- LED & Lighting (Optoelectronics)

- Desiccant Dehumidifier Market

Desiccant Dehumidifier Market Size, Share, and Growth Forecast 2026 - 2033

Desiccant Dehumidifier Market by Product Type (Fixed/Mounted, Portable), Application (Energy, Chemical, Construction, Electronics, Food and Pharmaceuticals, Academic and Research), by Regional Analysis, 2026 - 2033

Desiccant Dehumidifier Market Size and Trend Analysis

The global desiccant dehumidifier market size is expected to be valued at US$ 612.4 million in 2026 and projected to reach US$ 939.2 million by 2033, growing at a CAGR of 6.3% between 2026 and 2033.

This robust growth is principally driven by intensifying industrial demand for precise humidity control across high-sensitivity sectors, including pharmaceuticals, electronics manufacturing, food processing, and energy infrastructure.

Unlike conventional refrigerant-based dehumidifiers, desiccant systems offer superior moisture removal performance at low temperatures and in extremely low humidity conditions, making them indispensable in critical industrial environments. Expanding industrial output in the Asia Pacific, stringent regulatory mandates for controlled storage environments in the pharmaceutical and food sectors, and growing construction activity in humid climate regions collectively underpin the market’s sustained upward momentum through the forecast period.

Key Industry Highlights

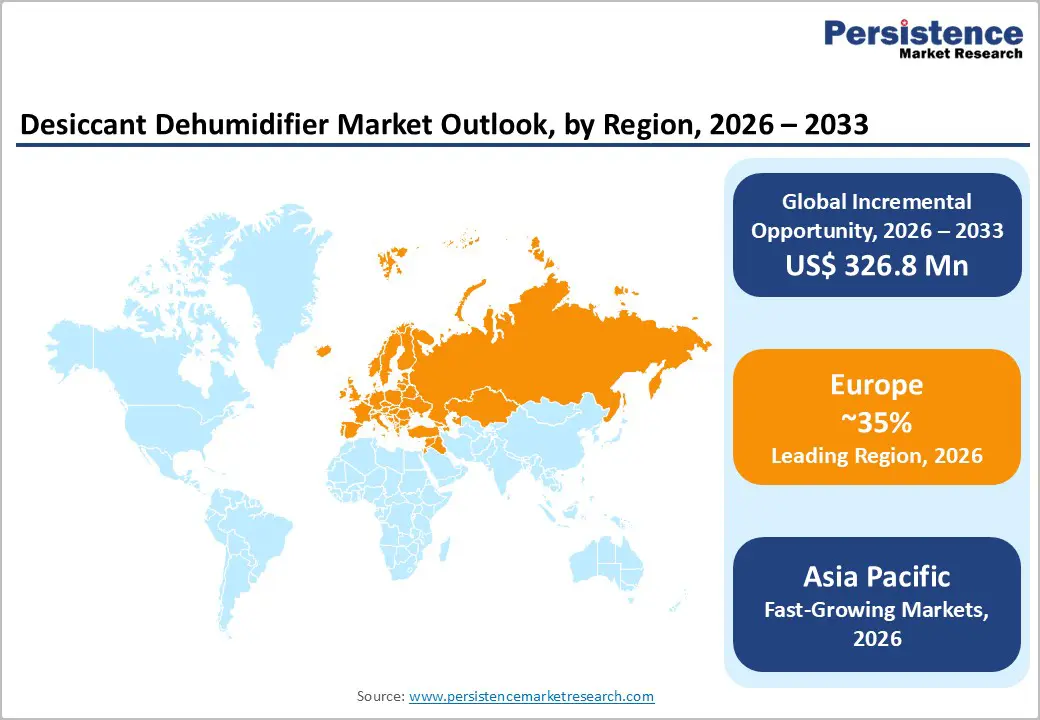

- Leading Region: North America leads the global desiccant dehumidifier market with approximately 35% revenue share in 2025, underpinned by robust pharmaceutical, semiconductor, and food processing industries, and accelerated by landmark government investments, including the U.S. CHIPS Act and Inflation Reduction Act 2022.

- Fastest Growing Regional Market: Asia Pacific is the fastest growing regional market for 2026-2033, driven by semiconductor facility expansion across China, Japan, and South Korea, India’s pharmaceutical manufacturing boom under the PLI scheme, and high-humidity construction markets across Southeast Asia.

