- Processed Food

- Hoisin Sauce Market

Hoisin Sauce Market Size, Share, Trends, Growth, Regional Forecasts, 2026 to 2033

Hoisin Sauce Market by Packaging (Glass Bottles, Plastic Bottles, Pouches), Distribution Channel (Supermarket, Online Retail), Product Type (Organic, Conventional), and Regional Analysis for 2026-2033

Hoisin Sauce Market Share and Trends Analysis

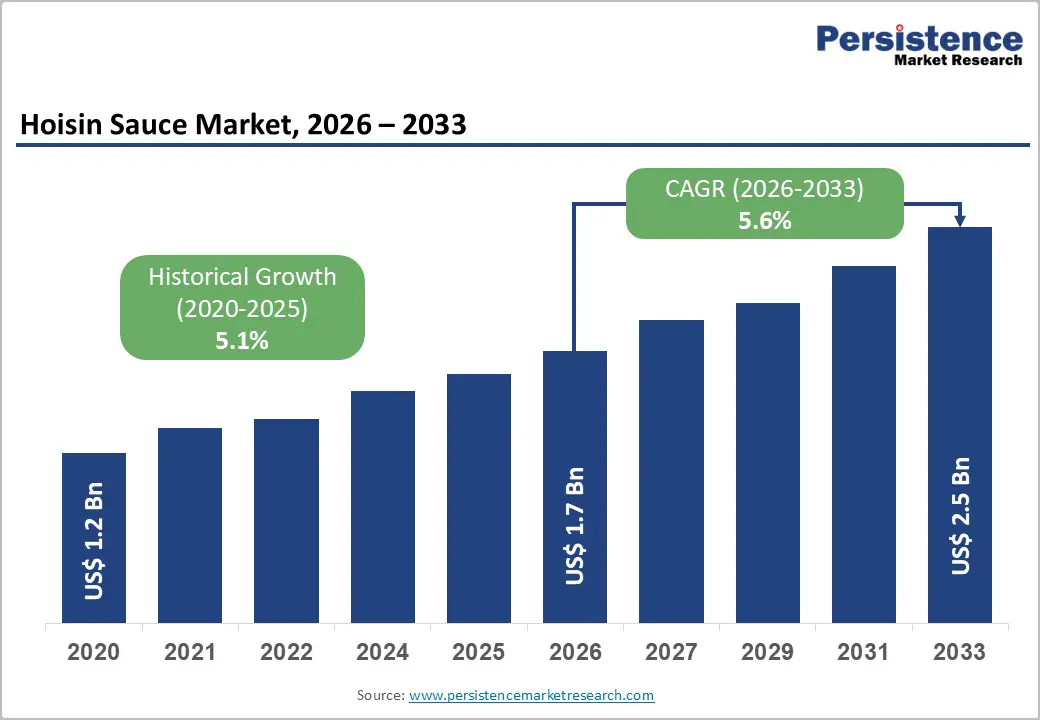

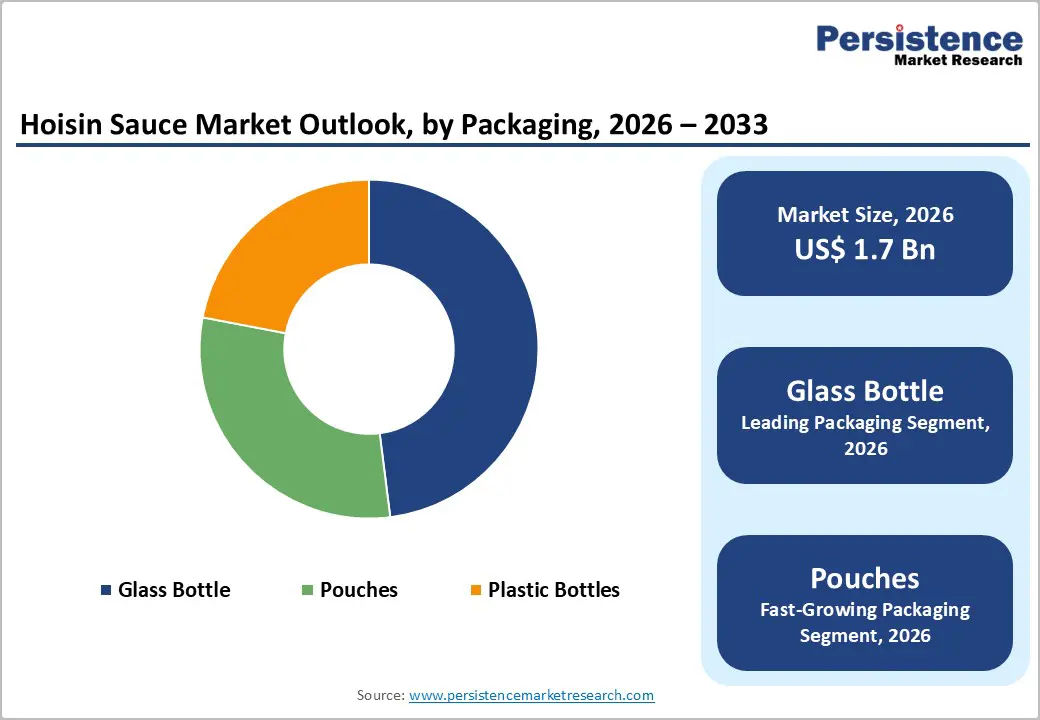

The global hoisin sauce market size is likely to be valued at US$ 1.7 billion in 2026, and is projected to reach US$ 2.5 billion by 2033, growing at a CAGR of 5.6% during the forecast period 2026−2033.

The market's upward momentum is principally driven by rising global consumer appetite for authentic Asian cuisine, growing penetration of hoisin sauce in Western retail and food-service channels, and expanding e-commerce-enabled access across emerging economies. Technological advancements in clean-label formulation and natural preservation are opening premium product tiers, while modern retail-channel diversification particularly omnichannel and direct-to-consumer models is accelerating household penetration.

