overall pace of market expansion.

Supply Chain Disruptions and Raw Material Price Volatility

Industrial brakes rely on specialized materials, including high-grade steel, friction-resistant composite materials, and precision-engineered hydraulic components. Global supply chain disruptions, as evidenced during the COVID-19 pandemic and subsequent geopolitical tensions, including the Russia-Ukraine conflict, exposed significant vulnerabilities in the procurement of these materials.

Price volatility for steel and specialty alloys, which are core to brake rotor and drum manufacturing, directly impacts production costs and margin structures for manufacturers. According to the World Steel Association, global crude steel production reached approximately 1.89 billion tonnes in 2023, yet price fluctuations remained significant, creating cost predictability challenges for industrial brake OEMs managing multi-year supply agreements with industrial equipment manufacturers.

Opportunities - Electrical and Electromagnetic Braking Systems as a Fast-Growing Segment

Electrical and electromagnetic braking systems represent the fastest-growing actuation segment in the industrial brakes market, driven by seamless integration with digital automation platforms, regenerative energy recovery, and lower maintenance requirements. As Industry 4.0 and smart manufacturing paradigms gain momentum globally, demand for braking solutions that interface directly with programmable logic controllers (PLCs), industrial IoT sensors, and machine learning-based predictive maintenance platforms is accelerating.

In November 2024, Kendrion showcased its latest electromagnetic braking solutions for industrial automation, including applications in Automated Guided Vehicles (AGVs), robotics, and servo motor systems at the SPS trade fair in Nuremberg. The growing deployment of AGVs in warehousing and manufacturing facilities, replacing traditional forklifts at accelerating rates, creates a particularly high-value application corridor for compact, precise electromagnetic brakes.

Renewable Energy Infrastructure: Wind Turbine Braking Applications

The global expansion of wind energy infrastructure creates a significant and rapidly expanding opportunity for industrial brake manufacturers. Wind turbines require highly specialized braking systems capable of operating in extreme environmental conditions while managing the considerable rotational forces generated by turbine rotors.

Dellner Bubenzer has specifically expanded its wind energy braking product line, scaling up local assembly for major wind turbine OEMs to support global renewable energy targets. According to the International Energy Agency (IEA), global wind power capacity additions reached approximately 116 GW in 2023, with cumulative capacity forecast to more than double by 2030 as governments accelerate energy transition commitments.

Category-wise Analysis

Brake Type Insights

Disc brakes dominate the industrial brakes market, commanding approximately 55% revenue share, supported by their superior stopping power, efficient heat dissipation, and durability under continuous heavy-duty industrial operation. Disc brakes’ exposed calliper design allows progressive heat dissipation that prevents the thermal build-up commonly associated with drum brake systems in enclosed configurations, making them the preferred choice for high-frequency stopping applications in manufacturing, crane and hoist, mining conveyors, and wind turbine installations.

Their modular design enables visual inspection without full disassembly, supporting planned maintenance schedules and minimizing unplanned downtime in critical production environments. According to industry analysis, disc brakes held approximately 45% of the industrial braking equipment market in 2024, with market leadership consolidated across crane, marine, and automated manufacturing applications.

Actuation Insights

Hydraulic braking systems hold the dominant position in the actuation segment, accounting for approximately 38% revenue share of the global Market. Hydraulic systems are favored for their precision control, ability to handle extreme loads, compact power-to-size ratio, and proven reliability in harsh operating environments, including mining, marine, offshore oil and gas, and heavy manufacturing.

The fluid-based actuation mechanism enables smooth, proportional braking force modulation, which is essential for crane and material-handling operations where sudden stops can compromise load safety and structural integrity. Dellner Bubenzer offers an extensive range of hydraulic disc and drum brakes with power packs delivering up to 200 bar of pressure, specifically engineered for demanding offshore and crane applications.

Application Insights

The manufacturing sector leads the industrial brakes market, accounting for an estimated 30% revenue share, driven by the extensive deployment of industrial braking systems across conveyor lines, press machines, robotic assembly cells, and automated guided vehicle (AGV) systems. Manufacturing facilities operating on 24/7 continuous production schedules demand brake systems capable of repeated high-stress duty cycles without performance degradation.