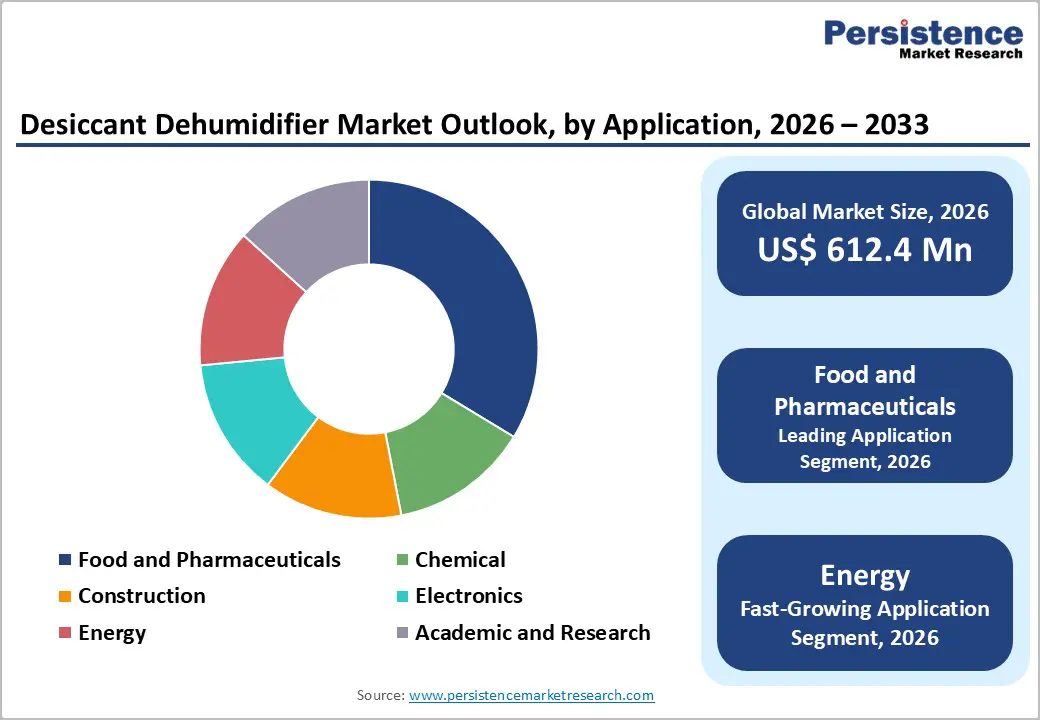

- Dominant Segment: The Food and Pharmaceuticals application segment dominates with approximately 30% market share in 2025, anchored by non-discretionary regulatory mandates from the FDA, EMA, and WHO that specify controlled humidity environments across pharmaceutical and food processing operations globally.

- Fastest Growing Segment: The Energy application segment is the fastest growing category, propelled by explosive lithium-ion battery gigafactory construction globally, where desiccant dry-room systems achieving dew points below -40°C are the only technically viable humidity control solution for cell manufacturing.

- Key Opportunity: The global transition to electric vehicles and grid-scale energy storage, with the IEA projecting global EV sales of 45 million units by 2030 and gigafactory capacity exceeding 9,000 GWh, represents the single most significant demand opportunity for desiccant dehumidifier manufacturers in the coming decade.

| Key Insights | Details |

|---|---|

| Desiccant Dehumidifier Market Size (2026E) | US$ 612.4 Million |

| Market Value Forecast (2033F) | US$ 939.2 Million |

| Projected Growth CAGR (2026 - 2033) | 6.3% |

| Historical Market Growth (2020 - 2025) | 5.8% |

Market Dynamics

Driver - Stringent Pharmaceutical and Food Storage Regulations Mandating Precision Humidity Control

Regulatory requirements governing humidity control in pharmaceutical manufacturing, storage, and logistics environments represent one of the most powerful and non-discretionary demand drivers for desiccant dehumidifiers globally. The U.S. Food and Drug Administration (FDA) mandates strict adherence to Good Manufacturing Practice (GMP) guidelines that specify controlled temperature and humidity conditions for drug production and storage facilities, conditions that only desiccant-based systems can reliably achieve at the low dew points required. Similarly, the European Medicines Agency (EMA) enforces EU GMP guidelines (EudraLex Volume 4) that mandate environmental controls in pharmaceutical facilities. In the food industry, the Codex Alimentarius Commission, jointly administered by the WHO and FAO, establishes humidity control benchmarks for food safety. With global pharmaceutical production volumes expanding rapidly and food safety regulations tightening in emerging markets, the demand for reliable desiccant dehumidification systems in these sectors is structurally assured throughout the forecast horizon.

