- Processed Food

- Gravy Mixes Market

Gravy Mixes Market Size, Share and Growth Forecast, 2026 - 2033

Gravy Mixes Market by Product & Formulation (Vegan, Non-Vegan, Powder, Liquid, Single-Serve), Nutritional Insights (Organic, Gluten-Free, Low-Sodium, Allergen-Friendly, Keto), Distribution (Modern Grocery, Online, Foodservice), and Regional Analysis for 2026 - 2033

Gravy Mixes Market Share and Trends Analysis

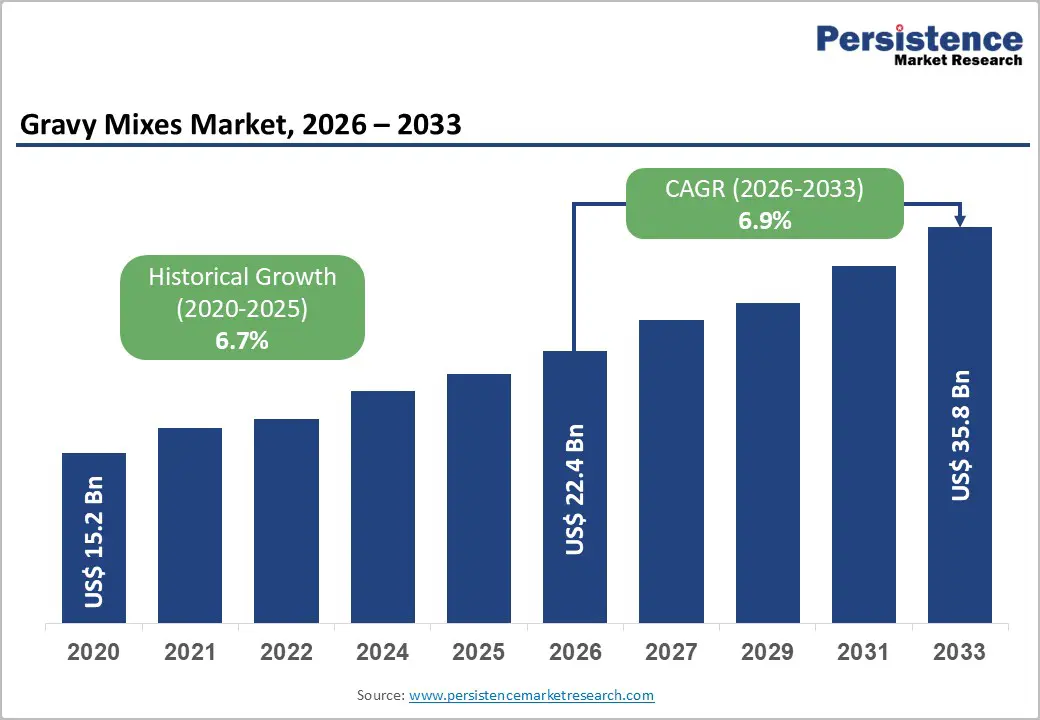

The global gravy mixes market size is likely to be valued at US$ 22.4 billion in 2026 and is projected to reach US$ 35.8 billion by 2033, growing at a CAGR of 6.9% during the forecast period 2026 - 2033.

The market is growing due to evolving consumer preferences for convenient, time-saving meal solutions and increasing demand for health-conscious and specialty formulations such as gluten-free, vegan, and low-sodium variants. Functional benefits, including consistent flavor, extended shelf life, and ease of preparation, enhance adoption in both household and foodservice applications.

Expansion of end-use sectors, particularly modern grocery retail, online food delivery, and quick-service restaurants, supports distribution growth. Additionally, rising disposable incomes, accelerating urbanization, and expanding middle-class populations in emerging markets drive higher consumption, creating sustained demand and enabling manufacturers to scale product availability and regional penetration effectively.

Key Industry Highlights

- Dominant Product & Formulation Segments: Non-vegan mixes are projected to hold approximately 45% of the market share in 2026, while vegan mixes are expected to grow positively by 2033, driven by increasing adoption of plant-based diets and health-conscious consumption.