According to the United Nations Industrial Development Organization (UNIDO), global manufacturing value added reached approximately US$ 16.3 trillion in 2022, reflecting the scale of industrial activity that underpins brake system procurement. The sector’s ongoing investment in automation, including the integration of digital brake control and predictive maintenance platforms, further reinforces manufacturing’s position as the primary driver of global industrial braking solutions.

Regional Insights

North America Industrial Brakes Market Trends & Analysis

North America represents a significant and technologically advanced regional market for industrial brakes, underpinned by the United States' robust manufacturing base, an extensive network of mining operations, and the most stringent workplace safety regulatory framework globally. The region’s strong position in oil and gas extraction, particularly offshore Gulf of Mexico operations, sustains demand for specialized marine and drilling-grade hydraulic braking systems.

Innovation ecosystems across Michigan, Texas, and Ohio are driving the adoption of electromagnetic and smart braking technologies, aligning with the Industry 4.0 manufacturing transformation. The U.S. federal government’s infrastructure investments under the Infrastructure Investment and Jobs Act (US$ 1.2 trillion) are stimulating construction equipment procurement, further expanding demand for disc and drum brake systems in heavy construction applications.

U.S. Industrial Brakes Market Size

Estimated at approximately US$ 490 Mn in 2026, driven by manufacturing automation, OSHA compliance mandates, oil & gas operations, and infrastructure-related construction equipment demand. The U.S. Occupational Safety and Health Administration (OSHA) updated its enforcement protocols for manufacturing and warehousing sectors in 2025, increasing penalties for serious machinery safety violations to US$ 165,514 per incident, compelling operators to invest in certified, high-performance braking solutions.

Europe Industrial Brakes Market Trends, Drivers, & Insights

Europe represents a mature and innovation-driven market for industrial brakes, characterized by rigorous regulatory harmonization and a strong emphasis on machinery safety standards. The European Union’s Machinery Directive (2006/42/EC) and its successor, the Machinery Regulation (EU) 2023/1230, which came into force in 2023 and applies from January 2027, mandate stringent safety performance requirements for industrial machinery across member states, thereby driving systematic brake system upgrades.

The European Green Deal investments in clean industrial infrastructure are also expected to generate new demand for energy-efficient braking systems across manufacturing and renewable energy sectors.

Germany Industrial Brakes Market Size

Estimated at approximately US$ 185 Mn in 2026, driven by mechanical engineering exports, crane and hoist OEMs, and wind energy braking systems. Germany leads European demand, supported by its position as the world’s leading mechanical engineering exporter and the density of heavy industrial manufacturers, crane OEMs, and wind turbine producers headquartered in the region.

U.K. Industrial Brakes Market Size

Estimated at approximately US$ 110 Mn in 2026, supported by offshore oil & gas, maritime applications, and industrial manufacturing safety compliance. The United Kingdom’s maritime and offshore energy sector sustains robust demand for marine-grade hydraulic braking systems.

France Industrial Brakes Market Size

Estimated at approximately US$ 90 Mn in 2026, driven by nuclear energy infrastructure, construction, and manufacturing automation. France’s nuclear energy infrastructure comprising 56 operational reactors according to Electricité de France (EDF)requires specialized fail-safe braking systems for critical safety applications.

Asia Pacific Industrial Brakes Market Drivers & Analysis

Asia Pacific is the dominant regional market for industrial brakes, accounting for approximately 36% of global revenue in 2026, and it is projected to maintain the highest regional CAGR through 2033. China is the largest country-level market, with Chinese steel production facilities alone consuming an estimated 180,000 industrial brake units annually, according to industry analysis.

The Production Linked Incentive (PLI) Scheme across automotive, textiles, and steel sectors is catalyzing new manufacturing capacity with commensurate brake system requirements. ASEAN economies, including Malaysia, Vietnam, and Indonesia, are emerging as high-growth markets as manufacturing activity relocates from higher-cost geographies.

