- Medical Devices

- Cryoablation Devices Market

Cryoablation Devices Market Size, Share, and Growth Forecast, 2026 - 2033

Cryoablation Devices Market by Product Type (Tissue Contact Probe Ablators, Others), Application (Lung Cancer, Liver Cancer, Breast Cancer, Kidney Cancer, Prostate Cancer, Cardiac Arrhythmia), End-User (Hospital, Research & Manufacturing, Outpatient Facilities), and Regional Analysis for 2026 - 2033

Cryoablation Devices Market Share and Trends Analysis

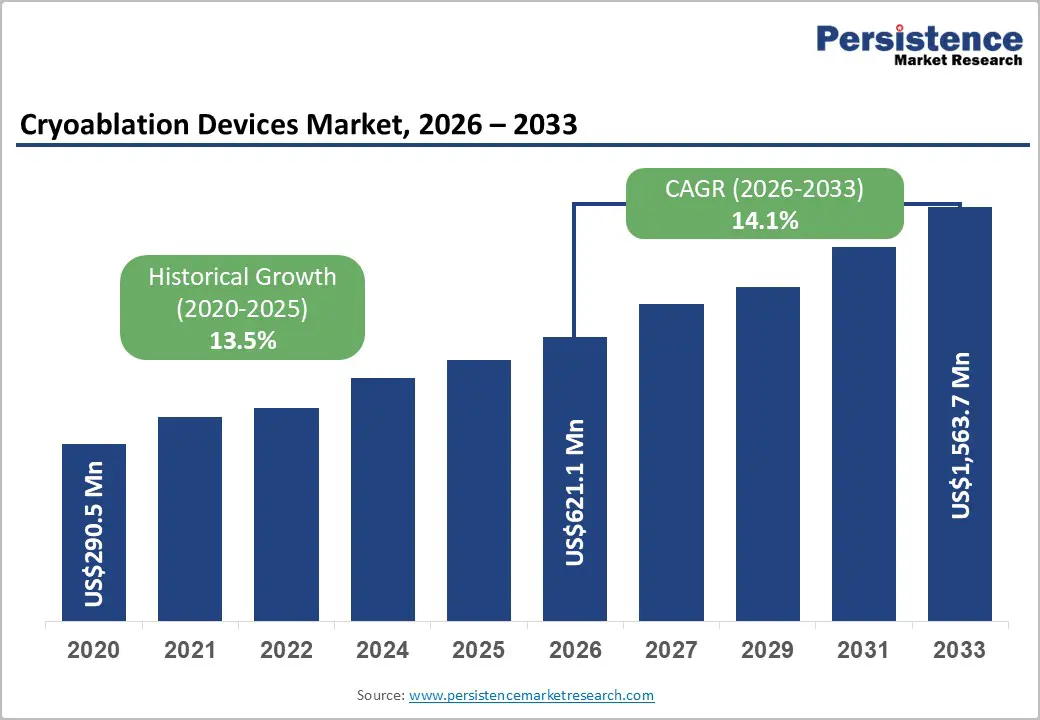

The global cryoablation devices market size is likely to be valued at US$621.1 million in 2026 and is estimated to reach US$1563.7 million by 2033, growing at a CAGR of 14.1% during the forecast period 2026 - 2033, driven by increasing clinical adoption of minimally invasive oncology and cardiology procedures, where targeted tissue destruction reduces procedural risk and recovery time.

Drivers include rising cancer and cardiac arrhythmia prevalence, growth in image-guided ablation using computed tomography and magnetic resonance imaging, and a shift toward outpatient day-care procedures. Integration into oncology pathways and regulatory support continues adoption.

Key Industry Highlights:

- Leading Product Type: Tissue contact probe ablators are expected to command around 48% of revenue in 2026 due to precise tissue targeting and strong compatibility with image-guided procedures.

- Fastest-growing Product Type: Tissue spray probe ablators are likely to be the fastest-growing segment due to expanding use in complex lesion treatments.

