- Automotive Components & Materials

- Electric Drive Unit Market

Electric Drive Unit Market Size, Share, and Growth Forecast 2026 - 2033

Electric Drive Unit Market by Component (Electric Motor, Power Electronics, Transmission/Gearbox, Differential, Others), by Propulsion (BEV, Hybrid), by Power Output (Below 100 kW, 100–250 kW, Above 250 kW), by Sales Channel (OEM, Aftermarket), and Regional Analysis, 2026 - 2033

Electric Drive Unit Market Size and Trend Analysis

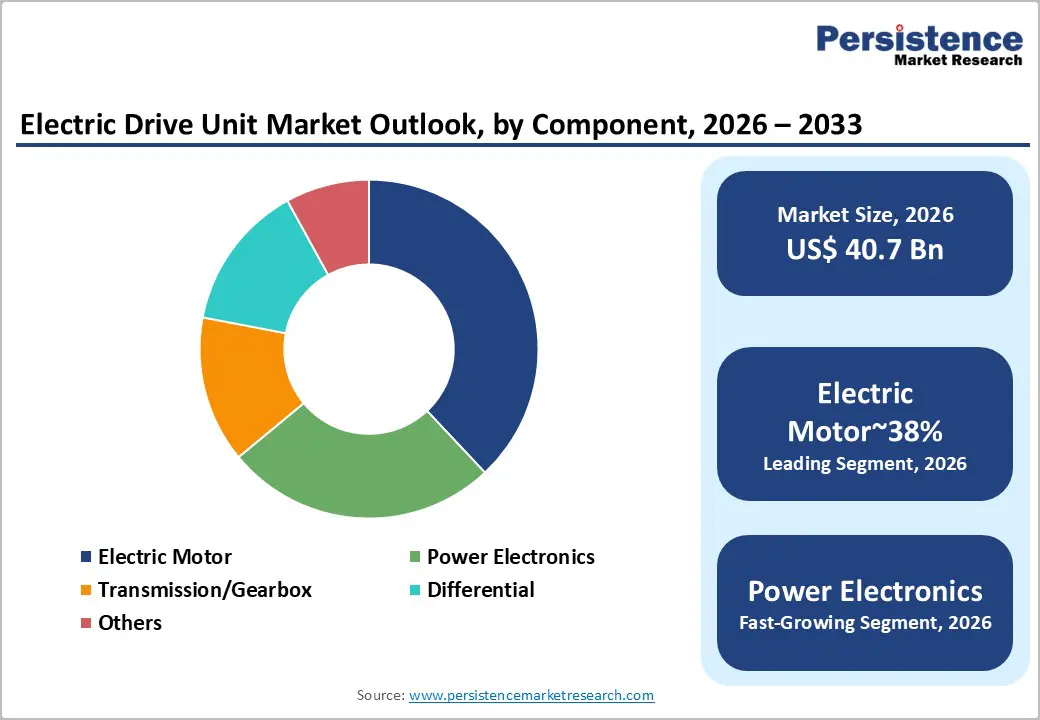

The global electric drive unit market size is likely to be valued at US$40.7 billion in 2026 and is expected to reach US$82.4 billion by 2033, growing at a CAGR of 10.6% during the forecast period from 2026 to 2033. The electric drive unit market is experiencing rapid growth due to the global shift toward vehicle electrification, increasing legislative pressure on OEMs to phase out internal combustion engines, and the commercialization of compact e-axle systems that integrate motors, power electronics, and transmission.

Key Industry Highlights:

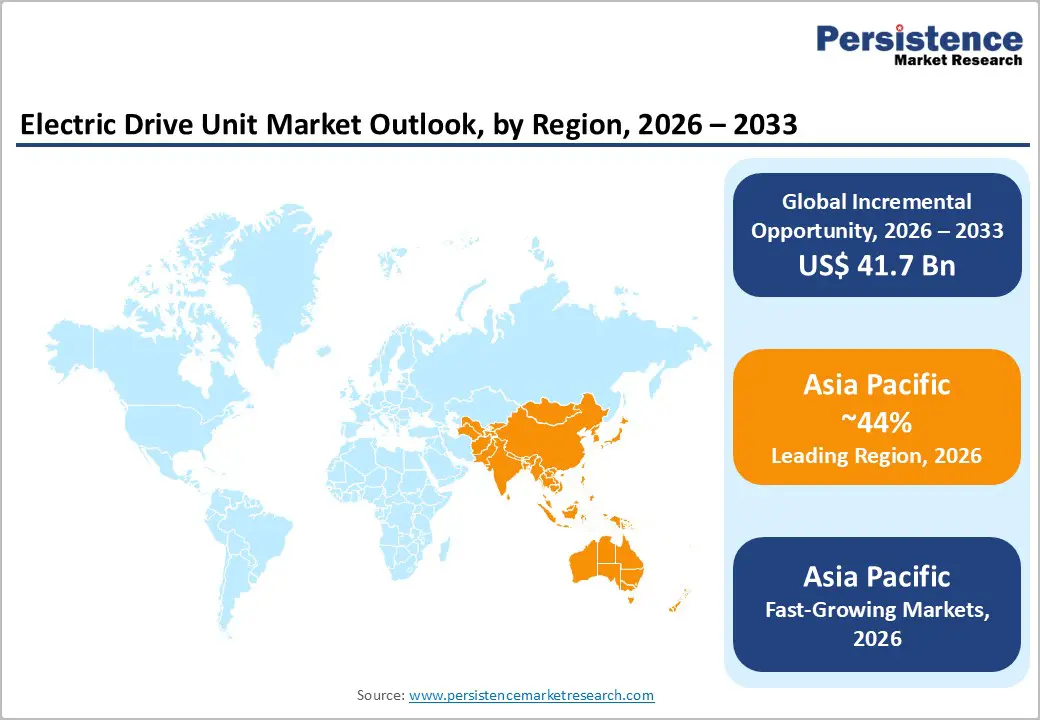

- Leading Region: Asia Pacific leads the global electric drive unit market with approximately 44% of total revenues, anchored by China's record 11 million EV sales in 2024 and a deeply integrated domestic EDU manufacturing ecosystem spanning BYD, CATL, and global Tier-1 suppliers investing in local production capacity

- Fastest-Growing Region: Asia Pacific is also the fastest-growing region, driven by China's NEV Plan targeting 50% EV share by 2035, India's PM E-Drive scheme catalyzing domestic EV production, and ASEAN nations attracting major OEM manufacturing investments in Thailand, Vietnam, and Indonesia

- Leading Segment: The Electric Motor component segment leads the By Component category with approximately 38% revenue share, reflecting universal OEM adoption of permanent magnet synchronous motor architectures achieving upto 95% peak efficiency in passenger BEV and hybrid drive unit platforms globally

- Fastest-Growing Segment: Battery Electric Vehicles (BEVs) are the dominant and fastest-growing propulsion segment with approximately 72% market share, reinforced by 17.1 million global EV sales in 2024 and binding legislative mandates in the EU, China, and the U.K. requiring 100% zero-emission new vehicle sales by 2035

- Key Opportunity: The commercial vehicle EDU electrification segment, targeting above 250 kW power output applications, represents the most significant near-term opportunity, with ICCT projecting that zero-emission commercial vehicles must represent over 60% of new sales by 2030 in leading markets, driving high-value long-term OEM procurement contracts

| Key Insights | Details |

|---|---|

|

Electric Drive Unit Market Size (2026E) |

US$ 40.7 Billion |

|

Market Value Forecast (2033F) |

US$ 82.4 Billion |

|

Projected Growth CAGR (2026–2033) |

10.6% |

|

Historical Market Growth (2020–2025) |

8.4% |

DRO Analysis

Driver - Record Global EV Adoption Driving Structural, High-Volume Demand for Integrated Drive Units

The rapid acceleration of global EV adoption is the key structural driver behind sustained demand growth in the electric drive unit market . Every battery electric and hybrid vehicle requires at least one complete electric drive unit, including the motor, inverter, and gearbox, while premium all-wheel-drive models often use two or more units per vehicle. Global EV sales reached 17.1 million units in 2024, and the IEA projects this will exceed 20 million units in 2025, meaning one in every four new vehicles sold will be electric.

China alone accounted for 11 million EV sales in 2024, marking a strong 40% year-on-year increase and driving significant procurement demand for drive units. With the global EV fleet reaching nearly 58 million vehicles by the end of 2024, the continuous rise in production ensures stable, high-volume demand for advanced EDUs through the 2026–2033 forecast period.

Technological Evolution Toward Highly Integrated E-Axle Architectures Expanding Per-Unit Value

In addition to volume growth, technological advancements are significantly increasing the value of electric drive units per vehicle. Automakers are shifting from sourcing separate components to adopting fully integrated e-axle systems that combine the motor, inverter, and gearbox into a single unit. This integration reduces vehicle weight, simplifies design, and improves efficiency and performance.