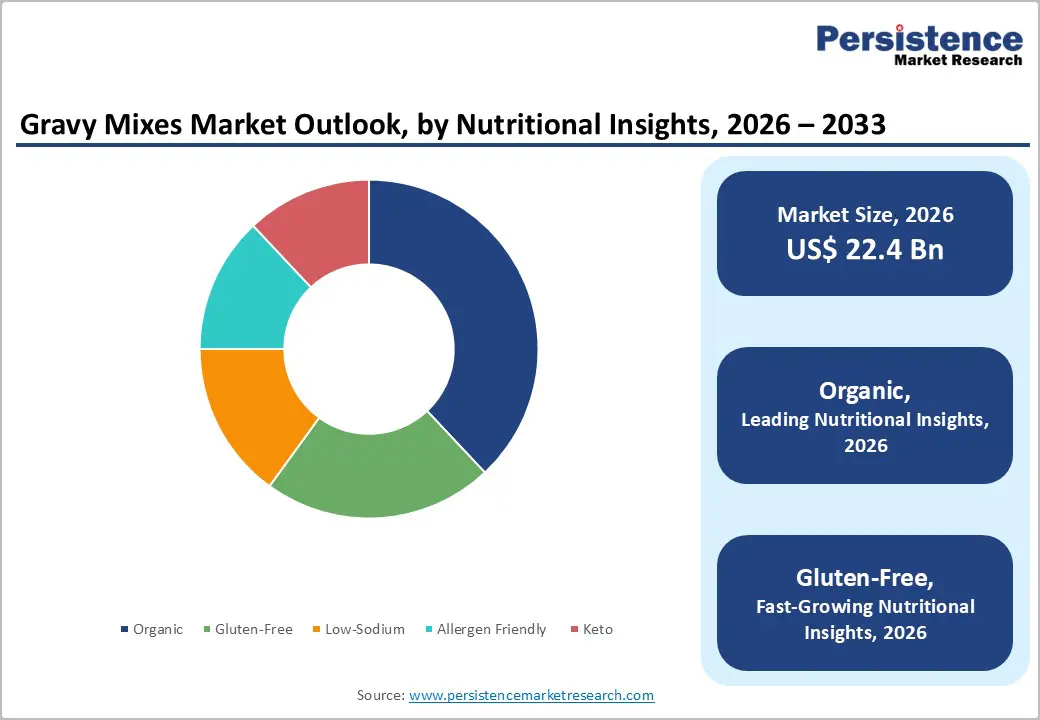

- Leading Nutritional Insights: Organic formulations are anticipated to account for roughly 38% of the market in 2026, whereas gluten-free and mixes are likely to expand the fastest during 2026 - 2033, reflecting rising demand for clean-label and specialty products.

- Dominant Distribution Channels: Modern grocery retail is expected to command the largest share at about 52% in 2026, while online retail channels are projected to achieve robust growth fueled by e-commerce penetration and convenience-driven purchasing.

