- Technology

- Geofencing Market

Geofencing Market Size, Share, and Growth Forecast, 2026 – 2033

Geofencing Market by Technology Type (GPS, Wi-Fi, RFID/Bluetooth/Cellular), Target Audience (B2C, B2B), Geofencing Type (Fixed, Mobile), End-user Vertical (Retail, Logistics/Transport, BFSI, Others), and Region Analysis 2026 – 2033

Geofencing Market Size and Trends Analysis

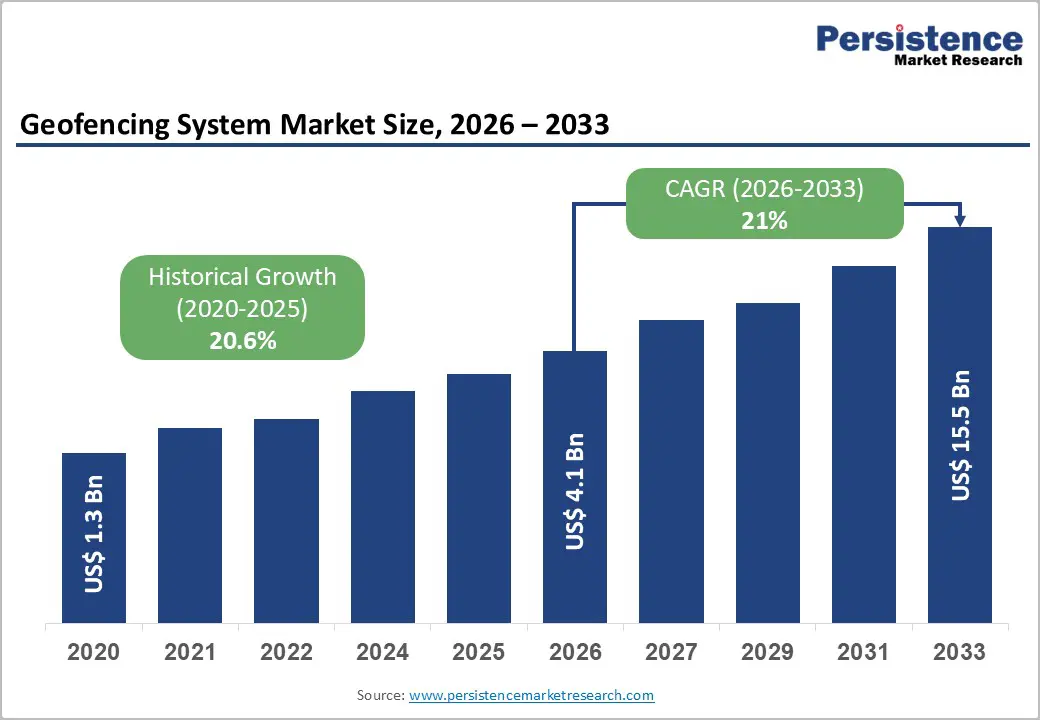

The global geofencing market size is likely to be valued at US$4.1 billion in 2026 and is expected to reach US$15.5 billion by 2033, growing at a CAGR of 21% during the forecast period from 2026 to 2033, driven by rapid adoption of location-based marketing, fleet and asset tracking, and security applications, geofencing is moving from pilot deployments to enterprise-scale rollouts.

Advances in GPS, BLE, Wi-Fi, and cellular networks, along with the rise of smartphones and IoT devices, are strengthening the tech stack. Key demand is emerging from retail, logistics, and BFSI, driven by IoT in logistics, retail, and urban planning. Meanwhile, strict data privacy regulations continue to shape the landscape.

Key Industry Highlights:

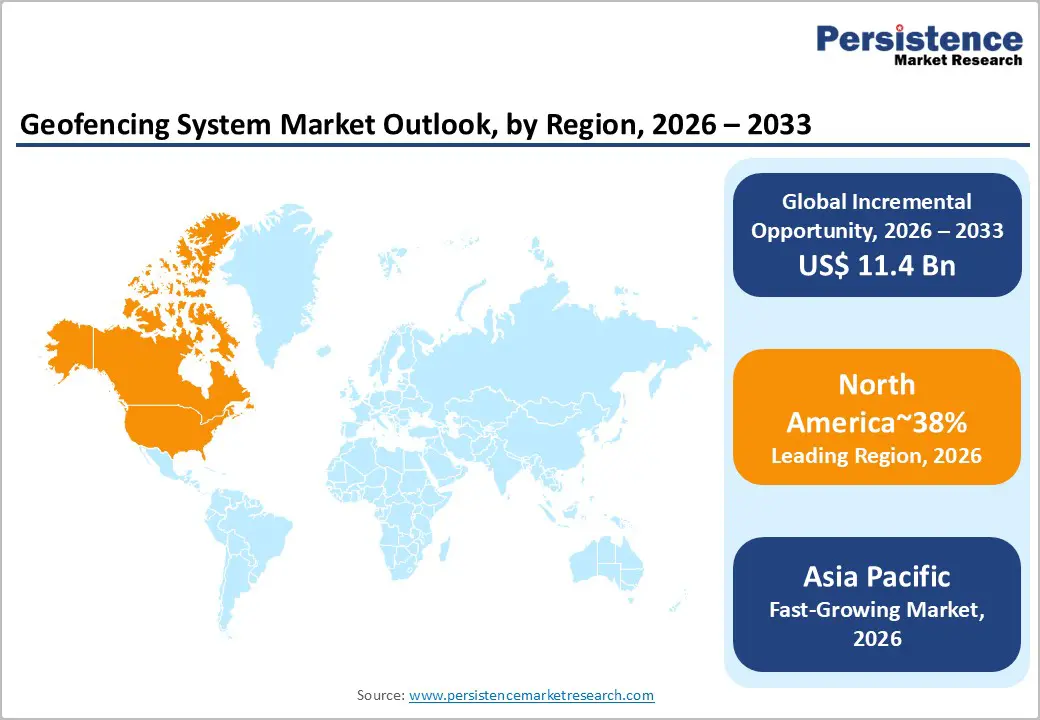

- Leading Region: North America is expected to lead the geofencing market with approximately 38% share, supported by early adoption of location-based marketing, high penetration of smartphones and connected devices, mature digital advertising ecosystems, and advanced enterprise mobility infrastructure.

- Leading Technology: GPS-based geofencing holds around 48% share, reflecting its dominance in outdoor location tracking use cases such as fleet management, asset monitoring, mobility services, and large area perimeter enforcement, where satellite-based positioning provides reliable coverage and mature device compatibility.