Key Industry Highlights

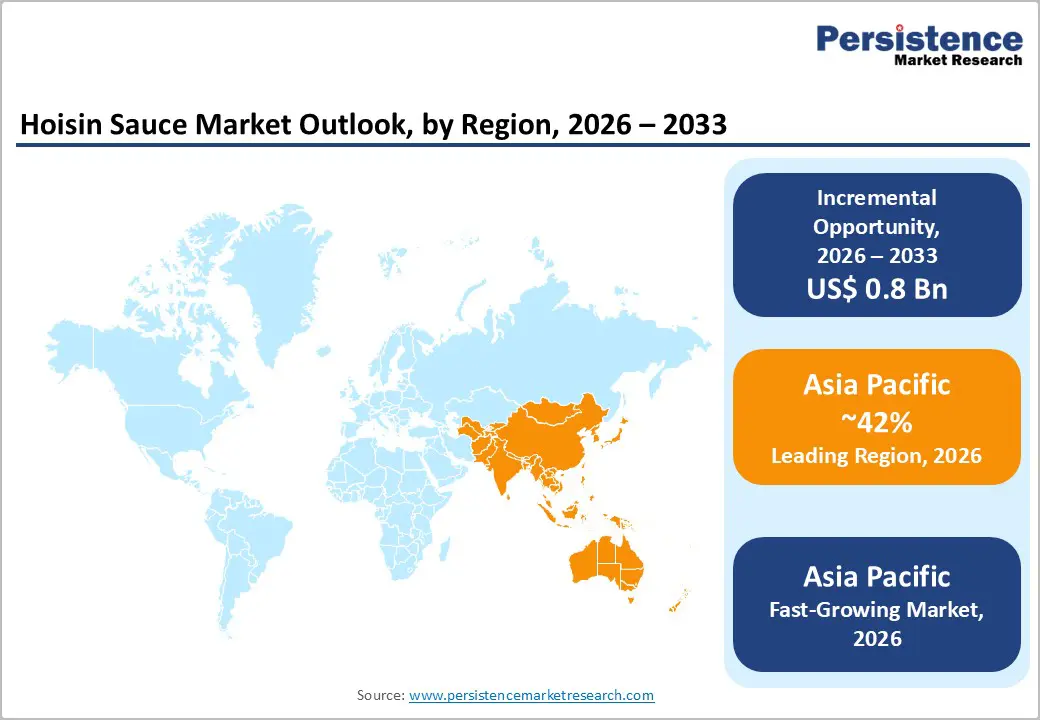

- Dominant Region & Fastest-growing Market: Asia Pacific is likely to dominate in 2026, holding around 42% market share, and the regional market is set to grow the fastest through 2033, backed by robust production capabilities with culturally-rooted consumption patterns.

- Leading & Fastest-growing Packaging: Glass is set to lead with approximately 48% market revenue share in 2026, with pouches growing the fastest during the 2026-2033 forecast period.

- Leading & Fastest-growing Distribution Channel: Supermarkets are projected to capture roughly 50% of the market revenue share in 2026, while online retail is expected to be the fastest-growing segment over the 2026-2033 forecast period.

- Major Driver: The growing adoption of Asian cuisine around the world is foreseen to boost the demand for authentic condiments, particularly in Chinese, Vietnamese, and Pan-Asian culinary traditions, benefitting the market.

| Key Insights | Details |

|---|---|

| Hoisin Sauce Market Size (2026E) | US$ 1.7 Bn |

| Market Value Forecast (2033F) | US$ 2.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.1% |

DRO Analysis

Rising Global Demand for Asian Culinary Experiences

The global spread of Asian cuisine is steadily strengthening demand for authentic condiments, especially within Chinese, Vietnamese, and broader Pan-Asian culinary traditions. Hoisin sauce is becoming a key ingredient as chefs and home cooks are continuing to adopt traditional flavor profiles in everyday meals. Restaurants are increasingly incorporating Asian-inspired dishes into their menus as they are responding to evolving consumer tastes. Food manufacturers are expanding their product lines to include region-specific sauces that are reflecting authenticity and quality. This shift is not only influencing food service channels but is also shaping retail shelves, where consumers are seeking convenient yet traditional options for home cooking.

Younger consumers, particularly millennials and Generation Z (Gen Z), are playing a central role in this transformation as they are actively exploring diverse cuisines and bold flavors. Their interest in cultural food experiences is driving experimentation in both dining and cooking habits. Retailers are responding by offering a wider range of international condiments, while brands are focusing on clean labels and premium ingredients. In the coming years, the market will have evolved to emphasize authenticity, sustainability, and convenience. This ongoing trend is strengthening global culinary integration and is positioning Asian sauces as essential components in modern kitchens.

Health & Wellness Reformulation Driving Premiumization

Rising awareness of healthy eating is encouraging food manufacturers to reformulate hoisin sauce with cleaner and simpler ingredients. Companies are actively developing variants that are low in sodium, free from genetically modified organisms, and suitable for gluten-sensitive consumers. These changes are aligning with evolving regulatory expectations set by the U.S. Food and Drug Administration (FDA) and the European Food Safety Authority, both of which are strengthening transparency in food labeling. As a result, producers are prioritizing clear ingredient disclosure and natural sourcing practices. This shift is helping brands build trust while also meeting the expectations of informed consumers who are carefully evaluating product labels before purchase.

Premiumization is gaining momentum as brands are positioning clean-label hoisin sauces as high-quality offerings. Consumers are increasingly willing to pay more for products that support health and wellness goals. This trend is expanding the total addressable market (TAM) by attracting individuals who previously avoided traditional condiments due to dietary concerns. Retailers are also dedicating more shelf space to better-for-you alternatives, which is improving product visibility and accessibility. Market has evolved to emphasize functional benefits alongside authentic flavor profiles, bolstering long-term growth prospects.

