- Automotive

- Electric Vehicle Adhesives Market

Electric Vehicle Adhesives Market Size, Share, and Growth Forecast 2026 - 2033

Electric Vehicle Adhesives Market by Product Type (Structural Adhesives, Sealants & Gasketing, Thermal Management Materials), End-Use (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles), Resin Type (Epoxy, Polyurethane, Silicone, Acrylic), and Regional Analysis for 2026 - 2033

Electric Vehicle Adhesives Market Size and Trend Analysis

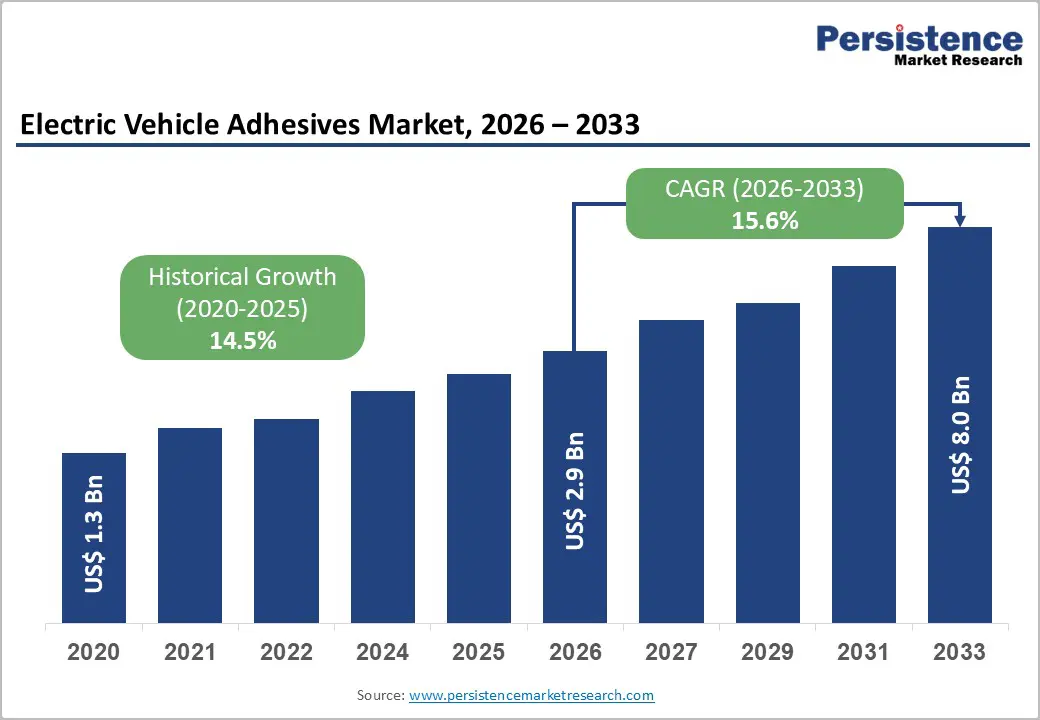

The global electric vehicle adhesives market is valued at US$ 2.9 Bn in 2026 and is projected to reach US$ 8.0 Bn by 2033, growing at a CAGR of 15.6% between 2026 and 2033.

This robust expansion is primarily driven by the accelerating global transition toward electric mobility, underpinned by stringent government emissions regulations and rapidly increasing EV production volumes. According to the International Energy Agency (IEA) Global EV Outlook 2025, global electric car sales exceeded 17 million units in 2024, representing over 20% of all cars sold worldwide, a milestone that directly amplifies demand for specialized adhesives used in battery assembly, structural bonding, and thermal management applications.

