- Automation & Robotics

- Cotton Spinning Machinery Market

Cotton Spinning Machinery Market Size, Share, and Growth Forecast, 2026 - 2033

Cotton Spinning Machinery Market by Machinery Type (Ring Spinning, Compact Spinning, Others), Application (Apparel & Garments, Home Textiles, Others), Automation Level, and Regional Analysis for 2026 - 2033

Cotton Spinning Machinery Market Size and Trends Analysis

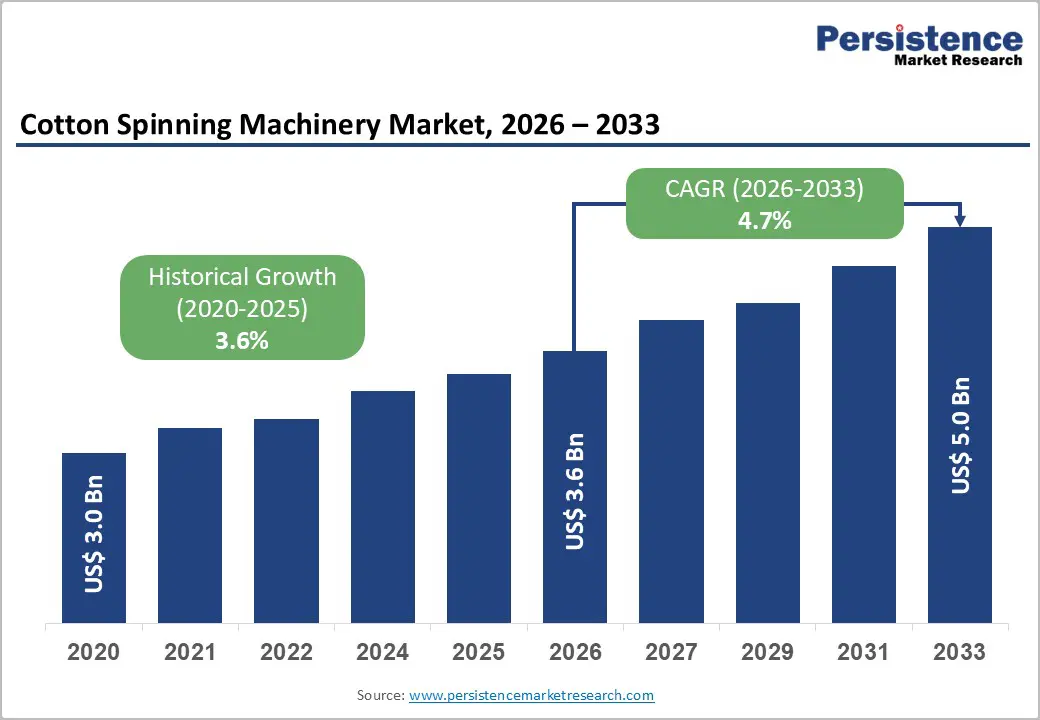

The global cotton spinning machinery market size is likely to be valued at US$3.6 billion in 2026 and is expected to reach US$5.0 billion by 2033, growing at a CAGR of 4.7% between 2026 and 2033, driven by increasing global demand for apparel and textile products, modernization of spinning facilities in emerging economies, and growing adoption of automated spinning systems.

Textile manufacturers are investing in advanced machinery that improves production efficiency, reduces energy consumption, and ensures consistent yarn quality. Asia Pacific remains the largest production hub, while equipment manufacturers in North America and Europe increasingly focus on high-value automated machinery and digital service offerings. The transition toward compact spinning technologies and integrated automation systems is strengthening capital investment cycles across global textile mills.

