- Executive Summary

- Global Hospital Workforce Management Market Snapshot, 2026 and 2033

- Market Opportunity Assessment, 2026 - 2033, US$ Bn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Key Trends

- Macro-Economic Factors

- Global Sectorial Outlook

- Global GDP Growth Outlook

- COVID-19 Impact Analysis

- Forecast Factors - Relevance and Impact

- Value Added Insights

- Product Adoption Analysis

- Recent Product Launches

- Regulatory Landscape

- Value Chain Analysis

- Key Deals and Mergers

- PESTLE Analysis

- Porter’s Five Force Analysis

- Price Trend Analysis, 2020 - 2033

- Key Highlights

- Key Factors Impacting Product Prices

- Pricing Analysis, By Product Type

- Regional Prices and Product Preferences

- Global Hospital Workforce Management Market Outlook:

- Key Highlights

- Market Size (US$ Bn) and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Bn) Analysis and Forecast

- Historical Market Size (US$ Bn) Analysis, 2020-2025

- Market Size (US$ Bn) Analysis and Forecast, 2026-2033

- Global Hospital Workforce Management Market Outlook: Product

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis and Volume (Units) Analysis, By Product, 2020 - 2025

- Market Size (US$ Bn) Analysis and Volume (Units) Analysis and Forecast, By Product, 2026 - 2033

- Software

- Standalone Software

- Time and Attendance

- HR AND PAYROLL

- Scheduling

- Talent Management

- Reporting & Analytics

- Others

- Integrated Software

- Standalone Software

- Services

- Software

- Market Attractiveness Analysis: By Product

- Global Hospital Workforce Management Market Outlook: Mode of Delivery

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By Mode of Delivery, 2020 - 2025

- Market Size (US$ Bn) Analysis and Forecast, By Mode of Delivery, 2026 - 2033

- Cloud Based

- On-Premise

- Market Attractiveness Analysis: Mode of Delivery

- Global Hospital Workforce Management Market Outlook: End User

- Introduction / Key Findings

- Historical Market Size (US$ Bn) Analysis, By End User, 2020 - 2025

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2026 - 2033

- Assisted Living Centers

- Long-term Care Centers

- Nursing Homes Centers

- Assisted Living Centers

- Others

- Market Attractiveness Analysis: End User

- Key Highlights

- Global Hospital Workforce Management Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Region, 2020 - 2025

- Market Size (US$ Bn) Analysis and Forecast, By Region, 2026 - 2033

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Hospital Workforce Management Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Product

- By Mode of Delivery

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- U.S.

- Canada

- Market Size (US$ Bn) Analysis and Volume (Units) Analysis and Forecast, By Product, 2026 - 2033

- Software

- Standalone Software

- Time and Attendance

- HR AND PAYROLL

- Scheduling

- Talent Management

- Reporting & Analytics

- Others

- Integrated Software

- Standalone Software

- Services

- Software

- Market Size (US$ Bn) Analysis and Forecast, By Mode of Delivery, 2026 - 2033

- Cloud Based

- On-Premise

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2026 - 2033

- Assisted Living Centers

- Long-term Care Centers

- Nursing Homes Centers

- Assisted Living Centers

- Others

- Market Attractiveness Analysis

- Europe Hospital Workforce Management Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Product

- By Mode of Delivery

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Rest of Europe

- Market Size (US$ Bn) Analysis and Volume (Units) Analysis and Forecast, By Product, 2026 - 2033

- Software

- Standalone Software

- Time and Attendance

- HR AND PAYROLL

- Scheduling

- Talent Management

- Reporting & Analytics

- Others

- Integrated Software

- Standalone Software

- Services

- Software

- Market Size (US$ Bn) Analysis and Forecast, By Mode of Delivery, 2026 - 2033

- Cloud Based

- On-Premise

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2026 - 2033

- Assisted Living Centers

- Long-term Care Centers

- Nursing Homes Centers

- Assisted Living Centers

- Others

- Market Attractiveness Analysis

- East Asia Hospital Workforce Management Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Product

- By Mode of Delivery

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- China

- Japan

- South Korea

- Market Size (US$ Bn) Analysis and Volume (Units) Analysis and Forecast, By Product, 2026 - 2033

