- Medical Devices

- Gastric Bands Market

Gastric Bands Market Size, Share, and Growth Forecast, 2026 - 2033

Gastric Bands Market by Product Type (Adjustable, Non-Adjustable), Surgery Type (Laparoscopic, Open), End-User (Hospitals & Surgical Centers, Ambulatory Surgical Centers (ASCs), Clinics & Specialty Bariatric Centers, Others), and Regional Analysis for 2026 - 2033

Gastric Bands Market Share and Trends Analysis

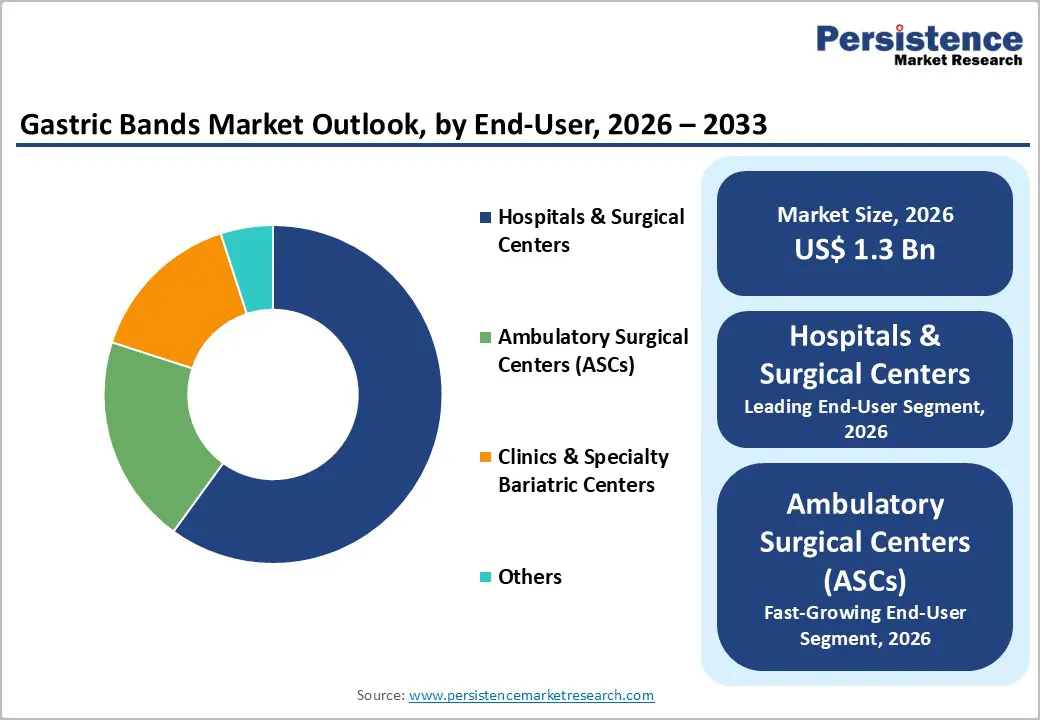

The global gastric bands market size is likely to be valued at US$ 1.3 billion in 2026, and is projected to reach US$ 1.8 billion by 2033, growing at a CAGR of 4.7% during the forecast period 2026−2033. Rising prevalence of obesity and metabolic disorders has created sustained demand for effective bariatric interventions. Increasing clinical awareness and adoption of minimally invasive treatments enhance patient trust and provider recommendation, influencing procedural volumes.

Technological integration in adjustable gastric bands, including improved silicone materials and remote adjustment capabilities, elevates treatment adherence and outcomes. Expansion of healthcare infrastructure in urban and semi-urban regions supports accessibility and procedural uptake. Government initiatives and insurance coverage for obesity management contribute to wider treatment penetration.