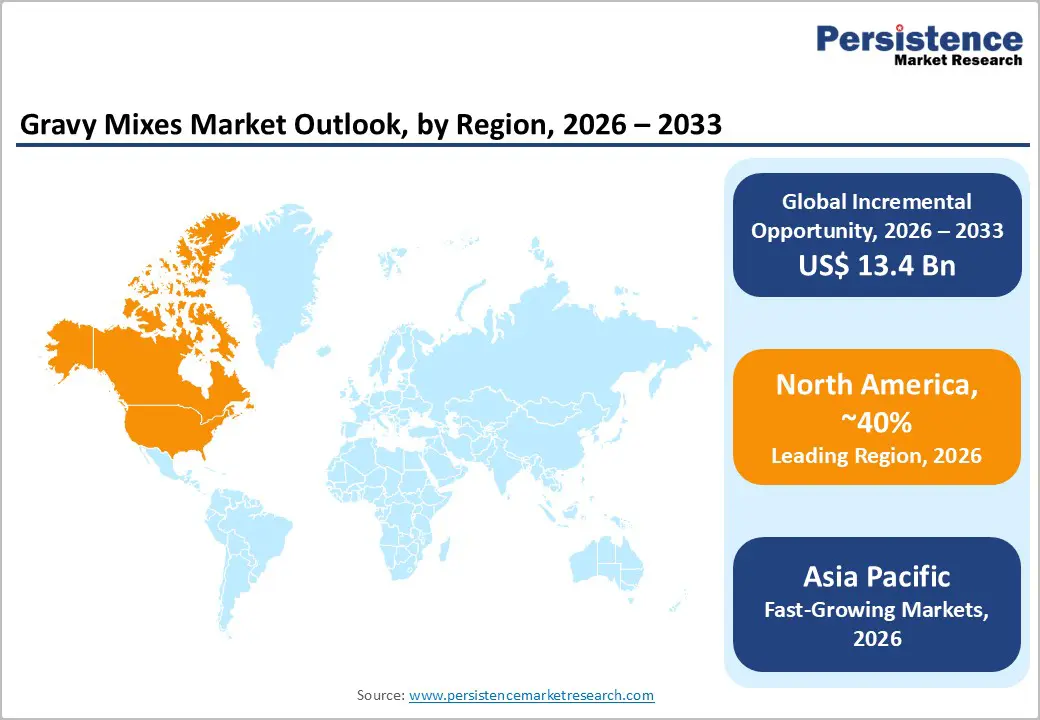

- Regional Leadership: North America is poised to dominate with an estimated 40% market share in 2026, while Asia Pacific is projected to register the fastest growth at a CAGR, supported by urbanization, rising incomes, and an expanding middle-class population.

- Competitive Environment: Market dynamics are shaped by product innovation, sustainability-focused initiatives, strategic mergers and acquisitions, and geographic expansion into high-growth regions such as the Asia Pacific and Latin America.

| Key Insights | Details |

|---|---|

| Gravy Mixes Market Size (2026E) | US$ 22.4 Bn |

| Market Value Forecast (2033F) | US$ 35.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.7% |

DRO Analysis

Driver - Rising Demand for Convenient Ready-to-Prepare Foods

Consumer preference for quick, easy-to-prepare meals is a significant growth driver in the gravy mixes market. Busy lifestyles, increased work hours, and the rise of dual-income households have intensified demand for convenience-oriented food solutions. Gravy mixes remove the complexities of traditional cooking, delivering consistent flavour and texture with minimal effort, which encourages repeated usage across households. This trend aligns with broader shifts in global food retail, where formats are innovating to cater to speed, portability, and ready-to-eat needs, blurring the lines between retail and foodservice convenience.

The convenience trend is also reflected in the rising prominence of hybrid store formats and expanded ready meal offerings, which integrate prepared foods with grocery purchases more seamlessly than ever before. Additionally, convenience food is becoming a fixed part of everyday diets worldwide, with a large proportion of consumers purchasing ready meals at least weekly, a structural pattern that supports long-term adoption of products such as gravy mixes. These developments are further supported by retailers introducing meal kits and complementary product bundles, enhancing consumer exposure and habitual use of convenient cooking solutions.

Increasing Health & Specialty Nutrition Awareness

Rising health consciousness among consumers is reshaping ingredient preferences and product development strategies in the gravy mixes market. Gluten-free, low-sodium, organic, and allergen-friendly gravy mixes are becoming increasingly popular as individuals prioritise wellness and dietary customisation. This shift is part of a much larger movement where "free-from" foods and healthier alternatives increasingly transition from niche categories to mainstream grocery baskets, supported by growing consumer knowledge and retail availability.

The international gluten-free food market is projected to expand significantly through 2033 at a high CAGR, driven by rising awareness of gluten sensitivities and a broader perception of gluten-free as a healthier choice, beyond medical necessity. As such, health-oriented innovation is a key driver for product reformulation, encouraging manufacturers to enhance nutrition profiles, improve ingredient transparency, and deliver better-for-you alternatives that resonate with modern dietary values. Government nutrition guidance and stricter labeling regulations further reinforce these trends, enabling consumers to make informed choices and driving the adoption of specialized, health-conscious gravy mixes.