Key Market Highlights

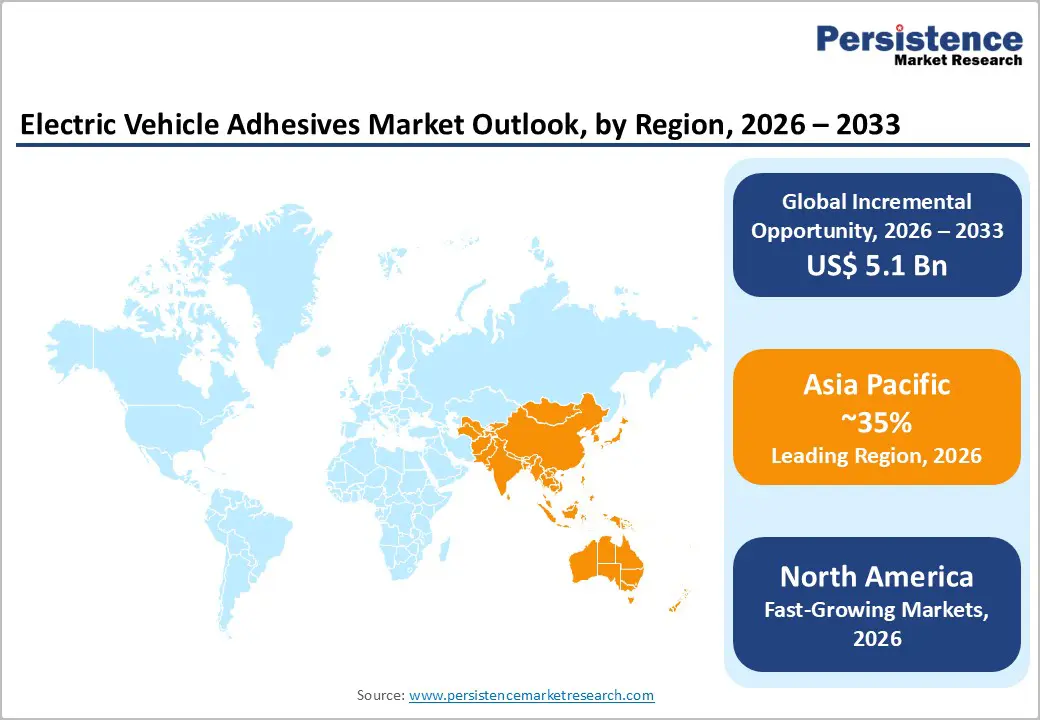

- Leading Region: Asia Pacific leads the global Electric Vehicle Adhesives market, supported by China's near-50% domestic EV sales penetration in 2024 and its position as the world's largest EV producer, creating unrivaled demand for battery and structural adhesive applications.

- Fastest Growing Region: North America represents a high-growth, innovation-driven market for Electric Vehicle Adhesives, anchored by the robust EV manufacturing ecosystem and regulatory framework in the United States.

- Dominant Segment: Structural Adhesives dominate the product type segment with approximately 42% share, driven by their critical role in battery pack frame bonding, body-in-white assembly, and powertrain component joining across EV platforms adopting multi-material architectures.