Key Industry Highlights

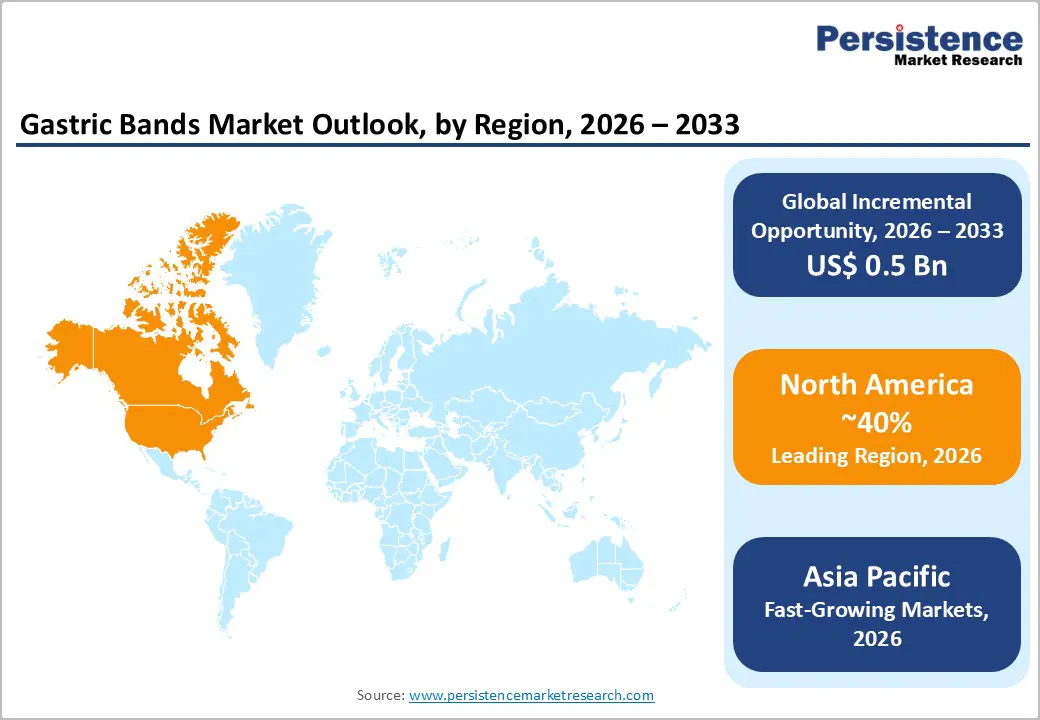

- Dominant Region: North America is poised to dominate the market with an estimated 40% share, driven by wide product adoption, strong presence of hospitals, and a robust reimbursement ecosystem.

- Fastest-growing Regional Market: Asia Pacific is slated to be the fastest-growing market from 2026 to 2033, owing to high obesity prevalence and rapidly improving healthcare infrastructure.

- Leading End-User: Hospitals and surgical centers are set to lead with nearly 60% revenue share, supported by volume, infrastructure, and multi-specialty services.

- Fastest-growing End-User: Ambulatory surgical centers (ASCs) are likely to be the fastest-growing end-user during 2026–2033, fueled by low cost, convenience, and outpatient adoption.

| Key Insights | Details |

|---|---|

|

Gastric Bands Market Size (2026E) |

US$ 1.3 Bn |

|

Market Value Forecast (2033F) |

US$ 1.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Obesity and Metabolic Disorders

Population-level increases in obesity and metabolic disorders are driven by lifestyle changes, urbanization, and dietary patterns that elevate body mass index and associated health risks. According to the World Health Organization (WHO), in 2022 about 43% of adults worldwide were overweight and approximately 16% were living with obesity, reflecting a significant increase compared with historical baselines. Excess weight disrupts metabolic regulation, increasing insulin resistance, chronic inflammation, and lipid imbalances. Individuals with these conditions often require interventions beyond conventional diet and exercise. The rising prevalence of metabolic disorders creates a larger pool of candidates for surgical procedures aimed at sustained weight reduction and mitigation of long-term health complications.

The growing incidence of obesity-related metabolic conditions imposes significant costs on healthcare systems due to progressive comorbidities requiring intensive management. Disorders such as type-2 diabetes, cardiovascular disease, and non-alcoholic fatty liver disease escalate without effective intervention. Patients with severe metabolic complications increasingly seek procedural solutions when conservative approaches fail to achieve desired outcomes. Healthcare providers respond by integrating weight-loss interventions that also address metabolic risks, improving long-term patient outcomes. The combination of rising obesity prevalence, associated comorbidities, and clinical demand establishes a strategic context for adoption of surgical solutions for patients with advanced weight-related health challenges.

Technological Advancements in Device Design and Integration

Enhanced device design and integration improve procedural precision, reduces complications, and streamlines surgical workflows, addressing growing clinical demand driven by obesity. In the United States, more than 25% of adults in all states and territories were classified as having obesity in 2024. Instruments with smaller incisions, ergonomic controls, and digital imaging guidance improve tissue handling and visibility, shortening operating times and minimizing intraoperative trauma. Advanced materials and refined anatomical interfaces reduce device-related risks, supporting surgeon confidence. Integration with hospital systems allows standardized procedures, data tracking, and outcomes analysis, increasing adoption of minimally invasive interventions across clinical settings.

