- Pharmaceuticals

- Hemophilia Therapeutics Market

Hemophilia Therapeutics Market Size, Share, and Growth Forecast, 2026-2033

Hemophilia Therapeutics Market by Disease Indication (Hemophilia A, Hemophilia B, Hemophilia C, Others), Therapeutic Category (Factor Replacement Therapies, Non-Factor Therapies, Gene Therapies, Immune Tolerance Induction (ITI), Adjunct & Supportive Therapies), Healthcare Settings (Hospitals & Hemophilia Treatment Centers (HTCs), Specialty Clinics, Home Care, Retail Pharmacies & E-Commerce Channels), and Regional Analysis for 2026-2033

Hemophilia Therapeutics Market Share and Trends Analysis

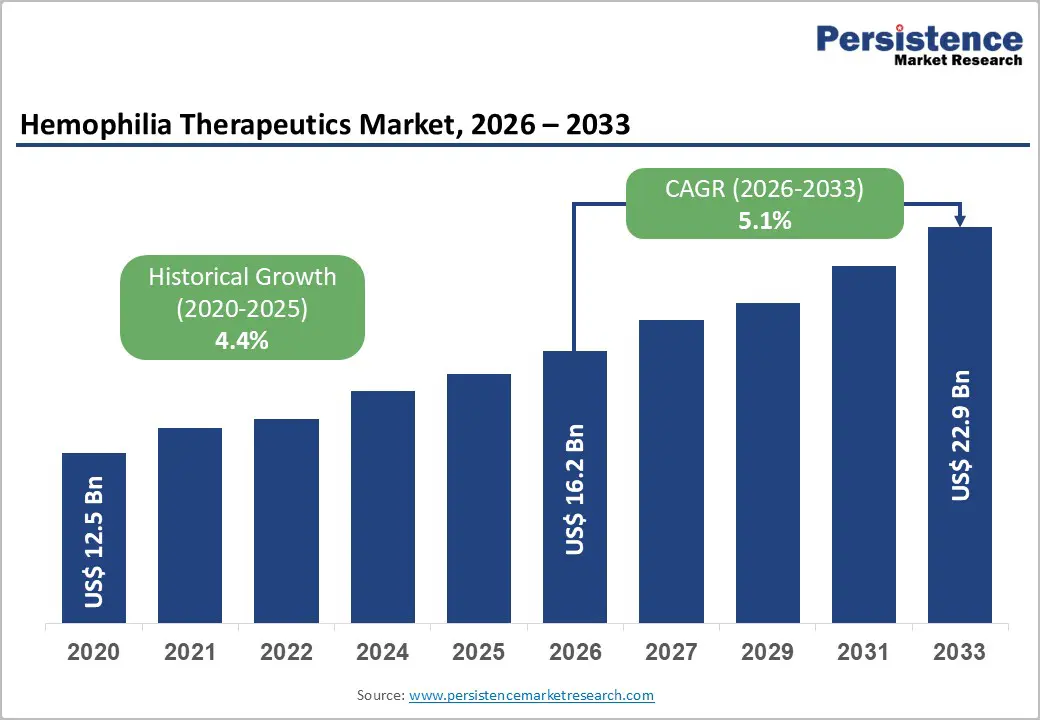

The global hemophilia therapeutics market size is likely to be valued at US$16.2 billion in 2026, and is projected to reach US$22.9 billion by 2033, growing at a CAGR of 5.1% during the forecast period 2026–2033. Market growth is being driven by increasing diagnosed prevalence of hemophilia A and hemophilia B, supported by improved screening programs and greater disease awareness.

National health systems and patient advocacy organizations are expanding early diagnosis initiatives, which are increasing the treated patient pool. At the same time, payers in developed markets are continuing to reimburse advanced therapies, which is sustaining premium pricing and supporting revenue growth. Emerging economies are gradually improving access through public procurement programs and broader insurance coverage, which is contributing to incremental volume expansion. Therapeutic innovation is strengthening the long-term outlook. Adoption of extended half-life clotting factor concentrates and non-factor therapies such as bispecific antibodies is improving treatment adherence and reducing bleeding episodes. Gene therapy platforms are progressing through regulatory pathways and are beginning to reshape treatment paradigms by offering the potential for durable factor expression following a single administration. Manufacturers are investing in distribution infrastructure and cold chain logistics to ensure consistent global supply.

