- Automotive

- EV Charging Cables Market

EV Charging Cables Market Size, Share, and Growth Forecast, 2026- 2033

EV Charging Cables Market by Power Type (AC charging, and DC charging), By Charging Level (Level 1, Level 2, and Level 3), By Application (Private charging, and Public charging), By Cable Length (2–5 meters, 6–10 meters, and >10 meters ), and Regional Analysis for 2026 – 2033

EV Charging Cables Market Size and Trends Analysis

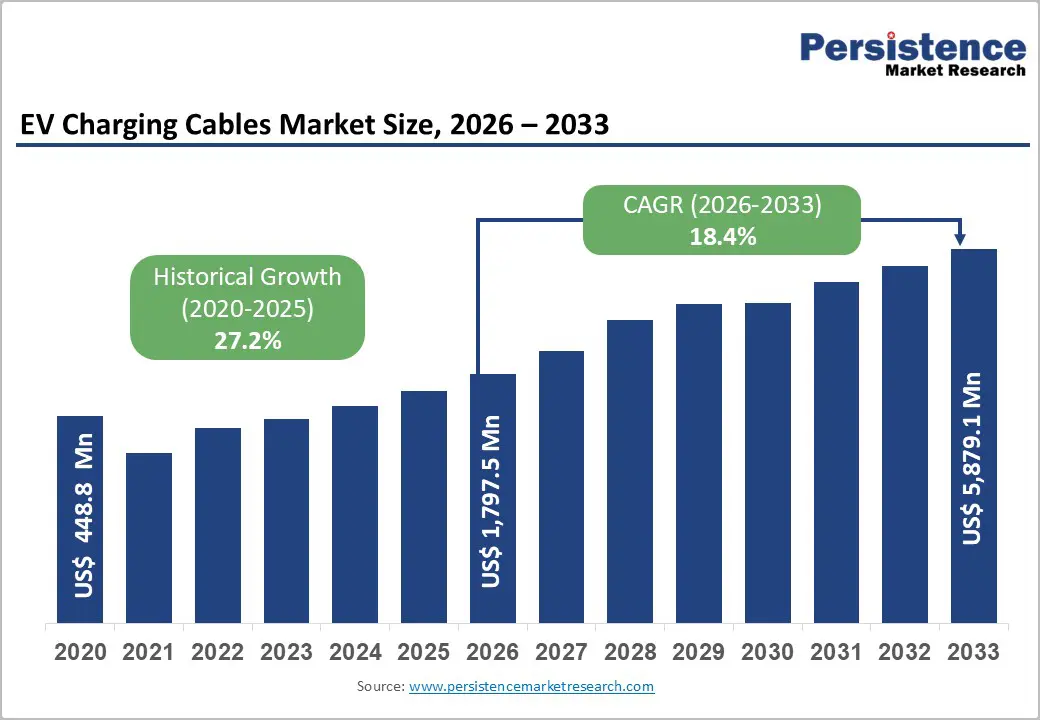

The global EV charging cables market was valued at US$ 448.8 Million in 2020 and reached US$ 1,797.5 Million in 2026, with projections to expand to US$ 5,879.1 Million by 2033, representing a CAGR of 18.4% between 2026 and 2033.

This robust growth trajectory is driven by accelerating electric vehicle adoption, expansion of charging infrastructure across developed and emerging markets, supportive governmental policies promoting zero-emission vehicles, and technological advancements enabling faster and more efficient charging solutions. The market's expansion reflects the critical role of charging cables as essential infrastructure components supporting the global EV transition, with demand patterns increasingly influenced by regional regulatory frameworks and evolving battery technologies.

Key Industry Highlights:

- DC Charging Segment Leadership in Growth: While AC charging dominates at 65%+ market share, DC fast-charging cables expand at 19.4% CAGR, with Level 3 (DC) charging expanding at 19.6% CAGR, reflecting strategic infrastructure operator focus on fast-charging network deployment and consumer preference for reduced charging times, driving premium-priced specialized cable demand.

- Public Charging Infrastructure Momentum: Public charging applications grow at a 19.5% CAGR, significantly exceeding private charging growth, driven by government charging station installation mandates and infrastructure operator capital investment programs that systematize public fast-charging network expansion globally through 2033.