Integration of real-time monitoring, sensor feedback, and robotic assistance expands clinical capabilities while improving patient outcomes. Smart technologies enable tailoring of surgical parameters to individual anatomy, remote adjustment of implants, and post-operative adherence monitoring. Support from regulatory bodies and healthcare providers reflects improved recovery profiles and optimized resource use. Enhanced device functionality strengthens training pathways, reduces variability among surgical teams, and improves procedural reliability. These innovations align operational efficiency with clinical value, reinforcing investment and adoption of advanced surgical platforms across healthcare facilities.

High Procedural and Device Costs

Surgical weight loss interventions using adjustable gastric bands require significant financial investment, making affordability a major concern for patients and healthcare providers. The cost of the device itself involves advanced materials, precise engineering, and quality certifications to meet regulatory standards. Operating room expenses, anesthesia, and specialized surgical team fees further elevate the total procedural cost. In regions where insurance coverage is limited or reimbursement rates are low, patients often bear the majority of expenses, creating a barrier to adoption. Economic disparities across different markets amplify this challenge, as price-sensitive populations may defer or avoid surgery despite clinical indications.

Training and infrastructure requirements contribute to overall financial burden, as surgeons must undergo specialized education and hospitals need equipped facilities for minimally invasive procedures. Long-term follow-up, band adjustments, and potential management of complications incur additional costs, increasing lifetime treatment expenditure. The complexity of supply chains for medical-grade devices, coupled with regulatory compliance and import duties in certain countries, drives pricing upward.

Regulatory Complexity and Approval Timelines

Approval processes for medical devices such as gastric bands involve multiple layers of regulatory scrutiny across regions. Manufacturers must meet strict safety, performance, and biocompatibility standards set by authorities such as the U.S. Food and Drug Administration (FDA) or the European Medicines Agency (EMA). These evaluations require extensive preclinical and clinical testing, detailed documentation, and post-market surveillance plans. The time-consuming nature of these procedures can delay product launch, limit market entry speed, and increase development costs. Differences in regulatory requirements across countries further complicate global commercialization, forcing manufacturers to customize submissions for each market.

Clinical trial design and patient recruitment contribute to extended timelines, as studies must demonstrate both efficacy and safety over prolonged periods. Any adverse events or insufficient data may trigger additional reviews or re-submissions, further slowing market introduction. Frequent updates to regulatory guidelines demand continuous compliance monitoring, which imposes resource and operational burdens on manufacturers. Smaller or emerging companies face heightened challenges due to limited regulatory expertise and financial capacity, restricting their ability to compete.

Integration of Digital Health Monitoring

Remote monitoring through digital health tools enables continuous tracking of patient weight, activity levels, and physiological parameters, allowing clinicians to assess progress and intervene when necessary. Personalized feedback delivered via mobile applications or connected devices encourages adherence to dietary and exercise plans. These platforms reduce the need for frequent in-person visits, improving convenience for patients and efficiency for healthcare providers. Early identification of deviations from expected recovery patterns allows timely adjustments to treatment plans, minimizing complications. Integration with clinical workflows supports structured post-surgery follow-up and ensures patients remain engaged throughout the recovery period.

Federal initiatives in the United States support the use of digital health solutions for chronic disease management and lifestyle interventions. Platforms for electronic health record interoperability allow secure sharing of remote monitoring data across care teams. Clinicians can make data-driven decisions, improving coordination and patient outcomes. Health systems are investing in telehealth infrastructure and remote patient monitoring programs to optimize care delivery. Remote engagement tools provide scalable solutions for managing patient populations, enhance communication between providers and patients, and promote long-term adherence to treatment plans, reinforcing structured care pathways and efficient resource utilization.

Development of Next-Generation Minimally Invasive and Smart Gastric Band Systems

Minimally invasive and smart iterations represent a key opportunity as procedural risk and patient recovery significantly influence clinical adoption. Innovations in device design that enable smaller incisions, enhanced precision, robotics, or real-time feedback systems reduce tissue damage, shorten hospital stays, and lower postoperative complication rates. These improvements align with broader healthcare objectives to improve safety profiles and patient satisfaction in bariatric care, increasing clinician confidence in recommending surgical options over long-term medical management alone.