Key Industry Highlights

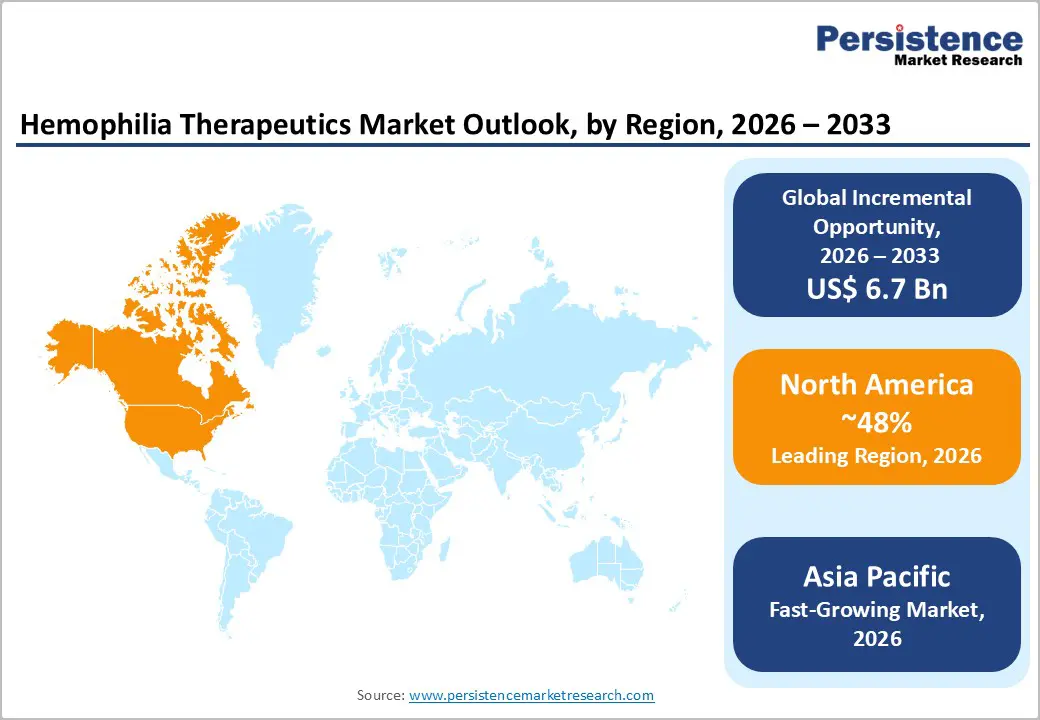

- Regional Leadership : North America is set to dominate with around 48% market share in 2026 owing to high healthcare spending, while the Asia Pacific market is expected to grow the fastest at roughly 6.5% CAGR through 2033, driven by expanding healthcare access.

- Dominant Disease Indication : Hemophilia A is set to command nearly 74% of the revenue share in 2026, while Hemophilia B is poised to grow the fastest through 2033, owing to gene therapy adoption.

- Leading Therapeutic Category : Factor replacement therapies are expected to lead with roughly 61% revenue share in 2026 due to their established efficacy

- Fastest-growing Therapeutic Category : Non-factor and gene therapies are likely to be fastest-growing at an estimated 6.6 % CAGR through 2033 on account of reduced infusion frequency.