Expanding Electronics Manufacturing and Semiconductor Industry Driving Low-Humidity Environment Demand

The global semiconductor and electronics manufacturing industry’s rapid expansion is generating significant and growing demand for ultra-low humidity environments where desiccant dehumidifiers are the only viable humidity control technology. Semiconductor fabrication processes, including wafer handling, lithography, and component assembly, require relative humidity levels as low as 1-5% RH, conditions that refrigerant-based dehumidifiers are physically incapable of achieving. The Semiconductor Industry Association (SIA) reported global semiconductor sales of US$ 526.8 billion in 2023, with continued capacity expansion announced across the United States, Europe, South Korea, Taiwan, and Japan driven by government-backed semiconductor self-sufficiency initiatives. The U.S. CHIPS and Science Act (2022), which allocated US$ 52.7 billion for domestic semiconductor manufacturing, and the EU Chips Act, targeting 20% of global chip production by 2030, are driving new fabrication plant construction, each representing a large-scale procurement opportunity for desiccant dehumidification systems.

Restraints - High Energy Consumption of Desiccant Dehumidifiers Relative to Refrigerant Alternatives

A significant technical limitation constraining broader adoption of desiccant dehumidifiers is their comparatively high energy consumption, particularly the thermal energy required to regenerate the desiccant rotor or bed. Desiccant systems typically consume 20-40% more energy than equivalent-capacity refrigerant dehumidifiers in moderate humidity and temperature conditions, according to assessments published by the American Society of Heating, Refrigerating and Air-Conditioning Engineers (ASHRAE). In an era of rising energy costs and increasing corporate focus on energy efficiency and carbon footprint reduction, this energy intensity creates a genuine procurement disincentive, especially for facilities where operational conditions do not specifically mandate desiccant performance, limiting the technology’s competitive positioning against improving refrigerant-based systems.

High Initial Capital Costs Limiting Penetration in Price-Sensitive End-Use Segments

Desiccant dehumidifiers, particularly industrial fixed/mounted systems equipped with silica gel or molecular sieve rotors, carry substantially higher upfront capital costs compared to refrigerant-based counterparts of equivalent capacity. Industrial-grade desiccant units can cost two to four times more than comparable refrigerant dehumidifiers, creating a meaningful adoption barrier in capital-constrained end-use segments, particularly SME-operated construction, warehousing, and mid-tier manufacturing facilities. The World Bank’s data indicating that access to industrial equipment financing remains constrained across much of South Asia, Sub-Saharan Africa, and parts of Latin America further compounds this challenge, restricting desiccant dehumidifier penetration in high-potential but price-sensitive developing markets.

Opportunity - Rapid Growth of Lithium-Ion Battery Manufacturing Creating Specialized Dry-Room Demand

The global transition to electric vehicles (EVs) and grid-scale energy storage is generating an unprecedented demand surge for lithium-ion battery manufacturing capacity, and with it, a critical and specialized requirement for desiccant dehumidification in dry-room environments. Lithium-ion battery cell manufacturing requires humidity levels of less than 1% RH (dew points as low as -40°C to -60°C) throughout electrode preparation, cell assembly, and electrolyte filling processes, making desiccant dehumidifiers the only technically viable humidity control solution. The International Energy Agency (IEA) projects that global EV sales will reach 45 million units by 2030, with battery gigafactory capacity expected to exceed 9,000 GWh globally by the same year. Announced gigafactory investments by Panasonic, CATL, LG Energy Solution, Samsung SDI, and numerous government-backed new entrants across North America, Europe, and Asia Pacific represent hundreds of billions of dollars in facility investment, each requiring industrial-scale desiccant dry-room systems, presenting a generational demand opportunity for desiccant dehumidifier manufacturers.

Construction Sector Expansion and Moisture-Damage Prevention in Humid Climate Markets

The global construction industry’s sustained expansion, particularly in tropical and high-humidity regions across Asia Pacific, the Middle East, and Latin America, is emerging as a high-growth application opportunity for portable and temporary desiccant dehumidifiers used in construction moisture management. Moisture control during building construction is critical to preventing concrete carbonation, reinforcement corrosion, mold growth, and coating adhesion failures, problems that carry significant structural and financial consequences. The Global Construction Perspectives and Oxford Economics research estimates that global construction output will grow by 42% to reach US$ 15.2 trillion by 2030, with the strongest growth projected in Asia Pacific, the Middle East, and Africa. Regulatory frameworks such as the UK Building Regulations (Approved Document C) and equivalent standards in the EU mandate moisture control in building envelopes, creating specification-driven demand for temporary desiccant dehumidification equipment during construction and fit-out phases, a market that is still significantly underpenetrated in many developing geographies.