Emerging systems incorporating smart technologies such as sensor feedback, adjustable components with remote monitoring, and integration with health applications support personalized post-surgical care and long-term compliance. This technological evolution broadens the patient pool to include individuals previously deterred by fear of invasive procedures or prolonged recovery. For healthcare providers and payors, investments in next-generation platforms improve procedural efficiency, reduce length of stay, and distribute care across outpatient settings, driving throughput and cost efficiency. As treatment paradigms shift toward value-based care and patient engagement, innovative, less invasive solutions deliver both clinical and operational performance advantages that can accelerate adoption amid rising chronic disease burdens.

Category-wise Analysis

Product Type Insights

Adjustable gastric bands are likely to be the leading segment with 68% revenue share in 2026, due to superior clinical efficacy and flexibility in weight management. Providers prefer adjustable bands because they allow incremental tightening or loosening based on patient response, improving adherence and safety outcomes. Hospital and clinic protocols favor minimally invasive adjustable devices to reduce complications and length of hospital stay. Material innovation and ergonomic design increase patient comfort and provider preference, enabling repeated adjustments without invasive procedures. Digital-enabled adjustability supports data-driven monitoring, aligning with healthcare quality standards.

Non-adjustable gastric bands are expected to witness the fastest growth between 2026 and 2033, as cost-effective implementation and simplified surgical workflow appeal to budget-constrained facilities. Smaller hospitals and emerging markets adopt non-adjustable bands to address growing obesity incidence without extensive capital expenditure. Clinical protocols benefit from predictable outcomes and reduced follow-up complexity. Innovations in biocompatible materials and modular design improve long-term safety, increasing provider confidence. Digital documentation and training modules support procedural standardization.

End-User Insights

Hospitals and surgical centers are anticipated to command nearly 60% of the gastric bands market revenue share in 2026, supported by high procedural volume, infrastructure readiness, and multi-specialty integration. Hospitals consolidate bariatric services within dedicated units, ensuring procedural standardization, post-operative care, and patient follow-up. Clinical credibility, referral networks, and advanced facilities encourage patient preference. Adoption of advanced adjustable devices is concentrated in these centers, reinforcing revenue dominance.

Ambulatory surgical centers are expected to emerge as the fastest-growing segment between 2026 and 2033, driven by low operational cost, patient convenience, and rising outpatient procedure adoption. ASCs leverage minimally invasive techniques to provide high-throughput, cost-efficient services. Digital patient tracking, tele-consultation, and streamlined administrative processes facilitate growth. Expansion in suburban and urban regions provides access to untapped patient bases, increasing adoption and supporting rapid market penetration.

Regional Insights

North America Gastric Bands Market Trends

North America is expected to lead with an estimated 40% of the gastric bands market share in 2026, supported by high procedural adoption, established hospital networks, and robust reimbursement frameworks. Well-capitalized healthcare institutions enable widespread use of adjustable gastric band systems, offering minimally invasive interventions with predictable outcomes. Clinical training programs enhance provider competence, increasing procedural confidence. Integration with electronic health records (EHRs) and digital monitoring allows continuous tracking of patient progress. Insurer coverage and policy support improve procedure accessibility. Investment in advanced operating theaters and post-operative care facilities reduces complication risk, sustaining high procedural volumes and solidifying market leadership.

Additional drivers include regulatory clarity, strong R&D presence, and technological integration. Clear pre-market approval pathways reduce commercialization uncertainty and enable faster introduction of device innovations. Manufacturers leverage clinical research centers for ergonomic band designs, telemetric adjustment systems, and biocompatible materials, improving patient adherence and safety. Digital connectivity with remote monitoring strengthens provider confidence in outcomes. High-income populations and growing awareness of obesity-related risks increase demand for minimally invasive interventions. Combined, these factors support procedural volume growth, premium device adoption, and stable expansion, reinforcing leadership and long-term investment potential in the market.

Europe Gastric Bands Market Trends

Europe presents mature adoption with well-established bariatric programs in Germany, France, and the United Kingdom. Adjustable gastric bands are widely implemented in hospitals and specialty centers to manage obesity and related comorbidities. Rising clinical awareness of long-term safety and effectiveness supports adoption, while national health coverage and insurance schemes improve patient access. Hospitals increasingly integrate smart adjustable systems that allow real-time monitoring and personalized therapy, enhancing patient outcomes and procedural efficiency. Regulatory alignment with international standards accelerates device approval and ensures consistent operational protocols. Training programs for surgeons and multidisciplinary support teams strengthen procedural quality, while improved outpatient capacity enables higher procedural throughput without compromising recovery or safety.