Intense Market Competition and Private Label Proliferation

The hoisin sauce market is experiencing rising competition as established multinational condiment companies are competing with private-label and store-brand products introduced by large retail chains. Retailers are actively expanding their in-house offerings to capture value-conscious consumers, which is increasing pressure on branded manufacturers. These private-label products are often positioned at lower price points while maintaining acceptable quality standards. Leading brands are adjusting their pricing strategies and promotional efforts to remain competitive. This environment is reducing profit margins and is challenging companies to balance cost efficiency with product quality. Strong retail control over shelf placement is influencing purchasing decisions and limiting brand visibility for smaller players.

The market is also becoming highly fragmented as numerous regional and artisanal producers are entering the space with specialized offerings. This diversity is creating challenges for differentiation, as consumers are facing a wide range of similar products. Companies are responding by focusing on branding, packaging innovation, and unique flavor profiles to stand out. In emerging markets, price sensitivity is playing a larger role, which is further intensifying competition. Companies will have been investing more in product innovation and targeted marketing to strengthen their market position and maintain consumer loyalty.

Raw Material Price Volatility

Hoisin sauce production is relying heavily on agricultural inputs such as fermented soybean paste, garlic, vinegar, and sweeteners, all of which are experiencing frequent price fluctuations. These variations are being influenced by changing weather patterns, geopolitical tensions, and ongoing disruptions in global logistics networks. Producers are continuously adjusting sourcing strategies to manage these uncertainties, yet cost volatility is making it difficult to maintain stable pricing. As input expenses are rising unpredictably, manufacturers are facing challenges in protecting profit margins while ensuring consistent product quality.

Smaller and mid-sized companies are experiencing greater pressure as they are lacking the large-scale procurement advantages held by multinational competitors. These businesses are often operating with limited bargaining power, which is reducing their ability to absorb sudden cost increases. Supply chain instability is continuing to create delays and inefficiencies in production planning. Companies are increasingly exploring long-term supplier contracts and alternative sourcing regions to reduce risk exposure. In the coming years, the industry will have been prioritizing supply chain resilience and cost optimization strategies to maintain operational stability and sustain competitive performance.

Food-Service Sector Expansion and Product Innovation

The food service sector is recovering strongly after the pandemic and is undergoing rapid modernization, which is increasing demand for versatile ingredients such as hoisin sauce. Industry insights from the National Restaurant Association and Technomic Inc. are indicating that restaurants are expanding menus and investing in operational efficiency. Hoisin sauce is gaining importance as chefs are using it across multiple applications such as dipping, marination, stir-frying, and even as a base for creative dishes. Quick service restaurants (QSR) and casual dining outlets are integrating this ingredient to enhance flavor while maintaining speed and consistency in preparation. At the same time, ghost kitchens are adopting it due to its adaptability and ease of use in diverse cuisines.

The rise of fusion cuisine is further strengthening demand as chefs are blending culinary traditions to create unique offerings. Combinations such as Korean-inspired barbecue and Asian-influenced street food are expanding the use of hoisin sauce in innovative formats. This trend is encouraging food service operators to seek customized flavor profiles that match evolving consumer preferences. Bulk packaging solutions are also gaining traction as restaurants are requiring cost-effective and scalable supply options. Market is advancing toward enhanced product customization and broader application diversity, fueling sustained expansion across international foodservice channels.

Sustainable Packaging Innovation

Alignment with environmental, social, and governance (ESG) principles is creating new opportunities for differentiation in the hoisin sauce market. Companies are actively shifting toward sustainable packaging solutions as they are responding to changing consumer expectations and environmental concerns. Manufacturers are adopting materials such as recyclable polyethylene terephthalate (PET), biodegradable containers, and refillable systems to reduce environmental impact. This transition is not only supporting sustainability goals but is also strengthening brand perception. As awareness is growing, consumers are evaluating packaging choices more carefully, which is encouraging companies to innovate and communicate their sustainability efforts more clearly.

