- Smart Packaging

- Healthcare and Laboratory Labels Market

Healthcare and Laboratory Labels Market Size, Share, and Growth Forecast, 2026 - 2033

Healthcare and Laboratory Labels Market by Material Type (Paper, Vinyl/PVC, Others), Printing Technology (Direct Thermal, Inkjet Printing, Others), Application, End-user, and Regional Analysis for 2026 - 2033

Healthcare and Laboratory Labels Market Size and Trends Analysis

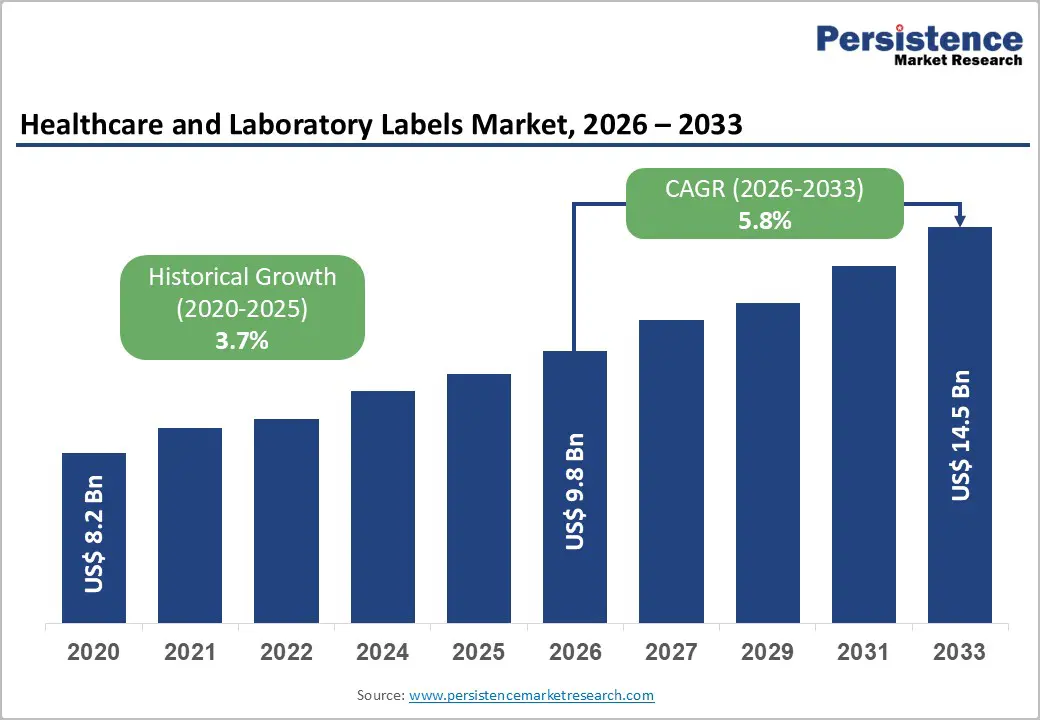

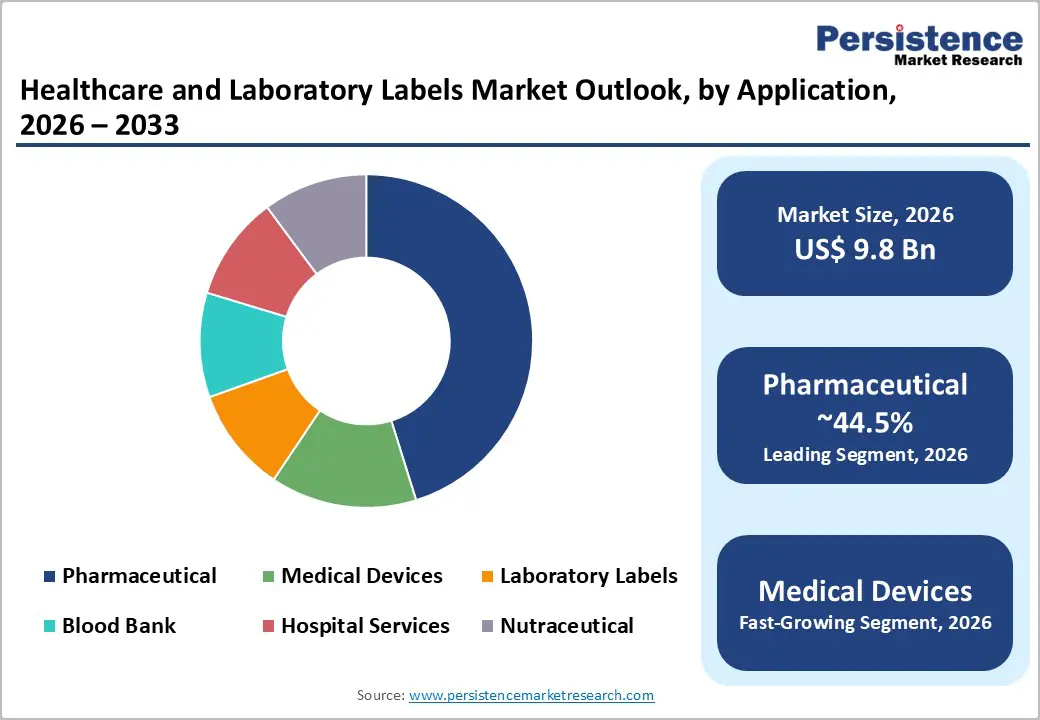

The global healthcare and laboratory labels market size is likely to be valued at US$ 9.8 billion in 2026 and is expected to reach US$14.5 billion by 2033, growing at a CAGR of 5.8% between 2026 and 2033, driven by stricter regulatory traceability requirements in pharmaceuticals and medical devices, rising