- Non-food Packaging

- Effervescent Packaging Market

Effervescent Packaging Market Size, Share, and Growth Forecast 2026 - 2033

Effervescent Packaging Market by Product Type (Tablets, Powder, Granules), Material Type (Aluminum, Plastic, Metal, Others), End-user (Pharmaceuticals, Nutraceuticals, Personal Care, Household Cleaning, Others), and Regional Analysis for 2026 - 2033

Effervescent Packaging Market Size and Trend Analysis

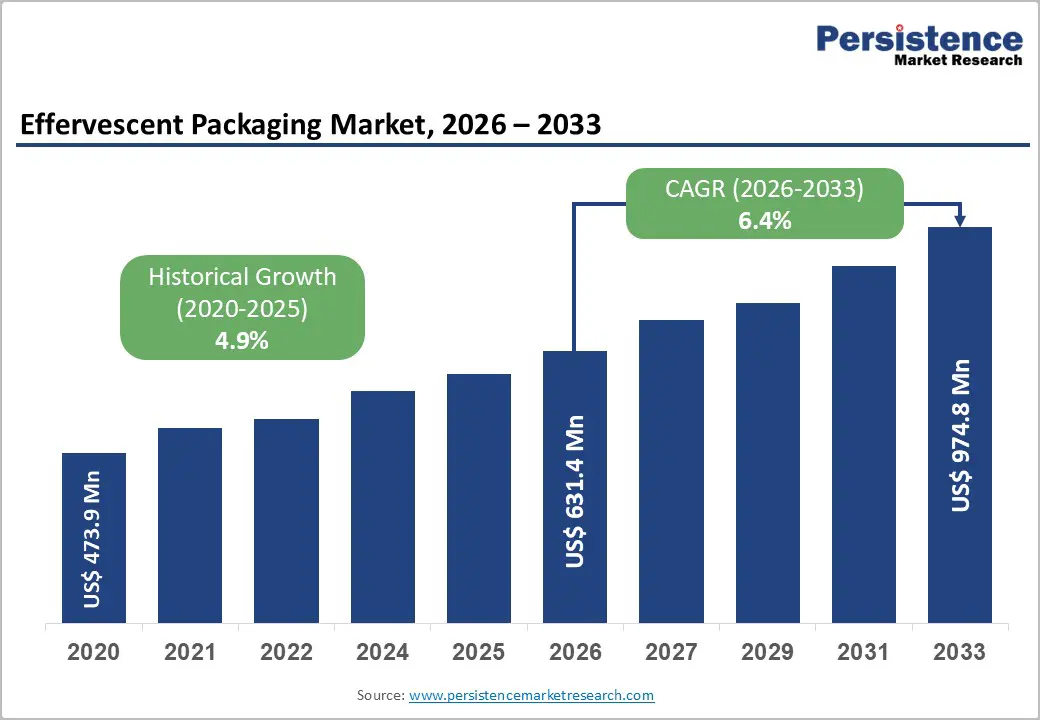

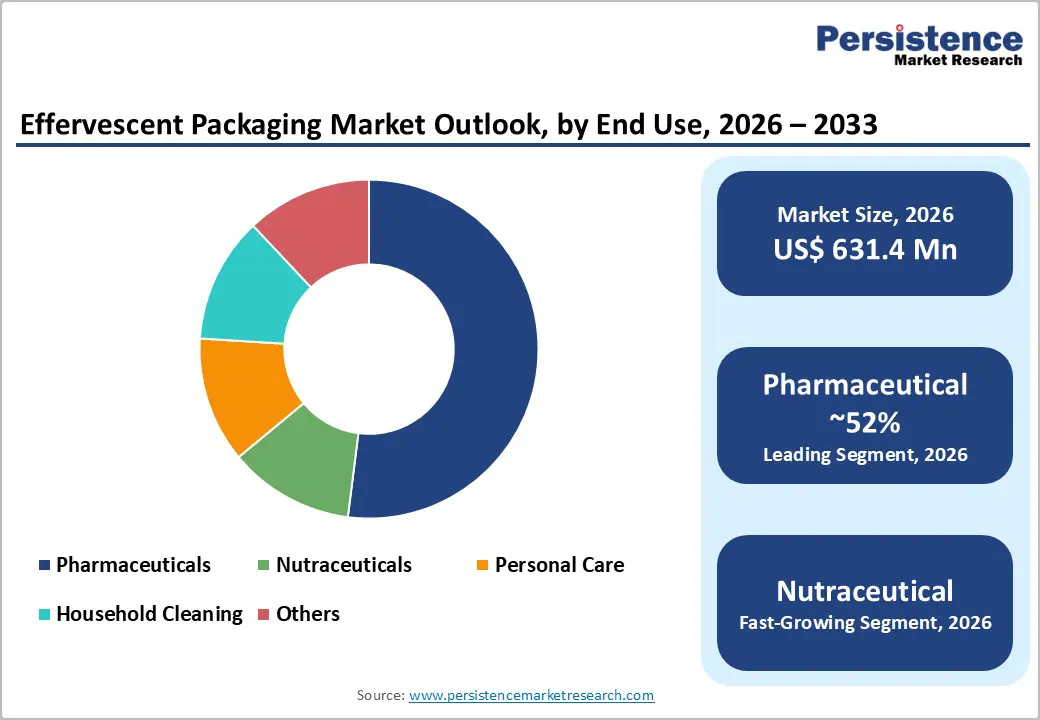

The global Effervescent Packaging market size is valued at US$ 631.4 million in 2026 and is projected to reach US$ 974.8 million by 2033, growing at a CAGR of 6.4% between 2026 and 2033. The market’s strong growth trajectory is driven by rising global demand for convenient and portable pharmaceutical and nutraceutical dosage forms that require advanced, high-barrier packaging to maintain product stability and extend shelf life.

