- Processed Food

- India Ghee Market

India Ghee Market Size, Share, and Growth Forecast 2026 - 2033

India Ghee Market by Source (Cow Milk Ghee, Buffalo Milk Ghee, Goat Milk Ghee, Others), by Variety (Traditional Ghee, Flavored Ghee, A2 Ghee, Cultured Ghee, Others), by Nature, by End Use Application, by Distribution Channel, by Regional Analysis, 2026 - 2033

India Ghee Market Size and Trend Analysis

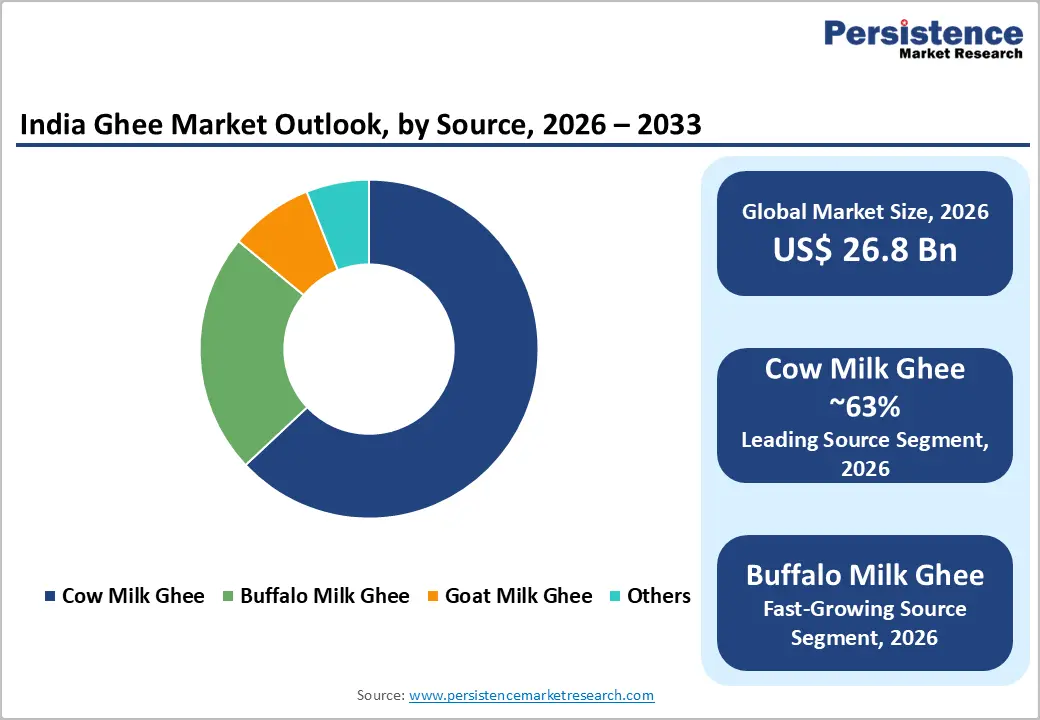

India ghee market size is expected to be valued at US$ 26.8 billion in 2026 and projected to reach US$ 44.0 billion by 2033, growing at a CAGR of 7.4% between 2026 and 2033.

It is experiencing sustained momentum, driven by the deep integration of ghee in Indian culinary traditions, a rising health-conscious urban consumer base, and rapid organized sector expansion. The country's burgeoning middle class, estimated at over 300 million people by the National Council of Applied Economic Research (NCAER) is shifting from unbranded to branded, premium ghee, elevating both value and volume growth.

Additionally, India's foundational position as the world's largest milk producer, as confirmed by the Department of Animal Husbandry and Dairying (DAHD) with annual output exceeding 230 million metric tonnes, provides a robust and cost-competitive raw material base, further reinforcing the market's structural growth trajectory.

Key Industry Highlights:

- Leading Region - North India, encompassing Rajasthan, Uttar Pradesh, Punjab, and Haryana, is the dominant consuming region, accounting for over 40% of domestic ghee demand, driven by deep cultural consumption traditions, high per-capita dairy intake, and strong cooperative dairy infrastructure.

- Fastest Growing Region - South and West Indian states, including Maharashtra, Karnataka, and Tamil Nadu, are the fastest-growing regions, driven by rising urban incomes, Ayurvedic wellness trends, and the rapid proliferation of premium A2 and organic ghee brands in metropolitan retail and e-commerce channels.

- Dominant Segment - Cow milk ghee commands approximately 63% of India's ghee market by source in 2025, underpinned by abundant cow milk supply, cultural preference, and strong brand association through cooperatives like Amul and Patanjali.

- Fastest Growing Segment - A2 ghee is the fastest-growing variety segment, fueled by scientific endorsements, premium pricing acceptance among health-conscious urban consumers, and active breed conservation investments by ICAR, driving rapid volume and value expansion.

- Key Opportunity - The convergence of India's expanding digital consumer base and rising willingness to pay for certified A2, organic, and bilona ghee presents significant revenue upside for brands investing in DTC models, traceability technology, and premium retail partnerships.