Category-wise Analysis

Product Type Insights

Fixed and mounted desiccant dehumidifiers represent the dominant product type segment, accounting for approximately 65% of total market share in 2025. Their market leadership is rooted in the high-volume deployment of permanently installed desiccant systems across industrial facilities, including pharmaceutical manufacturing plants, semiconductor fabrication facilities, lithium-ion battery dry rooms, chemical processing plants, and large-scale food storage warehouses, where continuous, uninterrupted humidity control is a non-negotiable operational requirement. Fixed systems offer higher capacity ranges, greater operational efficiency at sustained throughput, and compatibility with central HVAC integration, making them the preferred choice for critical process environments. Leading suppliers including Munters, Bry Air, and Seibu Giken DST generate the majority of their industrial revenue from fixed and mounted system configurations. The fastest growing segment is Portable desiccant dehumidifiers, driven by construction site moisture management applications and the expanding rental equipment market in developing economies.

Application Insights

The food and pharmaceuticals segment leads the application category for desiccant dehumidifiers, holding an estimated 30% market share in 2025. This dominance is structurally anchored in the mandatory, regulatory-driven nature of humidity control in both sectors, unlike discretionary investments in other industrial applications. FDA GMP guidelines, EMA EU GMP (EudraLex Volume 4) requirements, and WHO Good Storage and Distribution Practices collectively mandate strict environmental control parameters in pharmaceutical manufacturing, packaging, and storage facilities across global supply chains. In the food sector, Codex Alimentarius standards and national food safety regulations from bodies such as the European Food Safety Authority (EFSA) and the U.S. FDA Food Safety Modernization Act (FSMA) specify humidity-controlled environments for food processing, ingredient storage, and packaging operations. The fastest growing application segment is Energy, specifically driven by lithium-ion battery gigafactory dry-room demand and the expanding renewable energy infrastructure buildout.

Regional Insights

North America Desiccant Dehumidifier Market Trends and Insights

North America holds the leading position in the global desiccant dehumidifier market, accounting for approximately 35% of total revenue share in 2025. The United States is the primary regional driver, benefiting from a highly developed pharmaceutical manufacturing base, world-class semiconductor fabrication facilities, and a robust food processing industry, all of which are significant end-users of industrial desiccant dehumidification systems. The U.S. CHIPS and Science Act (2022), with its US$ 52.7 billion allocation for domestic semiconductor manufacturing expansion, has catalyzed the construction of new fabrication plants by Intel, TSMC, Samsung, and Micron, each representing major procurement events for desiccant dry-room systems. Additionally, the U.S. Inflation Reduction Act (IRA, 2022), which provides substantial incentives for domestic battery manufacturing, is accelerating gigafactory construction across the country, further amplifying desiccant dehumidifier demand.

The region also benefits from a proactive regulatory ecosystem: FDA and OSHA environmental control mandates consistently drive capital investment in precision humidity management across pharmaceutical, food processing, and electronics manufacturing facilities. Companies including Bry Air and Munters maintain strong North American commercial and service presences, while ASHRAE standard-setting activities continue to shape industry best practices in humidity control, reinforcing the region’s technological leadership in desiccant dehumidification system design and application.

Europe Desiccant Dehumidifier Market Trends and Insights

Europe is the second-largest regional market for desiccant dehumidifiers, with Germany, the United Kingdom, Sweden, and the Netherlands being the key contributing economies. Germany’s strength in chemical processing, pharmaceutical manufacturing, and industrial automation drives consistent procurement of high-performance fixed desiccant systems, with local companies including Trotec Laser GmbH and DEHUTECH AB (headquartered in Sweden) serving regional industrial demand. The European Medicines Agency (EMA) regulatory framework mandating GMP-compliant humidity control in pharmaceutical facilities is a non-discretionary procurement driver across the continent. The EU Chips Act, targeting 20% of global semiconductor production by 2030, is further stimulating new cleanroom and fabrication facility construction across Germany, the Netherlands, and France, each requiring industrial desiccant dehumidification infrastructure.

The EU Green Deal and associated energy efficiency directives, including the Energy Performance of Buildings Directive (EPBD) revision, are simultaneously driving innovation demand for energy-efficient desiccant systems incorporating heat recovery and low-regeneration-temperature desiccant materials. The UK Building Regulations and CIBSE (Chartered Institution of Building Services Engineers) guidance on moisture control in buildings continue to drive the specification of temporary desiccant dehumidification during construction, reinforcing demand in the construction application segment across Britain and Northern Europe.

