- Medical Devices

- Dental Abutment Market

Dental Abutment Market Size, Share, and Growth Forecast 2026 - 2033

Dental Abutment Market by Product Type (Prefabricated, Customized), by Material (Titanium, Zirconium, Others), by End Use (Solo Practices, DSO/Group Practices, Others), by Regional Analysis, 2026 - 2033

Dental Abutment Market Size and Trend Analysis

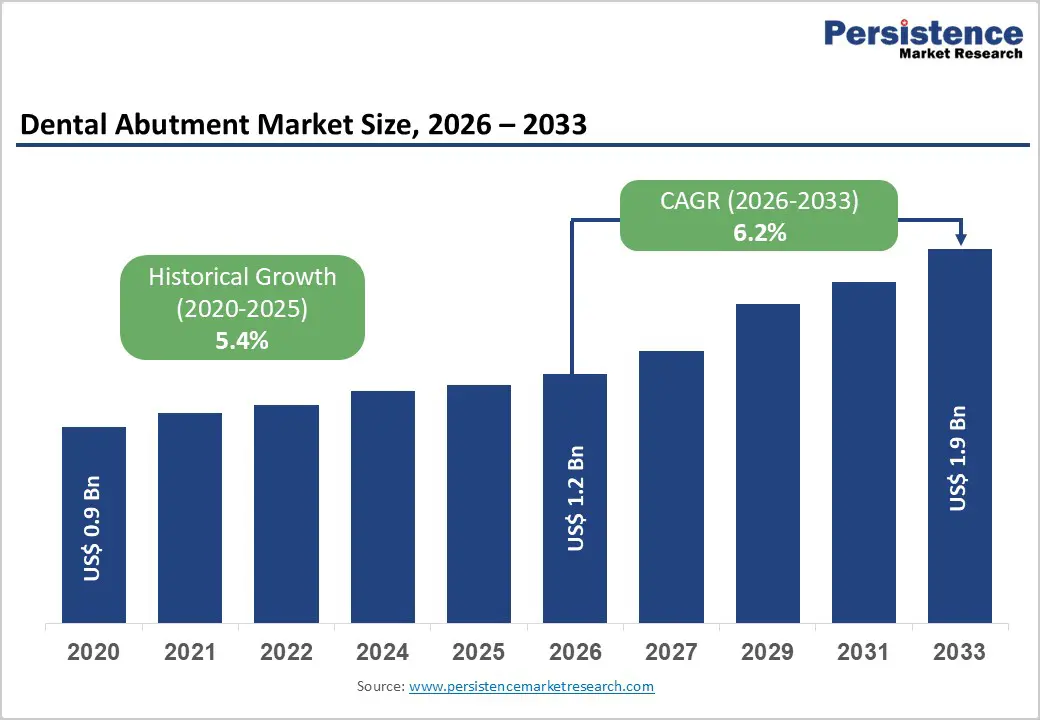

The global dental abutment market size is expected to be valued at US$ 1.2 billion in 2026 and projected to reach US$ 1.9 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033.

Rising adoption of implant-supported restorations for partially and fully edentulous patients, combined with an ageing global population, is accelerating demand for durable, aesthetic abutment solutions. Clinicians are increasingly shifting from conventional removable prostheses to implant-based options as edentulism remains highly prevalent, with hundreds of millions of adults affected worldwide, while technological advances in digital workflows, CAD/CAM customization, and high-performance materials such as titanium and zirconia are enhancing clinical outcomes and driving procedure volumes.