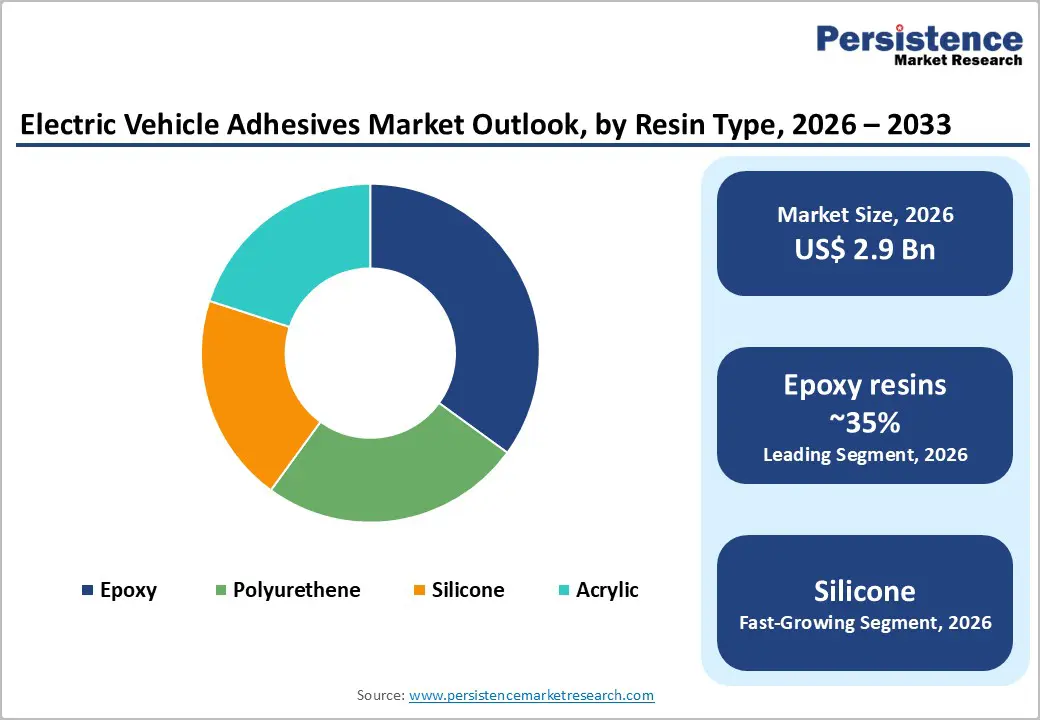

- Fastest Growing Segment: Epoxy resin-based adhesives represent the leading resin type segment, while Silicone is the fastest-growing owing to escalating thermal management requirements in high-voltage (400V-800V) EV battery systems requiring stable performance from -40°C to +200°C.

- Key Market Opportunity: A key market opportunity lies in the transition to Cell-to-Pack (CTP) and Cell-to-Body (CTB) battery architectures, which increases the adhesive-bonded surface area per vehicle by up to 300%, creating substantial incremental volume demand for thermal, structural, and sealing adhesive solutions.

| Key Insights | Details |

|---|---|

| Electric Vehicle Adhesives Market Size (2026E) | US$ 2.9 Bn |

| Market Value Forecast (2033F) | US$ 8.0 Bn |

| Projected Growth CAGR (2026 - 2033) | 15.6% |

| Historical Market Growth (2020 - 2025) | 14.5% |

Market Dynamics

Drivers - Surging Global EV Production and Government Policy Support

The most compelling driver of the Electric Vehicle Adhesives market is the exponential growth in electric vehicle production, reinforced by ambitious government policy frameworks across major economies. The IEA confirmed that EV sales surged by approximately 35% year-on-year in Q1 2025, with global electric car sales on track to exceed 20 million units in 2025 alone. In the United States, the Inflation Reduction Act (IRA) and the U.S. EPA's Multi-Pollutant Emissions Standards for model years 2027 and beyond are projected to drive electric passenger and light-duty vehicle sales to approximately 70% of total U.S. sales by 2032. In China, EV market share approached 50% of all car sales in 2024. The European Union's CO2 standards mandate a 90% reduction in vehicle emissions by 2040.

Rising Demand for Lightweight, Multi-Material Vehicle Architectures

As automakers worldwide intensify their focus on extending driving range and improving energy efficiency, the shift toward lightweight multi-material vehicle construction combining advanced high-strength steels, aluminum alloys, carbon fiber composites, and engineering polymers is dramatically increasing reliance on high-performance adhesives. Adhesives are uniquely capable of joining dissimilar materials without introducing stress concentrations or corrosion that mechanical fasteners cause at metal-composite interfaces. The European Automobile Manufacturers' Association (ACEA) highlights that every 100 kg reduction in vehicle weight can improve energy efficiency by approximately 6-8%, making structural adhesive bonding a critical enabler of EV range optimization.

Market Restraints

High Production Costs and Raw Material Price Volatility

A significant restraint on the Electric Vehicle Adhesives market is the high cost of specialized adhesive formulations and the inherent volatility of key raw materials. For example, the cost of epoxy resin a foundational resin type in the market increased by approximately 15% between 2023 and 2024 owing to supply chain disruptions and tightening feedstock availability. Specialty performance additives, including thermally conductive fillers and reactive diluents, further compound input cost pressures. Smaller adhesive manufacturers face difficulties achieving cost parity with global players such as Henkel and 3M, which leverage large-scale procurement and proprietary process integration. These cost dynamics can slow adoption of advanced adhesive solutions, particularly among cost-sensitive EV Tier-2 and Tier-3 assembly suppliers.