Key Industry Highlights:

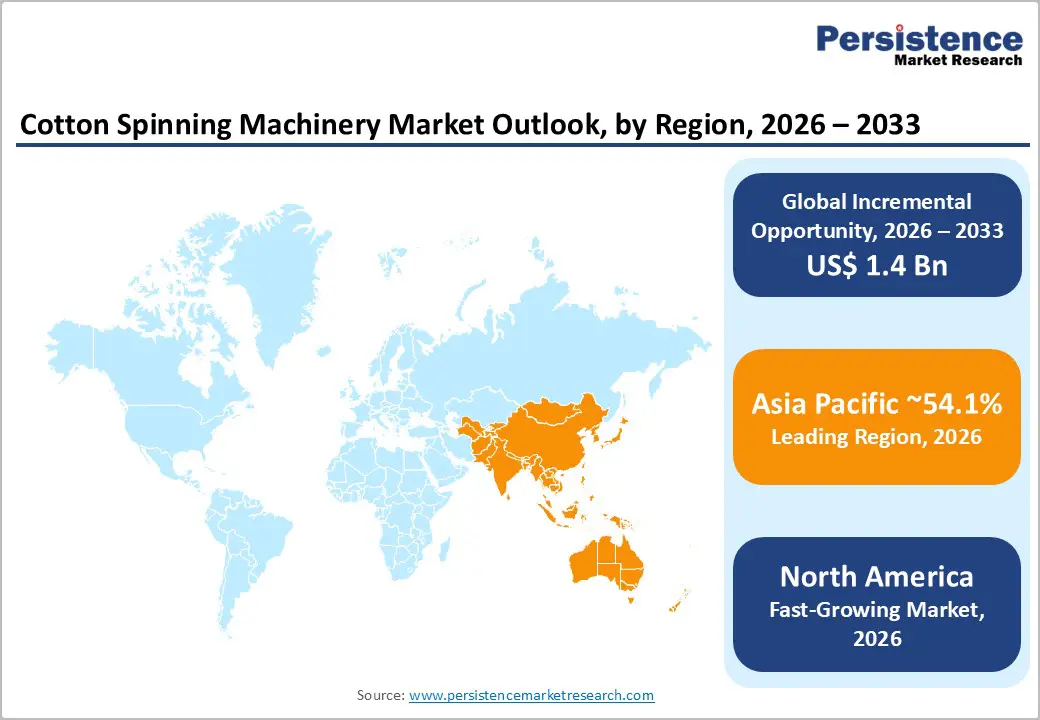

- Leading Region: Asia Pacific is projected to lead the regional market, accounting for 54.1% of the market share, supported by large-scale textile manufacturing hubs in China, India, Bangladesh, and Vietnam.

- Fastest-Growing Region: North America is projected to be the fastest-growing regional market, driven by increasing investments in automated spinning technologies, textile manufacturing reshoring initiatives, and rising demand for technical textiles in the U.S.

- Investment Plans: Textile manufacturers worldwide are increasing investments in modern spinning mills and advanced automated machinery to improve production efficiency, reduce labor dependency, and meet sustainability requirements in yarn manufacturing.