Restraints - Preference for Traditional and Homemade Alternatives

Despite the rising demand for convenience foods, a key restraint in the gravy mixes market is consumer preference for traditional homemade gravies. In regions with rich culinary heritage and strong local taste profiles, fresh ingredients, herbs, and spices are favored for authenticity, limiting packaged product adoption. Many households continue to value personalization and the perception of superior taste in homemade preparations, which challenges packaged alternatives. This preference is especially visible in cultural food markets where traditional cooking practices remain deeply rooted.

Additionally, intermittent food inflation and price sensitivity reinforce homemade cooking choices. For example, global food prices have experienced pronounced upward pressure in early 2026 due to disruptions such as geopolitical tensions and commodity cost increases, which can lead households to rely more on scratch cooking to manage budgets. Consumers concerned about preservatives or artificial ingredients may also avoid processed mixes, slowing adoption among health-focused demographics and reinforcing loyalty to traditional methods. This dynamic creates a structural ceiling on market penetration in certain regions, particularly in developing markets where culinary heritage strongly influences purchasing decisions.

Raw Material Price Volatility

Price fluctuations for essential food inputs pose a significant challenge for gravy mix manufacturers. According to recent USDA food price outlook data, broad food-at-home prices rose through early 2026 and remain elevated compared with prior years, reflecting persistent inflationary pressures across multiple categories. Ingredients such as spices, thickeners, and flavourings are subject to these supply chain cost shifts, increasing production expenses and compressing margins. In turn, manufacturers face pressure to either absorb costs or pass them on to consumers, which may weaken demand among price-sensitive segments.

These structural cost pressures are compounded by global market volatility and geopolitical influences on agricultural commodities, which further affect input costs and availability. As consumer budgets tighten under sustained high grocery bills, retailers and food producers must balance product quality with competitive pricing. The volatility also impacts long-term planning, as companies may hesitate to expand production or launch new products until supply costs stabilize. This ongoing instability in raw material pricing creates uncertainty for long-term growth and can delay innovation in convenience-focused and health-oriented product lines.

Opportunities - Expansion in Emerging Markets

Emerging economies in Asia Pacific and Latin America offer significant growth potential for the gravy mixes market. Rising disposable incomes, a growing middle class, and rapid urbanization are reshaping food consumption patterns, boosting demand for convenient and ready-to-prepare products. Producers can capitalize on these trends by expanding distribution networks and tailoring products to local tastes, including regional flavor variants and culturally aligned marketing campaigns. This approach enables companies to address unmet demand and accelerate adoption. Strategic collaborations with local distributors and food retailers can further enhance product reach, ensuring timely availability across urban and semi-urban centers.

Supporting this, real-world retail developments in 2025 show that convenience store and modern trade expansion in India, China, and Southeast Asia is rapidly increasing product accessibility, particularly for packaged foods and ready-to-cook components such as gravies. These retail innovations provide structured avenues for introducing new products while strengthening brand recognition. Coupled with government initiatives promoting organized retail infrastructure and food processing investments, these factors create a strong foundation for market growth, allowing brands to capture an estimated 10-15% incremental share over the next decade. Demographic shifts and increasing urban consumer sophistication further reinforce the opportunity for market expansion.

Growth of Online & Direct-to-Consumer (D2C) Channels

The surge in online grocery and D2C channels presents a major expansion opportunity. Digital platforms reduce distribution friction, enable personalized marketing, and allow direct engagement with urban and semi-urban consumers. Online channels also provide actionable data on buying behavior, helping companies optimize offerings, pricing, and promotions while supporting faster adoption of niche products such as vegan, keto, or allergen-friendly gravy mixes. Subscription-based models and targeted promotions can further increase consumer retention and drive repeat purchases, creating sustainable revenue streams.

Recent news from 2025 highlights that online grocery penetration continues to grow fastest in Asia and North America, with digital adoption and quick-commerce infrastructure significantly expanding consumer reach. Quick commerce and same-day delivery models are lowering the barriers to trial for convenience and specialty products, further accelerating category adoption. These trends support premium and functional product launches while creating direct, scalable channels that increase brand loyalty. Combined with rising smartphone penetration and digital literacy, D2C offers a high-margin, long-term growth pathway for both mainstream and niche product lines in emerging and developed markets.