Stringent Performance Requirements and Complex Qualification Timelines

EV adhesives must withstand extreme thermal cycling (typically from -40°C to +150°C), mechanical vibration, chemical exposure from electrolytes, and dimensional changes over battery lifecycles, all while meeting increasingly demanding IP68 ingress protection standards for battery enclosures. The qualification and validation cycle for new adhesive formulations in automotive applications can span 18 to 36 months, representing a substantial barrier for new entrants and product innovations alike. This extended timeline constrains suppliers' ability to rapidly respond to evolving EV platform designs, such as the shift to cell-to-pack and cell-to-body architectures, where adhesives must interface with coolants and structural load paths simultaneously.

Opportunities - Emerging Cell-to-Pack and Cell-to-Body Battery Architecture Transition

One of the most transformative opportunities for the Electric Vehicle Adhesives market lies in the industry-wide transition toward advanced battery architectures, including Cell-to-Pack (CTP) and Cell-to-Body (CTB) designs pioneered by leading manufacturers such as BYD, CATL, and Tesla. These architectures eliminate conventional module housings and bond battery cells directly to structural pack frames or vehicle floor structures, increasing the surface area requiring specialized adhesives by up to 300% compared to traditional module-based designs. This shift intensifies demand for thermally conductive gap fillers, structural epoxy adhesives, and flame-retardant sealants simultaneously. Dow Inc. has actively invested in dedicated EV adhesive and gap filler production capacity, explicitly targeting this architectural transition. As CTP designs gain traction beyond China into Europe and North America, adhesive volume per vehicle is expected to increase substantially through the forecast period.

Thermal Management Materials for Next-Generation High-Energy-Density Batteries

The accelerating development of next-generation battery chemistries, including lithium iron phosphate (LFP) cells operating at higher charge rates, solid-state precursor designs, and 400V-800V high-voltage battery systems, creates a significant opportunity for advanced Thermal Management Materials within the EV adhesives ecosystem. Higher energy densities inherently generate greater heat loads, which must be precisely managed to protect cell integrity and prevent thermal runaway events. Thermally conductive adhesives and gap fillers that simultaneously provide structural bonding and heat dissipation are expected to be among the fastest-growing sub-segments. Henkel AG showcased AI-powered virtual adhesive simulation capabilities and its Loctite HT 1000 high-temperature silicone gap filler series at the Battery Show Europe 2025, underscoring the intensifying innovation pipeline targeting this opportunity.

Category-wise Analysis

Product Type Insights

Among the product type segments, structural adhesives, sealants & gasketing, and thermal management materials, structural adhesives represent the dominant segment, accounting for approximately 42% of the overall market share. The leading position of structural adhesives is underpinned by their critical role in EV battery pack assembly, body-in-white construction, and powertrain component bonding. Structural adhesives, particularly epoxy-based crash-resistant formulations and two-component polyurethane systems, are increasingly deployed as direct replacements for mechanical fasteners in high-load structural joints, offering superior fatigue resistance and enabling multi-material bonding. Volkswagen's documented use of DuPont BETAMATE 2090 adhesive for structural battery pack frame assembly exemplifies the growing OEM preference for structural adhesive solutions.

End-Use Analysis

The Passenger Cars segment dominates the End-Use category, holding approximately 58% of the global Electric Vehicle Adhesives market share. This leadership is directly attributable to the disproportionate volume and growth rate of battery-electric passenger vehicles relative to commercial vehicle segments. According to the IEA Global EV Outlook 2025, passenger electric cars accounted for the overwhelming majority of the 17 million+ EVs sold globally in 2024, with China alone representing nearly half of global passenger EV sales. Passenger EV platforms, particularly in the compact SUV and sedan segments, consume significant volumes of structural adhesives, sealants, and thermal management materials per vehicle across battery systems, closures, and body structures. The rapid introduction of new passenger EV models, with nearly 600 electric car models available globally as of 2024 per IEA data sustains robust per-vehicle adhesive demand.

Resin Type Analysis

Epoxy resins are the leading resin type, accounting for approximately 35% of the market share. Epoxy-based adhesives deliver the combination of high tensile strength (often exceeding 30 MPa), excellent chemical resistance, low shrinkage on cure, and compatibility with diverse substrates, including metals, composites, and engineering polymers, properties essential for structurally demanding EV applications. Their use in crash-resistant structural bonding for battery pack frames, body-in-white assembly, and powertrain housings is particularly widespread among European and North American OEMs. DuPont's broad-bake epoxy adhesive technology, which reduces curing temperatures by 20°C to save energy while maintaining structural integrity, exemplifies ongoing innovation in the epoxy segment.