According to the World Health Organization, global pharmaceutical spending reached USD 1.48 trillion in 2023, with effervescent formulations constituting a rapidly expanding sub-segment. This growth is further reinforced by the continued expansion of the OTC medication and dietary supplement industries, influenced by increasing chronic disease prevalence, aging populations, and heightened health-and-wellness awareness across emerging markets, all of which intensify the need for hermetically sealed, moisture-resistant packaging systems.

Key Industry Highlights:

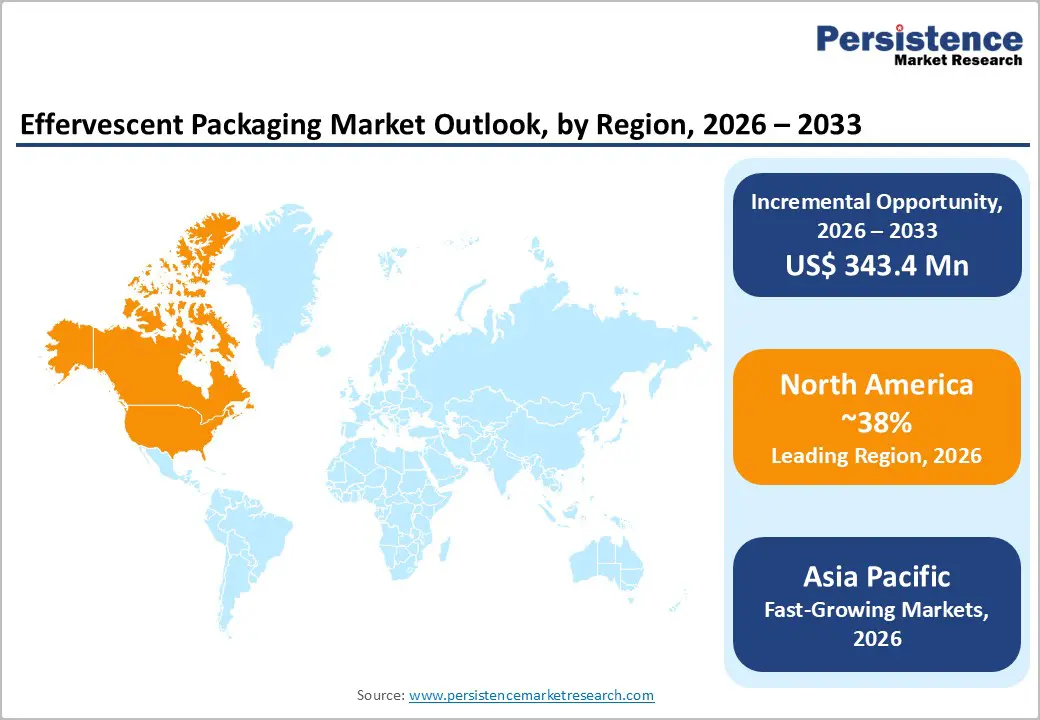

- Regional Leader: North America leads the global effervescent packaging market, holding approximately 38% of global revenue in 2026, supported by a mature pharmaceutical and nutraceutical industry, high OTC supplement consumption, and FDA compliance mandates that sustain demand for premium-grade, high-barrier packaging formats.