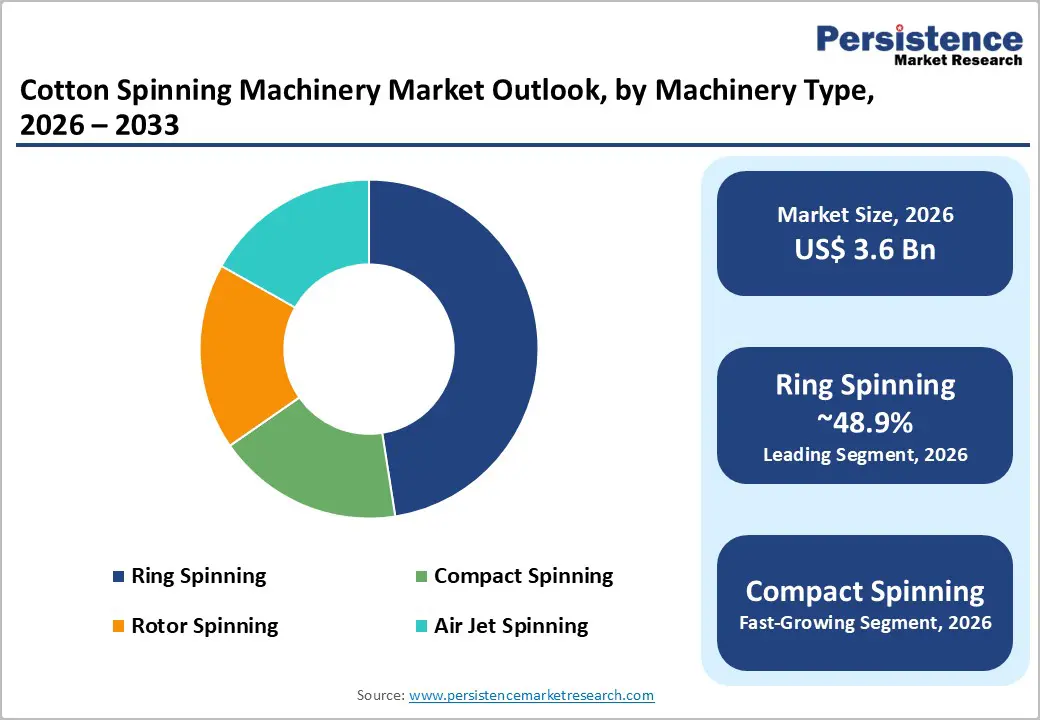

- Dominant Machinery Type: Ring spinning machinery is the dominant machinery type segment, anticipated to hold 48.9% of the market share, due to its ability to produce high-quality yarn across a wide range of textile applications.

- Leading Application: The apparel and garments segment represents the leading application category, anticipated to account for 55.2% of the market, supported by strong global clothing demand and expanding garment manufacturing industries in the Asia Pacific.

| Key Insights | Details |

|---|---|

| Cotton Spinning Machinery Market Size (2026E) | US$3.6 Bn |

| Market Value Forecast (2033F) | US$5.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expansion of Textile Manufacturing Capacity in Asia Pacific

The rapid expansion of textile manufacturing capacity across the Asia Pacific continues to be the most significant driver for cotton spinning machinery demand. Countries including China, India, Bangladesh, Vietnam, and Indonesia have become major textile production hubs due to competitive labor costs, strong export-oriented apparel industries, and supportive government policies. Textile export revenues from several Asian economies account for a substantial portion of global apparel supply chains, encouraging mills to invest in new spinning equipment and upgrade aging facilities. Large-scale spinning mills in these countries frequently expand capacity through greenfield projects or modernization programs. New installations require advanced ring, rotor, and compact spinning systems capable of higher spindle speeds and improved yarn consistency. The continuous expansion of apparel production capacity across the region is expected to generate consistent machinery demand throughout the forecast period.

Automation and Digitalization Improving Production Efficiency

Automation has become a major technological driver in the cotton spinning machinery industry. Textile manufacturers are adopting fully automated spinning lines integrated with machine-monitoring systems, predictive maintenance software, and digital process-optimization platforms. These technologies allow mills to improve operational efficiency, reduce machine downtime, and minimize labor dependency. Modern spinning machines are equipped with sensors, intelligent control systems, and integrated mill management platforms that track machine performance and yarn quality in real time. These innovations significantly improve overall equipment effectiveness and reduce production waste. As labor costs rise across several manufacturing regions, textile producers are increasingly shifting toward automated solutions to achieve higher productivity and better process control. This trend is accelerating equipment replacement cycles and supporting steady growth in machinery demand.