- Software

- Standalone Software

- Time and Attendance

- HR AND PAYROLL

- Scheduling

- Talent Management

- Reporting & Analytics

- Others

- Integrated Software

- Standalone Software

- Services

- Software

- Market Size (US$ Bn) Analysis and Forecast, By Mode of Delivery, 2026 - 2033

- Cloud Based

- On-Premise

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2026 - 2033

- Assisted Living Centers

- Long-term Care Centers

- Nursing Homes Centers

- Assisted Living Centers

- Others

- Market Attractiveness Analysis

- South Asia & Oceania Hospital Workforce Management Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Product

- By Mode of Delivery

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Market Size (US$ Bn) Analysis and Volume (Units) Analysis and Forecast, By Product, 2026 - 2033

- Software

- Standalone Software

- Time and Attendance

- HR AND PAYROLL

- Scheduling

- Talent Management

- Reporting & Analytics

- Others

- Integrated Software

- Standalone Software

- Services

- Software

- Market Size (US$ Bn) Analysis and Forecast, By Mode of Delivery, 2026 - 2033

- Cloud Based

- On-Premise

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2026 - 2033

- Assisted Living Centers

- Long-term Care Centers

- Nursing Homes Centers

- Assisted Living Centers

- Others

- Market Attractiveness Analysis

- Latin America Hospital Workforce Management Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Product

- By Mode of Delivery

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- Brazil

- Mexico

- Rest of Latin America

- Market Size (US$ Bn) Analysis and Volume (Units) Analysis and Forecast, By Product, 2026 - 2033

- Software

- Standalone Software

- Time and Attendance

- HR AND PAYROLL

- Scheduling

- Talent Management

- Reporting & Analytics

- Others

- Integrated Software

- Standalone Software

- Services

- Software

- Market Size (US$ Bn) Analysis and Forecast, By Mode of Delivery, 2026 - 2033

- Cloud Based

- On-Premise

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2026 - 2033

- Assisted Living Centers

- Long-term Care Centers

- Nursing Homes Centers

- Assisted Living Centers

- Others

- Market Attractiveness Analysis

- Middle East & Africa Hospital Workforce Management Market Outlook:

- Key Highlights

- Historical Market Size (US$ Bn) Analysis, By Market, 2020 - 2025

- By Country

- By Product

- By Mode of Delivery

- By End User

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2026 - 2033

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Market Size (US$ Bn) Analysis and Volume (Units) Analysis and Forecast, By Product, 2026 - 2033

- Software

- Standalone Software

- Time and Attendance

- HR AND PAYROLL

- Scheduling

- Talent Management

- Reporting & Analytics

- Others

- Integrated Software

- Standalone Software

- Services

- Software

- Market Size (US$ Bn) Analysis and Forecast, By Mode of Delivery, 2026 - 2033

- Cloud Based

- On-Premise

- Market Size (US$ Bn) Analysis and Forecast, By End User, 2026 - 2033

- Assisted Living Centers

- Long-term Care Centers

- Nursing Homes Centers

- Assisted Living Centers

- Others

- Market Attractiveness Analysis

- Competition Landscape

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Company Profiles (Details - Overview, Recent Developments)

- IBM Corporation

- Overview

- Segments and Product & End User

- Key Financials

- Market Developments

- Market Strategy

- McKesson Corporation

- UKG (Ultimate Kronos Group)

- Cornerstone

- Oracle Corporation

- ATOSS Software AG

- Workday, Inc.

- NICE Ltd.

- Infor, Inc.

- RLDatix

- SAP SE

- ADP, LLC

- Strata Decision Technology, LLC

- WorkForce Software, LLC

- Symplr, Inc.

