- Power Generation, Transmission, & Distribution

- DC Distribution Network Market

DC Distribution Network Market Size, Share, and Growth Forecast, 2026 - 2033

DC Distribution Network Market by Technology (DC-DC Converters, EV Fast-Charging Infrastructure, Others), Voltage Level (Low-Voltage DC (LVDC ≤1.5 kV), Very High/Distribution HVDC, Application, End-user, and Regional Analysis for 2026 – 2033

DC Distribution Network Market Size and Trends Analysis

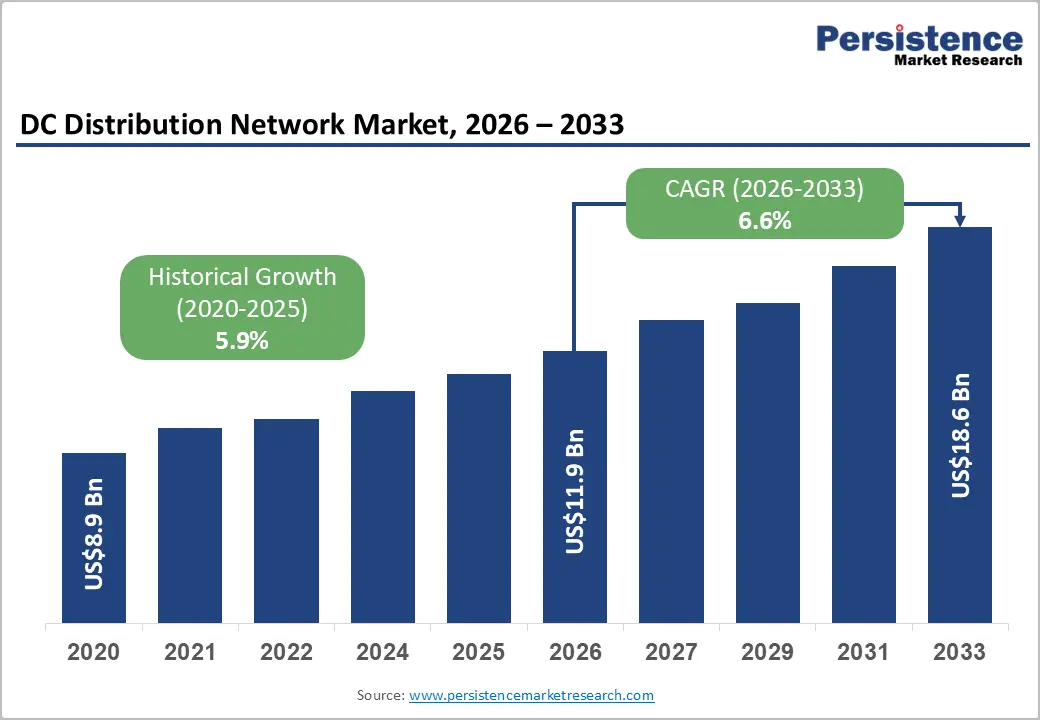

The global DC distribution network market size is likely to be valued at US$11.9 billion in 2026 and is expected to reach US$18.6 billion by 2033, growing at a CAGR of 6.6% between 2026 and 2033, driven by increasing deployment of AI-driven data centers, rapid expansion of EV fast-charging infrastructure, and rising investments in distributed energy systems.

Organizations across industrial, commercial, and utility sectors are adopting DC distribution architectures to improve energy efficiency, reduce power conversion losses, and support higher power densities. Regulatory initiatives promoting energy efficiency and grid modernization further strengthen long-term market prospects. As electrification accelerates globally, DC distribution networks are becoming a critical component of next-generation power infrastructure.