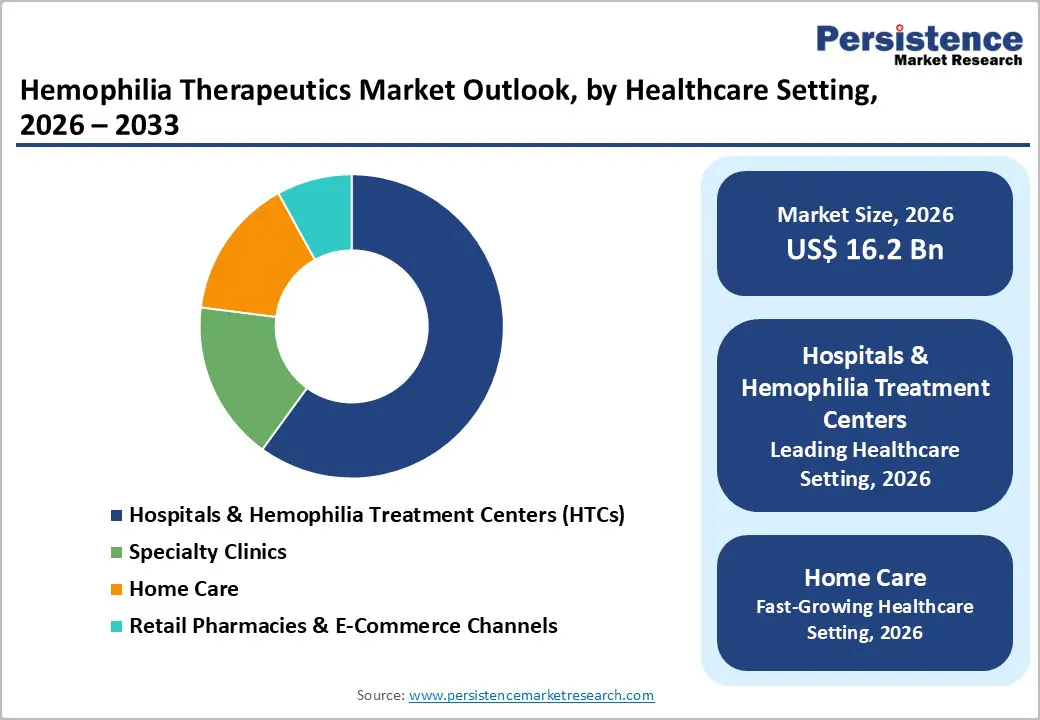

- Dominant Healthcare Setting : Hospitals & hemophilia treatment centers are slated to lead with about 60% share in 2026 on the back of supervised administration, while home care and specialty clinics are set to grow the fastest due to patient convenience and home infusion adoption.

- Competitive Environment: Pipeline advances such as Pfizer's Hympavzi success and Novo Nordisk's Alhemo approval, plus extended half-life and non-factor biologics, drive market differentiation.

- September 2025 : Novo Nordisk submitted a Biologics License Application (BLA) to the US Food and Drug Administration (FDA) for MIM8, an investigational prophylactic therapy for people living with hemophilia A with or without inhibitors.

| Key Insights | Details |

|---|---|

| Hemophilia Therapeutics Market Size (2026E) | US$ 16.2 Bn |

| Market Value Forecast (2033F) | US$ 22.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Disease Burden, Technological Advancements, and Improving Healthcare Support

Hemophilia continues to be a hereditary bleeding disorder with a substantial unmet need for effective treatments. According to the U.S. Centers for Disease Control and Prevention (CDC), around 33,000 males in the United States live with hemophilia, and early diagnosis programs have improved detection and access to care. The World Federation of Hemophilia (WFH) estimates that up to 75% of people with inherited bleeding disorders remain undiagnosed and untreated, highlighting significant gaps in awareness, screening, and access. Enhanced newborn screening programs and public health initiatives are expanding the diagnosed patient population, driving uptake of both traditional factor replacement therapies and emerging novel treatments. These factors directly contribute to consistent market demand and support long-term growth projections through 2033.

Technological advances in gene therapies and non-factor biologics are further reshaping treatment paradigms. These innovations offer longer-lasting therapeutic benefits, reduced infusion frequency, and improved clotting efficacy, aligning with patient and physician preferences for convenience and better outcomes. In developed regions such as North America and Europe, well-established reimbursement frameworks and high per-capita healthcare spending make advanced treatments more accessible. The combination of rising diagnosis rates, innovative therapies, and supportive healthcare infrastructure is fueling adoption of premium and next-generation therapeutics, reinforcing long-term market expansion and investment in research and development.

High Costs, Regulatory Oversight, and Manufacturing Complexities Limiting Market Expansion

The high cost of advanced hemophilia therapeutics, including factor replacement, non-factor biologics, and gene therapy options, continues to pose a significant barrier to adoption worldwide. In low- and middle-income countries, limited insurance coverage and high out-of-pocket expenses amplify the financial burden on patients and healthcare systems, slowing treatment uptake even when clinical need is high. For example, gene therapies such as valoctocogene roxaparvovec are priced over US$ 2 million per patient, limiting accessibility in many markets despite proven clinical benefit. These affordability challenges, combined with the need for specialized storage, handling, and patient monitoring, restrict market penetration and dampen revenue growth in developing regions.