Asia Pacific Desiccant Dehumidifier Market Trends and Insights

Asia Pacific is the fastest growing regional market for desiccant dehumidifiers, projected to record the highest regional CAGR during the forecast period. The region’s growth is fueled by simultaneous expansion across multiple high-value end-use sectors: semiconductor and electronics manufacturing in China, South Korea, Taiwan, and Japan; pharmaceutical production scale-up in India and China; lithium-ion battery gigafactory construction across the region; and rapid construction activity in tropical, high-humidity markets throughout Southeast Asia. China dominates regional volume demand as both a manufacturing hub and a massive domestic consumer of industrial humidity control equipment. The Ministry of Industry and Information Technology (MIIT) of China has set ambitious targets for domestic semiconductor self-sufficiency, driving new cleanroom facility investments that require desiccant dry-room systems.

India represents the region’s most rapidly emerging market opportunity, propelled by the government’s Production Linked Incentive (PLI) scheme for Pharmaceuticals and the Semicon India Programme, both of which are drawing significant manufacturing investment requiring controlled humidity environments. The Japan Electronics and Information Technology Industries Association (JEITA) consistently reports strong output growth in Japan’s semiconductor and electronic components sectors, sustaining robust demand for desiccant dehumidification in manufacturing environments. Across ASEAN markets, particularly Vietnam, Thailand, and Malaysia, rapid growth in electronics manufacturing FDI and food processing capacity expansion are creating new demand pockets for both fixed industrial and portable construction-grade desiccant dehumidifiers.

Competitive Landscape

The global desiccant dehumidifier market demonstrates a moderately consolidated structure, characterized by a core group of technology-driven manufacturers supported by regional suppliers and niche engineering firms. Competition is primarily technology-centric, with differentiation anchored in proprietary desiccant rotor performance, ultra-low dew point capability, energy efficiency, and application-specific system design. Established players leverage extensive service networks, turnkey project execution capabilities, and long-term maintenance contracts to strengthen customer retention across pharmaceutical, semiconductor, food processing, and energy sectors.

Strategically, companies are prioritizing R&D investments in advanced desiccant materials, low-energy regeneration systems, and IoT-enabled remote monitoring with predictive maintenance functionality. Geographic expansion into high-growth Asia Pacific markets and participation in lithium-ion battery gigafactory dry-room projects are key growth levers. Emerging entrants are focusing on specialized dry-room engineering and sustainable, low-carbon solutions to carve out differentiated positions within high-value industrial segments.

Key Developments:

- November, 2025: Bry Air launches the P80X dehumidifier based on MOF (Metal-Organic Framework) technology, positioned as an advanced humidity control solution tailored for pharmaceutical manufacturing environments.

- April, 2025: Modine expands its commercial indoor air quality portfolio by acquiring Climate by Design International, enhancing its offerings in climate control and air quality solutions.

- May, 2023: Mayekawa develops a desiccant dehumidifier that uses a CO2 heat pump system, offering enhanced energy efficiency and sustainable humidity control for industrial applications.

Companies Covered in Desiccant Dehumidifier Market

- Bry Air

- Munters

- Condair Group

- Cotes

- Seibu Giken DST

- Trotec Laser GmbH

- DEHUTECH AB

- Fisen Corporation

- Kaeser Kompressoren

- Atlas Copco AB

- Desiccant Technologies Group (DTG)

- Compu-Aire Inc.

- Stulz GmbH

- Des-Case Corporation

- Humi-Dry (HiDew)

- Mayekawa

- Modine

Frequently Asked Questions

The market is projected to reach US$ 612.4 million in 2026, driven by pharmaceutical compliance, semiconductor expansion, and lithium-ion battery gigafactory demand.

Growth is fueled by strict humidity regulations in pharma and food, semiconductor fab expansion, and rapid EV battery manufacturing capacity buildout.

North America leads due to strong pharmaceutical, semiconductor, and battery manufacturing investments supported by federal incentives.

Opportunities lie in ultra-low dew point dry rooms for battery gigafactories and expanding construction activity in high-humidity emerging markets.

The global desiccant dehumidifier market features Munters, Bry Air, Condair Group, Seibu Giken DST, Cotes, Atlas Copco AB, Kaeser Kompressoren, Trotec Laser GmbH, DEHUTECH AB, Fisen Corporation, Stulz GmbH, and Desiccant Technologies Group, among others.