Key Indystry Highlights

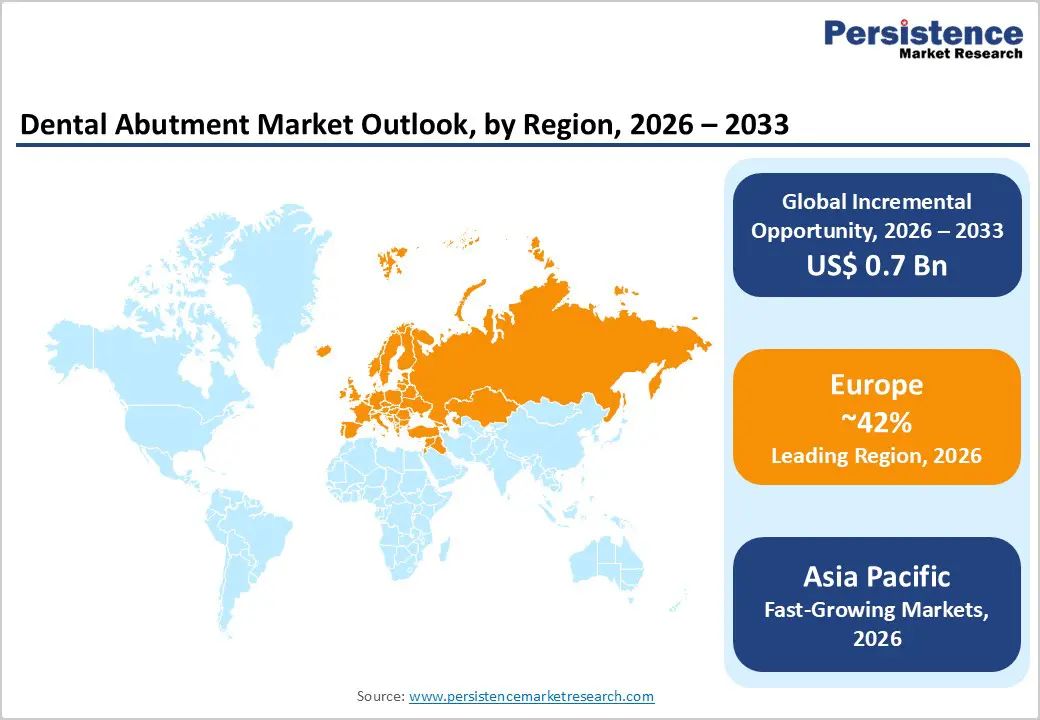

- Europe leads the dental abutment market, supported by strong healthcare infrastructure, favorable reimbursement systems, and high adoption of implant dentistry across major countries.

- Asia Pacific is the fastest-growing region, driven by rising dental tourism, improving healthcare infrastructure, increasing disposable income, and expanding access to advanced dental treatments.