Compounding the cost challenge are regulatory scrutiny and complex manufacturing requirements. Gene therapies and biologics face intense evaluation by regulatory authorities, which increases development risk and prolongs time-to-market. For instance, the U.S. FDA review process for therapies such as Roctavian and emerging non-factor biologics demonstrates the rigorous oversight required for approval. Moreover, manufacturing these therapies involves highly specialized facilities, precise viral vector production, and strict quality control, which limits scalable output and often causes supply bottlenecks. These operational hurdles introduce uncertainty in planning for pharmaceutical companies, tempering investment confidence, and slowing capacity expansion.

Innovative Therapies and Strategic Expansion in Emerging Markets Drivinga Growth

Emerging economies of Asia Pacific and Latin America present significant growth potential as healthcare infrastructure improves and disease awareness rises. Expanding public health programs and rising healthcare investment create favorable conditions for hemophilia therapeutics adoption. Asia Pacific, in particular, is projected to register a faster CAGR than Western markets due to structural healthcare improvements and a large undiagnosed patient population. The real-world administration of Hemgenix® (etranacogene dezaparvovec) in Denmark and Germany illustrates how approved gene therapies are now reaching patients under new care and reimbursement models, demonstrating commercial potential beyond clinical trials. These trends support the adoption of both established factor replacement therapies and next-generation treatments, creating strategic growth opportunities for global pharma companies.

Simultaneously, novel therapeutic innovations are expanding the treatment landscape. In 2025, for example, the first-in-human clinical trial of BE101, a B-cell therapy for hemophilia B, successfully dosed its first patient, marking a new mechanism of action in development. Alongside advances such as long-acting factor products and non-factor biologics, these developments enable improved patient outcomes, reduced treatment burden, and differentiation in the market. Combined with strategic regional expansion by major pharmaceutical firms, these innovations provide actionable opportunities to capture market share, establish leadership in emerging markets, and accelerate adoption of next-generation hemophilia therapeutics worldwide.

Category-wise Analysis

Disease Indication Insights

Hemophilia A is estimated to account for approximately 74% of the global market revenues in 2026, reflecting its dominant position in terms of prevalence and therapeutic adoption. Patients continue to rely heavily on factor VIII replacement therapies, complemented by expanding access to non-factor and gene therapies. Roche’s next-generation bispecific antibody NXT007 demonstrated positive Phase I/II results, highlighting ongoing innovation in Hemophilia A management. Early diagnosis initiatives and structured treatment protocols support sustained treatment volumes, ensuring continued market leadership. Hospitals and specialized HTCs remain primary administration channels, offering clinical oversight and patient monitoring. The combination of established protocols and emerging therapeutic options reinforces Hemophilia A’s critical contribution to overall market revenue.

Hemophilia B is projected to grow at an estimated CAGR of 6.7% from 2026 to 2033, driven by innovations in gene therapy and extended half-life Factor IX products. These therapies reduce infusion frequency and improve adherence, enhancing patient quality of life and clinical outcomes. China approved Dalnacogene Ponparvovec Injection as the first gene therapy for moderate-to-severe Hemophilia B, expanding access in emerging markets. Long-term data for Hemgenix® presented at ASH 2025 also underscore the durability of gene therapy outcomes. The segment is expected to attract increasing clinical adoption and investment, supporting faster growth relative to Hemophilia A. Improved diagnostics and patient monitoring further expand the addressable population.

Therapeutic Category Insights

Factor replacement therapies are estimated to represent around 61% of the hemophilia therapeutics market revenue share in 2026, maintaining their position as the largest therapeutic category. These therapies continue to provide reliable bleed management for both Hemophilia A and B, supported by extensive clinical experience and provider familiarity. The post-marketing data from Hemlibra® highlighted sustained activity and reduced bleed rates after switching from factor VIII replacement, reinforcing confidence in optimized care models. Hospitals and HTCs remain key channels for administration, providing clinical supervision for complex cases. Extended half-life factor formulations further strengthen adoption. Factor replacement remains the backbone of hemophilia management while complementing emerging therapies.