Category-wise Analysis

Product & Formulation Insights

Non-vegan gravy mixes are expected to hold approximately 45% of the product & formulation revenue in 2026, driven by broad appeal among traditional meat-eating consumers and frequent use in everyday and festive meals. Their versatility and deep flavor profiles support repeat purchases and strong retail performance across supermarkets and grocery aisles. Mainstream availability through modern grocery and private-label portfolios strengthens visibility and reinforces consumption habits.

In 2025, Amazon Grocery launched a new private-label lineup with over 1,000 everyday grocery essentials, including shelf-stable sauces and meal accompaniments, underscoring robust demand for familiar, value-oriented formats. These developments underline non-vegan mixes as enduring staples amid shifting retail strategies.

Vegan gravy mixes are forecast to grow at an approximate CAGR of 8.1% through 2033, buoyed by rising plant-based diets, sustainability concerns, and greater taste parity with conventional products. Enhanced flavor innovation and broader shelf presence in both modern grocery and online channels are expanding adoption beyond niche audiences. During Veganuary 2026, brands such as Aldi’s Plant Menu and Beyond Meat’s expanded line introduced several new plant-based offerings, from vegan Pepperami-style snacks to high-protein drinks, reflecting retailer confidence in mainstream plant-based demand and encouraging parallel category growth. These initiatives strengthen the cultural and retail momentum supporting vegan gravy mixes.

Nutritional Insights

Organic gravy mixes are poised to lead the nutritional insights category with roughly 38% of segment revenue in 2026, anchored in consumer demand for clean-label, minimally processed ingredients. Certified organic claims resonate with health-oriented shoppers who prioritize ingredient transparency and natural formulations, commanding price premiums in key markets. Organic product momentum continued strongly in 2025, with U.S. organic food sales reaching a record US$ 76.6 billion and outpacing the conventional market by more than twofold, signaling widespread consumer prioritization of organic options.

Retailers and specialty grocers are expanding organic assortments, reinforcing visibility for organic staples and prepared goods alike, thereby supporting gravy mix adoption among discerning buyers.

Gluten-free gravy mixes are expected to grow at an approximate CAGR of 7.9% from 2026 to 2033, reflecting heightened consumer awareness of dietary needs and stronger retail penetration. Mainstream shoppers increasingly choose gluten-free options for both health and lifestyle reasons, expanding the segment beyond niche medical demand. In 2025, Banza introduced new gluten-free brown rice pasta nationwide at Whole Foods, addressing texture and flavour gaps that historically limited mainstream gluten-free adoption.

Advances such as these have made gluten-free foods, particularly pastas, snacks, and meal components, more accessible and appealing, reinforcing growth potential for allergen-friendly gravy mixes as part of broader dietary solutions.

Regional Insights

North America Gravy Mixes Market Trends

North America is expected to remain the largest regional share of the global gravy mixes market, with approximately 40% of total revenue in 2026, driven primarily by the United States’ entrenched preference for convenience and packaged foods. Well-developed modern retail infrastructure, high disposable incomes, and robust supply chains support widespread distribution. Regulatory frameworks, shaped by entities such as the U.S. Food and Drug Administration (FDA), ensure food safety standards and transparent labeling, reinforcing consumer trust in packaged meal components.

Technological advancements in food processing and packaging further extend product shelf life and consistent quality, enabling broad penetration across households and foodservice channels.

Retail expansion activities also underscore North America’s leadership. In 2026, PepsiCo announced strategic reforms focused on boosting sales and enhancing product affordability and nutritional content, which included plans to introduce new high-protein and whole-grain offerings and optimize supply chains for broader market reach. Such strategic initiatives from major food companies reflect confidence in packaged food categories and indirectly support demand for convenience-oriented products such as gravy mixes.

With ongoing innovation, online grocery adoption, and targeted portfolio diversification, North America is positioned to sustain leadership and reinforce its benchmark role in the global market.