- Fastest Growing Region: Asia-Pacific is the fastest-growing region, projected to expand at approximately 9.2% CAGR through 2033, driven by expanding pharmaceutical manufacturing investment in China and India, rising health-and-wellness spending, and growing demand for advanced moisture-barrier packaging in high-humidity tropical climate environments.

- Leading Segment: Tablets dominate the product type segment with approximately 40% market share, reflecting their widespread pharmaceutical and nutraceutical adoption, superior bioavailability profile, and consumer-friendly rapid-dissolution characteristics that are particularly valued by geriatric, pediatric, and on-the-go consumer segments.

- Fastest Growing Segment: Aluminum represents the fastest-growing segment, driven by its unrivalled combination of barrier performance, pharmaceutical regulatory acceptability, and recyclability credentials.

- Key Market Opportunity: The transition to sustainable packaging, mandated by the EU’s PPWR by 2030, is the most transformative market opportunity, with bio-based, post-consumer recycled (PCR), and mono-material recyclable effervescent packaging solutions creating measurable competitive differentiation and significant addressable incremental revenue streams for innovating manufacturers.

| Key Insights | Details |

|---|---|

|

Effervescent Packaging Market Size (2026E) |

US$ 631.4 Mn |

|

Market Value Forecast (2033F) |

US$ 974.8 Mn |

|

Projected Growth CAGR (2026–2033) |

6.4% |

|

Historical Market Growth (2020–2025) |

4.9% |

DRO Analysis

Drivers - Accelerating Demand from the Pharmaceutical and OTC Sector

The pharmaceutical sector remains the foremost and most structurally resilient end-use driver of the effervescent packaging market, owing to its reliance on advanced, high-integrity packaging solutions. Effervescent formulations offer a clinically recognized advantage in bioavailability over conventional solid oral dosage forms, as active ingredients dissolve before ingestion, enabling faster gastric absorption and more uniform therapeutic outcomes. This superiority has supported their widespread use in pain management, antacid therapy, vitamin and mineral supplementation, and electrolyte replacement. With non-communicable diseases accounting for 74% of global deaths, demand for accessible and convenient medication formats continues to rise. Concurrently, the OTC pharmaceutical segment is expanding at a 6.7% CAGR through 2030, further increasing the need for moisture-resistant, oxygen-barrier packaging engineered to preserve product stability and performance.

Rising Health-and-Wellness Consciousness and Dietary Supplement Consumption

The rapid global expansion of the dietary supplement and nutraceutical sector has emerged as a significant structural catalyst for the effervescent packaging industry. Growing consumer inclination toward preventive healthcare is driving demand for effervescent formats used for vitamins, minerals, probiotics, and immunity-enhancing formulations. This preference is particularly prominent among geriatric and pediatric populations, who often have difficulty swallowing conventional tablets, as well as among athletes who require rapid hydration and electrolyte replenishment.

With the Global Wellness Institute valuing the global wellness economy at over USD 5.6 trillion, dietary supplements remain one of its fastest-growing segments. Effervescent packaging, with its hermetically sealed, moisture-resistant designs, including high-barrier aluminum closures and desiccant-integrated tubes, has become essential for manufacturers seeking extended shelf life, strong brand differentiation, and enhanced consumer convenience.

Restraints - High Cost of Specialized Packaging Materials and Volatility in Raw Material Prices

The effervescent packaging market continues to face significant cost-related constraints, particularly in price-sensitive emerging economies. High-performance moisture-barrier materials, such as aluminum laminates, desiccant-integrated closures, and multi-layer polymer films, carry a substantial cost premium compared with standard pharmaceutical packaging. Industry estimates indicate that these advanced materials can be 40–60% more expensive than conventional alternatives. This challenge is further intensified by volatility in raw material prices. For example, aluminum experienced nearly 15% fluctuations in 2024, reducing cost predictability for manufacturers. For small and mid-sized producers, these elevated input costs compress margins and often impede transitions away from lower-cost traditional packaging formats, thereby moderating overall market expansion.