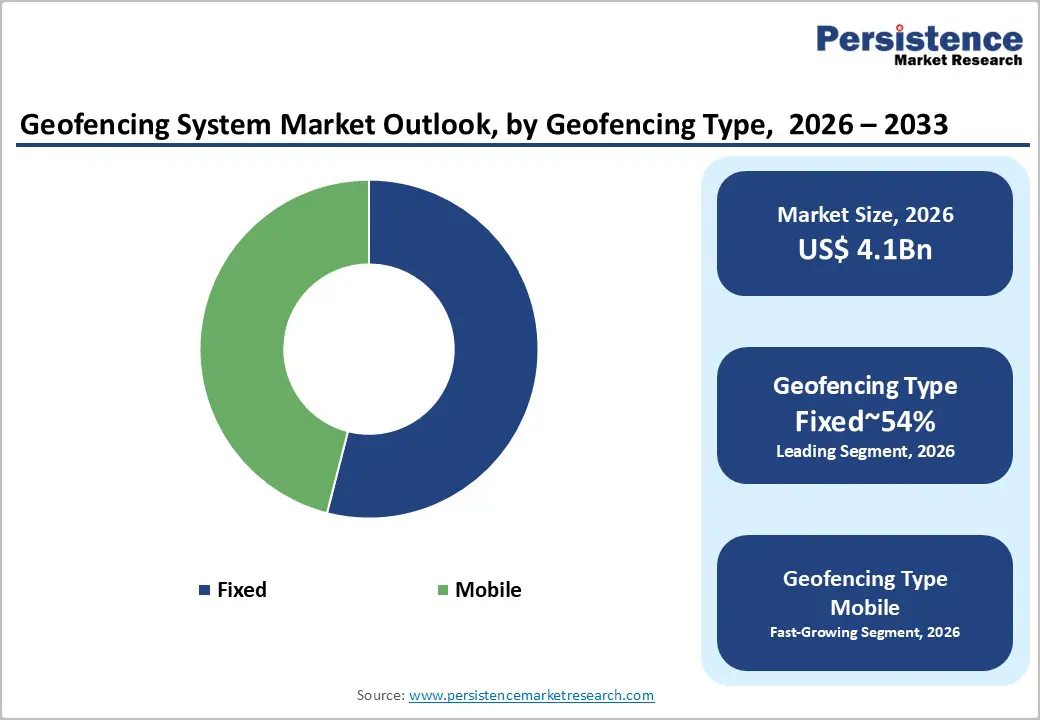

- Leading Geofencing Type: Fixed geofencing represents approximately 54% share, supported by its widespread deployment in static perimeter applications such as retail store zones, warehouse boundaries, restricted industrial areas, and security-controlled locations, where predefined virtual perimeters enable consistent rule-based automation.

| Key Insights | Details |

|---|---|

| Geofencing Market Size (2026E) | US$ 4.1 Bn |

| Market Value Forecast (2033F) | US$ 15.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 21% |

| Historical Market Growth (CAGR 2020 to 2025) | 20.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Proliferation of Smartphones, IoT, and Connected Devices

Smartphone penetration and the rapid growth of IoT are expanding the installed base for location-based services, embedding geofencing across both consumer and industrial sectors. The widespread availability of devices enables low-latency, real-time positioning through hybrid GNSS, cellular, and short-range radios, enhancing perimeter enforcement in logistics, urban infrastructure, and retail.

As geofencing integrates with workflow automation and customer engagement, demand shifts from isolated applications to platform-level solutions. This drives revenue growth for software platforms and API services, reducing delivery costs while increasing reliance on cloud processing. Regulatory frameworks around consent, data localization, and cross-border telemetry add complexity, favoring standardized architectures and data compliance. This boosts the importance of scalable location middleware and secure data management, leading to stable, recurring revenue. In May 2025, Google and Samsung partnered to enhance geofencing accuracy, driving growth in mobile ecosystems.

Rising Adoption in Logistics, Transportation, and Compliance-driven Sectors

Geofencing is becoming integral to fleet management, last-mile delivery, and cold chain operations, where continuous location tracking and route adherence are critical. By integrating GPS and cellular triggers into workflows such as dispatch, proof of delivery, and asset custody, location data is transformed into actionable process controls, creating virtual boundaries within transportation and warehouse management systems. This shift makes real-time boundary logic a core component of logistics platforms, evolving geofencing from an optional feature to a baseline capability.

Regulatory pressures around duty logging, hazardous routing, and sensitive zone protection are further driving the adoption of geofencing as essential compliance infrastructure. In sectors such as financial services and government, location constraints ensure transaction integrity and risk containment, expanding geofencing beyond mobility into digital security. This demand for auditable, policy-driven location middleware and cloud orchestration layers increases switching costs for operators. The cumulative impact creates sustained institutional demand for scalable geofencing platforms across regulated industries. In November 2024, FedEx integrated dynamic real-time geofencing with AI-driven route optimization, improving last-mile delivery efficiency by reducing missed delivery attempts by 15%.

Barrier Analysis – Technical and Operational Frictions in Scalable Geofencing Deployment

Persistent technical challenges hinder widespread geofencing adoption across enterprise and consumer applications. Continuous GPS-based location tracking results in significant battery drain on mobile and IoT devices, leading to higher opt-out rates and reduced long-term user engagement. Geofencing accuracy remains inconsistent, especially in urban areas and indoor environments, where signal occlusion and multipath interference undermine reliability. While Bluetooth Low Energy (BLE) offers some improvement, fragmented hardware standards and device compatibility issues complicate large-scale, interoperable deployments.

Geofencing requires stable GPS, Wi-Fi coverage, secure connectivity, and deep integration with systems such as CRM, marketing automation, TMS, and ERP, adding complexity to IT infrastructure. Cost and capability constraints, particularly for small to mid-sized businesses, further limit adoption. Indoor accuracy issues often necessitate additional investments in BLE beacons, Wi-Fi triangulation, or RFID, increasing upfront costs for retailers, warehouses, and transport hubs. The total cost of ownership is also elevated by software licensing, system integration, and device management, while ROI can be difficult to project. Inconsistent network quality and device standardization, particularly in emerging markets, exacerbate these challenges. In June 2025, Esri released updates to ArcGIS Location Services with enhanced geofencing tools such as “Snap to Roads,” signaling a trend toward more sophisticated GIS integration.