- Others

- IBM Corporation

- Market Structure

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Healthcare Services

- Hospital Workforce Management Market

Hospital Workforce Management Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Hospital Workforce Management Market by Product (Software and Services), by Mode of Delivery (Cloud-based and On-Premise), End-user (Hospitals, Long-term Care Centers, Nursing Homes Centers, Assisted Living Centers, and Others), and Regional Analysis from 2026 to 2033

Key Industry Highlights:

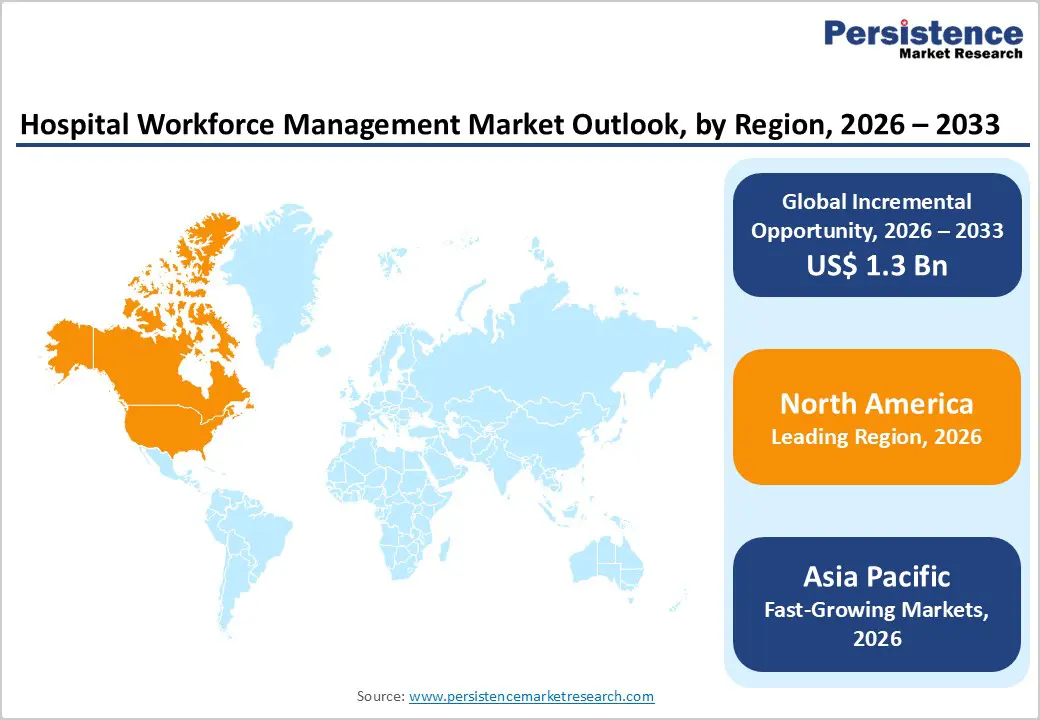

- Leading Region: North America accounts for 47.3% of total revenue, supported by mature healthcare IT infrastructure, strong digital spending capacity, and early deployment of enterprise labor analytics platforms.

- Fastest-Growing Region: Asia Pacific is witnessing the fastest expansion, fueled by hospital digitization programs, increasing private healthcare investment, and rapid scaling of organized hospital networks.