Stringent and Geographically Fragmented Regulatory Compliance Requirements

Effervescent packaging for pharmaceutical and nutraceutical products is governed by stringent and geographically diverse regulatory frameworks, resulting in considerable compliance complexity and elevated operational costs for manufacturers. Requirements span multiple authorities, including the U.S. FDA under 21 CFR Part 211, the European Medicines Agency, and regulatory bodies across Asia-Pacific and Latin America, each imposing distinct standards.

These regulations mandate rigorous material-compatibility assessments, child-resistance performance testing aligned with ISO 8317 and ASTM D3475, comprehensive shelf-life validation, and moisture-barrier certification. The lack of regulatory harmonization necessitates parallel certifications and extensive validation procedures, prolonging development timelines and creating substantial entry barriers for smaller and emerging packaging suppliers.

Opportunity - Growing Adoption of Sustainable and Eco-Friendly Packaging Solutions

The global shift toward sustainable packaging has become one of the most significant commercial opportunities for effervescent packaging manufacturers in the coming decade. The European Union’s Packaging and Packaging Waste Regulation (PPWR) requires all packaging sold within the EU to be fully recyclable by 2030, prompting manufacturers across the value chain to redesign material strategies and accelerate investment in next-generation solutions. This regulatory push, combined with rising consumer demand for environmentally responsible packaging, is driving substantial adoption of bio-based polymers, post-consumer recycled (PCR) resins, and mono-material recyclable barrier films suitable for moisture-sensitive effervescent products. Sanner GmbH exemplifies early innovation with its BioBase® tube, produced from over 90% renewable materials. Companies that successfully balance high moisture-barrier performance with credible recyclability credentials are positioned to secure competitive advantage and premium market positioning.

Rapid Market Expansion in Asia-Pacific Emerging Economies

The Asia-Pacific region, comprising China, India, Japan, and ASEAN economies, represents the most substantial untapped growth opportunity for participants in the global effervescent packaging market. Rising per-capita healthcare expenditure, an expanding middle-income population, and continued government investment in domestic pharmaceutical manufacturing are accelerating the adoption of effervescent dosage formats across the region.

China and India together account for 38% of new global packaging facility investments, driven by efforts to upgrade production capabilities to international standards for effervescent tubes, sachets, and blister formats. The regional market is projected to grow at a CAGR of approximately 9.2%, nearly double the global average. For multinational manufacturers, strategic capacity expansion, partnerships with regional contract packaging organizations, and localized product development tailored to tropical climatic conditions offer high-return avenues to capture this structural growth potential.

Category-wise Analysis

Product Type Insights

Within the product type segmentation, effervescent tablets constitute the leading category, accounting for nearly 40% of the global market. This dominance is attributed to their extensive use across pharmaceutical, nutraceutical, and personal care applications, where accurate dosing, rapid dissolution, and enhanced user convenience are essential. Effervescent tablets provide a documented bioavailability advantage over conventional solid oral forms, as active ingredients dissolve before ingestion, promoting faster gastric absorption and more consistent pharmacokinetic performance.

Peer-reviewed studies have demonstrated significantly higher peak plasma concentrations with effervescent formulations of commonly used analgesics and vitamins. Furthermore, the expanding global geriatric population continues to favor these formats due to widespread dysphagia among older adults. Combined with ongoing advances in high-barrier tubes and closure technologies, these factors firmly reinforce the segment’s leading market position.

Material Type Insights

Aluminum maintains a dominant position within the material type segmentation of the effervescent packaging market, with 43% market share, due to its exceptional barrier properties, strong regulatory acceptance, and well-established recyclability profile. Its ability to achieve moisture vapor transmission rates below 0.05 g/m²/day is critical for preventing the premature chemical reaction between citric acid and sodium bicarbonate in effervescent tablets, thereby preserving product stability. The material’s complete impermeability to oxygen and resistance to photodegradation further reinforce its suitability for tubes, blister foils, and laminated single-dose sachets.

Sustainability considerations also strengthen aluminum’s competitive position, as it is infinitely recyclable without quality loss and aligns closely with the European Union’s PPWR recyclability mandates and similar global policies. Despite facing approximately 15% price volatility in 2024, manufacturers are increasingly adopting long-term supply contracts to stabilize costs and safeguard margins.

End-user Insights

The pharmaceutical segment holds the leading position within the end-use classification of the effervescent packaging market, accounting for nearly 52% of global revenue. This dominance is attributable to the sector’s stringent and uncompromising packaging standards, which require exceptional moisture-barrier performance, regulatory conformity, tamper-evident features, and validated shelf-life stability. Global pharmaceutical expenditure exceeded USD 1.48 trillion in 2023, and effervescent formulations are expected to capture approximately 28% of the OTC medication segment by 2026, driven by rising demand for fast-acting, easy-to-administer alternatives to traditional solid dosage forms.