Opportunity Analysis – Convergence with Autonomous Systems and Smart City Platforms

The integration of geofencing with autonomous vehicles and drone delivery systems is poised to significantly expand location intelligence platforms. As drone regulations evolve, dynamic geofencing is becoming a critical control layer for virtual no-fly zones, airspace corridors, and adaptive routing within urban air mobility networks. Simultaneously, smart city initiatives extend geofencing into traffic management, electric vehicle charging zones, curbside access control, and public safety, aligning with long-term municipal digitalization efforts. These applications elevate geofencing from a simple perimeter trigger to a regulatory-compliant orchestration layer in urban mobility and civic operations.

The value of geofencing further increases through its convergence with AI analytics, digital twins, and IoT platforms. By embedding geofencing within cloud-native location intelligence suites, predictive fleet routing, anomaly detection, dynamic pricing, and automated resource allocation are enabled using real-time spatial data. As enterprises leverage cloud data platforms, geofencing events become key inputs for machine learning pipelines, driving experimentation, segmentation, and optimization. This shift expands monetization opportunities, moving from basic triggers to sophisticated analytics and decision-making workflows, enhancing platform value across logistics, retail, and smart manufacturing. In June 2025, the City of Singapore partnered with Esri to deploy a city-wide geofencing grid for autonomous public shuttles, ensuring safe integration of AVs within designated lanes and speeds.

Expansion into Indoor Spatial Analytics

While GPS remains the dominant modality for outdoor location intelligence, indoor positioning represents a structurally underpenetrated growth vector for geofencing platforms. Enterprises are increasingly deploying Wi-Fi and RFID/Bluetooth infrastructures to capture granular, meter-level spatial telemetry within enclosed environments such as retail stores, warehouses, hospitals, and transport terminals. This enables high-resolution insights into in-store movement patterns, dwell time by zone, queue dynamics, and asset flow, addressing a critical visibility gap in omnichannel operations. The shift expands geofencing applicability beyond perimeter enforcement into continuous, context-aware spatial intelligence across indoor operational domains.

The convergence of indoor positioning with cloud analytics and edge computing elevates geofencing from rule-based alerts to behavior-driven decision systems. Retailers can optimize planogram design, inventory placement, and labor scheduling using real-time zone analytics, while logistics operators can improve pick-path efficiency and congestion management within fulfillment centers. As indoor telemetry integrates with CRM, workforce management, and demand forecasting platforms, location events become high-frequency signals for machine learning models that support experimentation, micro-segmentation, and closed-loop operational optimization. This evolution materially increases solution value density, supports higher enterprise spend per deployment, and accelerates adoption across retail, healthcare, manufacturing, and large venue ecosystems.

Category-wise Analysis

Technology Type Insights

GPS-based geofencing is projected to dominate, accounting for approximately 48% share in 2026, underpinned by its universal availability and embedded presence across smartphones, vehicles, and industrial tracking devices. Adoption remains anchored by its indispensable role in outdoor, long-range positioning across logistics, agriculture, maritime, and autonomous mobility workflows, where alternative technologies lack coverage. Ongoing platform evolution, including dual-frequency GNSS support, LEO-based positioning augmentation, battery-efficient heartbeat tracking, and 5G-assisted hybrid positioning, continues to reinforce utilization intensity across fleet, asset, and workforce management use cases. Vendors such as Trimble, Garmin, and Esri, alongside platform providers such as Google Maps Platform and Mapbox, are expanding precision services and APIs to lock in enterprise geofencing workflows.

Bluetooth Low Energy (BLE) and Ultra-Wideband (UWB) are projected to be the fastest-growing geofencing technologies, driven by unmet indoor positioning needs and the performance limitations of GPS in enclosed environments. Growth is being catalyzed by centimeter-level ranging, virtual beacon integration within enterprise Wi-Fi, and energy-harvesting tags, which materially improve proximity accuracy, deployment scalability, and operating economics. Accelerating adoption is supported by AI-driven pathing analytics, digital twin integration for facilities management, and cross-platform standardization across mobile ecosystems, lowering operational friction for first-time indoor geofencing adopters. Companies including Cisco Meraki, Aruba (HPE), Kontakt.io, Estimote, BlueUp, and Wiliot are scaling infrastructure and sensing platforms to capture early-cycle enterprise demand.