Key Industry Highlights:

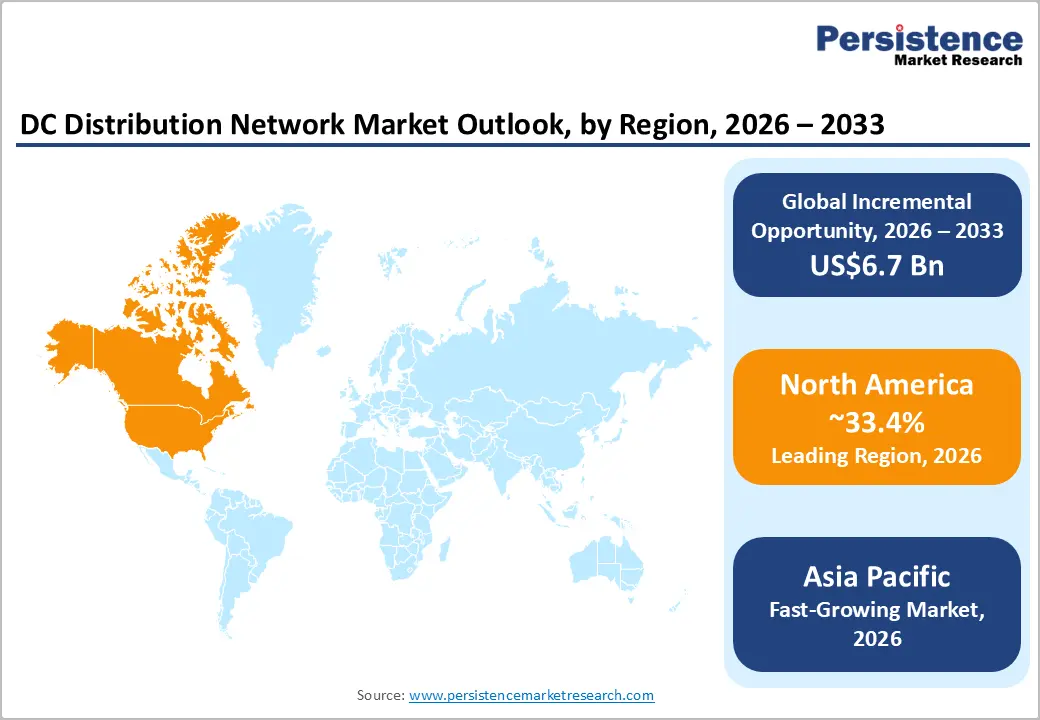

- Leading Region: North America is anticipated to account for approximately 33.4% of the market share in 2026, driven by extensive data center infrastructure, AI investments, and grid modernization initiatives.

- Fastest-growing Region: Asia Pacific is projected to register the highest growth rate through 2033, supported by rapid EV charging deployment, renewable energy investments, expanding data center capacity, and strong manufacturing capabilities across China, India, Japan, and ASEAN countries.