- Asia-Pacific Regional Dominance: Asia-Pacific commands 45%+ market share with concentrated growth in China (50%+ of global demand), emerging markets (India, ASEAN) at 25%+ CAGR, establishing the region as the primary market driver and production center for global cable supply chains through 2033.

- Extended-Length Cable Growth: 6-10 meter and >10 meter cable segments expand at 19.1% CAGR and 20%+ CAGR, respectively, driven by high-density urban parking requirements, commercial fleet charging specialization, and specialized applications supporting premium-margin differentiated products.

- Strategic Development Concentration: Technology partnerships (Siemens-Ionity, Eaton-EVgo) advancing V2G integration, Chinese manufacturer capacity expansion (US$ 2.5+ billion investments), and NACS standardization completion establish market momentum toward integrated fast-charging ecosystem solutions with enhanced profitability potential through 2033.

| Key Insights | Details |

|---|---|

| EV Charging Cables Market Size (2026E) | US$1,797.5 Mn |

| Market Value Forecast (2033F) | US$5,879.1 Mn |

| Projected Growth (CAGR 2026 to 2033) | 18.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 27.2% |

Market Dynamics

Key Growth Drivers

Government Policy Support and EV Infrastructure Mandates

Regulatory frameworks are mandating the development of charging infrastructure as a prerequisite for EV market expansion. The European Union's Alternative Fuels Infrastructure Directive requires member states to install charging stations at regular intervals on major highways, establishing standardized charging protocols and cable specifications. The United States allocated US$ 7.5 billion under the Inflation Reduction Act for EV charging infrastructure deployment, requiring compliance with specific cable standards and safety certifications. China's government mandates that all new residential constructions include EV charging preparation, creating systematic demand for charging cable installation. These regulatory frameworks establish minimum infrastructure requirements that directly translate into cable procurement specifications and volume requirements. Governments are also implementing vehicle-to-grid (V2G) regulations that require specialized charging cables capable of bidirectional power flow. Such policy-driven infrastructure investments create predictable, multi-year demand cycles that support sustained cable manufacturer revenue streams and justify capital investment in production capacity expansion.

Market Restraining Factors

Infrastructure Development Costs and Investment Barriers

Establishing comprehensive EV charging networks requires substantial capital investment, creating barriers to rapid infrastructure deployment in developing economies. A single fast-charging station installation costs between US$150,000 and US$300,000, including grid upgrades, land acquisition, and regulatory compliance. Scaling this to achieve the International Energy Agency's target of 14 million public charging points by 2030 (from the current 2.7 million) would require estimated investments exceeding US$2 trillion globally. In emerging markets with limited government funding and underdeveloped financial institutions, this investment barrier significantly constrains infrastructure expansion. Grid capacity limitations in many regions necessitate expensive infrastructure upgrades before charging stations can operate effectively, creating cascading cost increases. These capital constraints limit the pace of charging network deployment, directly impacting the timelines for cable demand growth. Developing economies in Sub-Saharan Africa, parts of Southeast Asia, and South America are experiencing slower infrastructure deployment due to investment barriers, creating geographic disparities in market growth rates.

EV Charging Cables Market Trends and Opportunities

Commercial Fleet Electrification and Heavy-Duty Vehicle Charging Infrastructure

Commercial vehicle electrification (buses, trucks, delivery vehicles) represents a distinct, rapidly growing market segment with unique charging requirements. Electric bus fleets are expanding globally, with over 1 million e-buses already deployed (concentrated in China), creating demand for charging cables optimized for high-frequency depot charging. Heavy-duty truck electrification is accelerating, with manufacturers such as Volvo, Daimler, and BYD releasing commercial EV models that require specialized charging infrastructure. Charging cables for commercial applications must accommodate higher power specifications (150-350 kW) and more frequent charging cycles, increasing per-unit specifications and cable complexity. Fleet operators prioritize reducing the total cost of ownership, driving demand for durable, reliable charging cables. This commercial vehicle segment is projected to expand at a 20-22% CAGR through 2033, outpacing overall market growth due to concentrated fleet procurement and government logistics electrification mandates.