diagnostic and laboratory testing volumes, and greater adoption of durable, chemical-resistant label materials for specimen and blood-bank workflows. Digital printing and variable-data printing (VDP) adoption support higher-value, low-volume runs for clinical trials and personalized medical devices.

Key Industry Highlights:

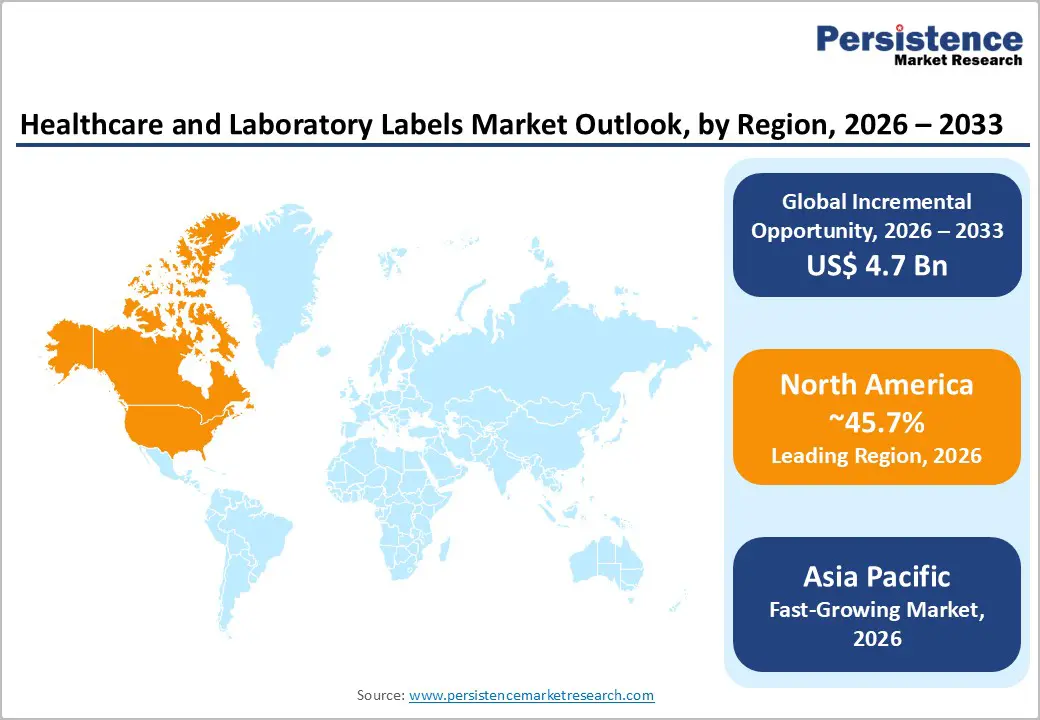

- Leading Region: North America is projected to hold approximately 45.7% of the market share, supported by strong U.S. pharmaceutical manufacturing, high diagnostic throughput, and stringent FDA and GS1 traceability requirements.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, driven by rapid pharmaceutical production expansion in China and India, laboratory infrastructure investments, and localized converting capacity development.