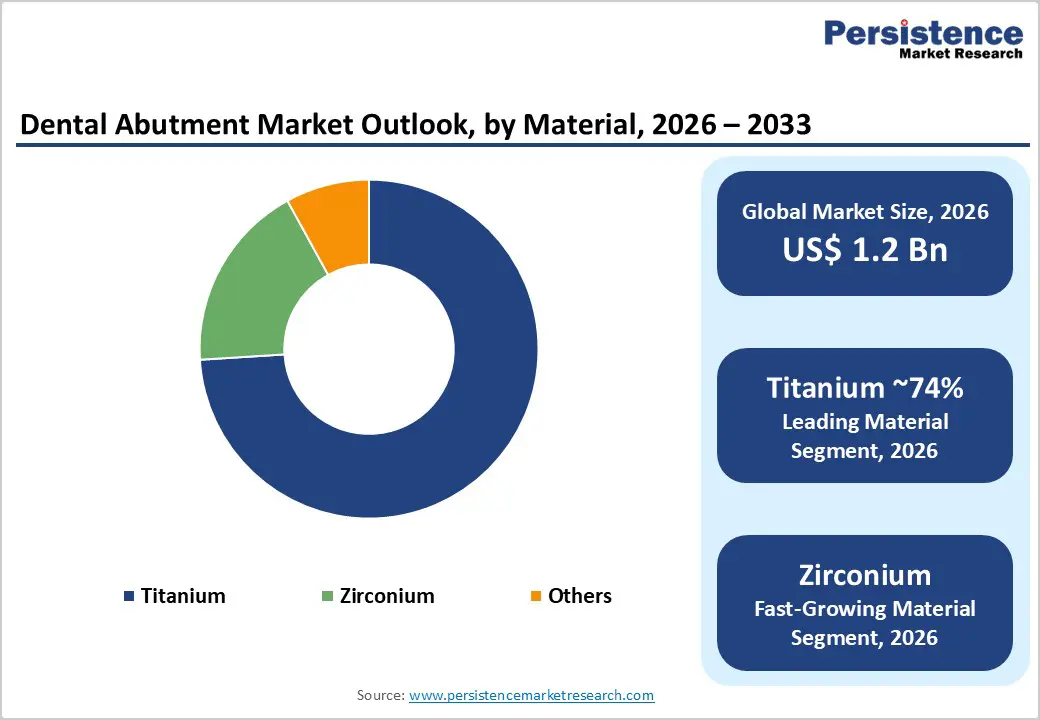

- Titanium dominates the material segment due to its superior strength, durability, corrosion resistance, and proven long-term clinical success in implant-supported dental restorations globally.

- Zirconia is the fastest-growing material segment, driven by increasing demand for aesthetic dentistry, biocompatibility, and preference for natural-looking tooth-colored dental restorations among patients.

- Growing adoption of digital dentistry technologies, including CAD/CAM systems and 3D printing, creates significant opportunities for customized, precise, and efficient dental abutment solutions.

| Global Market Attributes | Key Insights |

|---|---|

| Dental Abutment Market Size (2026E) | US$ 1.2 billion |

| Market Value Forecast (2033F) | US$ 1.9 billion |

| Projected Growth CAGR (2026 - 2033) | 6.2% |

| Historical Market Growth (2020 - 2025) | 5.4% |

Market Dynamics

Drivers - Rising Burden of Edentulism and Ageing Population

The dental abutment market benefits directly from the persistent global burden of edentulism and the rapid expansion of the older population segment, who are the primary candidates for implant-supported prostheses. Recent global analyses estimate tens of millions of older adults living with complete tooth loss and indicate that edentulism-related disability-adjusted life years remain high despite improvements in preventive dentistry. In parallel, the World Health Organization (WHO) projects that people aged 60 years and above will increase from about 1 billion in 2020 to 1.4 billion by 2030, and to around 2.1 billion by 2050, representing a rapidly expanding pool of patients needing fixed oral rehabilitation. As tooth loss strongly correlates with age and cumulative periodontal and caries experience, this demographic shift structurally increases demand for implant fixtures and the associated abutments that enable stable, functional, and aesthetic restorations.

Growing Adoption of Dental Implants and Preference for Fixed, Aesthetic Solutions

Another key growth driver is the steady rise in implant placement rates and the preference for fixed restorations that closely mimic natural dentition, especially in developed markets such as the U.S. and Western Europe. In the U.S. alone, estimates suggest that more than 3 million people already have dental implants and around 500,000 new implants are placed each year, highlighting a robust and expanding procedure base that directly translates into abutment demand. European data further show strong penetration in countries like Germany, where implant usage per 10,000 inhabitants is among the highest globally, reflecting mature clinical adoption and patient awareness. As patients increasingly seek long-lasting, highly aesthetic, and minimally invasive treatment options, abutments engineered for optimal emergence profiles, soft-tissue support, and compatibility with digital restorative workflows become central components in modern implant dentistry, sustaining market growth.

Restraints - High Treatment Costs and Limited Reimbursement Coverage

The relatively high total cost of implant-abutment restorations compared with conventional dentures or fixed bridges remains a major barrier, particularly in price-sensitive markets and among lower-income patient segments. Analyses of European implant markets indicate that limited reimbursement for implant therapy in many public insurance systems forces patients to pay largely out of pocket, constraining uptake despite clear functional and quality-of-life benefits. Similar affordability challenges are reported in emerging economies, where growing middle classes drive demand, but income disparities and lack of comprehensive dental coverage slow the transition from removable to implant-based solutions, thereby tempering abutment market expansion.

Clinical Complications, Peri-Implant Disease, and Mechanical Risks

Although implant and abutment technologies have advanced significantly, concerns about biological and mechanical complications continue to restrain faster adoption and influence material and design choices. Clinical studies comparing titanium and zirconia abutments report overall high survival rates but also highlight issues such as marginal bone loss, soft-tissue inflammation, and occasional abutment or screw fractures, particularly under high occlusal load or when design and torque protocols are not optimally followed. The need for rigorous long-term data on newer customized and ceramic abutment concepts, combined with practitioner caution in high-risk patients with periodontitis, smoking, or systemic diseases, can delay wider diffusion of innovative abutment systems and keep some clinicians reliant on familiar, proven solutions, slightly moderating market growth.