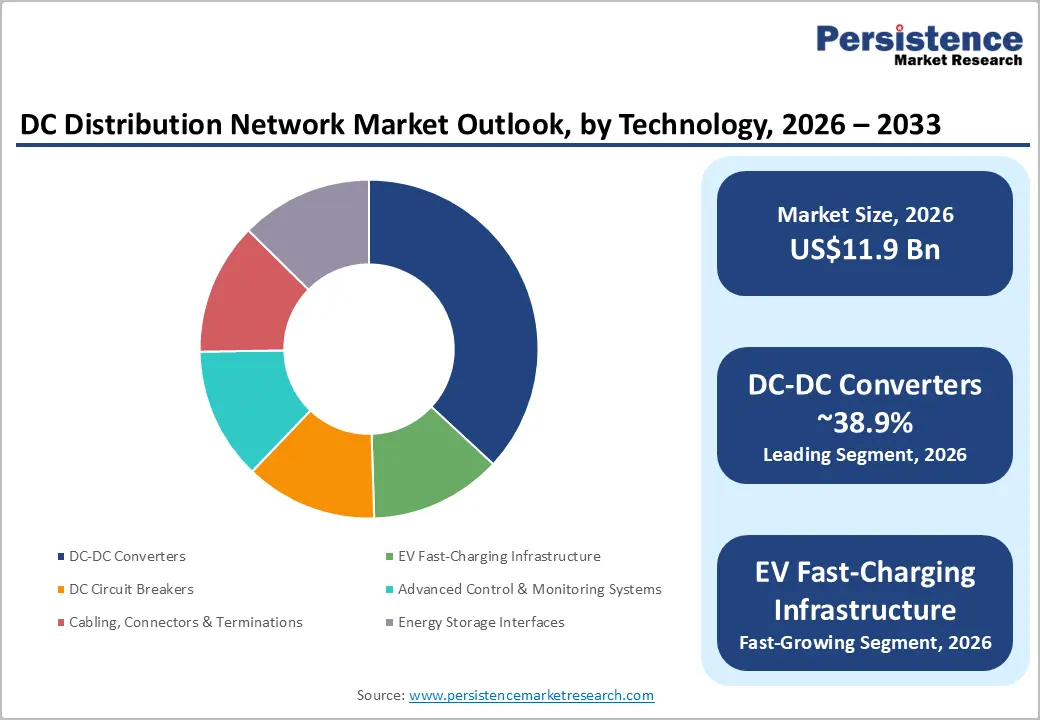

- Dominant Technology: DC-DC Converters are anticipated to account for approximately 38.9% of the market share in 2026, owing to their critical role in voltage regulation and power conversion across data centers, telecom networks, EV charging infrastructure, and energy storage systems.

- Leading Voltage Level: Low-Voltage DC (LVDC ≤1.5 kV) is anticipated to hold approximately 52.7% of the market share in 2026, supported by widespread deployment in data centers, commercial buildings, telecommunications facilities, and distributed energy applications.

DRO Analysis

Driver - Growing Demand for High-Density Data Centers and AI Infrastructure

The rapid expansion of artificial intelligence, cloud computing, and hyperscale data centers is significantly increasing demand for efficient power distribution systems. Global data center electricity consumption has surpassed 400 TWh annually and continues to grow as organizations deploy larger AI training clusters and high-performance computing facilities. Traditional AC power architectures introduce multiple conversion stages, resulting in energy losses and higher operational costs.

DC distribution networks enable direct power delivery, reduce conversion losses, improve power quality, and support high-density computing environments. Data center operators are increasingly evaluating 380VDC and other advanced DC architectures to enhance energy efficiency and optimize rack-level power delivery. The continued expansion of AI infrastructure, hyperscale cloud facilities, and edge computing deployments is expected to remain a major growth catalyst throughout the forecast period.

Expansion of EV Fast-Charging Infrastructure

Global electric vehicle adoption is driving substantial investments in public and private charging infrastructure. Fast-charging stations require high-power DC distribution systems capable of delivering electricity efficiently while maintaining operational reliability. The rapid increase in public charging points across North America, Europe, and Asia Pacific is creating demand for DC switchgear, converters, protection devices, and monitoring systems.

Government programs supporting transportation electrification further strengthen market growth. Public investments in charging corridors, commercial fleet electrification, and urban charging networks are accelerating the deployment of DC-based charging hubs. As charging capacities continue to increase from 150 kW to ultra-fast charging levels exceeding 350 kW, the requirement for advanced DC distribution technologies will expand correspondingly.

Restraint - High Capital Costs and System Integration Complexity

Despite long-term efficiency advantages, DC distribution networks require significant upfront investment. Implementation often involves specialized DC circuit breakers, protection systems, advanced control architectures, and custom engineering solutions. Unlike conventional AC systems, DC networks require dedicated safety standards and protection mechanisms, increasing deployment costs.

Integration challenges are particularly significant for retrofit projects, where existing infrastructure must be redesigned to accommodate DC architectures. Extended project timelines, certification requirements, and limited availability of experienced engineering resources can increase implementation risks. These factors may slow adoption among small and medium-sized enterprises, particularly in cost-sensitive regions.

Opportunity - Standardization of Low-Voltage DC Power Architectures

The development of standardized low-voltage DC systems presents a significant market opportunity. Growing industry consensus around common voltage levels and protection standards is reducing deployment complexity and encouraging broader adoption across commercial buildings, data centers, and industrial facilities.

Standardized architectures improve interoperability between equipment vendors, reduce engineering costs, and simplify maintenance. As more organizations seek energy-efficient power distribution solutions, demand for modular LVDC systems is expected to increase substantially. This trend creates opportunities for suppliers offering integrated DC distribution platforms, intelligent monitoring solutions, and lifecycle management services.