ZF Friedrichshafen’s modular eDrive platform offers power outputs ranging from 75 kW to 400 kW using advanced 400V and 800V architectures with SiC-based power electronics. Such systems allow OEMs to customize performance while reducing development timelines by up to 50%. The transition toward 800V platforms and silicon carbide inverters is also increasing the average selling price of drive units. As a result, suppliers are benefiting from higher revenue per vehicle and expanding overall market opportunities.

Restraint - Raw Material Price Volatility and Rare Earth Supply Chain Concentration

The electric drive unit market faces significant risks due to its reliance on rare-earth materials such as neodymium and dysprosium, which are essential to permanent-magnet motors widely used in EVs. According to the U.S. Geological Survey, China controls nearly 85% of global rare earth processing capacity, creating a highly concentrated supply chain.

This dependence exposes manufacturers to price fluctuations and supply disruptions, which directly impact production costs. When rare earth prices rise, the overall bill of materials for drive units increases, putting pressure on profit margins for both OEMs and Tier-1 suppliers. Smaller manufacturers, in particular, face challenges due to their limited ability to hedge against price volatility. Additionally, cost uncertainty can delay new vehicle programs, as automakers prioritize cost optimization in component sourcing. This supply chain vulnerability remains a critical challenge for the long-term stability of the market.

High Capital Investment Requirements for Manufacturing Capacity Expansion

Expanding electric drive unit manufacturing capacity requires substantial capital investment, creating a major barrier for new and smaller market players. Production involves advanced processes such as precision machining, motor winding, power electronics assembly, and rigorous testing systems, all of which demand high-cost infrastructure. Setting up a new integrated e-axle production facility typically requires investments of USD 200-500 million.

These facilities often take 18 to 36 months to reach full production capacity. This high capital intensity limits participation to well-established automotive suppliers such as Bosch, ZF Friedrichshafen, BorgWarner, and Magna International. As a result, the market remains concentrated among a few large players, reducing competition and increasing OEMs' supply dependency. This concentration can also create risks in terms of supply continuity and pricing power within the industry.

Opportunities - Electrification of Commercial Vehicles and Heavy-Duty Applications Demanding High-Power EDUs

The growing electrification of commercial vehicles presents a major opportunity for electric drive unit manufacturers. Segments such as buses, delivery vans, heavy trucks, and construction equipment require high-performance drive units designed for demanding operating conditions. According to the ICCT, zero-emission vehicles must account for over 60% of new commercial vehicle sales by 2030 in leading markets. Electric drive units used in these applications typically operate above 250 kW and command higher prices due to their advanced engineering requirements, including thermal durability and high load capacity.

Companies such as Equipmake have developed specialized high-torque motors tailored for heavy-duty applications. These solutions are increasingly being adopted by fleet operators and transit authorities, creating long-term supply contracts and stable revenue streams. This shift toward commercial EV electrification is expected to significantly expand the high-value segment of the EDU market.

Emerging Markets and Regional Manufacturing Localization Creating New Supplier Entry Points

Government initiatives promoting local EV manufacturing are opening new growth avenues for electric drive unit suppliers in emerging markets. Countries such as India, Brazil, and those in Southeast Asia are introducing policies to boost domestic production and reduce import dependence. India’s PM E-Drive scheme and Production-Linked Incentive (PLI) programs are encouraging OEMs such as Tata Motors and Mahindra to build localized supply chains.

ASEAN countries, including Vietnam, Thailand, and Indonesia, are becoming key EV manufacturing hubs, attracting investments from global players such as BYD, Toyota, and Great Wall Motors. These developments are creating strong demand for locally produced drive units and components. Suppliers that establish regional production or form partnerships with local OEMs can gain a competitive advantage. This trend is expected to diversify the global supply chain while creating new revenue opportunities in high-growth markets.

Category-wise Analysis

By Component Insights

The electric motor segment leads the component category, accounting for around 38% of total market revenue. At the core of the drive unit, electric motors combine advanced electromagnetic design with efficient thermal management systems, typically using permanent-magnet synchronous motor technology. These motors deliver high efficiency levels of up to 97%, making them the preferred choice for major automakers such as Tesla, Volkswagen, BYD, and Hyundai. Their ability to provide high torque density and support regenerative braking further strengthens their dominance.

At the same time, increasing performance demands are driving innovations in motor design and materials, raising their overall cost and value. Meanwhile, the power electronics segment is the fastest-growing, fueled by the shift toward silicon carbide-based inverters. These advanced systems enable faster charging and improved efficiency, particularly in 800V vehicle architectures, thereby increasing their adoption across next-generation EV platforms.