Opportunities - Shift Toward Zirconia and Customized Abutments for Superior Aesthetics and Tissue Integration

There is a significant opportunity in the accelerating transition from purely stock titanium designs to zirconia and digitally customized abutments tailored to individual soft-tissue profiles and aesthetic needs. Systematic reviews show that zirconia abutments can provide favorable soft-tissue responses and reduced bleeding on probing, while maintaining high survival rates comparable to titanium over several years of follow-up, especially in anterior regions where aesthetics is critical. Randomized clinical trials on customized healing and definitive abutments indicate improved pink esthetic scores, better preservation of peri-implant soft tissue volume, and lower patient-reported discomfort compared with prefabricated options, supporting broader clinical uptake of CAD/CAM and 3D-printed abutment workflows. As laboratories and manufacturers integrate advanced digital design platforms and chairside scanning, companies that offer comprehensive customized zirconia and titanium abutment portfolios, validated by robust clinical evidence, are well positioned to capture this premium, fast-growing segment.

Expansion of DSO/Group Practices and Digital Workflows in High-Growth Regions

The rapid proliferation of dental service organizations (DSOs) and large group practices, particularly in North America and increasingly in Europe and Asia, creates strong volume and standardization opportunities for abutment suppliers. Data from the American Dental Association (ADA) Health Policy Institute indicate that the share of dentists in solo practice has been steadily declining, while the proportion working in large, multi-location groups and DSOs continues to rise, with DSO affiliation in the U.S. nearly doubling over the past decade. These corporatized settings typically favor standardized implant and abutment platforms, negotiated purchasing contracts, and integrated digital workflows from surgical planning to final prosthetics, which can significantly increase unit throughput per site. In emerging Asia-Pacific markets, where implant volumes in countries such as China and India are growing at high single- to double-digit rates, group clinics and chain operators are adopting guided surgery kits and digital restorative systems, offering abutment manufacturers a scalable channel to penetrate large patient bases and accelerate adoption of advanced prosthetic solutions.

Category-wise Insights

Product Type Analysis

Within product types, prefabricated abutments are estimated to remain the leading segment, accounting for roughly 65% of global dental abutment usage in 2025, supported by their wide availability, standardized interfaces, and lower unit costs relative to fully customized alternatives. Prefabricated titanium abutments have been shown to provide strong mechanical performance, with comparative studies reporting higher fracture and fatigue strength versus customized counterparts under standardized loading conditions, reinforcing clinician confidence in routine posterior and multi-unit cases. At the same time, improvements in emergence profiles, angulation options, and compatibility with guided surgery kits allow stock abutments to be integrated into many digital workflows, further cementing their role as workhorse solutions in both solo practices and DSOs. While customized abutments are rapidly gaining ground in aesthetic zones, the cost-effectiveness and reliability of prefabricated systems ensure they retain the dominant share of clinical indications in the medium term.

End Use Analysis

In terms of end use, solo practices are expected to remain the leading segment in 2025, accounting for an estimated majority share of global dental abutment procedures despite the accelerating shift toward DSOs and group practices. Historical data from the ADA Health Policy Institute show that although the percentage of US dentists in solo practice has declined from about 65% in 1999 to roughly 35-36% in 2023, solo-owned practices still represent the single largest practice model and perform a substantial volume of restorative and implant services. In many countries across Europe, Latin America, and Asia, independent clinics continue to dominate the delivery of implant dentistry, particularly in suburban and rural areas where corporate dental chains have yet to achieve strong penetration. Solo practitioners often favor versatile implant-abutment platforms and reliable support from manufacturers, driving steady baseline demand, while DSOs and group practices, though smaller in count, are emerging as the fastest-growing end-use customers due to their scale and aggressive expansion strategies.