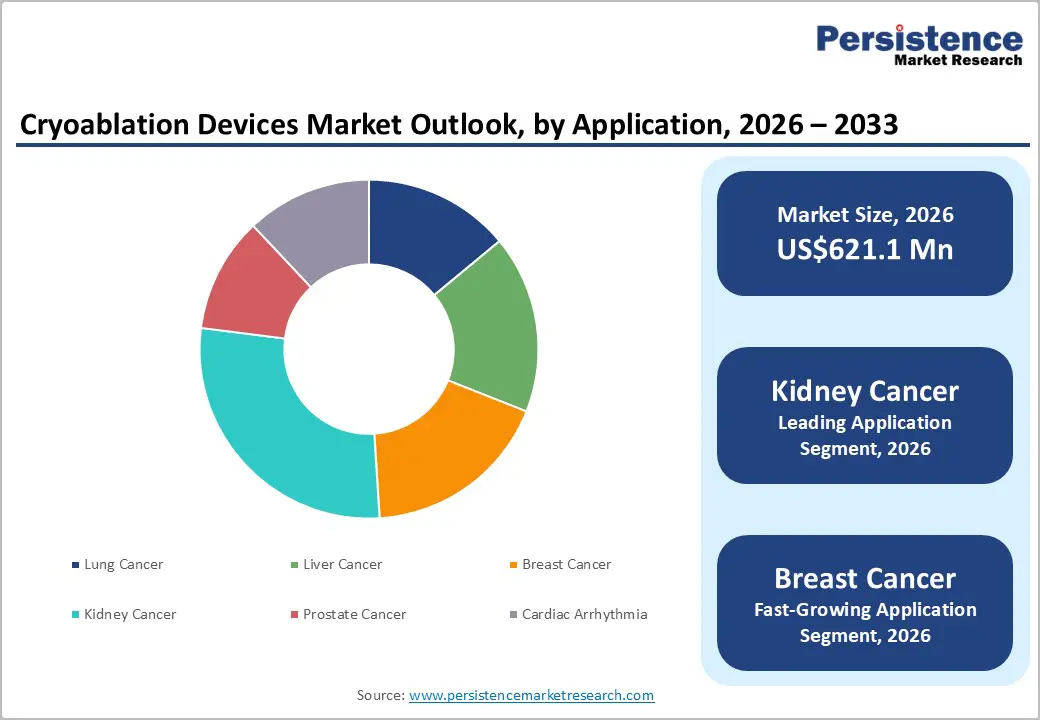

- Leading Application: Kidney cancer is anticipated to secure around 28% revenue share in 2026, fueled by strong adoption in nephron-sparing treatment approaches.

- Fastest-growing Application: Breast cancer is expected to be the fastest-growing segment, driven by increasing preference for minimally invasive tumor management.