By Propulsion Insights

Battery electric vehicles dominate the propulsion segment, contributing approximately 72% of total market revenue. Unlike hybrid vehicles, which use electric drive units as supplementary systems, BEVs rely entirely on them for propulsion, resulting in higher system complexity and content per vehicle. Global production of BEVs has increased significantly, driven by strong demand in China and supportive government policies in Europe and other regions.

Regulatory initiatives such as the European Union’s 2035 ban on internal combustion engine vehicles are accelerating the shift toward fully electric platforms. This transition is prompting automakers to invest heavily in BEV development, ensuring the continued dominance of this segment. As hybrid vehicles gradually phase out, the reliance on full battery systems will further increase demand for advanced drive units, reinforcing BEV leadership in the market throughout the forecast period.

By Power Output Insights

The 100–250 kW segment holds the largest share of the market, accounting for approximately 48% of total revenue. This range aligns with the requirements of most passenger vehicles and light commercial EVs, offering a balanced combination of performance, efficiency, and cost. Popular models such as the Tesla Model 3, Hyundai IONIQ 6, and Volkswagen ID.4 fall within this category, making it the most widely adopted power range globally.

Leading suppliers are designing scalable platforms around this segment to maximize compatibility across multiple vehicle models. For example, modular systems allow manufacturers to adapt power outputs based on vehicle requirements. Meanwhile, the above 250 kW segment is experiencing the fastest growth, driven by increasing demand for high-performance vehicles and heavy-duty applications. These high-power systems command premium pricing due to their advanced engineering and superior performance capabilities.

By Sales Channel Insights

The OEM sales channel dominates the market, accounting for approximately 88% of total revenue. Electric drive units are highly integrated into vehicle architecture, making them essential components designed during the vehicle development phase. This integration limits the scope for aftermarket replacement, as EDUs are not easily interchangeable like traditional automotive parts. OEMs typically enter into long-term supply agreements with Tier-1 suppliers, ensuring consistent demand and stable revenue.

These agreements often include co-development partnerships, allowing suppliers to align closely with automaker requirements. While the aftermarket segment currently represents a small share, it is gradually emerging in niche applications such as vehicle retrofitting and fleet electrification. In particular, bus and commercial fleet operators are exploring replacing conventional drivetrains with electric systems, creating new opportunities for aftermarket EDU suppliers, especially in regions such as Europe and India.

Regional Insights

North America Electric Drive Unit Market Trends

North America represents a highly dynamic market driven by strong policy support and technological innovation. The U.S. Inflation Reduction Act has significantly accelerated EV adoption by offering incentives for domestic manufacturing and clean energy investments. This has encouraged major suppliers such as BorgWarner, Magna, and Dana to expand their production capabilities within the region.

Automakers, including General Motors, Ford, and Stellantis, are also increasing EV production, driving demand for locally sourced drive units. Canada is contributing to regional growth through its zero-emission vehicle mandate, which targets full electrification of new passenger vehicles by 2035. Additionally, government-backed research initiatives are supporting the development of next-generation technologies, including silicon carbide inverters and advanced motor designs. These combined efforts are strengthening North America’s position as a key innovation hub for the development of electric drive units.

Europe Electric Drive Unit Market Trends

Europe remains a strategically important market, supported by strong regulatory frameworks and a well-established automotive supply chain. The European Green Deal and the 2035 ban on internal combustion engine vehicles are driving rapid electrification across the region. Germany serves as the central hub for drive unit innovation, hosting leading suppliers such as Bosch, ZF Friedrichshafen, and Continental. Automakers, including BMW, Volkswagen, and Mercedes-Benz, are expanding their electric vehicle portfolios, generating sustained demand for advanced drive systems.

France and the UK are also contributing through companies like Valeo and Equipmake, which focus on both passenger and commercial EV applications. Additionally, countries such as Spain are emerging as manufacturing centers due to increasing investments from global automakers. This strong ecosystem of suppliers and OEMs ensures continued growth and technological advancement in the European market.

Asia Pacific Electric Drive Unit Market Trends

Asia Pacific is the largest and fastest-growing region, accounting for nearly half of global market revenue. China dominates the region, with 11 million EVs sold in 2024 and a highly integrated manufacturing ecosystem covering batteries, motors, and power electronics. Domestic companies such as BYD and Huawei are developing advanced integrated drive systems, competing with global suppliers.

Japan contributes through strong engineering capabilities from companies like DENSO and AISIN, supporting both hybrid and electric platforms. India is emerging as a key growth market, driven by government incentives and increasing domestic EV production. Meanwhile, ASEAN countries, including Thailand, Vietnam, and Indonesia, are attracting significant investments, positioning themselves as new EV manufacturing hubs. This regional expansion is creating diverse growth opportunities for drive unit suppliers and strengthening the Asia Pacific’s leadership in the global market.