Regulatory developments are also accelerating this shift, particularly in Europe, where the EU Packaging and Packaging Waste Regulation is guiding stricter recyclability requirements. Businesses are investing in packaging infrastructure to ensure compliance and long-term readiness. These efforts are enabling brands to position themselves as environmentally responsible while gaining a competitive edge. Sustainable practices are opening access to new consumer segments that prioritize ethical consumption. The market is shifting toward circular economy principles, prioritizing packaging reuse and material efficiency as core elements of operational strategies and value creation.

Category-wise Analysis

Packaging Insights

Glass is expected to secure approximately 48% of the hoisin sauce market revenue share in 2026. Glass packaging is widely preferred due to its premium appearance, strong flavor preservation, and association with high product quality. In retail settings, it supports better shelf visibility and enables effective brand storytelling, which is essential in a competitive condiment category. This format is especially common in Western markets, where premium trends are influencing purchasing behavior. Food service operators are also favoring glass for front-of-house presentation in Asian restaurants and upscale dining environments. Although it carries higher costs and environmental impact than polyethylene terephthalate (PET), improving recycling systems are helping reduce sustainability concerns and maintain its strong market position.

Pouches are likely to be the fastest-growing segment during the 2026-2033 forecast period, driven by the benefits such as lower material weight, reduced transportation costs, longer shelf life, and improved sustainability through less plastic usage. This format is becoming popular in Asia Pacific and Middle East and Africa regions, where affordability strongly influences buying decisions. Demand is increasing for single-serve and portable pouch options, especially across food service, institutional, and convenience channels. Improvements in barrier film technology are enhancing product protection and durability. These advancements are making pouches suitable for premium offerings while helping manufacturers meet rising consumer demand for convenience and efficiency.

Distribution Channel Insights

Supermarkets represent the dominant distribution channel, capturing approximately 50% of the hoisin sauce market share in 2026. The strong foot traffic, wide consumer access, and well-established supplier networks that support prominent shelf placement. Organized retail settings are enabling effective promotions, in-store sampling, and structured category management, which are encouraging impulse purchases of condiments. The channel is also strengthening through private-label expansion, which is both competing with and supporting branded products. Major retailers such as Walmart, Tesco, Carrefour, and Reliance Fresh are expanding Asian sauce sections, ensuring continued visibility and growth for hoisin sauce brands.

Online retail is expected to be the fastest-growing segment over the 2026-2033 forecast period. Post-pandemic behavior and the growth of online grocery platforms. Digital marketplaces such as Amazon and Walmart are enabling wider product availability, direct-to-consumer engagement, and personalized marketing through data insights. Subscription services, recipe kits, and direct-to-consumer (DTC) strategies are further supporting this expansion. Brands are using digital storytelling, influencer partnerships, and search-optimized content to boost visibility, leading to faster growth compared to traditional retail and making online investment essential.

Regional Insights

Asia Pacific Hoisin Sauce Market Trends

Asia Pacific is likely to be both the leading and fastest-growing regional market for hoisin sauce in 2026, accounting for approximately 42% share, as it is combining strong production capabilities with deep cultural consumption. China is serving as the central market, where hoisin sauce is originating from traditional culinary practices and remains widely used in daily cooking and food service. A large network of domestic manufacturers is supporting steady supply, while restaurants are continuing to integrate the sauce into diverse menu offerings. Japan is contributing a premium segment, where consumers are demanding clean-label, low-sodium, and functional variants.

In India, rapid urban development and changing food preferences are encouraging greater adoption of Chinese and Pan-Asian cuisines, especially in major and emerging cities. ASEAN economies are also strengthening regional growth, with Thailand, Vietnam, Malaysia, and Indonesia benefiting from strong culinary traditions and cost-efficient manufacturing environments. These markets are supporting both domestic consumption and export activities. Access to raw materials within the region is helping producers maintain competitive pricing. Governments are actively promoting food processing industries, which is encouraging investment and capacity expansion.