Geofencing Type Insights

Fixed geofencing is projected to dominate, accounting for approximately 54% share in 2026, underpinned by its role as the primary infrastructure layer for location-triggered workflows across retail, government, and industrial environments. Adoption remains anchored by the stability of static coordinates, enabling low-latency triggers, reliable perimeter enforcement, and historical baseline modeling across storefronts, warehouses, enterprise zones, and regulated industrial sites. Ongoing platform evolution, including polygon-based perimeter modeling, predictive fixed zoning, multi-layered geofence hierarchies, and digital twin synchronization, continues to reinforce utilization across high-volume deployments. Vendors such as Salesforce, Adobe Experience Cloud, Esri, HERE Technologies, Radar, and Mapbox are expanding enterprise geofencing platforms and APIs to lock in long-term workflow integration.

Mobile geofencing is projected to be the fastest-growing geofencing type, driven by the shift toward dynamic, moving-entity interactions across on-demand logistics, autonomous mobility, and workforce safety use cases. Growth is being catalyzed by inter-device proximity standards, edge-AI–based proximity computation, and 5G-enabled low-latency communications, which materially improve responsiveness, safety enforcement, and real-time coordination between moving assets. Accelerating adoption is supported by dynamic pricing engines, temporary event-based mobile fencing, and transient geofencing architectures that reduce privacy and storage burdens for first-time implementers. Companies including Uber, Lyft, Samsara, Verizon Connect, Radar, Blue-dot Innovation, and AWS IoT Core are scaling mobility-centric platforms to capture early-cycle demand and embed switching costs across fleet and last-mile networks.

Regional Insights

North America Geofencing Market Trends

North America is expected to maintain its position as the largest regional market, with projections showing it holding approximately 38% of the market share in 2026. The U.S. leads this growth with strong adoption across retail, transportation, logistics, and media and entertainment, driven by high smartphone penetration and a mature digital advertising ecosystem. Canada contributes through initiatives in logistics, smart city projects, and public sector applications. The region’s growth is supported by advanced GPS infrastructure, widespread 4G/5G networks, and a strong cloud and app development ecosystem.

Regulatory impacts are mixed: while federal and state privacy laws such as the CCPA increase compliance burdens, clear regulations also facilitate the development of scalable, privacy-conscious solutions. North America is home to many leading platform providers, resulting in a consolidated high-end market alongside numerous niche SaaS firms. Investment has been robust, particularly in location-based marketing, telematics, and fleet management, with both venture capital and corporate funding targeting AI-driven geospatial analytics. A typical example includes large U.S. retailers leveraging GPS and Wi-Fi-based geofences for in-app promotions and curbside pickup coordination, while logistics companies use geofences around distribution centers to automate detention billing and monitor service level agreements (SLAs).

Europe Geofencing Market Trends

Europe is expected to remain a structurally important geofencing market, shaped by regulatory harmonization, industrial digitization, and urban mobility policy frameworks. Core demand is anticipated to be anchored by Germany, the U.K., and France, with Germany likely to sustain higher utilization across automotive, manufacturing logistics, and Industry 4.0 workflows, while the U.K. and France are expected to maintain comparatively stronger exposure in retail, financial services, and media-led location-based engagement. The integration of geofencing into sustainable mobility schemes, including low-emission zone management, shared mobility compliance, and urban traffic control, is likely to reinforce demand from municipal and transport authorities.

Regulatory oversight under GDPR and related e-Privacy frameworks is anticipated to continue shaping solution architectures through consent management, data minimization, and security-by-design requirements. While compliance obligations are likely to moderate deployment velocity relative to North America, they are expected to support a higher-trust operating environment, favoring enterprise-grade and public-sector implementations over purely marketing-led use cases. Cross-border logistics digitization and connected corridor initiatives are likely to sustain incremental uptake across freight tracking and fleet compliance, particularly in Germany and France, while smart city programs in Southern and Western Europe are expected to expand geofencing applications in transport management and urban services.