Rising Demand for Premium and Specialty Yarn

Demand for higher-quality yarn products is expanding rapidly as evolving requirements from apparel brands, home textile manufacturers, and technical textile producers drive demand. Premium textile products require yarns with improved tensile strength, reduced hairiness, and greater fiber alignment consistency. Compact spinning technology has emerged as a preferred solution for producing such high-performance yarns. Compact spinning machines reduce fiber fly and yarn imperfections, resulting in stronger and smoother yarn suitable for high-end fabrics. Manufacturers are therefore upgrading traditional spinning systems to compact spinning solutions or installing new production lines capable of meeting stringent quality standards. The growing demand for premium yarn products is expected to continue driving equipment modernization across the global textile industry.

Barrier Analysis - High Capital Investment Requirements

Cotton spinning machinery represents a capital-intensive investment for textile manufacturers. Advanced spinning equipment, particularly fully automated systems, requires substantial upfront capital expenditure and often involves significant factory layout modifications. Small and medium-sized textile mills may face financial constraints that limit their ability to adopt the latest spinning technologies. The payback period for automated spinning systems can extend over several years depending on production volume, yarn pricing fluctuations, and labor cost savings. In markets with volatile cotton prices or uncertain textile demand, manufacturers may postpone large capital investments. As a result, the adoption of high-end spinning machinery can progress gradually in cost-sensitive regions.

Supply Chain Disruptions and Component Availability

The cotton spinning machinery industry relies heavily on precision components, including electronic control modules, bearings, high-speed spindles, and specialized motors. Global supply chain disruptions can delay the production and delivery of these components, resulting in extended machine lead times. Such disruptions can affect project timelines for new spinning mills and capacity expansions. In some cases, textile manufacturers may delay machinery purchases until component availability stabilizes. Supply chain instability, therefore, represents an operational challenge for machinery manufacturers and can influence short-term market growth patterns.

Opportunity Analysis - Expansion of Aftermarket Services and Retrofit Solutions

The global installed base of cotton spinning machinery offers significant opportunities for aftermarket services, spare parts supply, and machine retrofits. Many textile mills operate mixed fleets consisting of both modern and legacy spinning equipment. Manufacturers can extend the operational life of existing machines through upgrades such as automation modules, improved control systems, and energy-efficient drive systems. Service contracts, predictive maintenance programs, and digital monitoring platforms are increasingly becoming important revenue streams for equipment suppliers. These services allow mills to optimize machine performance while reducing unexpected downtime. The growing importance of lifecycle support services is expected to create new revenue opportunities across the spinning machinery value chain.

Growing Demand for Compact Spinning Technology

Compact spinning technology is gaining popularity among textile manufacturers due to its ability to produce superior yarn quality with reduced fiber loss. Compared with conventional ring spinning, compact spinning systems generate yarn with improved strength and lower hairiness, making them ideal for high-end textile applications. Textile mills supplying international apparel brands are increasingly investing in compact spinning machinery to meet strict quality specifications. As demand for premium fabrics and technical textiles continues to expand, adoption of compact spinning technology is expected to accelerate, creating strong growth potential for machinery manufacturers.

Category-wise Analysis

Machinery Type Insights

Ring spinning machinery is anticipated to account for 48.9% of the market share in 2026, making it the largest segment within the machinery type category. This technology remains the most widely adopted spinning method due to its ability to produce high-quality yarn across a broad range of yarn counts. Ring spinning machines are widely used to produce cotton yarn for apparel fabrics, knitwear, denim, and woven textiles. Their ability to deliver superior yarn strength and consistent fiber twisting has made them a core technology across large textile manufacturing hubs.

The technology offers excellent yarn strength, uniformity, and versatility, making it suitable for both mass-market and premium textile products. Large spinning mills in countries such as China, India, and Bangladesh rely heavily on ring spinning systems for core yarn production used in global garment supply chains. For instance, major textile clusters in Gujarat and Tamil Nadu, India, operate thousands of ring spinning frames to supply yarn to international apparel exporters. Continuous improvements in spindle speed, traveler materials, and energy-efficient drive systems have further enhanced productivity and reduced operational costs, reinforcing the segment’s dominant position.