EV Charging Cables Market Insights and Trends

Product Type Insights

AC Dominance Meets Rapid DC Growth in EV Charging Cable Market

The EV charging cable market is defined by a clear contrast between the dominance of volume-driven AC charging and the rapid expansion of high-performance DC charging solutions. AC charging remains the leading power type, accounting for over 65% of total market revenue. Its leadership is supported by a mature global infrastructure, standardized connectors such as Type 1 and Type 2, and lower cable complexity, which significantly reduces manufacturing costs. AC charging cables are widely used in residential and workplace installations, forming the largest installed base of charging points worldwide. Their affordability, ease of use, and well-established supply chains across Asia, Europe, and North America make AC charging central to mass-market EV adoption. Despite rising competition, AC charging is expected to retain over 60% market share through 2033, supported by stable, high-volume demand.

In contrast, DC charging represents the fastest-growing segment, expanding at a 19.4% CAGR. DC fast-charging enables charging times of 20–30 minutes, making it essential for highway corridors and commercial fleets. Higher power ratings, advanced thermal management, and premium materials increase manufacturing costs but support stronger margins. Growing government mandates and premium EV adoption continue to accelerate the deployment of DC charging cables globally.

Charging Level Insights

EV Charging Levels Market Shifts Toward Faster Infrastructure Adoption

The global EV charging cable market is shaped by distinct growth dynamics across Level 1, Level 2, and Level 3 charging systems. Level 1 charging continues to hold market leadership, accounting for over 40% of revenue, supported by the widespread adoption of residential EV charging in developed markets. Its low cost, universal compatibility, and massive installed base of more than 120 million units worldwide ensure steady replacement-driven demand. However, this segment is increasingly commoditized, with growth moderating as consumers seek faster charging solutions and policymakers prioritize advanced infrastructure.

In contrast, Level 3 (DC fast charging) represents the fastest-growing segment, expanding at nearly 19.6% CAGR through 2033. High charging speeds, premium pricing, and strong government backing for highway corridor electrification are accelerating deployment. Network operators such as Electrify America, EVgo, Ionity, and NIO Power are reinforcing a virtuous cycle between fast-charging availability and EV adoption, positioning Level 3 as critical to mass-market electrification.

Level 2 charging occupies a balanced middle ground, growing at 16–17% CAGR. Its moderate installation costs and suitability for workplaces and multi-unit residences support scalable growth, though intense competition is driving margin pressure.