Asia Pacific Geofencing Market Trends

Asia Pacific is expected to remain the fastest-growing regional market for geofencing through the forecast horizon, with regional growth trajectories anticipated to outpace global averages as urbanization, mobile commerce, and platform-based service models scale across dense metropolitan corridors. China is expected to anchor volume deployment through e-commerce logistics, super-app ecosystems, and smart city programs, where platforms such as Alibaba and Tencent integrate geofencing into last-mile delivery, ride-hailing, and municipal service workflows. Japan is likely to sustain structurally higher penetration in industrial automation, automotive telematics, and logistics optimization, supported by network reliability and established manufacturing digitization programs, while India is expected to expand rapidly across retail engagement, mobility services, and public-sector applications linked to Smart Cities Mission deployments.

Regulatory environments across the region are expected to remain heterogeneous, with China and several ASEAN markets strengthening data localization and cybersecurity oversight, while other jurisdictions maintain more permissive digital innovation frameworks. This divergence is anticipated to reinforce the need for localized compliance architectures and hybrid cloud deployment models, particularly for global SaaS providers and telecom-led geofencing platforms. Competitive intensity is likely to remain high, combining regional cloud providers, super-app ecosystems, and global technology firms such as Google and Esri, alongside network-based location services offered by telcos. Manufacturing depth in China and Southeast Asia is expected to continue supporting cost-efficient scaling of hardware-enabled geofencing, including BLE beacons and telematics devices, reinforcing Asia Pacific’s positioning as a high-growth, scale-driven market with expanding public and commercial end-use adoption.

Competitive Landscape

The global geofencing market is moderately fragmented, with dominant platform players such as Google and Apple setting technical standards through OS-level location frameworks. At the application layer, specialized providers such as Ground-Truth (location-based marketing), Samsara (telematics), and Esri (spatial analytics) focus on tailored enterprise solutions. Large cloud and software vendors enhance their position by integrating geofencing with analytics, CRM, and IoT ecosystems.

Competitive dynamics reflect a split between horizontal platforms, which scale through ecosystem integration, and vertical specialists, which differentiate through industry-specific solutions, indoor accuracy, and privacy-focused architectures. Rising M&A activity indicates a shift towards ecosystem consolidation, as marketing clouds and enterprise software firms acquire niche geofencing startups, while competition remains specialized at the application layer.

Key Industry Highlights:

- In August 2025, Visa introduced "Location-Based Fraud Alerts" that utilize geofencing to match a card transaction location with a user's phone GPS. This significantly reduces false declines for travelers and adds a layer of security that traditional PIN-based systems lack.

- In June 2025, the City of Singapore partnered with Esri to deploy a city-wide geofencing grid for autonomous public shuttles. This ensures autonomous vehicles stay strictly within designated lanes and speeds, providing a blueprint for safe urban AV integration globally.

- In February 2025, Google officially rolled out "Protected Audience API" updates to its geofencing tools to align with Privacy Sandbox. This allows advertisers to target specific perimeters without accessing individual raw GPS data, overcoming the barrier of increasing privacy regulations.

Companies Covered in Geofencing Market

- Google LLC

- Apple Inc.

- Microsoft Corporation

- IBM Corporation

- Bluedot

- Radar Labs, Inc.

- ESRI

- Foursquare Labs Inc.

- Gimbal

- HERE Technologies

- Verizon Connect

- Samsara

- SZ DJI Technology Co. (DJI)

- Salesforce Inc.

- Airship

- Simpli.fi

- Location-Smart

Frequently Asked Questions

The global geofencing market is projected to be valued at US$4.1 billion in 2026 and is expected to reach US$15.5 billion by 2033, driven by its widespread adoption in location-based marketing, logistics, and security applications.

The widespread availability of smartphones and connected devices enables real-time, hybrid positioning (GPS, BLE, Wi-Fi), making scalable, low-latency geofencing viable for consumer engagement, logistics, and smart city applications.

The geofencing market is forecast to grow at a CAGR of 21% from 2026 to 2033, reflecting its rapid integration into enterprise workflows and its expansion into new applications such as autonomous systems and smart cities.

North America is the leading regional market, accounting for approximately 38% share, supported by high smartphone penetration, mature digital advertising and logistics ecosystems, and advanced GPS and cellular network infrastructure.

The market is moderately fragmented, with tech giants such as Google and Apple shaping OS-level location frameworks. Specialized providers such as ESRI, Samsara, and Radar lead in spatial analytics, fleet telematics, and marketing. Large cloud and CRM vendors such as Microsoft, IBM, and Salesforce play key roles through integrated solutions.