- Investment Plans: Market participants are prioritizing automation of narrow-web converting lines, digital/variable data printing (VDP) capability expansion, serialization infrastructure, and regional validation labs, particularly in Asia Pacific and emerging markets, to support multi-year clinical trial and biologics contracts.

- Dominant Material Type: Paper is anticipated to account for approximately 63.4% of market share, due to cost-efficiency and widespread adoption in high-volume hospital and laboratory workflows.

- Leading Application: Pharmaceutical applications are expected to hold around 44.5% of the market share, driven by serialization mandates, tamper-evident labeling requirements, and global drug manufacturing scale.

| Key Insights | Details |

|---|---|

| Healthcare and Laboratory Labels Market Size (2026E) | US$9.8 Bn |

| Market Value Forecast (2033F) | US$14.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory Traceability and Serialization Mandates (Pharmaceuticals & Medical Devices)

Global regulatory authorities increasingly mandate end-to-end product traceability across pharmaceuticals, biologics, in vitro diagnostics (IVDs), and medical devices. Unique Device Identification (UDI) systems, serialization frameworks, and GS1-compliant barcode standards require manufacturers to apply machine-readable codes and unique identifiers on cartons, primary packaging, and, in certain cases, individual units and specimen containers. This regulatory shift has elevated label complexity, transitioning the market from basic identification labels to high-performance constructions capable of supporting 2D barcodes, serialized data, and tamper-evident features. As a result, demand is rising for durable substrates, precision printing technologies, and integrated data management solutions. The commercial impact is significant: average selling prices per label increase due to added technical requirements, while suppliers benefit from recurring revenue streams tied to serialization services, validation support, and compliance documentation.

Rising Diagnostic Volume and Decentralization of Testing

The global expansion of laboratory testing, driven by chronic disease prevalence, preventive screening programs, and decentralized healthcare delivery, has directly increased the consumption of healthcare and laboratory labels. Growth in clinical laboratories, point-of-care (POC) testing centers, and decentralized diagnostic facilities necessitates reliable labeling for sample tubes, slides, cryovials, and related consumables. Laboratories require labels that maintain barcode readability after exposure to extreme temperatures (freeze/thaw cycles), solvents, and centrifugation. These technical specifications favor synthetic materials such as polyolefin and polyester, along with thermal transfer and inkjet printing technologies that ensure durability and high-resolution output. As testing throughput increases, healthcare institutions adopt high-speed roll labels and on-demand printing systems, generating sustained consumables demand and service revenue opportunities for label manufacturers and printer OEMs.

Material and Functional Innovation (Durability and Smart Labels)

Technological advancements in adhesives, facestock coatings, and embedded identification technologies are expanding the functional scope of healthcare labels. Modern constructions incorporate smudge-resistant surfaces, chemical-resistant laminates, tamper-evident designs, and RFID or near-field communication (NFC) inlays to enhance tracking and authentication. These innovations enable labels to transition from passive identifiers to active components within supply-chain visibility and patient-safety ecosystems. Sustainability considerations and circular-economy mandates are accelerating the adoption of recyclable substrates and removable adhesive systems. Suppliers capable of integrating advanced material science with digital and variable-data printing capabilities are well-positioned to capture higher-margin segments and secure long-term supply contracts with pharmaceutical manufacturers, hospitals, and diagnostic networks.

Barrier Analysis - Cost of Qualification and Validation for Medical Use

Healthcare-grade labels must comply with rigorous regulatory and performance standards, including biocompatibility, sterility compatibility, adhesion reliability, and defined shelf-life parameters. Achieving compliance with cGMP and ISO standards requires extensive testing, documentation, and process validation. These qualification cycles increase time-to-market and raise capital expenditure requirements, particularly for small and mid-sized converters. Procurement onboarding within regulated healthcare supply chains can extend between 6 and 18 months, delaying revenue realization and increasing operational risks. Consequently, regulatory validation acts as a structural barrier to entry, favoring established players with proven compliance track records and certified production facilities.