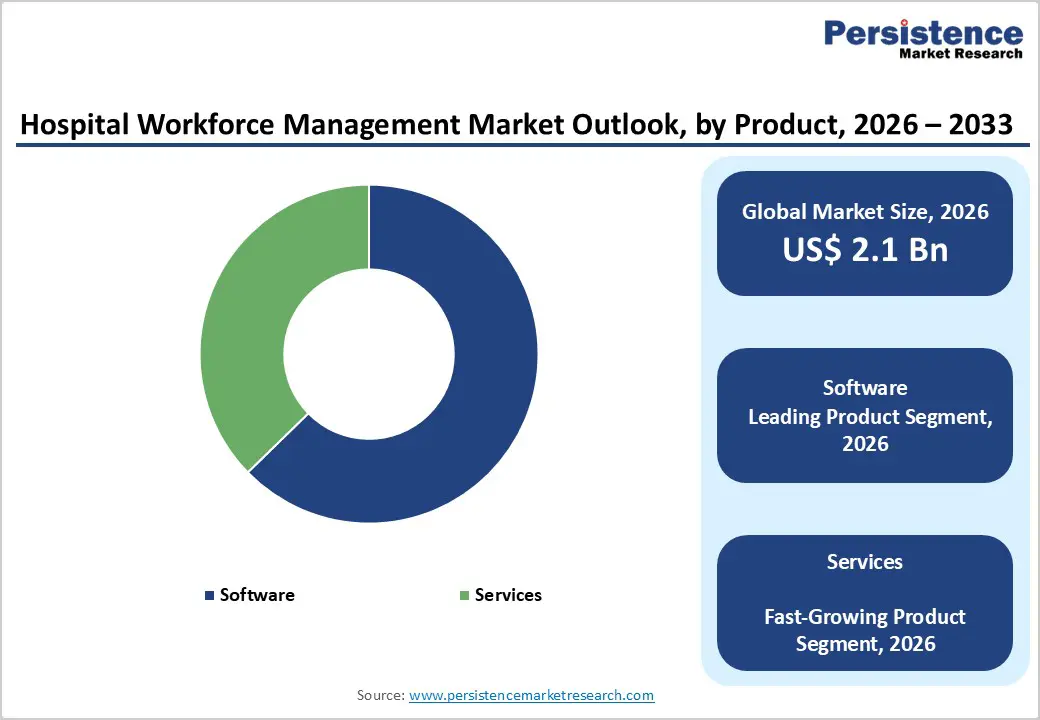

- Leading Product Segment: Software captures 39.6% share, reflecting high utilization of automated scheduling, compliance monitoring, and workforce analytics solutions across hospital systems.

- Fastest-Growing Product Segment: Services are expanding rapidly as healthcare providers increasingly require implementation support, system integration, workforce consulting, ongoing technical maintenance, and optimization services to maximize platform efficiency and ensure seamless digital transformation.

- Leading Mode of Delivery Segment: Cloud based leads with 20.0% share, supported by expanding regenerative medicine programs and increasing focus on cell differentiation and tissue regeneration studies.

- Fastest-Growing Mode of Delivery Segment: On-premise solutions continue to grow steadily, particularly among institutions requiring strict internal data governance and customized infrastructure control.

| Key Insights | Details |

|---|---|

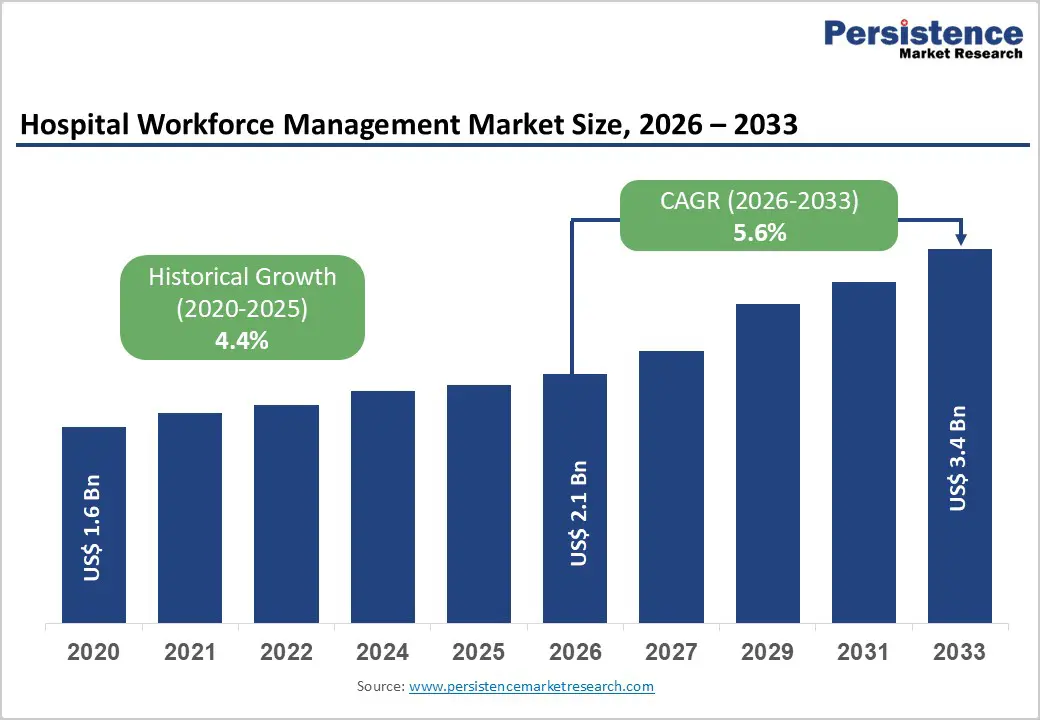

| Hospital Workforce Management Market Size (2026E) | US 2.1 Bn |

| Market Value Forecast (2033F) | US$ 3.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.4% |