Market Dynamics

Drivers - Surging Domestic Milk Production and Government-Backed Dairy Infrastructure

India's position as the world's largest milk producer forms the bedrock of its thriving ghee market. According to the Department of Animal Husbandry and Dairying (DAHD), India's milk production crossed 230.58 million metric tonnes in 2022-23, registering a consistent annual growth rate of approximately 3-4%. Government initiatives such as the National Programme for Dairy Development (NPDD) and the Animal Husbandry Infrastructure Development Fund (AHIDF) worth INR 15,000 crore are strengthening processing capacity, cold-chain networks, and value addition capabilities. This infrastructure expansion directly enables ghee manufacturers to scale production, maintain quality consistency, and reduce per-unit costs. The cooperative model anchored by organisations like GCMMF (Amul) and state dairy federations further channels raw milk supply efficiently, ensuring stable input availability and competitive pricing that drives market volume growth.

Deepening Cultural Integration and Rising Premiumization Trends

Ghee holds an irreplaceable position in Indian culture, used as a cooking medium, a religious offering, and an Ayurvedic health supplement, creating a structurally resilient demand base. According to a 2023 report by the Indian Council of Medical Research (ICMR), ghee consumed in moderate quantities is recognized as a source of beneficial short-chain fatty acids, including butyric acid, supporting gut and metabolic health. This scientific validation, combined with a growing urban awareness of Ayurvedic nutrition, is driving a pronounced premiumization shift. Consumers in Tier-1 and Tier-2 cities are actively trading up from loose/unbranded ghee, which still constitutes an estimated 40-45% of India's total ghee consumption to branded, certified, and specialty variants such as A2 and bilona ghee. This premiumization dynamic is significantly expanding market value per unit, underpinning above-average revenue growth.

Restraints - Fragmented Unorganized Sector and Quality Adulteration Concerns

Despite organized sector growth, India's ghee market continues to be dominated by unbranded and unorganized players who account for an estimated 40-45% of total consumption. Adulteration remains a persistent challenge; the Food Safety and Standards Authority of India (FSSAI) regularly report significant proportions of tested ghee samples failing purity standards. Adulterated products sold at lower price points directly undercut branded players, eroding profit margins and depressing overall market pricing. This limits the pace at which organized manufacturers can gain market share and reduces consumer confidence in product authenticity, particularly in rural and semi-urban markets where regulatory enforcement remains less rigorous.

Volatility in Milk Procurement Prices and Seasonal Supply Constraints

Ghee production is highly sensitive to fluctuations in raw milk procurement prices, which in India are subject to seasonal variation, peak flush season (October-March) and lean season (April-September), creating supply-side unpredictability. According to data from the National Dairy Development Board (NDDB), milk procurement prices have witnessed periodic spikes of 10-15% year-on-year during lean seasons. For manufacturers, this translates into compressed margins unless pass-through pricing is exercised, which can dampen consumer demand at already price-sensitive market segments. Smaller regional ghee producers with limited working capital are particularly vulnerable, restricting their ability to invest in branding, packaging, and distribution enhancements.

Opportunities - A2 Ghee and Organic Certification: High-Value Premiumization

The rapid ascent of A2 ghee derived from indigenous Indian cattle breeds such as Gir, Sahiwal, Tharparkar, and Red Sindhi represents the single most significant premiumization opportunity in India's ghee market. A2 ghee commands retail prices of INR 1,500-INR 3,000 per kilogram, compared to INR 400-INR 600 per kilogram for conventional ghee, translating into dramatically higher value per unit. The Indian Council of Agricultural Research (ICAR) is actively funding genetic conservation programs for A2 cattle breeds, improving herd quality and milk output.

Simultaneously, digital-native brands such as Anveshan Farm Technologies and Aadvik Foods are scaling via e-commerce platforms with strong subscription models. Organic ghee certified under India Organic (NPOP) standards is gaining shelf space in premium urban retail and export markets. Manufacturers investing in breed-specific sourcing, bilona production methods, and transparent traceability can unlock disproportionate revenue premiums in the coming years.

E-Commerce Expansion and Direct-to-Consumer Model Adoption

India's rapid e-commerce penetration with the Ministry of Electronics and Information Technology (MeitY) projecting the domestic e-commerce market to reach US$ 350 billion by 2030, is creating a transformational distribution channel for ghee brands.

Online platforms, including Amazon India, Flipkart, BigBasket, and JioMart are enabling ghee brands to reach consumers beyond traditional organized retail geographies. Direct-to-consumer (DTC) models adopted by emerging brands like Anveshan and Go Desi are demonstrating that subscription-based ghee delivery can build strong brand loyalty with lower customer acquisition costs. According to NASSCOM, India added over 100 million new online shoppers between 2021 and 2024, predominantly from Tier-2 and Tier-3 cities. This expanding digital consumer base offers ghee brands a cost-efficient route to grow nationally without heavy brick-and-mortar retail investment, significantly lowering barriers to scale.