Supply-Chain Volatility for Specialty Materials

Healthcare and laboratory labels often rely on specialty films, high-performance adhesives, and narrow-web coating technologies that are sensitive to fluctuations in petrochemical feedstock prices and global manufacturing capacity. Volatility in raw material availability can disrupt production schedules and compress margins. When input costs increase, suppliers face a strategic dilemma: absorb higher costs and reduce profitability, or transfer price increases to healthcare customers operating under strict procurement budgets. This dynamic limits short-term pricing flexibility and constrains rapid margin expansion. Over time, sustained volatility may also encourage healthcare buyers to diversify supplier bases, intensifying competitive pressure within the industry.

Opportunity Analysis - Serialized Labels and Integrated Data Services for Clinical Trials and Biologics

The expansion of clinical trials, advanced biologics, and personalized medicine is creating sustained demand for serialized, tamper-evident labeling solutions integrated with secure traceability systems. Regulatory frameworks governing pharmaceuticals and investigational products require accurate lot identification, unique device identifiers (UDI), expiry management, and audit-ready documentation. This complexity elevates the role of labels from simple identification tools to compliance-critical data carriers. Suppliers that combine variable data printing (VDP), cloud-based validation logs, serialization software integration, and compliance reporting services can capture higher-margin solution contracts rather than compete solely on consumable pricing. Serialization programs typically extend across multi-year clinical trial phases or long biologics commercialization cycles, generating predictable recurring revenues through ongoing consumable replenishment and digital service subscriptions. As decentralized trials and temperature-controlled biologics expand globally, the demand for secure, data-integrated labeling ecosystems will continue to rise, presenting a structurally attractive growth segment within the healthcare labeling market.

Rapid Adoption in Emerging Markets through Localized Converting Hubs

Emerging economies in Asia Pacific and select Latin American markets are expanding pharmaceutical manufacturing capacity and laboratory infrastructure to support domestic demand and export growth. Governments in countries such as China, India, Brazil, and Indonesia are investing in healthcare manufacturing ecosystems, creating downstream demand for compliant, medical-grade labeling solutions. Establishing localized converting hubs that offer validated adhesives, regulatory-compliant facestocks, and short lead times enables suppliers to reduce import dependency and lower total landed costs for regional pharmaceutical and diagnostics producers. Local production also mitigates supply-chain volatility and currency exposure while improving responsiveness to regulatory updates. Investors and established global converters can capitalize on this opportunity by deploying validated narrow-web lines and qualification labs within high-growth regions, securing long-term supply agreements with domestic pharma and diagnostic companies.

Category-wise Analysis

Material Type Insights

Paper-based face stocks are anticipated to maintain their leadership position, accounting for approximately 63.4% of market share in 2026, primarily due to their cost-efficiency, ease of printability, and compatibility with direct thermal printing systems widely deployed across hospitals and diagnostic laboratories. In high-throughput healthcare environments, paper labels are extensively used for patient wristbands, prescription labels, pharmacy packaging, laboratory request forms, and secondary pharmaceutical cartons. For non-critical specimen management and short lifecycle applications, direct thermal paper labels provide a practical and economical solution that integrates seamlessly with existing hospital printer fleets. Large healthcare networks often standardize paper roll formats across facilities to streamline procurement and inventory management, reinforcing volume dominance. While paper labels typically command lower unit prices compared to synthetics, their widespread use across routine healthcare operations ensures sustained volume leadership throughout the forecast period.

Vinyl constructions are expected to record the fastest growth rate within the material segment, driven by increasing demand for chemical resistance, temperature stability, and long-term durability. These engineered synthetics offer superior adhesion on curved or small-diameter surfaces such as cryovials, ampoules, and blood collection tubes. They also maintain barcode readability after exposure to sterilization processes, including ethylene oxide (EO), gamma radiation, and autoclaving. Adoption is particularly strong in blood-bank labeling, biorepository storage, and implantable medical device identification, where label failure can result in regulatory non-compliance or patient safety risks. The integration of RFID inlays and tamper-evident constructions is also more stable within laminated synthetic structures, supporting smart-label expansion.

Application Insights

The pharmaceutical application segment is anticipated to hold approximately 44.5% of market share in 2026, making it the largest contributor within the healthcare and laboratory labels market. This dominance is supported by stringent regulatory requirements related to product traceability, serialization, tamper evidence, dosage instructions, and expiry labeling across both branded and generic medicines. Pharmaceutical manufacturers and contract development and manufacturing organizations (CDMOs) require validated label suppliers capable of meeting compliance standards for multi-language printing, GS1-compliant barcoding, and anti-counterfeiting features. High-value pharmaceutical packaging frequently incorporates multi-layer booklet labels, peel-and-reseal constructions, and tamper-evident seals for injectables and biologics. For instance, temperature-sensitive biologic vials require durable labels that remain legible throughout cold-chain logistics. Given the scale of global drug production and regulatory enforcement intensity, pharmaceutical labeling maintains both volume and value leadership in the market.