Application Insights

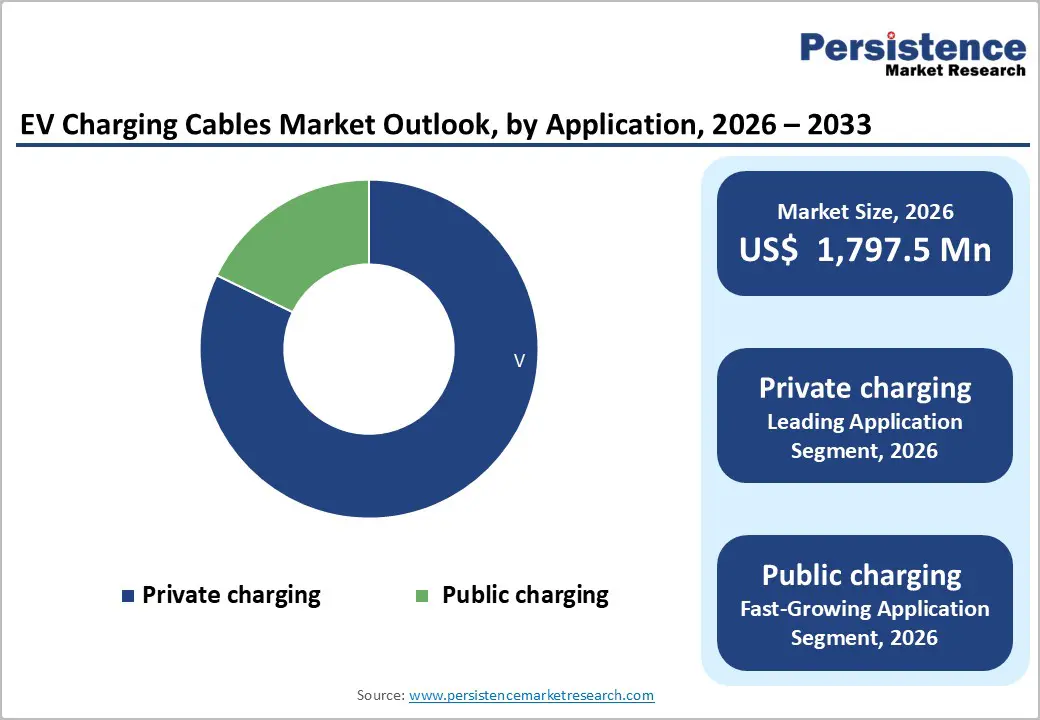

Private Dominance and Rapid Public Charging Infrastructure Expansion Reshape EV Cable Market

Private charging remains the dominant application segment in the EV charging cable market, accounting for over 70% of total revenue. This leadership reflects EV owners’ strong preference for residential and private workplace charging, driven by convenience, the ability to charge overnight, and reduced reliance on public infrastructure. With a global installed base exceeding 30 million private charging points and annual additions of 3–4 million units, the segment generates stable, recurring demand for replacement and upgraded cables due to wear, evolving standards, and vehicle compatibility needs. Private charging cables are typically high-volume products with lower technical complexity and well-established retail distribution channels. While growth in developed markets such as the U.S. and Western Europe is moderating as EV penetration approaches saturation levels of 8–12% of vehicles on the road, emerging markets across Asia-Pacific and parts of Eastern Europe continue to offer strong expansion potential. Manufacturers focusing on affordability, easy installation, and user-friendly design are best positioned here.

In contrast, public charging represents the fastest-growing application segment, expanding at a projected 19.5% CAGR through 2033. Growth is driven by government mandates, infrastructure investment programs, and increasing reliance on fast charging for long-distance travel. Public charging cables demand superior durability, weather resistance, and high-duty-cycle performance, and per-unit costs are significantly higher than those of private systems. Although deployment remains concentrated in China, Europe and North America are rapidly scaling networks, creating attractive high-margin and technology-led opportunities for cable manufacturers.

Cable Length Insights

Standard-Length Dominance with Rapid Growth in Extended EV Charging Cables

The EV charging cable market shows clear differentiation by cable length, reflecting varied use cases and infrastructure constraints. Standard 2–5 meter cables dominate with over 40% revenue share, supported by their broad suitability for residential charging, workplaces, and most public stations. These lengths align with typical parking layouts and vehicle-to-charger distances, while mature, automated manufacturing enables cost-efficient, high-volume production, keeping prices competitive. As residential EV adoption accelerates and parking designs remain standardized, this segment is expected to retain leadership through 2033, although its growth rate is moderating.

In contrast, 6–10 meter cables are the fastest-growing segment, expanding at a 19.1% CAGR. Their appeal lies in their ability to address complex parking configurations, such as multi-level structures, fleet depots, and urban residential setups where chargers are farther from vehicles. Higher material use and installation complexity support 25–35% price premiums, yet demand remains strong, particularly from commercial fleet operators and public transit authorities, driving infrastructure standardization around these lengths.

Ultra-extended cables (>10 meters) form a smaller, niche segment with less than 15% share, but exhibit over 20% CAGR. Growth is fueled by large facilities, underground parking, and heavy-duty vehicle charging, where customization commands 40–50% price premiums. Together, these trends indicate a gradual market shift toward longer, higher-value cable solutions.