Competitive Landscape

The electric drive unit market is moderately consolidated, with a few large players dominating global supply. Companies such as Bosch, ZF Friedrichshafen, BorgWarner, Magna, and Valeo offer integrated solutions combining motors, inverters, and transmission systems. Their competitive advantage lies in scalable platform designs, advanced power electronics integration, and strong engineering capabilities. Modular solutions, such as ZF’s eDrive platform, allow automakers to reduce development time and improve efficiency.

Software integration is becoming a key differentiator, with features such as over-the-air updates and performance optimization gaining importance. Alongside these major players, specialized companies such as Equipmake and Hofer Powertrain are focusing on high-performance and niche applications, particularly in commercial and heavy-duty segments. This mix of large-scale suppliers and specialized innovators is shaping a competitive and evolving market landscape.

Key Developments:

- January 2025: ZF Friedrichshafen introduced its advanced 800V electric axle drive featuring integrated silicon carbide (SiC) power electronics, significantly enhancing efficiency and performance. Designed for premium EV platforms launching from 2026, the system delivers 30% higher power density, supporting next-generation high-performance electric vehicles.

- March 2024: BorgWarner Inc. launched its Integrated Drive Module (iDM) for a leading global OEM’s BEV platform, combining motor, inverter, and gearbox into a compact unit. Rated up to 250 kW, the solution strengthens BorgWarner’s position in North America’s electric drive unit supply market.

- October 2024: BluE Nexus, a joint venture of Toyota, AISIN, and DENSO, began mass production of its next-generation transaxle electric drive unit for Toyota’s BEV lineup. The new system achieves 15% higher efficiency, reinforcing Japan’s strong innovation capabilities in electric and hybrid drivetrain technologies.

Companies Covered in Electric Drive Unit Market

- Bosch

- ZF Friedrichshafen AG

- Magna International

- BorgWarner Inc.

- Valeo

- Continental AG

- Schaeffler AG

- DENSO Corporation

- AISIN Corporation

- BluE Nexus

- DANA TM4 INC.

- Equipmake

- ElringKlinger AG

- FRIWO Gerätebau GmbH

- hofer powertrain

Frequently Asked Questions

The global Electric Drive Unit Market is estimated at US$ 40.7 Billion in 2026 and is projected to reach US$ 82.4 Billion by 2033, growing at a CAGR of 10.6%, driven by 17.1 million global EV sales in 2024, a 25% year-on-year increase, and the rapid OEM transition to fully integrated e-axle architectures incorporating SiC power electronics and 800V platforms.

The key drivers are the explosive surge in global EV production, with the IEA projecting over 20 million new EVs sold in 2025, combined with the technology-driven shift to integrated e-axle architectures such as ZF's modular eDrive kit, which reduces OEM development time by 50% and substantially increases per-vehicle EDU content value across passenger car and commercial vehicle platforms.

The Electric Motor segment leads with approximately 38% revenue share, driven by universal OEM adoption of permanent magnet synchronous motor (PMSM) architectures achieving 94–97% peak efficiency in BEV and hybrid platforms. Companies including Bosch, DENSO, and Nidec are investing in next-generation winding and magnetic material innovations to sustain performance advantages as 800V system architectures become the new OEM standard.

Asia Pacific leads with approximately 44% of global revenues, anchored by China's record 11 million EV sales in 2024, a 40% year-on-year increase, and a deeply integrated domestic EDU manufacturing ecosystem. Japan's technical leadership through DENSO, AISIN, and BluE Nexus, combined with India's rapidly expanding EV sector under the PM E-Drive scheme, reinforces Asia Pacific's dominant regional position through 2033.

The electrification of commercial vehicles, buses, delivery vans, and Class 6–8 trucks, targeting the Above 250 kW power band represents the highest-value near-term opportunity. The ICCT projects zero-emission commercial vehicles must represent over 60% of new sales by 2030, generating large, multi-year OEM procurement contracts for purpose-built, high-torque electric drive units with premium per-unit pricing well above passenger car equivalents.

The leading participants include ZF Friedrichshafen AG, Bosch, BorgWarner Inc., Magna International, Valeo, Continental AG, Schaeffler AG, DENSO Corporation, AISIN Corporation, BluE Nexus, DANA TM4 INC., Equipmake, ElringKlinger AG, FRIWO Gerätebau GmbH, and hofer powertrain, with Nidec Corporation and Vitesco Technologies also holding significant positions in the global EDU competitive landscape.