Key therapeutic categories contributing to this demand include analgesics, antacids, and mineral supplements. Furthermore, mandatory FDA and EMA requirements, such as child-resistant closures, integrated desiccants, and multi-layer barrier film validation, continue to elevate per-unit packaging costs, reinforcing this segment’s substantial revenue share.

Regional Insights

North America Effervescent Packaging Market Trends

North America maintains a leading position in the global effervescent packaging market, with 38% market share, supported by a mature, innovation-oriented pharmaceutical and nutraceutical sector, strong consumer spending on health-and-wellness products, and a highly advanced packaging technology landscape. The United States accounts for nearly 88.8% of the region’s total revenue, enabled by a well-established OTC medication and dietary supplement distribution network, sustained investment in premium packaging formats, and widespread consumer familiarity with effervescent vitamins, sports supplements, and analgesics.

The region is also home to major pharmaceutical corporations whose extensive OTC portfolios drive consistent and large-scale packaging procurement. Moreover, a rigorous regulatory framework, overseen by the FDA through cGMP standards and by the CPSC under the PPPA, continues to elevate quality benchmarks. The presence of leading innovators such as Aptar CSP Technologies further consolidates North America’s status as a hub for advancements in effervescent packaging.

Europe Effervescent Packaging Market Trends

Europe stands as the second-largest regional market for effervescent packaging, supported by strong pharmaceutical manufacturing capabilities and a well-established ecosystem of specialty packaging companies and research institutions across Germany, France, the United Kingdom, and Spain. Germany, in particular, serves as both a major consumer market and a global hub of effervescent packaging innovation, housing leading manufacturers such as Sanner GmbH and Gerresheimer AG, whose extensive international operations supply clients throughout Europe, the Americas, and Asia-Pacific.

The region benefits from a highly structured regulatory environment overseen by the European Medicines Agency, ensuring harmonized product approval standards across member states. Moreover, the EU’s Packaging and Packaging Waste Regulation, mandating full recyclability by 2030, is accelerating the shift toward bio-based tubes, mono-material laminates, and PCR-based solutions. The EMA’s 2025 approval of a new effervescent ibuprofen formulation further reflects ongoing pharmaceutical innovation driving sustained demand for high-performance packaging.

Asia Pacific Effervescent Packaging Market Trends

Asia-Pacific remains the fastest-growing regional market for effervescent packaging, supported by rapid advancements in healthcare infrastructure, a rising middle-income population, and strategic government initiatives aimed at strengthening domestic pharmaceutical manufacturing. China and India together account for 38% of global investments in new packaging facilities as manufacturers upgrade production lines to meet international standards for effervescent tubes, sachets, and blister formats.

Japan continues to sustain a sophisticated, effervescent supplement market, driven by an aging population and a strong preventive healthcare culture, while South Korea is projected to expand its effervescent packaging demand at approximately 6.5% CAGR. Sanner GmbH’s 2023 expansion in Kunshan reflects rising demand, while the growth of contract packaging organizations across Southeast Asia enables cost-efficient, localized supply for global and regional brands.

Competitive Landscape

The global effervescent packaging market is characterized by a moderately consolidated competitive landscape, with the top five companies, Sanner GmbH, Amcor plc, Berry Global Group, Huhtamaki Oyj, and Gerresheimer AG, collectively accounting for an estimated 55% of global revenue. Market leaders distinguish themselves through advanced moisture-management technologies, integrated CDMO capabilities, and sustainability-focused material innovation. Consolidation remains a key strategic trend, evidenced by Amcor’s acquisition of Berry Global’s pharmaceutical packaging assets in 2024 and Sanner GmbH’s acquisition of Gilero LLC the same year. Meanwhile, cost-competitive manufacturers in India and Southeast Asia are steadily expanding their presence within the mid-tier segment, while European incumbents retain leadership in premium, regulated packaging categories.

Key Developments:

- July 2025: Sanner, a global leader in high-quality healthcare packaging and drug delivery solutions, officially opened its first U.S.-based production facility in Greensboro, North Carolina, just weeks after commencing initial operations.

- April 2025: Amcor plc announced the successful completion of its all-stock combination with Berry Global. Through this combination, Amcor enhances its position as a global leader in consumer and healthcare packaging solutions with the unique material science and innovation capabilities required to revolutionize product development and meet customers’ and consumers’ sustainability aspirations.