The medical device segment is anticipated to register the highest growth rate through 2033. Growth is fueled by device miniaturization, personalized implants, expansion in surgical procedures, and stricter Unique Device Identification (UDI) regulations across major markets. Device labels must accommodate regulatory symbols, manufacturing details, sterilization indicators, and serialized identifiers within a limited surface area. Labels for implantable devices, surgical instruments, and diagnostic equipment must withstand sterilization processes such as gamma radiation, EO gas, and high-pressure steam autoclaving without compromising adhesion or barcode clarity. For example, orthopedic implants and cardiac stents require permanent identification labels for traceability throughout their lifecycle. Hospital asset tracking systems increasingly use durable polyester or polyolefin labels embedded with 2D barcodes or RFID tags for equipment management. These technical requirements elevate average label value per unit, driving accelerated growth in this application segment.

Regional Insights

North America Healthcare and Laboratory Labels Market Trends - Regulatory-Driven Serialization and High Diagnostic Throughput

North America accounts for approximately 45.7% of the market share in 2026, making it the leading regional contributor. The U.S. drives the majority of regional revenue, supported by its extensive installed base of hospital printers, high-volume diagnostic laboratories, pharmaceutical manufacturing facilities, and contract research organizations (CROs). Strong healthcare expenditure and regulatory enforcement sustain high per-capita label consumption and demand for validated, medical-grade constructions. The U.S. market benefits from large integrated hospital systems and national laboratory networks that require standardized labeling formats for patient identification, specimen tracking, and pharmaceutical packaging. Canada contributes through specialty medical device manufacturing and regulatory alignment with U.S. standards, while Mexico presents growth opportunities through expanding pharmaceutical production and regional supply-chain integration.

Growth in North America is driven by regulatory complexity and traceability mandates, including FDA labeling rules and GS1 standards adoption, which require serialized, durable, and legible labels across pharmaceuticals and devices. High diagnostic throughput, both centralized and point-of-care, continues to increase specimen-label volumes. Third, strong clinical trial and biologics activity support demand for cold-chain compatible, tamper-evident, and serialized labeling solutions. The regulatory environment elevates compliance costs but strengthens long-term supplier relationships. Companies offering validated adhesives, biocompatibility documentation, and stability testing secure preferred vendor status and extended procurement cycles. Investment activity in the region focuses on automation of narrow-web converting lines, digital printing for short-run serialized jobs, and data-enabled labeling services. Sustainable label constructions and recyclable facestocks are also gaining visibility as healthcare providers incorporate environmental criteria into procurement decisions.

Europe Healthcare and Laboratory Labels Market Trends - MDR/IVDR Compliance and Multilingual Standardization

Europe represents a mature yet steadily expanding regional market supported by advanced pharmaceutical manufacturing clusters and harmonized regulatory frameworks. Germany, the U.K., France, and Spain drive demand through medical device production, contract packaging, and expanding diagnostic networks. Germany maintains a strong industrial base for medical device manufacturing and pharmaceutical exports. The U.K. remains a hub for clinical trials and life-science innovation. France and Spain are investing in hospital modernization and laboratory centralization programs, increasing labeling standardization and automation.

Regional growth is primarily influenced by regulatory harmonization under the EU Medical Device Regulation (MDR) and In Vitro Diagnostic Regulation (IVDR), which increase labeling and documentation requirements. These regulations mandate clearer symbol usage, multilingual instructions, and enhanced traceability, elevating demand for compliant, technically validated labels. Sustainability initiatives also influence purchasing decisions, encouraging the adoption of recyclable paper facestocks and removable-adhesive constructions.

Healthcare digitization further supports the integration of barcode standards and interoperability across hospital information systems. Compliance with EN ISO 15223-1 symbol standards and documentation requirements raises validation thresholds for suppliers, creating barriers to entry but favoring established converters with regulatory expertise. Investment trends in Europe emphasize advanced digital printing capabilities, multilingual production lines, and acquisitions aimed at building pan-European supply networks.