Regional Insights and Trends

Asia-Pacific EV Charging Cable Market Driven by Manufacturing Scale Leadership

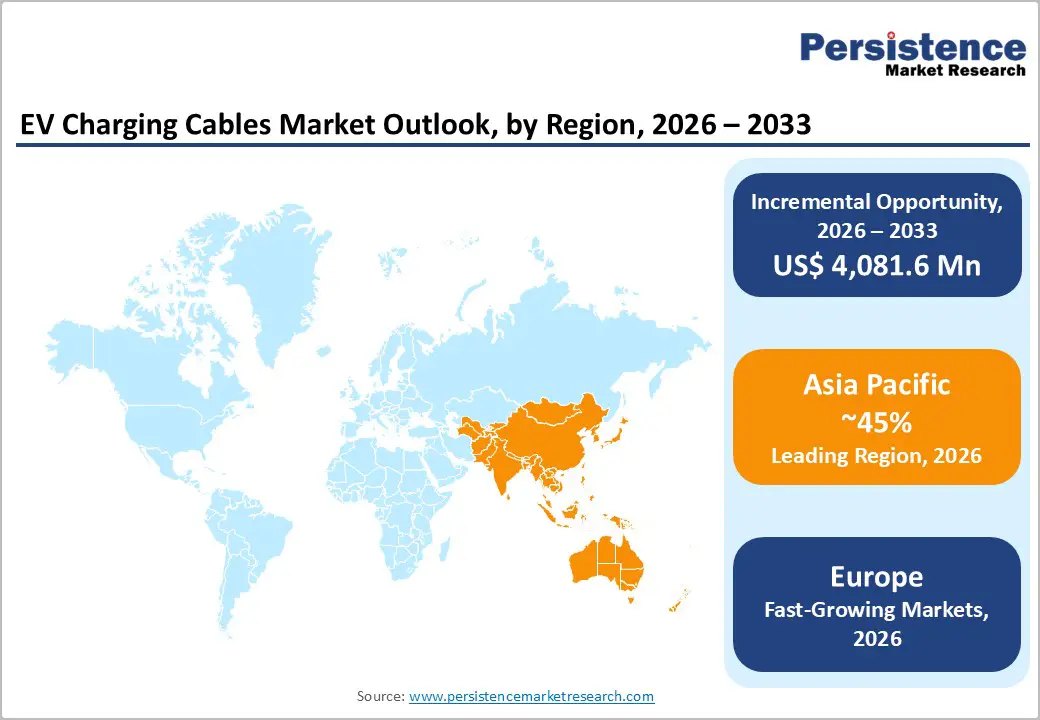

Asia-Pacific dominates the global market, accounting for over 45% of total revenue and maintaining leadership through 2033. This dominance is fundamentally anchored in China, which hosts more than 60% of global charging cable manufacturing capacity, supplies nearly 75% of core components, and contributes over half of global end-market demand. With EV sales reaching 9.5 million units in 2023, around 60% of global volumes, China’s charging infrastructure rollout directly translates into large-scale cable procurement. Strong policy backing through New Energy Vehicle incentives and mandated infrastructure investments, supported by state-backed entities such as China State Grid, ensures consistent, volume-driven demand.

Japan represents the region’s second-largest market, valued at approximately US$180–200 million annually. Its market is characterized by premium-quality, high-reliability charging cables, driven by early EV adoption and strong domestic OEM participation. Japanese suppliers leverage advanced manufacturing to lead innovation in fast-charging and high-specification cable technologies.

India and Southeast Asia are emerging as high-growth subregions. India’s rapid two-wheeler electrification and supportive subsidies are driving demand for charging cables at over a 25% CAGR. Meanwhile, ASEAN markets are accelerating electrification through government targets and investments by manufacturers such as BYD. Supported by low-cost manufacturing, strong electronics supply chains, and an estimated US$250–300 billion in regional investments in charging infrastructure through 2033, Asia-Pacific remains the global production and demand hub.

Europe EV Charging Cable Market Shaped by Regulation and Premiumization

Europe is the second-largest EV charging cable market, contributing approximately 25–28% of global revenue and growing at a robust 19.4% CAGR. Market expansion is strongly policy-driven, with Germany at the center of regional demand. Germany’s EV sales reached around 770,000 units in 2023, supported by a structured infrastructure rollout targeting one million public charging points by 2030. This systematic deployment ensures long-term, predictable cable procurement aligned with domestic EV production priorities.

France, the United Kingdom, and Spain form the next tier of demand, together accounting for a substantial share of European EV sales. Incentive programs such as France’s ADVENIR scheme and strong adoption in Nordic countries have pushed infrastructure density to advanced levels, shifting parts of the market toward replacement and upgrade demand rather than greenfield installations.