Growth of Renewable Energy and Energy Storage Integration

Increasing deployment of solar photovoltaic systems, battery energy storage systems, and microgrids is creating favorable conditions for DC distribution technologies. Since solar generation and battery storage inherently operate in DC format, direct integration through DC distribution networks can reduce conversion losses and improve overall system efficiency.

Commercial facilities, industrial campuses, and utility-scale renewable projects are increasingly adopting DC-based architectures to optimize energy management. The convergence of renewable energy, battery storage, and intelligent grid technologies is expected to create new revenue opportunities for manufacturers of DC converters, protection equipment, and control systems.

Category-wise Analysis

Technology Insights

DC-DC converters are anticipated to account for approximately 38.9% of the market share in 2026, making them the leading technology segment. Their dominance stems from their critical role in voltage regulation and power conversion across data centers, telecom infrastructure, EV charging systems, renewable energy installations, and battery storage facilities. For example, hyperscale data centers and battery energy storage systems rely on DC-DC converters to improve energy efficiency and maintain stable power delivery. Growing adoption of distributed energy resources and high-density computing environments continues to support segment leadership.

EV fast-charging infrastructure is anticipated to be the fastest-growing technology segment. Rising electric vehicle adoption and increasing investments in public charging networks are driving demand for advanced DC distribution systems. For example, ultra-fast charging hubs along highways and commercial fleet charging depots require high-capacity DC converters, protection systems, and intelligent monitoring solutions to support rapid charging and efficient energy management.

Voltage Level Insights

Low-Voltage DC (LVDC) is anticipated to hold approximately 52.7% of the market share in 2026, making it the leading voltage-level segment. LVDC systems are widely used in data centers, telecom facilities, commercial buildings, and localized energy storage systems due to their ease of deployment and cost-effectiveness. For example, edge data centers and telecom base stations commonly utilize LVDC architectures to improve power efficiency and simplify infrastructure requirements.

Very High/Distribution HVDC (>320 kV) is anticipated to be the fastest-growing voltage segment. Growth is supported by increasing renewable energy integration, long-distance power transmission projects, and grid modernization initiatives. For example, offshore wind farm connections and cross-border electricity interconnections increasingly rely on HVDC technology to reduce transmission losses and improve grid reliability.

Regional Insights

North America DC Distribution Network Market Trends

North America is anticipated to account for approximately 33.4% of the market share in 2026, making it the leading regional market. Growth is primarily supported by expanding hyperscale data centers, rising EV charging infrastructure deployment, and ongoing investments in grid modernization. The region benefits from strong technology adoption, advanced electrical infrastructure, and increasing demand for energy-efficient power distribution systems.

U.S. DC Distribution Network Market Trends

The U.S. is expected to dominate the North America market, accounting for nearly 86% of regional revenue in 2026. The country's leadership is supported by a large concentration of hyperscale data centers, accelerating AI infrastructure investments, and expanding EV charging networks. Major cloud providers and colocation operators are increasingly adopting DC power architectures to improve energy efficiency and reduce power conversion losses. Federal and state-level initiatives supporting electrification and clean energy infrastructure continue to strengthen market growth.

Canada DC Distribution Network Market Trends

Canada is emerging as an important market due to growing investments in renewable energy, data center development, and grid modernization projects. The country's abundant clean energy resources and increasing focus on sustainable digital infrastructure are creating opportunities for DC distribution technologies across commercial and utility-scale applications.

Europe DC Distribution Network Market Trends

Europe remains a strategically important market characterized by ambitious decarbonization targets, energy-efficiency regulations, and increasing investments in renewable energy integration. The region's focus on sustainability and grid modernization is encouraging adoption of advanced DC distribution systems across industrial, commercial, and utility sectors.

Germany DC Distribution Network Market Trends

Germany leads the Europe market due to its strong industrial base and advanced manufacturing sector. The country continues to invest heavily in smart grid infrastructure, industrial automation, and renewable energy integration, driving demand for efficient DC power distribution technologies.

U.K. DC Distribution Network Market Trends

The U.K. is a key market supported by expanding data center capacity, investments in transmission infrastructure, and growing adoption of renewable energy systems. The country's commitment to achieving net-zero emissions is accelerating the modernization of power distribution networks.