Asia Pacific Healthcare and Laboratory Labels Market Trends - Pharma Expansion and Rapid Localization of Medical-Grade Converting

Asia Pacific is the fastest-growing regional market, supported by expanding pharmaceutical manufacturing, rapid laboratory infrastructure development, and increasing localization of converting capacity. Growth is the strongest in China, Japan, India, and ASEAN economies. China continues to scale pharmaceutical and diagnostic production, with domestic converters upgrading to medical-grade materials and validated processes. Japan maintains a strong demand for high-precision devices and diagnostic labeling. India’s growing CRO sector and expanding laboratory networks support rising specimen-label volumes, while ASEAN nations invest in centralized lab systems and contract packaging capabilities.

Regional growth is driven by manufacturing onshoring, export-oriented pharmaceutical production, and public health investments that expand testing capacity. As governments strengthen regulatory alignment with international standards such as ISO, WHO, and GS1 frameworks, demand for compliant and serialized labeling increases. Local converting hubs provide cost advantages and shorter lead times compared to imports, accelerating adoption of advanced label formats. Investment opportunities center on establishing regional validation labs, certified medical-grade material lines, and partnerships between global label-material suppliers and local converters. Multinational firms are expanding through joint ventures and capacity additions to capture long-term growth.

Competitive Landscape

The global healthcare and laboratory labels market is moderately fragmented. A limited group of multinational converters and material suppliers holds meaningful, but not dominant, market shares, while a broad base of regional converters serves localized and niche requirements. Although leading companies such as Avery Dennison, Brady Corporation, and 3M account for a notable portion of top-tier revenues, the overall market remains far from highly concentrated.

Even the top ten players collectively control well below full market share, reflecting the presence of numerous regional specialists and application-focused providers across different geographies. Suppliers compete on their ability to provide labels engineered for chemical exposure, extreme temperatures, sterilization processes, and long-term durability, while also supporting regulatory compliance and traceability requirements. Companies with distributed converting operations benefit from shorter lead times, local regulatory familiarity, and improved customer responsiveness.

Dominant strategies in the market include validated-material leadership, vertical integration, digital and variable data printing (VDP) capabilities, and geographic expansion. Market leaders increasingly combine label converting with compliance documentation, data services, and validation support to offer bundled solutions. Long-term supply agreements, certification assistance, and integrated printing and serialization services further strengthen competitive positioning, enabling leading suppliers to secure recurring contracts and deepen customer relationships within the healthcare and laboratory sectors.

Key Industry Developments:

- In April 2025, Schreiner MediPharm introduced NFC-enabled anti-counterfeiting labels for self-administered injectable drugs, combining smartphone authentication with secure traceability to protect against counterfeit products.

- In July 2025, IL Group launched its Light Protect Pack label solution, engineered to protect light-sensitive medications while maintaining visibility and compliance throughout supply-chain handling.

Companies Covered in Healthcare and Laboratory Labels Market

- Avery Dennison Corporation

- CCL Industries Inc.

- 3M Company

- Brady Corporation

- Zebra Technologies Corporation

- UPM Raflatac

- SATO Holdings Corporation

- Multi-Color Corporation

- Schreiner Group GmbH & Co. KG

- Honeywell International Inc.

- Nitto Denko Corporation

- LINTEC Corporation

- HERMA GmbH

- Cenveo Worldwide Limited

- Constantia Flexibles Group GmbH

- Fuji Seal International Inc.

- Labelcraft Products Ltd.

- Denny Bros Ltd.

Frequently Asked Questions

The global market size is estimated to be valued at approximately US$9.8 billion in 2026.

The healthcare and laboratory labels market is projected to reach approximately US$14.5 billion by 2033.

Key trends include the increasing adoption of serialization and variable data printing (VDP), demand for cryogenic and chemical-resistant labels, expansion of RFID-enabled tracking, and rising use of sustainable and linerless label materials.

The pharmaceutical application segment is expected to lead the healthcare and laboratory labels market, accounting for nearly 44.5% of market share in 2026, due to strict regulatory labeling requirements and global drug manufacturing scale.

The healthcare and laboratory labels market is expected to grow at a CAGR of approximately 5.8% during the forecast period.

Major players include Avery Dennison Corporation, CCL Industries Inc., 3M Company, Brady Corporation, and UPM Raflatac.