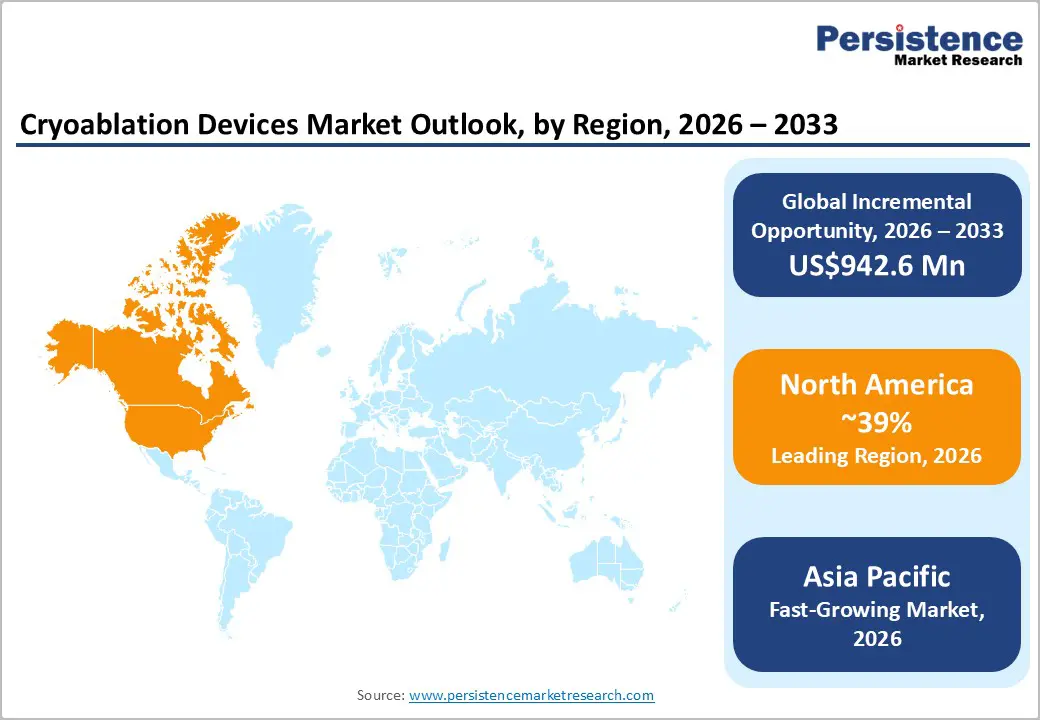

- Regional Leadership: North America is expected to lead with an estimated 39% market share in 2026, while Asia Pacific is forecast to be the fastest-growing regional market, driven by healthcare expansion and increasing oncology treatment demand.

- Competitive Environment: Moderately consolidated structure due to the strong presence of global medical device manufacturers and increasing strategic collaborations with healthcare institutions.

- Innovation Trends: Shift toward imaging-integrated systems due to demand for precision-guided procedures and development of portable cryo platforms.

DRO Analysis

Driver - Increasing Burden of Oncological and Cardiac Conditions

Rising patient volumes in oncology and cardiology are climbing steadily to propel the cryoablation devices market. The National Cancer Institute reports 2,041,910 projected new cancer cases for 2025. Cardiac conditions compound pressure on healthcare systems. Cryoablation devices fulfill the need through targeted tissue ablation. Providers secure operational gains via shorter recovery periods. Demand expands due to the preference for outpatient-compatible solutions.

Physicians favor cryoablation for its tissue preservation qualities in delicate cardiac structures. Tumor ablation procedures benefit from real-time imaging compatibility. Systems deliver lower overall costs through reduced follow-up care. Adoption rates rise steadily in specialized centers nationwide. Structural reimbursement shifts further encourage integration into standard protocols. Efficiency gains position the technology as the preferred choice amid rising volume surges.

Restraint - Limited Specialized Training Availability Impedes Procedural Scalability

Specialized training scarcity restricts cryoablation procedural rollout. Cryoablation requires advanced catheter navigation and real-time imaging skills. Few fellowship programs train electro physiologists and oncologists adequately. In 2025, the American Board of Internal Medicine (ABIM) data showed only 4,034 certified clinical cardiac electro physiologists nationwide. High-volume centers monopolize expertise. New facilities struggle to launch services. Operational delays hinder geographic expansion. Demand growth stalls without distributed proficiency. Providers face prolonged waitlists. Economic barriers limit patient access in underserved regions.

Training deficits elevate costs and inconsistency risks. Inexperienced operators increase complication rates and erode confidence. Hospitals postpone device purchases until staff certification is complete. Rural networks encounter severe shortages. Procedure variability undermines reimbursement standardization. Scalability suffers from prolonged ramp-up periods. Investment returns diminish amid operator constraints. Broader adoption demands expanded curricula and simulation programs. Workforce limitations cap volume potential across networks.

Opportunity - Integration with Advanced Imaging and Robotic Platforms

Advanced imaging and robotic integration elevate cryoablation precision substantially. Magnetic Resonance Imaging (MRI) and Computed Tomography (CT) fusion visualizes ice-ball margins accurately. Robotic arms ensure tremor-free catheter delivery. Operators deliver consistent results across varying expertise levels. Procedure durations shorten, lifting throughput capacity. Hospitals secure elevated reimbursements for technology-driven care. Demand intensifies for complex oncological and cardiac interventions.

Synergies amplify operational leverage and penetration. Artificial Intelligence (AI) navigation anticipates ablation boundaries dynamically. Robotic systems normalize techniques, offsetting training constraints. Outpatient volumes climb with streamlined workflows. Unit economics improve via scale efficiencies. Providers differentiate on superior outcomes and safety metrics. Patient inflows expand through minimized complications. Collaborations hasten ecosystem maturity. Adoption gains traction in advanced facilities.