Regional Insights

North America Electric Vehicle Adhesives Trends

North America is a high-growth, innovation-driven market for Electric Vehicle Adhesives, anchored by the robust EV manufacturing ecosystem and the United States' regulatory framework. The U.S. EPA's Multi-Pollutant Emissions Standards for model years 2027 and beyond are expected to drive electric light-duty vehicle sales to approximately 70% of total U.S. passenger vehicle sales by 2032, while California's Advanced Clean Cars II regulations, adopted by 12 additional states collectively representing around one-third of U.S. light-duty vehicle sales reinforce a durable demand trajectory.

The North American market is further characterized by a strong innovation ecosystem, with leading adhesive manufacturers maintaining dedicated R&D centers in the region. DuPont's Battery Technology centre of Excellence in Auburn Hills, Michigan, and Dow's investment in renewable-energy-powered EV adhesive and gap filler production facilities underscore the region's role as a critical centre for next-generation adhesive development.

Europe Electric Vehicle Adhesives Trends

Europe holds a significant share of the global Electric Vehicle Adhesives market, driven by stringent regulatory mandates and deep-rooted automotive manufacturing traditions in Germany, the U.K., France, and Spain. The European Union's CO2 standards for cars and vans require progressive zero-emission sales share increases, targeting approximately 60% electric LDV share by 2030 and 85% by 2035 under stated policy scenarios (IEA). Germany became the third country globally to record over 500,000 new BEV registrations in a single year, with battery electric vehicles representing 18% of total car sales in 2023.

European automotive OEMs, including Volkswagen Group, Stellantis, and BMW Group, are advancing multi-material body-in-white designs, accelerating structural adhesive adoption across vehicle platforms. Sika AG and Henkel are particularly well-positioned given their strong European operational footprints and dedicated automotive adhesive R&D capabilities.

Asia Pacific Electric Vehicle Adhesives Trends

Asia Pacific is both the largest and fastest-growing regional market for Electric Vehicle Adhesives, led by China's unrivaled position as the world's dominant EV producer and consumer. Electric cars accounted for nearly 50% of all car sales in China in 2024, with Chinese OEMs producing more than 70% of global electric cars and exporting nearly 1.25 million vehicles internationally (IEA 2025). China's dominance in cell-to-pack battery architecture pioneered by CATL and BYD is a key driver of per-vehicle adhesive content growth, as these designs substantially increase adhesive-bonded surface areas within battery systems.

Southeast Asia is emerging as an important growth frontier, with electric car sales growing nearly 50% in the region in 2024 to represent 9% of total regional car sales (IEA). Thailand and Vietnam are particularly active markets, attracting EV manufacturing investments from BYD and other Chinese OEMs.

Competitive Landscape

The global Electric Vehicle Adhesives market exhibits a moderately consolidated competitive structure, dominated by a group of large, diversified chemical and specialty materials companies that collectively hold the majority of market share. Henkel AG, 3M, Sika AG, Dow, DuPont, BASF, Arkema (Bostik), and H.B. Fuller command strong positions owing to their broad adhesive portfolios, global manufacturing footprints, and established relationships with Tier-1 automotive suppliers and OEMs. Key differentiation strategies among market leaders include proprietary resin technology, application-specific product development, co-development partnerships with automakers, investments in digital simulation tools such as Henkel's AI-powered virtual adhesives, and capacity expansions near growing EV manufacturing hubs in Asia, Europe, and North America.

Key Developments:

- In December 2025, BASF co-developed and unveiled a solid-state battery pack concept with Welion, highlighting new battery-pack integration approaches where bonding, sealing, and pack materials performance are critical.

- In November 2025, Henkel introduced new LOCTITE thermal potting solutions aimed at protecting and improving the reliability of EV components, strengthening its e-mobility adhesives and encapsulation portfolio.

Companies Covered in Electric Vehicle Adhesives Market

- Henkel

- 3M

- Sika AG

- H.B. Fuller Company

- Arkema

- Dow

- DuPont

- BASF

- Huntsman International LLC.

- PPG Industries, Inc.