Market Dynamics

Driver - Growing Workforce Shortages and Rising Demand for Intelligent Staffing Optimization

Healthcare systems globally are confronting persistent staffing shortages, increasing patient volumes, and mounting regulatory oversight, all of which are accelerating investment in advanced workforce management technologies. Hospitals operate in high-acuity environments where improper staff allocation directly affects patient safety, clinical outcomes, and financial stability. Traditional manual scheduling practices lack the analytical depth required to manage fluctuating census levels, specialty skill mix requirements, and overtime exposure. Modern digital platforms incorporate predictive analytics and demand forecasting algorithms that align workforce capacity with real-time patient inflow and historical utilization patterns. Growing labor expenses, particularly for nursing staff, are compelling administrators to deploy automation tools that reduce premium pay, minimize burnout, and improve retention. Compliance with labor laws, accreditation standards, and union agreements further necessitates transparent tracking systems capable of audit-ready reporting.

Additionally, expansion of multi-site hospital networks requires centralized visibility across facilities, encouraging adoption of interoperable cloud-based systems. Integration with electronic health records and enterprise resource planning platforms enhances operational cohesion. As healthcare organizations prioritize efficiency, accountability, and data-driven decision-making, intelligent workforce optimization solutions are becoming indispensable to sustaining service quality and financial performance.

Restraints - Integration Complexities, Budget Constraints, and Organizational Resistance to Digital Transition

Despite clear efficiency benefits, the implementation of workforce management platforms presents structural and financial barriers. Many hospitals continue to operate on legacy IT infrastructure, making system integration technically demanding and resource-intensive. Migrating historical workforce data, ensuring interoperability with payroll systems, and maintaining cybersecurity compliance can extend deployment timelines. Smaller healthcare facilities, particularly in emerging markets, often face capital budget limitations that delay procurement decisions. Operational resistance also poses a challenge. Clinical staff accustomed to manual rostering methods may hesitate to adopt algorithm-driven scheduling tools, particularly when transparency alters long-standing work allocation practices. Training requirements, change management initiatives, and workflow redesign increase administrative burden during early transition phases.

Data privacy regulations add further complexity, especially in regions with stringent compliance mandates. Concerns about cloud security and data sovereignty can slow adoption among conservative institutions. Additionally, rapid technological evolution occasionally results in platform obsolescence, creating uncertainty around long-term return on investment. Collectively, financial caution, interoperability constraints, and organizational inertia continue to moderate full-scale deployment across certain healthcare environments.

Opportunity - AI-Enabled Workforce Analytics, Remote Accessibility, and Expansion into Long-Term Care Ecosystems

Significant growth potential lies in the integration of artificial intelligence and advanced analytics into workforce management ecosystems. Predictive staffing models capable of analyzing admission trends, seasonal illness patterns, and departmental acuity levels provide administrators with proactive planning capabilities. Real-time mobile applications empower clinicians to manage shift swaps, availability updates, and attendance tracking remotely, enhancing workforce engagement and flexibility. Expansion beyond acute-care hospitals into long-term care centers, assisted living facilities, and community health networks presents an additional avenue for revenue generation. Aging populations and chronic disease prevalence are increasing demand for structured staffing oversight in extended care environments. Cloud-native architectures offer scalable subscription models suitable for decentralized facilities with limited IT infrastructure.

Technological convergence with performance benchmarking, payroll automation, and financial analytics further enhances value propositions for executive leadership. Emerging markets investing in healthcare digitization initiatives represent untapped demand pools. Strategic partnerships between technology vendors and healthcare providers are accelerating customization and localization efforts. As operational efficiency and workforce sustainability gain prominence, digitally enabled labor management platforms are positioned to capture sustained expansion opportunities across diversified care settings.