Europe’s regulatory framework under the EU Alternative Fuels Infrastructure Directive mandates CCS standardization, enabling unified supply chains while raising technical and safety requirements. This environment favors premium manufacturers offering certified, high-durability products, often priced 20–30% above Asian alternatives. Companies such as Mennekes and Leoni benefit from this premium positioning. Sustained investments by infrastructure players, including ABB and Siemens, combined with the EU Green Deal’s 2050 carbon-neutral target, underpin stable, long-term growth and technology-led differentiation through 2033.

EV Charging Cables Market Competitive Landscape

The global EV charging cable market demonstrates moderate consolidation characteristics, with the top 5 manufacturers commanding approximately 35-40% combined market share, while the remaining 60-65% is distributed among 50-75 competing manufacturers. This market structure reflects relatively low barriers to entry for standard cable manufacturing combined with specialized requirements for advanced fast-charging cables that support differentiation and margin advantages. Geographic specialization is pronounced: Chinese manufacturers control 60%+ of global production capacity, European manufacturers emphasize premium segments, and North American manufacturers focus on proprietary ecosystem products (particularly Tesla-related cables).

Leading market participants include Yazaki (Japan), Leoni (Germany), Lapp (Germany), TE Connectivity (U.S.), Amphenol (U.S.), Samtian Group (China), and Huayu Automotive Systems (China). These manufacturers benefit from established relationships with vehicle manufacturers and charging infrastructure operators, providing supply chain stability and volume demand. Specialized fast-charging cable manufacturers (Mennekes, Lapp Gruppe) command premium market positions through technology differentiation and comprehensive safety certifications. Chinese domestic manufacturers gain competitive advantages through cost structure benefits and vertical integration with EV and battery manufacturers.

Market concentration is gradually increasing as manufacturers invest in specialization (fast-charging, V2G, smart charging) and expand regional production capacity. Fragmentation remains in residential charging cable segments, where local manufacturers serve regional markets with low-cost products.

Key Industry Developments

- In December 2025, Polycab India Limited expanded its electric mobility portfolio by launching a new range of electric vehicle charging solutions and automotive power products at Auto EV Bharat India, held at the KTPO Convention Centre in Bengaluru. The launch reflects Polycab’s strategic entry into EV infrastructure and power electronics, targeting growing domestic demand for integrated charging and automotive electrical solutions across passenger and commercial EV segments.

- On July 9, 2024, JAE officially released its CHAdeMO standard-compliant KW03C Series EV charging and discharging connector. The UL-recognized and JCS-compliant product supports a rated voltage of DC 750V and a current of 80A, making it suitable for fast and medium-speed charging applications as well as vehicle-to-grid (V2G) systems, strengthening its position in advanced EV power transfer technologies.

- In June 2025, Lynkwell highlighted its flagship XLynk Level-2 charger, originally launched in Q3 2024. The next-generation XLynk delivers up to 80 amps (19.2 kW) and features physical dip switches for flexible configuration from 12 to 80 amps. The charger supports RFID, Tap-to-Pay, Guest Charging without app downloads, dynamic local load management, an EZ-Swap Faceplate for rapid customization, and a lifetime warranty, enhancing both user convenience and operational efficiency.

Companies Covered in EV Charging Cables Market

- Leoni AG

- Coroplast

- Chengdu Khons Technology Co., Ltd.

- Phoenix Contact

- Aptiv

- BESEN-Group

- General Cable Technologies Corporation

- Dyden Corporation

- TE Connectivity

- Other Market Players

Frequently Asked Questions

The EV Charging Cables market is estimated to be valued at US$ 1,797.5 Mn in 2026.

The primary demand driver for the EV charging cables market is the rapid growth of electric vehicle (EV) adoption, directly linked with the large-scale expansion of charging infrastructure.

In 2026, the Asia Pacific region will dominate the market with an exceeding 75% revenue share in the global EV Charging Cables market.

Among applications, private charging has the highest preference, capturing beyond 70% of the market revenue share in 2026, surpassing other applications

Leoni AG, Coroplast, Chengdu Khons Technology Co., Ltd., Phoenix Contact, Aptiv, BESEN-Group, and General Cable Technologies Corporation. There are a few leading players in the EV Charging Cables market