Non-factor biologics and gene therapies are projected to grow at a CAGR of roughly 6.6% between 2026 and 2033, reflecting their rapid adoption due to novel mechanisms and reduced dosing frequency. Fitusiran (Qfitlia) received approval as a subcutaneous therapy for hemophilia A and B, providing a simplified prophylaxis approach. Single-dose gene therapies are advancing globally, offering curative potential for patients. These therapies are increasingly adopted across both developed and emerging markets due to convenience and improved long-term outcomes. Regulatory approvals and pipeline progress are further boosting growth prospects. By reducing treatment burden, non-factor and gene therapies are shaping the future market landscape and redefining standard care practices.

Healthcare Setting Insights

Hospitals and hemophilia treatment centers (HTCs) are estimated to account for approximately 60% of the market share in 2026, reflecting their continued importance for managing severe cases and advanced therapies. These settings provide supervised infusion, integrated care, and access to advanced diagnostics. Expansion of hospital-based HTCs in North America and Europe, supported by multidisciplinary clinical models, reinforces their leadership. Enhanced patient education and structured care pathways improve adherence and clinical outcomes. Hospitals continue to support early adoption of innovative therapies. Their established infrastructure sustains high treatment volumes and ensures consistent market demand.

Specialty clinics and home care services are projected to grow at a CAGR of approximately 6% from 2026 to 2033, driven by patient preference for convenience and decentralized treatment models. Home infusion programs, telehealth monitoring, and patient education initiatives are enabling patients to manage therapy outside hospital settings. Retail pharmacies and e-commerce channels complement this trend by providing improved access to routine therapies and prescription refills. The growth of decentralized care models reduces the burden on hospitals while enhancing treatment adherence. Increasing healthcare infrastructure investments in emerging regions support this shift.

Regional Insights

North America Hemophilia Therapeutics Market Trends

North America is anticipated to hold 48% of the hemophilia therapeutics market share in 2026, making it the leading regional contributor. The FDA approved Sanofi’s Qfitlia (fitusiran) for routine prophylaxis in hemophilia A and B, offering a novel siRNA therapy with fewer injections. This highlights regulatory support for diversified treatments and patient-friendly options. Comprehensive Hemophilia Treatment Centers and screening programs enable early diagnosis and continuous care. High healthcare spending and broad insurance coverage maintain access to both traditional and advanced therapies. Domestic biotech and pharma presence strengthens clinical research and innovation. These factors underpin North America’s sustained market leadership and revenue potential.

Regional market growth momentum is being reinforced by emerging therapies and real-world application of advanced treatments. For instance, in 2025, Phase 3 results for marstacimab showed improved outcomes in hemophilia A or B with inhibitors, expanding options for complex cases. Digital monitoring and real-world evidence initiatives are improving adherence and long-term outcomes. Value-based reimbursement models are optimizing access for high-cost treatments. Strategic collaborations among payers, providers, and innovators enhance care pathways. Combined, these developments support steady adoption of innovative therapies.

Europe Hemophilia Therapeutics Market Trends

The Europe hemophilia therapeutics market benefits from regulatory harmonization and structured reimbursement frameworks across the European Union (EU), enabling efficient and uninterrupted access to innovative hemophilia therapies. Countries such as Germany, the U.K., France, and Spain are adopting diverse treatment portfolios through aligned approval pathways. Roche highlighted updates on Hemlibra® and next-generation bispecific antibodies at the ASH Annual Meeting, reinforcing Europe’s adoption of advanced therapies. Integrated clinical networks and specialized treatment centers provide comprehensive care models and facilitate early diagnosis. Pricing negotiations and health technology assessments balance cost-effectiveness with access to new therapies. Local manufacturers and mid-sized biotech players continue investing in clinical collaborations and research initiatives.

The expansion of the market here is also gaining support from real-world evidence initiatives and continuity of care programs. Collaborative efforts between health agencies and patient advocacy groups are improving diagnosis rates, particularly in underserved populations. Joint procurement strategies and coordinated policy frameworks enhance affordability and uptake of newer therapies. European guidelines increasingly emphasize personalized treatment pathways, including prophylactic and non-factor options. Cross-border clinical studies and shared data strengthen evidence-based decision making. Adoption of advanced therapeutics is further reinforced by clinical network expansion.