Category-wise Analysis

By Product Insights

Software is projected to account for 62.7% of global revenue in 2026 within the hospital workforce management market. Leadership is attributed to the broad deployment of integrated scheduling engines, time and attendance modules, payroll interfaces, compliance tracking, and predictive labor analytics. Hospitals increasingly prioritize digital workforce platforms to reduce overtime expenses, manage unionized staffing structures, and maintain accreditation standards. Advanced solutions incorporate AI-driven forecasting to align staffing levels with fluctuating patient volumes and acuity metrics. Seamless interoperability with electronic health records (EHRs), ERP systems, and financial platforms further strengthens enterprise adoption. Additionally, configurable dashboards and real-time performance monitoring tools enhance administrative decision-making. Growing emphasis on workforce transparency, labor optimization, and regulatory reporting continues to reinforce software as the primary revenue contributor globally, while service components remain essential for implementation and long-term system optimization.

By Mode of Delivery Insights

Cloud-based solutions are expected to hold 75.0% of market revenue in 2026, reflecting accelerated digital transformation across healthcare institutions. Hospitals are transitioning away from legacy infrastructure toward subscription-based platforms that offer remote accessibility, automated upgrades, and centralized data management. Cloud architecture enables rapid system deployment across multi-site hospital networks without significant capital expenditure. Enhanced cybersecurity frameworks, compliance certifications, and encrypted data environments have improved confidence in hosted models. Moreover, cloud platforms support mobile workforce applications, enabling staff to access schedules, shift swaps, and attendance logs in real time. Integration capabilities with third-party HR, finance, and clinical systems improve operational coherence. As healthcare organizations pursue cost containment and IT simplification strategies, cloud-based workforce management platforms continue to demonstrate superior flexibility, driving sustained dominance over on-premise alternatives.

By End-user, Hospitals Lead Due to Complex Staffing Structures and High Workforce Density

Hospitals are anticipated to command 55.9% of the global market share in 2026, making them the largest end-user category. Acute care environments operate with multidisciplinary teams, rotating shifts, emergency coverage requirements, and strict compliance mandates, necessitating advanced workforce coordination tools. Implementation of automated rostering and acuity-based staffing models enhances patient care continuity while minimizing burnout risks. Rising patient admissions, expansion of specialty departments, and increasing regulatory scrutiny further elevate demand for digital labor management systems. Financial pressures to optimize staffing costs without compromising clinical quality are also accelerating procurement. Integration of workforce analytics with performance metrics supports strategic planning and resource allocation. As hospitals continue modernizing administrative infrastructure to improve efficiency and accountability, they remain the primary revenue-generating segment within the global hospital workforce management ecosystem.

Regional Insights

North America Hospital Workforce Management Market Trends

North America is projected to maintain the largest share, accounting for 47.3% of global revenue in 2026. Market leadership is underpinned by the United States’ advanced healthcare IT ecosystem and early adoption of enterprise workforce technologies. Large hospital networks across the region actively invest in digital staffing optimization tools to address persistent nurse shortages and rising labor expenditures. Regulatory frameworks emphasizing transparency in workforce reporting and patient safety standards further stimulate software deployment.

Healthcare providers are increasingly implementing predictive scheduling algorithms to manage seasonal admission variability and emergency department congestion. Additionally, strong presence of established health IT vendors and cloud infrastructure providers ensures rapid innovation cycles and technical support availability. Integration of workforce management with revenue cycle systems and enterprise resource planning platforms enhances administrative efficiency. Continuous modernization initiatives, combined with high healthcare spending and strong digital maturity, position North America as the dominant contributor to overall market revenue.

Europe Hospital Workforce Management Market Trends

Europe demonstrates steady expansion supported by structured healthcare systems and ongoing digitization reforms. Governments across Germany, the United Kingdom, France, Italy, and Spain are promoting hospital IT modernization to enhance operational transparency and labor efficiency. Increasing workforce shortages, particularly in nursing and geriatric care, are prompting healthcare administrators to adopt automated scheduling and compliance monitoring tools. Data protection regulations such as GDPR have influenced procurement decisions, encouraging adoption of secure, standards-compliant cloud platforms. Cross-border collaborations and public health initiatives also foster technology exchange within the region.