France DC Distribution Network Market Trends

France benefits from a well-established electrical equipment manufacturing industry and increasing investments in sustainable energy infrastructure. Growing adoption of energy-efficient building technologies and distributed energy systems is supporting market expansion.

Spain DC Distribution Network Market Trends

Spain is emerging as a high-potential market due to significant investments in solar energy, battery storage projects, and grid modernization initiatives. Increasing renewable energy capacity is creating demand for advanced DC transmission and distribution solutions.

Asia Pacific DC Distribution Network Market Trends

Asia Pacific is anticipated to be the fastest-growing regional market during the forecast period. Rapid urbanization, industrialization, digital transformation, and large-scale infrastructure development are driving demand for DC distribution technologies. The region also benefits from strong manufacturing capabilities, competitive production costs, and growing investments in electrification projects.

China DC Distribution Network Market Trends

China dominates the Asia Pacific market through its leadership in EV adoption, charging infrastructure deployment, renewable energy investments, and power equipment manufacturing. The country's large-scale deployment of public fast-charging stations and utility-scale renewable projects continues to create substantial demand for DC distribution systems.

Japan DC Distribution Network Market Trends

Japan remains a significant market due to its advanced power electronics industry, technological innovation, and focus on energy-efficient infrastructure. The country continues to invest in smart grids, battery storage systems, and next-generation power distribution technologies.

India DC Distribution Network Market Trends

India is emerging as one of the fastest-growing national markets, supported by government-led electrification programs, expanding EV charging infrastructure, and increasing renewable energy deployment. Rapid urban development, data center investments, and industrial expansion are further driving adoption of DC distribution networks.

Competitive Landscape

The global DC distribution network market exhibits a moderately fragmented competitive structure. While several multinational companies maintain strong positions in data center power systems, HVDC technologies, and industrial electrification solutions, regional suppliers and specialized integrators continue to compete effectively in niche applications. Companies are increasingly focusing on software-enabled power management platforms, intelligent monitoring systems, and modular DC architectures to strengthen their market position.

Leading companies are prioritizing innovation, digitalization, and geographic expansion. Strategic investments in AI-ready infrastructure, intelligent power management platforms, modular DC architectures, and regional manufacturing capabilities remain key competitive differentiators. Partnerships with cloud providers, data center operators, and energy infrastructure developers are becoming increasingly important for long-term growth.

Key Industry Developments:

- In April 2026, Siemens AG launched a comprehensive portfolio of direct current (DC) protection and switching solutions, including the SENTRON 3QD2 semiconductor circuit breaker and SIRIUS 3RF5 solid-state switching device, aimed at data centers, battery storage systems, industrial facilities, and renewable energy applications.

- In October 2025, ABB announced a strategic collaboration with NVIDIA to develop next-generation power solutions for gigawatt-scale AI data centers.

Companies Covered in DC Distribution Network Market

- ABB Ltd.

- Siemens AG

- Schneider Electric SE

- Eaton Corporation plc

- Vertiv Holdings Co.

- Delta Electronics, Inc.

- Hitachi Energy Ltd.

- GE Vernova Inc.

- Huawei Digital Power Technologies Co., Ltd.

- Mitsubishi Electric Corporation

- Toshiba Energy Systems & Solutions Corporation

- Legrand SA

- Fuji Electric Co., Ltd.

- Emerson Electric Co.

- Nexans S.A.

- Prysmian S.p.A.

Frequently Asked Questions

The global DC distribution network market is estimated to be valued at US$11.9 billion in 2026.

The DC distribution network market is projected to reach US$18.6 billion by 2033.

Key trends include increasing adoption of AI-ready data center power architectures, expansion of EV fast-charging networks, growing deployment of battery energy storage systems, rising investments in HVDC transmission infrastructure, and the integration of renewable energy resources with DC power networks.

DC-DC Converters are the leading technology segment, anticipated to account for approximately 38.9% of the market share, owing to their extensive use in data centers, telecom networks, EV charging systems, and energy storage applications.

The DC distribution network market is projected to grow at a CAGR of 6.6% between 2026 and 2033.

Major companies include ABB, Siemens, Schneider Electric, Eaton, and Vertiv.