Category-wise Analysis

Source Insights

Cow milk ghee commands the dominant position within India's ghee market by source, holding an estimated 63% market share in 2025. This supremacy is deeply rooted in India's dairy composition: according to the Department of Animal Husbandry and Dairying (DAHD), cow milk constitutes approximately 50% of India's total milk production, with an expanding base of indigenous and crossbred cattle herds. Cultural and religious preference for cow-derived products particularly in North and Western India, further reinforces this segment's dominance. The rising popularity of A2 cow milk ghee from Desi breeds such as Gir and Sahiwal is further strengthening cow milk's share within the premium sub-segment. Leading brands including Amul and Patanjali Ayurved, predominantly use cow milk for their flagship ghee product lines, entrenching category leadership through brand equity and mass distribution.

Variety Insights

Traditional ghee holds the leading position in the variety segment, accounting for approximately 54% of India's ghee market by variety in 2025. Prepared using conventional cream method or curd-based churning, traditional ghee resonates deeply with India's cultural and culinary heritage. The Food Safety and Standards Authority of India (FSSAI) has defined specific standards for traditional ghee under the Food Safety and Standards (Food Products Standards and Food Additives) Regulations, 2011, lending regulatory clarity and consumer confidence.

Across the country's diverse regional cuisines, Punjabi, Rajasthani, Bengali, and South Indian traditional ghee remains the preferred cooking fat. While A2 and cultured ghee are gaining traction in urban premium segments, traditional ghee's affordability and familiar sensory profile (colour, aroma, texture) ensure its entrenched dominance across both rural and urban mass-market consumer groups.

Distribution Channel Insights

Supermarkets and hypermarkets constitute the leading organized distribution channel for branded ghee in India, capturing an estimated 35% of total market distribution in 2025. Organized retail chains such as Reliance Retail, D-Mart, Big Bazaar, and Spencer's provide branded ghee manufacturers with high-visibility shelf placements and access to urban middle-class consumers. However, India's traditional trade, including kirana stores and mandis, continues to account for most overall sales when both organized and unorganized segments are considered.

Online retail is the fastest-growing channel: platforms such as BigBasket, Amazon India, and Flipkart Grocery are enabling premium ghee brands to reach digitally savvy, health-conscious consumers directly, bypassing multi-layer distribution infrastructure and supporting margin expansion for branded players.

Competitive Landscape

India's ghee market is moderately fragmented, with a mix of dominant national cooperatives, established private dairy companies, regional players, and a rapidly growing segment of artisan DTC brands. GCMMF (Amul) commands overall market leadership through its pan-India distribution network of over 3.5 million retail outlets and strong cooperative procurement. Patanjali Ayurved has disrupted the market through aggressive pricing and Ayurvedic positioning.

Key differentiators across the competitive landscape include A2 certification, bilona method authentication, organic credentials, and digital-first marketing. Premium DTC brands like Anveshan and Aadvik Foods are leveraging social commerce and subscription models to build loyal urban consumer bases, signaling an emerging bifurcation between mass-market cooperatives and premium artisan players.

Key Developments:

- In November 2026, Karnataka’s flagship Nandini ghee, produced by the Karnataka Milk Federation (KMF), marked its international debut with exports to Australia, the U.S., and Saudi Arabia.

- February 2025: GCMMF (Amul) expanded its premium ghee portfolio by launching single-origin Gir cow A2 ghee in 250g and 500g formats, targeting India's fast-growing urban wellness consumer segment through modern retail and Amazon India.

- September 2024: Patanjali Ayurved Limited announced a capacity expansion at its Haridwar dairy plant, increasing ghee processing capacity by 30%, aimed at meeting surging demand across North India and enhancing its export capabilities to Gulf markets.

India Ghee Market Report - Key Insights & Details

| India Market Attributes | Key Insights |

|---|---|

| Historical Market Value (2020) | US$ 18.7 Billion |

| Projected Market Value (2026) | US$ 26.8 Billion |

| Projected Market Value (2033) | US$ 44.0 Billion |

| CAGR (2026 - 2033) | 7.4% |

| Top-ranking Product | Cow Milk Ghee, 63% share |

| Incremental Opportunity | US$ 17.2 Billion |

Companies Covered in India Ghee Market

- GCMMF (Amul)

- Heritage Foods Limited

- Patanjali Ayurved Limited

- Verka

- ITC Limited

- Paras Dairy

- RKG Ghee

- Saputo Inc.

- Britannia Industries

- Simple Truth Organic

- Aadvik Foods

- Ancient Organics

- 4th & Heart

- Anveshan Farm Technologies Pvt. Ltd.

- Others

Frequently Asked Questions

India Ghee market is expected to be valued at US$ 26.8 billion in 2026.

India’s ghee market grows due to high milk production, government support, cultural usage, and rising demand for premium A2/organic variants.

Key opportunity lies in premium A2/organic ghee expansion via e-commerce and DTC channels, enabling higher margins and scalable distribution.

The leading players include GCMMF (Amul), Patanjali Ayurved Limited, Heritage Foods Limited, Verka, ITC Limited, Paras Dairy, Parag Milk Foods (Govardhan), and Mother Dairy.