Category-wise Analysis

Product Type Insights

Tissue contact probe ablators are anticipated to secure around 48% of the cryoablation devices market share in 2026, reflecting deep-tissue access requirements across solid-organ applications. Clinical preference is supported by predictable ice-ball formation, with studies showing ice-ball diameters reaching 4 cm and enabling consistent ablation margins. Direct probe contact ensures uniform necrosis zones, while compatibility with CT and MRI guidance improves workflow efficiency and procedural accuracy. Modular probe configurations and advancements in thermal conductivity materials support treatment flexibility and durability across varied lesion profiles.

Epidermal and subcutaneous cryoablation systems are expected to be the fastest-growing segment, propelled by expansion into superficial and breast indications, where regulatory authorizations enable broader utilization. Clinical acceptance accelerates as minimally invasive profiles suit skin cancer and keloid treatments with reduced scarring. Surface energy delivery limits depth in melanoma and actinic keratosis cases, sparing muscle. Providers favor office integration for dermatofibroma ablation. Patient-friendly probes cut discomfort in lipoma removal. Miniaturized applicators target basal cell lesions precisely.

Application Insights

Kidney cancer is likely to be the leading segment with a projected 28% of the cryoablation devices market share in 2026, due to established protocols that preserve renal function while achieving local control in small masses. Clinical data indicate local control rates above 90% for tumors under 4 cm, supporting nephron-sparing goals. Percutaneous access with CT guidance improves precision, reduces hospital stay, and lowers the need for repeat interventions.

Breast cancer is anticipated to be the fastest-growing segment, fueled by recent regulatory authorizations that validate use in select low-risk cohorts and open pathways for non-surgical candidates. Clinical studies report complete tumor ablation rates above 90% in early-stage cases, supporting adoption. Outpatient procedures reduce hospital stay, while improved cosmetic outcomes and faster recovery increase patient preference and provider referrals across breast care centers.

End-user Insights

Hospitals are anticipated to secure around 62% of the cryoablation devices market share in 2026, powered by a comprehensive infrastructure that supports multidisciplinary coordination and advanced imaging integration. Provider infrastructure enables integration with interventional suites, improving scheduling and resource use. Clinical acceptance is supported by established credentialing and high-volume expertise. Dedicated procedural units enhance access, while hybrid operating environments support evolving device platforms and precision-driven workflows.

Outpatient facilities are estimated to be the fastest-growing segment from 2026 to 2033, fueled by the migration of lower-acuity cases toward ambulatory environments that reduce overhead and improve patient throughput. Provider preference aligns with cost-efficiency and same-day discharge models. Compact system designs enable easy clinic integration. Reduced travel and recovery time improve adherence, while portable consoles support decentralized and scalable treatment delivery.

Regional Insights

North America Cryoablation Devices Market Trends

North America leads with an estimated 39% of the cryoablation devices market share in 2026, supported by Medtronic and Boston Scientific innovations in catheter precision. Dense interventional cardiology networks in the United States concentrate expertise for atrial fibrillation treatments. Mayo Clinic protocols standardize renal mass ablations, driving procedural volumes. Favorable Centers for Medicare & Medicaid Services reimbursements accelerate adoption in outpatient centers. Incidence of localized prostate cancers spurs urology demand. Population aging swells cardiac cryoablation caseloads across integrated delivery networks.

Advanced infrastructure elevates dominance through real-time imaging integration at Cleveland Clinic facilities. Canada's regulatory pathways expedite Health Canada approvals for breast cancer indications. Venture capital fuels startups such as Adagio Medical in Silicon Valley hubs. Physician training fellowships at Johns Hopkins expand operator pools. Value-based care models reward low-complication outcomes in ambulatory surgery centers. Competitive device pricing from domestic manufacturers intensifies hospital procurement cycles. Patient preference for minimally invasive options boosts referral patterns nationwide.

Europe Cryoablation Devices Market Trends

Europe secures robust procedural uptake through clinical leadership at Karolinska Institute in Sweden. Medtronic PolarSens systems dominate atrial fibrillation ablations in German electrophysiology labs. The U.K. National Institute for Health and Care Excellence guidelines endorse renal cryoablation for small masses. France Haute Autorité de Santé reimbursement schedules prioritize outpatient breast cancer protocols. Italy European Institute of Oncology networks integrate real-time Magnetic Resonance Imaging (MRI) guidance for liver tumors. Physician societies unify training standards across member states.