Competition involves both multinational manufacturers and regional distributors, with collaboration focused on device availability, clinical support, and technology transfer. Non-adjustable gastric bands maintain relevance in smaller clinics and emerging practices due to lower cost and simplified maintenance. Private healthcare networks adopt advanced adjustable systems to attract patients seeking personalized bariatric care, while investment in smart device integration and telemonitoring facilitates long-term follow-up and adherence. Hospitals leverage digital tracking to optimize therapy and reduce post-operative complications. Strong clinical validation and standardized protocols support adoption and innovation, positioning Europe for stable growth in the gastric bands sector during the forecast period.

Asia Pacific Gastric Bands Market Trends

Asia Pacific is forecasted to be the fastest-growing market for gastric bands between 2026 and 2033, stimulated by rising urban obesity, expanding healthcare infrastructure, and growing adoption of minimally invasive procedures. China exhibits a rapidly increasing patient base due to urban lifestyle changes, driving demand for bariatric interventions. India shows heightened hospital investment and government-backed obesity management programs, improving access and procedural readiness. Japan demonstrates advanced clinical adoption and structured post-operative monitoring, enhancing outcomes. South Korea integrates digital health platforms with surgical care, increasing patient adherence. Combined investments in hospitals and specialty centers, along with rising awareness of obesity risks, support scalable market expansion.

Regulatory facilitation, strategic partnerships, and technology-enabled monitoring further accelerate growth. Emerging frameworks streamline approval processes for innovative gastric band systems, reducing market entry delays. Collaborations between manufacturers and local hospitals enhance training, distribution, and service delivery, accelerating adoption. Telemetric adjustment features and digital adherence platforms enable continuous patient monitoring and provider confidence. Investment in minimally invasive surgical equipment and post-operative protocols improves recovery efficiency and procedural throughput.

Competitive Landscape

The global gastric bands market exhibits a moderately consolidated structure, with leading players collectively accounting for approximately 60% of revenue in 2026. Medtronic, Johnson & Johnson Medical Devices, Apollo Endosurgery, Allergan, and Bariatric Innovations dominate through broad product portfolios, technological innovation, and strong clinical validation. Competition centers on device efficacy, safety profiles, and provider adoption. Established manufacturers invest in adjustable and smart systems with telemetric adjustment and digital monitoring features. Geographic reach and regulatory compliance enable access to diverse patient populations and faster market entry.

Smaller regional suppliers and emerging innovators target niche segments, including non-adjustable bands and cost-efficient solutions for resource-limited settings. Strategic collaborations with hospitals and surgical centers improve credibility and procedural uptake. Fragmented segments encourage differentiation through ergonomic design, device customization, and integration with minimally invasive protocols. Focused offerings allow incremental revenue growth while fostering innovation.

Key Industry Developments

- In October 2025, One Ashford Hospital launched a new comprehensive bariatric surgery and weight management service across Kent and the Southeast to address rising obesity rates and expand access to multidisciplinary obesity care.

- In July 2025, St. Luke’s Medical Center Quezon City reopened its enhanced Weight Management Center offering multidisciplinary medical, surgical, and personalized weight-loss services to address rising obesity and support sustainable health outcomes.

- In June 2025, a study presented by researchers from NYU Langone Health and NYC Health + Hospitals at the American Society for Metabolic and Bariatric Surgery (ASMBS) 2025 meeting showed bariatric surgery delivers about five times greater weight loss than glucagon-like peptide-1 (GLP-1) drugs over two years.

Companies Covered in Gastric Bands Market

- Medtronic

- Johnson & Johnson Medical Devices

- Apollo Endosurgery

- Allergan

- Bariatric Innovations

- SlimBand Technologies

- ObTech GmbH

- Olympus Corporation

- Cook Medical

- MedAsia Healthcare

- Zimmer Biomet

- EndoMed Solutions

- Enteromed

Frequently Asked Questions

The global gastric bands market is projected to reach US$ 1.3 billion in 2026.

Rising obesity prevalence, increasing clinical awareness, and adoption of minimally invasive and smart adjustable devices are driving the market.

The market is poised to witness a CAGR of 4.7% from 2026 to 2033.

Expansion of minimally invasive procedures and integration of smart, connected gastric band systems present key market opportunities.

Some of the key market players include Medtronic, Johnson & Johnson Medical Devices, Apollo Endosurgery, Allergan, and Bariatric Innovations.