Asia Pacific Hemophilia Therapeutics Market Trends

The hemophilia therapeutics market growth in Asia Pacific is projected to be the highest, projected to exhibit a CAGR of roughly 6.5% during the 2026-2033 forecast period, driven by rising healthcare investment, improved rare disease awareness, and better diagnostics. In April 2025, for example, China’s National Medical Products Administration (NCMA) approved Dalnacogene Ponparvovec Injection, the first hemophilia B gene therapy in the country, expanding access to advanced treatments. This highlights the region’s adoption of innovative therapies beyond Western markets. Investments in diagnostic programs are identifying more patients in China, India, and Japan. Public-private partnerships and rare disease initiatives strengthen healthcare infrastructure. Awareness campaigns and specialized training for hemophilia care teams improve treatment delivery. These factors accelerate therapy adoption and market expansion.

Regional market growth prospects are also being bolstered by national programs such as China’s Rare Disease Treatment Initiative, India’s National Health Mission, and Japan’s Advanced Therapy Promotion Strategy, improving coverage and reducing patient costs. Local and multinational biotech players are increasingly involved in clinical research and regulatory engagement, supporting faster adoption of novel therapies. Expansion of medical infrastructure in urban centers enhances access to care. Digital health tools and remote monitoring platforms improve adherence. Cross-country collaborations and government initiatives boost diagnostic reach. Targeted public health efforts are strengthening patient awareness and enabling early intervention.

Competitive Landscape

The global hemophilia therapeutics market structure is moderately consolidated, with top players such as Roche, Sanofi, Novo Nordisk, Bayer, and Pfizer controlling a significant portion of revenues. These established companies leverage long-standing relationships with treatment centers, extensive clinical expertise, and broad therapeutic portfolios that include factor replacement, non-factor biologics, and gene therapies. They also invest heavily in R&D and pipeline development, focusing on next-generation gene therapies, bispecific antibodies, and extended half-life products to maintain technological leadership.

Regional and niche competitors, including BioMarin, uniQure, and CSL Behring, focus on specialized therapies, rare bleeding disorders, and emerging markets. They strengthen their position through targeted clinical programs, localized manufacturing, and patient support initiatives. Barriers such as regulatory approvals, complex biologic and gene therapy manufacturing, and high treatment costs limit new entrants. Digital health solutions and remote monitoring platforms are enabling smaller innovators to participate with patient-centric approaches. Market consolidation is expected to continue gradually as leading players pursue strategic acquisitions, licensing agreements, and collaborations to expand portfolios, reach, and capabilities.

Key Industry Developments

- In December 2025, BioMarin Pharmaceutical announced a definitive agreement to acquire Amicus Therapeutics for approximately US$ 4.8 billion, significantly expanding its rare-disease footprint. The transaction adds approved therapies Galafold and Pombiliti + Opfolda, reducing BioMarin’s dependence on Voxzogo and the challenged rollout of its hemophilia gene therapy, Roctavian.

- In November 2025, Metagenomi reported strong preclinical data for its hemophilia A program MGX-001, demonstrating durable and therapeutically relevant Factor VIII activity in non-human primates. The gene-editing therapy maintained stable expression for up to 19 months, supporting its potential as a one-time curative treatment.

- In June 2025, Pfizer announced that its investigational bleeding-disorder therapy met its primary efficacy endpoint in a late-stage clinical trial in 2025. The therapy demonstrated a meaningful reduction in bleeding episodes among patients with specific hemophilia subtypes, reiterating the growing role of non-factor prophylactic therapies in hemophilia management.

Companies Covered in Hemophilia Therapeutics Market

- Takeda Pharmaceutical Company Limited

- CSL Behring

- Pfizer Inc.

- Bayer AG

- BioMarin Pharmaceutical Inc.

- Novo Nordisk A/S

- Sanofi

- F. Hoffmann La Roche Ltd.

- Octapharma AG

- Grifols S.A.

- Sangamo Therapeutics

- UniQure N.V.

Frequently Asked Questions

The global hemophilia therapeutics market is projected to reach US$ 16.2 billion in 2026.

Rising diagnosis rates, continuous therapeutic innovation, and improved reimbursement support are the primary drivers of market growth.

The market is poised to witness a CAGR of 5.1% from 2026 to 2033.

Expansion of gene therapies, increasing access in emerging regions, and integration of personalized and digital care models present major opportunities.

Roche, Sanofi, Novo Nordisk, Bayer, Pfizer, CSL Behring, and Takeda are among the leading market participants.