Infrastructure sophistication propels consistent expansion via specialized ablation facilities. Netherlands Leiden University Medical Center advances prostate applications with durable local control. Spain's national cancer strategy outfits tertiary centers with advanced consoles. European Society of Cardiology registries monitor long-term efficacy data. Siemens Healthiness competitive tenders enforce pricing efficiency. Patient advocacy coalitions champion nephron-sparing alternatives in multidisciplinary tumor boards. Venture investments back innovators such as CryoShape in Zurich medical corridors.

Asia Pacific Cryoablation Devices Market Trends

Asia Pacific is forecast to be the fastest-growing market for cryoablation devices between 2026 and 2033, stimulated by surging procedural adoption in high-density urban centers. China's regulatory reforms at the National Medical Products Administration expedite device clearances for liver cancer protocols. Indian private hospital chains such as Apollo Hospitals scale outpatient cryoablation for renal masses. Japan's national health insurance revisions boost cardiac arrhythmia treatments at Tokyo Medical University Hospital. South Korea's advanced manufacturing by Samsung Medison integrates ultrasound-guided probes. Incidence of hepatocellular carcinoma drives urology demand nationwide.

Infrastructure investments propel volume acceleration through dedicated electrophysiology suites. Singapore clinical trials at National University Hospital validate breast cancer applications, spurring referrals. Thailand's medical tourism hubs in Bangkok prioritize minimally invasive options for international patients. Vietnam government tends to favor cost-effective systems from Terumo Corporation affiliates. Australia Medicare enhancements reward nephron-sparing kidney procedures at the Royal Melbourne Hospital. Competitive pricing pressures elevate procurement cycles across integrated networks. Patient volumes climb with localized training programs at Asian Heart Institute.

Competitive Landscape

The global cryoablation devices market is moderately consolidated, characterized by strong participation from global medical device manufacturers and specialized interventional technology firms. Leading players such as Medtronic, Boston Scientific, and Terumo Corporation maintain influence through regulatory approvals, clinical validation, and established hospital partnerships. Competitive positioning is driven by continuous innovation in probe design, integration with imaging systems, and improvements in procedural efficiency across oncology and cardiology applications.

Mid-tier and niche-focused companies, including Galil Medical, CooperSurgical, and IceCure Medical, concentrate on targeted clinical applications and regional market expansion. These firms emphasize product differentiation, cost optimization, and flexible system configurations to address specific treatment needs. The market structure reflects a balanced mix of large multinational corporations and specialized innovators, supporting technological advancement and broader adoption across diverse healthcare settings.

Key Industry Developments

- In November 2025, IceCure Medical received regulatory approval in Switzerland for its ProSense cryoablation system covering breast, lung, liver, and kidney cancer indications, expanding multi-organ clinical use and accelerating commercial access across European oncology treatment settings.

- In September 2025, AtriCure announced the launch of its cryoXT cryoablation device, designed for post-operative pain management following amputation, with FDA 510(k) clearance supporting clinical adoption and expanding application of cryoablation technologies in nerve-targeted therapies.

Companies Covered in Cryoablation Devices Market

- Medtronic

- Boston Scientific

- Galil Medical

- Terumo Corporation

- CooperSurgical

- IceCure Medical

- HealthTronics

- Varian Medical Systems

- Siemens Healthineers

- Philips Healthcare

- AngioDynamics

- Merit Medical Systems

- BTG International

- Johnson & Johnson MedTech

Frequently Asked Questions

The global cryoablation devices market is projected to reach US$621.1 million in 2026.

Rising demand for minimally invasive procedures, supported by increasing cancer and cardiac arrhythmia cases and growing adoption of image-guided precision therapies, drives the cryoablation devices market.

The cryoablation devices market is poised to witness a CAGR of 14.1% from 2026 to 2033.

Expansion of image-guided interventions, outpatient treatment models, and adoption across emerging healthcare systems creates key growth opportunities in the cryoablation devices market.

Some of the key market players include Medtronic, Boston Scientific, Galil Medical, Terumo Corporation, CooperSurgical, and IceCure Medical.