Europe Hoisin Sauce Market Trends

Europe is holding a strong position in the global market for hoisin sauce, as demand is rising across both food service and home cooking segments. Key countries such as Germany, United Kingdom, France, and Spain are forming the core demand base. Urban consumers are increasingly exploring Asian cuisine, which is encouraging restaurants to expand menu offerings and retailers to stock diverse sauce options. The United Kingdom is leading regional consumption due to its multicultural population and well-established Chinese dining sector. Meanwhile, Germany and France are experiencing steady growth as disposable incomes rise and global food preferences continue to evolve.

Regulatory developments are shaping the market landscape, particularly through initiatives such as the Farm to Fork Strategy and guidelines from the European Food Safety Authority (EFSA). These frameworks are encouraging manufacturers to adopt cleaner formulations and transparent labeling practices. While compliance is increasing operational costs, it is also enabling standardized distribution across the European Union (EU). Companies are focusing on organic certification and sustainable packaging to meet high consumer expectations. Emerging markets such as Poland and Czech Republic are gaining momentum as retail infrastructure improves and interest in diverse cuisines continues to expand.

North America Hoisin Sauce Market Trends

North America is the second-largest regional market for hoisin sauce, holding approximately 22% of global market revenue in 2026, with the United States acting as the primary growth engine. Demand is increasing as Asian cuisine continues to integrate into mainstream food culture, supported by a large Asian-origin population and a well-established restaurant network. Consumers are actively preparing Asian dishes at home, which is driving retail demand for authentic condiments. The premiumization of sauces is encouraging brands to focus on quality, flavour authenticity, and ingredient transparency. The expansion of specialty grocery stores and Asian retail chains is further improving product availability and visibility across urban and suburban markets.

Regulatory frameworks such as the Food Safety Modernization Act under the U.S. FDA are pushing manufacturers to adopt higher safety and labeling standards. Leading brands such as Lee Kum Kee, Kikkoman, and Dynasty are maintaining strong market presence, while new entrants are focusing on natural and organic products. E-commerce platforms are playing a major role in expanding reach, supported by digital content that is influencing cooking habits. Companies will have been investing more in innovation, partnerships, and acquisitions to strengthen competitive positioning.

Competitive Landscape

The global hoisin sauce market structure is moderately consolidated, dominated by leading players such as Lee Kum Kee, Kikkoman Corporation, Amoy Food Limited, Wan Ja Shan Brewery Co., and Koon Chun Sauce Factory. These players collectively capture 35-40% of the market share. Market concentration is higher in regions such as North America and Europe, where a few established players are maintaining strong control over distribution and brand visibility.

In contrast, Asia Pacific is showing a more fragmented structure, with numerous regional and local brands actively competing for market share. This diversity is increasing competition and encouraging product differentiation. Companies are focusing on innovation, brand heritage, and expanding distribution networks to strengthen their position. These factors are shaping competitive dynamics and influencing long-term growth strategies across both mature and emerging markets.

Companies Covered in Hoisin Sauce Market

- Lee Kum Kee

- Kikkoman Corporation

- Amoy Food Limited

- Wan Ja Shan Brewery Co.

- Koon Chun Sauce Factory

- House of Tsang

- Panda Express

- Pearl River Bridge

- Dynasty

- Woh Hup Food Industries

- Kimlan Foods Co., Ltd.

- Lingham's Food Industries

- Chung Jung One

- S&B Foods Inc.

Frequently Asked Questions

The global hoisin sauce market is projected to reach US$ 1.7 billion in 2026.

The market is driven by rising global demand for Asian fusion cuisines, and health-focused variants such as low-sodium and organic hoisin.

The market is poised to witness a CAGR of 5.6% from 2026 to 2033.

Major opportunities lie in rapid urbanization in developing economies, sustainable packaging innovations, and foodservice partnerships for customized applications.

Lee Kum Kee, Kikkoman Corporation, Amoy Food Limited, Wan Ja Shan Brewery Co., and Koon Chun Sauce Factory are some of the key players in the market.