Europe Gravy Mixes Market Trends

Europe represents a consistently expanding market for gravy mixes, underpinned by harmonized EU regulations that emphasize product safety, nutritional transparency, and sustainable practices. Mature retail channels across Germany, France, and the U.K. cater to both traditional and convenience-oriented eating occasions, with consumer preferences increasingly favoring organic and functional food products.

Nutrition claims and health-driven choices have become central to buying decisions, especially among younger and wellness-focused consumers. This regulatory predictability and consumer sophistication supports the regional growth by 2033, making Europe one of the hottest destinations for this category.

Concrete evidence of this expansion is seen in 2026 retail dynamics: Whole Foods Market announced plans to double its UK store count by mid-2026, increasing access to organic, fresh, and specialty food products across London and surrounding areas. This planned expansion reflects broader European consumer demand for high-quality, responsibly sourced food and enhances distribution channels for convenience items and packaged meal components. Additionally, the UK and broader European organic food sector continued strong growth in 2025-2026, with rising sales and supermarket chain commitments to organic ranges that demonstrate sustained demand for health-oriented foods.

Asia Pacific Gravy Mixes Market Trends

The Asia Pacific region presents compelling growth prospects for gravy mixes, driven by rising urbanization, expanding middle-class incomes, and evolving dietary patterns that increasingly incorporate Western-style convenience foods alongside traditional cuisine. Countries such as China, Japan, and India are pivotal growth drivers, where expanding modern grocery formats and digital marketplaces boost product accessibility and visibility. Large populations and rapidly shifting food preferences underpin a projected CAGR of 6.9% by 2033, reflecting robust appetite for convenient packaged foods in both retail and foodservice channels.

Supporting this, the Asia-Pacific food packaging market exceeded USD 160 billion in 2024 and continued growth in 2025, driven by consumer demand for convenience foods, rising incomes, and government initiatives promoting sustainable and safe food packaging solutions. These developments highlight structural expansion in supply chains and retail ecosystems facilitating greater penetration of packaged meal components such as gravy mixes.

Digital commerce growth and expanding organized retail networks also enhance distribution reach in urban and peri-urban markets, positioning Asia Pacific as a high-growth region with significant long-term potential for both global and local brands.

Competitive Landscape

The global gravy mixes market is moderately consolidated, with leaders such as McCormick & Company, Unilever, Nestlé, Kraft Heinz, and General Mills controlling a substantial revenue share. These companies leverage strong retail networks, consumer loyalty, and multi-channel marketing. Investment in R&D drives product innovation in plant-based, organic, gluten-free, and allergen-friendly variants. Advanced packaging and flavor research further strengthen their market positioning.

Regional and niche players, including Olam International, Ajinomoto, and Gits Food Products, focus on local flavors and specialty diets, building strongholds in emerging markets. Regulatory compliance, supply chain complexity, and brand trust limit new entrants. Growth in e-commerce and D2C channels enables smaller players to capture niche segments. Strategic mergers, acquisitions, and sustainability initiatives continue to shape competitive dynamics.

Key Developments:

- In March 2026, McCormick and Unilever combined Unilever’s Foods business in a US$ 65 billion deal, creating a global flavor leader with brands like Knorr, Hellmann’s, French’s, and Cholula, aiming to expand in high-growth condiment and sauce markets.

- In March 2026, Sysco acquired Jetro for US$ 29.1 billion, entering the “Cash & Carry” sector with 166 U.S. warehouses, strengthening its foodservice distribution network and market reach.

Companies Covered in Gravy Mixes Market

- Southeastern Mills, Inc.

- McCormick & Company

- Campbell Soup Company

- Edward & Sons

- Kent Precision Foods Group

- Knorr

- Food Club

- Schwartz

- Pioneer Foods

- Suhana Masala

Frequently Asked Questions

The global gravy mixes market is projected to reach US$ 22.4 billion in 2026.

Rising demand for convenient, ready-to-use meals and growing health-conscious consumption are driving the market.

The market is poised to grow at a CAGR of 6.9 % from 2026 to 2033.

Expansion in emerging markets and online sales channels present the largest opportunities for growth.