Hospitals are leveraging analytics-driven workforce planning to balance cost control with quality-of-care objectives. Furthermore, investments in smart hospital infrastructure and centralized digital records create favorable conditions for system integration. While growth is moderate compared to emerging economies, Europe remains an innovation-focused and regulation-driven market characterized by structured adoption and consistent demand for scalable workforce solutions.

Asia Pacific Hospital Workforce Management Market Trends

Asia Pacific is forecast to record the fastest expansion, registering a CAGR of approximately 7.6% between 2026 and 2033. Rapid healthcare infrastructure development across China, India, Japan, South Korea, and Australia is generating substantial demand for digital administrative platforms. Growing patient volumes, urban hospital expansion, and increasing private healthcare investment necessitate efficient workforce coordination systems. Governments are encouraging hospital digitization through national e-health initiatives and funding programs aimed at improving service delivery standards. Rising awareness of labor optimization, combined with expanding hospital chains, supports adoption of scalable cloud-based solutions.

Regional providers are also partnering with global software vendors to enhance technical capabilities and system interoperability. As healthcare systems modernize and workforce complexity intensifies, Asia Pacific is emerging as the most dynamic growth engine within the global hospital workforce management market, driven by cost sensitivity, scalability requirements, and digital transformation momentum.

Competitive Landscape

The global hospital workforce management market is highly competitive, with strong participation from IBM Corporation, McKesson Corporation, UKG (Ultimate Kronos Group), Cornerstone, Oracle Corporation, and ATOSS Software AG. These companies leverage established brand positioning, extensive global client bases, and advanced workforce analytics capabilities to address the growing need for staffing optimization and regulatory compliance in healthcare settings.

Their portfolios focus on cloud-based workforce platforms, real-time scheduling tools, time and attendance systems, labor cost analytics, and AI-enabled demand forecasting solutions. Continuous platform enhancements, strategic partnerships, interoperability with hospital IT systems, and compliance with healthcare regulations remain critical for sustaining competitive advantage and long-term market leadership.

Key Industry Developments:

- In November 2025, ADP® introduced the ADP® WorkForce Suite across ADP Workforce Now®, ADP® Lyric HCM, and ADP Global Payroll®, expanding access to advanced time tracking, scheduling, absence management, and workforce analytics tools in over 140 countries. Following its 2024 acquisition of WorkForce Software, ADP now offers organizations with 150+ employees a unified global platform to manage workforce operations efficiently across multiple geographies.

- In September 2025, Accenture announced a strategic collaboration with UKG (Ultimate Kronos Group) to enhance and modernize hospital workforce management operations through integrated digital solutions. The partnership focuses on improving staffing efficiency, workforce visibility, and data-driven decision-making across healthcare systems.

- In August 2025, MedLern collaborated with Mediversal Hospital to implement a digital learning platform focused on staff upskilling, compliance tracking, and performance improvement. The solution offers mobile-based training modules and real-time assessments to strengthen workforce readiness and enhance patient care standards.

Companies Covered in Hospital Workforce Management Market

- IBM Corporation

- McKesson Corporation

- UKG (Ultimate Kronos Group)

- Cornerstone

- Oracle Corporation

- ATOSS Software AG

- Workday, Inc.

- NICE Ltd.

- Infor, Inc.

- RLDatix

- SAP SE

- ADP, LLC

- Strata Decision Technology, LLC

- WorkForce Software, LLC

- Symplr, Inc.

- Others

Frequently Asked Questions

The global hospital workforce management market is projected to be valued at US$ 2.1 Bn in 2026.

Rising healthcare labor shortages, regulatory compliance pressure, and increasing adoption of cloud-based digital workforce optimization solutions.

The global hospital workforce management market is poised to witness a CAGR of 5.6% between 2026 and 2033.

AI-driven predictive staffing, expansion in long-term care facilities, and integration of workforce platforms with hospital ERP and clinical systems.

IBM Corporation, McKesson Corporation, UKG (Ultimate Kronos Group), Cornerstone Oracle Corporation, and ATOSS Software AG are some of the key players in the hospital workforce management market.