- April 2025: Gerresheimer progressed the acquisition of Italy's Bormioli Pharma, boosting its European glass pharmaceutical packaging footprint. Concurrently, under investor pressure, Gerresheimer announced the divestiture of its moulded glass lateral business (cosmetics/beverage), explicitly concentrating resources on higher-growth pharmaceutical and healthcare packaging segments.

Top Companies in the Effervescent Packaging Market

Sanner GmbH (Bensheim, Germany) is the undisputed global market leader in effervescent tablet packaging, credited with inventing the world’s first desiccant closure (DASG) for effervescent tablets in the 1960s. Operating across six global manufacturing facilities, including sites in Germany, the USA, China, France, Hungary, and India, with a comprehensive portfolio of desiccant closures (DASG, DOSG), bio-based BioBase® tubes, child-resistant TabTec® CR packaging, and in-mold labelled Brilliance Tube formats, Sanner serves pharmaceutical, nutraceutical, and personal care clients across more than 50 countries.

Amcor plc (Zurich, Switzerland) ranks among the world’s largest diversified packaging companies, offering a comprehensive effervescent packaging portfolio spanning pharmaceutical blister foils, flexible multi-layer laminates, and rigid primary containers. The company’s 2024 consolidation of Berry Global's pharmaceutical packaging assets significantly extended its manufacturing capacity and global geographic footprint, reinforcing its position as a preferred strategic packaging partner for multinational pharmaceutical and consumer health brands.

Gerresheimer AG (Düsseldorf, Germany) specializes in high-quality glass and engineered plastic primary packaging for the pharmaceutical and healthcare industries, with a well-established range of precision containers, closures, and vials for effervescent tablet and powder applications. The company’s strong FDA and EMA regulatory credentials, combined with its deep expertise in sterile and specialty pharmaceutical packaging, position it as a premium-tier supplier and strategic long-term partner for global pharmaceutical manufacturers.

Companies Covered in Effervescent Packaging Market

- Sanner GmbH

- Amcor plc

- Berry Global Group

- Huhtamaki Oyj

- Gerresheimer AG

- Aptar CSP Technologies

- Romaco Pharmatechnik GmbH

- Constantia Flexibles

- Mondi Group

- ACG Group

- CCL Industries Inc.

- Winpak Ltd.

- Alpla Group

Frequently Asked Questions

The global Effervescent Packaging Market is valued at US$ 631.4 Mn in 2026 and is projected to reach US$ 974.8 Mn by 2033, expanding at a CAGR of 6.4% over the forecast period, driven by growing pharmaceutical industry demand, rising nutraceutical consumption, and accelerating adoption of convenient effervescent dosage forms globally.

Growth is primarily driven by the expanding global pharmaceutical and OTC medication market, the rapid rise of the dietary supplement and nutraceutical industry, increasing consumer preference for fast-dissolving and convenient effervescent dosage forms, and accelerating health-and-wellness spending across emerging economies in Asia-Pacific and Latin America.

Tablets represent the leading product type segment, accounting for approximately 40% of global market share, owing to their widespread adoption across pharmaceutical and nutraceutical applications, clinically documented superior bioavailability, and broad consumer acceptance, particularly among geriatric and pediatric populations who benefit most from their dissolution format.

North America leads the global Effervescent Packaging Market, holding approximately 38% of global revenue, supported by a mature pharmaceutical and nutraceutical industry, high OTC supplement consumption, FDA packaging regulatory requirements that sustain premium packaging adoption, and the presence of leading packaging technology innovators such as Aptar CSP Technologies.

The most significant opportunities include the transition to sustainable packaging solutions, mandated by the EU’s Packaging and Packaging Waste Regulation (PPWR) by 2030, and the rapid expansion of the Asia-Pacific market, projected to grow at approximately 9.2% CAGR, driven by pharmaceutical manufacturing investment and rising healthcare expenditure in China, India, and ASEAN economies.

The leading companies in the global Effervescent Packaging Market include Sanner GmbH, Amcor plc, Gerresheimer AG, Berry Global Group, Huhtamaki Oyj, Aptar CSP Technologies, Romaco Pharmatechnik GmbH, Constantia Flexibles, Mondi Group, and ACG Group, among others, operating across the global pharmaceutical, nutraceutical, and personal care packaging supply chains.