Regional Insights

North America Dental Abutment Market Trends and Insights

North America, led by the U.S., represents one of the most advanced and innovation-driven markets for dental implants and abutments, supported by high healthcare spending, strong patient awareness, and a dense network of specialist clinicians. The region benefits from widespread access to advanced dental technologies and a high acceptance of implant-based restorative procedures. Estimates indicate that the U.S. alone performs around 500,000 implant placements annually, with more than 3 million people currently living with implants, creating a large and recurring demand pool for abutments used in both initial restorations and long-term replacements.

A key trend shaping the market is the rapid adoption of digital dentistry, including CAD/CAM-based customized abutments and guided implant surgery, which enhance precision and patient outcomes. The growing aging population and rising demand for aesthetic dental solutions are further accelerating market growth. Additionally, the strong presence of leading manufacturers and continuous product innovation in materials such as titanium and zirconia are reinforcing North America’s position as a mature, high-value market with steady technological advancements and sustained demand.

Europe Dental Abutment Market Trends and Insights

Europe is estimated to dominate the global market with approximately 42% share in 2026, supported by advanced healthcare infrastructure, strong regulatory frameworks, and high adoption of implant dentistry. Countries such as Germany, the UK, France, Italy, and Spain dominate regional demand due to well-established dental care systems and skilled professionals. The region shows a strong preference for aesthetic and customized abutments, particularly zirconia-based solutions, driven by increasing demand for cosmetic dentistry and patient-specific restorations. Additionally, favorable reimbursement policies and rising private dental expenditure have increased implant procedure volumes, particularly in Western Europe.

A key trend shaping the market is the rapid adoption of digital dentistry technologies, including CAD/CAM systems and 3D-guided implant planning, enabling high precision and reduced treatment time. Over 60% of dental practices in Western Europe are already utilizing customized abutments, reflecting a shift toward personalized treatment solutions. The growing geriatric population and rising prevalence of tooth loss further support demand for implant-based restorations. Moreover, continuous product innovation and strong presence of leading manufacturers strengthen Europe’s position as a mature yet innovation-driven market with steady long-term growth.

Asia Pacific Dental Abutment Market Trends and Insights

Asia Pacific is the fastest-growing region in the dental abutment market, driven by rapid urbanization, increasing disposable income, and expanding healthcare infrastructure. Countries such as China, India, Japan, and South Korea are key growth engines due to rising awareness of oral health and increasing adoption of implant-based restorations. The region is also a global hub for dental tourism, attracting patients seeking cost-effective treatments, which significantly boosts procedure volumes. Additionally, government initiatives to improve healthcare access and modernization of dental facilities are accelerating market expansion across both urban and semi-urban areas.

Technological advancements are playing a crucial role, with increasing adoption of CAD/CAM-based custom abutments, digital workflows, and 3D printing technologies across dental clinics. Nearly 57% of clinics in the region have introduced implant restoration services, reflecting strong penetration potential. The large patient pool, growing middle-class population, and improving affordability further enhance demand. Additionally, strategic collaborations and manufacturing expansions by global and regional players are strengthening supply chains and innovation capabilities. Overall, Asia Pacific offers high-growth opportunities, supported by evolving patient preferences, expanding dental infrastructure, and rising investment in advanced implant technologies.

Companies Covered in Dental Abutment Market

- Institut Straumann AG

- Dentsply Sirona

- ZimVie Inc.

- Zest Dental Solutions

- ALLIANCE GLOBAL TECHNOLOGY

- Ziacom

- BioHorizons

- Cortex

- Dentium

- Others

Frequently Asked Questions

The dental abutment market is projected to reach approximately US$ 1.2 billion in 2026, driven by increasing implant procedures and oral healthcare demand.

Rising dental implant procedures and growing adoption of digital dentistry technologies are key drivers supporting demand for advanced and customized abutment solutions globally.

Europe dominates the dental abutment market with approximately 42% share, supported by strong healthcare infrastructure, reimbursement policies, and high implant adoption rates.

Key opportunities include rising demand for zirconia-based customized abutments and expansion of dental tourism, particularly in emerging markets offering cost-effective treatments.

Key players include Institut Straumann AG, Dentsply Sirona, ZimVie Inc., BioHorizons, Dentium, and Zest Dental Solutions, leading innovation and market expansion.