China Industrial Brakes Market Size

Estimated at approximately US$ 395 Mn in 2026, driven by steel production, port infrastructure, and manufacturing modernization. The Chinese government’s 14th Five-Year Plan allocated RMB 500 billion for manufacturing modernization, generating sustained procurement of automated machinery equipped with advanced braking systems. Port expansion along China’s coastline and major infrastructure initiatives, including the Belt and Road Initiative (BRI), further amplify demand for crane, hoisting, and marine-grade industrial brakes.

India Industrial Brakes Market Size

Estimated at approximately US$ 165 Mn in 2026, driven by the PLI Scheme, National Infrastructure Pipeline investments, and mining sector expansion. India is the fastest-growing country market in the region, with the government’s National Infrastructure Pipeline committing INR 111 trillion (approximately US$ 1.3 trillion) through 2030, creating extensive demand for construction and heavy machinery braking systems.

Japan Industrial Brakes Market Size

Estimated at approximately US$ 130 Mn in 2026, supported by industrial robot density, automotive manufacturing, and precision engineering applications. Japan represents a mature but steadily growing market, led by industrial robot density the highest globally according to the IFR, and ongoing manufacturing modernization in the automotive and precision engineering sectors.

Competitive Landscape

The global Industrial Brakes Market exhibits a moderately fragmented competitive structure, with a mix of large diversified industrial technology corporations and specialized braking system manufacturers. Market leaders, including Dellner Bubenzer, Sibre Siegerland Bremsen GmbH, Kendrion N.V., and AKEBONO BRAKE INDUSTRY Co., Ltd., differentiate through proprietary hydraulic and electromagnetic braking technologies, extensive application engineering capabilities, and global service networks.

Strategic priorities center on expanding application portfolios into wind energy and automation, developing smart braking systems with integrated condition monitoring, and geographic expansion into high-growth Asia Pacific and Middle East markets.

Key Developments:

- In March 2025, Wabtec Corporation announced the acquisition of Dellner Couplers for approximately US$ 970 million, strengthening its rail and industrial motion control portfolio and expanding its global presence in braking and coupling technologies.

- In January 2025, Dellner Bubenzer reported growing demand from Zambian mining operations for its German-engineered industrial braking solutions, reinforcing the company’s strategic expansion into African mining markets as a key growth frontier.

Companies Covered in Industrial Brakes Market

- Dellner Bubenzer

- AKEBONO BRAKE INDUSTRY Co., Ltd.

- AMETEK Inc.

- Danfoss

- Kendrion N.V.

- Regal Rexnord Corporation

- Sibre Siegerland Bremsen GmbH

- The Hilliard Corporation

- TMD Friction Holding GmbH

- Wabtec Corporation

Frequently Asked Questions

The global Industrial Brakes Market is valued at US$ 1.8 Bn in 2026 and is projected to reach US$ 2.5 Bn by 2033, expanding at a CAGR of 4.8% during the forecast period.

The key demand drivers include the global expansion of industrial automation and robotics, increasingly stringent workplace machinery safety regulations such as OSHA standards in the U.S. with penalties up to US$ 165,514 per violation large-scale infrastructure investments in Asia Pacific and North America, and the rapid growth of wind energy installations requiring specialized turbine braking systems.

Disc brakes dominate the market with approximately 55% revenue share, owing to their superior heat dissipation capacity, reliable stopping power under continuous heavy-duty operation, and ease of visual maintenance inspection. Their dominance is especially pronounced in crane and hoist, wind turbine, offshore, and automated manufacturing applications globally.

Asia Pacific is the leading regional market with approximately 36% of global revenue in 2026, driven by China’s massive steel and manufacturing operations, India’s infrastructure investment programs, and expanding mining and industrial activity across ASEAN economies.

Leading companies in the global Industrial Brakes Market include Dellner Bubenzer, AKEBONO BRAKE INDUSTRY Co., Ltd., AMETEK Inc., Danfoss, Kendrion N.V., Regal Rexnord Corporation, Sibre Sieger land Bremsen GmbH, The Hilliard Corporation, TMD Friction Holding GmbH, and Wabtec Corporation, among other global and regional specialists.