Compact spinning machinery represents the fastest-growing segment within the cotton spinning machinery market due to increasing demand for premium and high-performance yarn products. Compact spinning technology minimizes fiber fly and significantly improves fiber alignment during spinning. This results in yarns with higher tensile strength, lower hairiness, and improved surface quality, which are essential for producing high-end fabrics and fine garments.

Textile manufacturers supplying global apparel brands and technical textile producers are increasingly adopting compact spinning machines to meet strict quality requirements. For example, spinning mills producing yarn for luxury fashion labels and high-quality knitwear often use compact spinning technology to achieve smoother yarn surfaces and enhanced durability. The technology also improves production efficiency by reducing fiber waste and minimizing downstream processing defects. As sustainability initiatives encourage efficient fiber utilization and improved product durability, compact spinning machinery is expected to witness strong adoption in modern textile manufacturing facilities worldwide.

Application Insights

The apparel and garments sector is anticipated to account for 55.2% of the market share in 2026. Rising global demand for clothing continues to drive large-scale yarn production, particularly in major garment manufacturing countries. The apparel industry requires vast quantities of cotton yarn for the production of shirts, denim, knitwear, sportswear, and fashion garments. Textile manufacturers supplying apparel brands require consistent yarn quality and high production volumes, which drives investment in reliable and high-capacity spinning machinery. Countries such as Bangladesh, Vietnam, and India have developed extensive garment manufacturing ecosystems that rely heavily on large spinning mills to supply yarn for export-oriented apparel factories.

For example, major textile groups in Bangladesh operate vertically integrated spinning and garment facilities to support global fast-fashion brands. Continuous expansion of garment manufacturing hubs in the Asia Pacific, along with rising demand from international apparel retailers, further reinforces the dominance of this segment.

Home textiles are the fastest-growing application segment for cotton spinning machinery, driven by rising consumer demand for household textile products. Increasing disposable incomes, rapid urbanization, and expanding housing markets have driven increased consumption of products such as bed sheets, towels, blankets, curtains, and upholstery fabrics. Manufacturers of home textile products require yarns with greater durability, softness, and moisture absorption.

As a result, spinning mills are investing in specialized machinery capable of producing thicker yarn counts and blended yarns suited for home textile applications. For instance, large textile producers in Turkey and Pakistan supply cotton yarn to global home furnishing brands and hotel chains, requiring advanced spinning systems that ensure consistent product quality and durability. Growth in the global hospitality industry and increasing demand for premium bedding and interior décor products are expected to further strengthen investment in spinning machinery for home textile production.

Regional Insights

North America Cotton Spinning Machinery Market Trends - Textile Reshoring and Automated High-Value Yarn Production

North America is emerging as the fastest-growing regional market, driven largely by increasing investments in advanced textile manufacturing technologies and a renewed focus on reshoring textile production. The U.S. plays a central role in this transformation as manufacturers seek to reduce dependence on overseas supply chains and strengthen domestic textile capabilities. Several large textile producers are investing in modern spinning facilities equipped with automated machinery to improve efficiency and supply high-value yarns for specialized applications.

Companies such as Parkdale Mills, one of the largest yarn manufacturers in the U.S., continue to modernize their spinning operations by adopting energy-efficient ring spinning and automated yarn processing technologies to support domestic apparel and textile production. Similarly, Unifi, Inc., known for its performance yarns and recycled fiber solutions, has expanded advanced yarn manufacturing operations in the U.S. to meet rising demand from apparel and industrial textile markets. These investments highlight a broader trend toward high-value, technologically advanced spinning operations in North America.

Demand from industries such as defense, automotive textiles, and medical fabrics is also supporting equipment modernization. For example, the U.S. government’s focus on strengthening domestic manufacturing capabilities has encouraged textile manufacturers supplying military uniforms and protective fabrics to invest in automated spinning systems that deliver consistent yarn quality. Labor shortages and rising wages across North America are further accelerating the adoption of fully automated spinning machinery, enabling mills to reduce manual intervention while maintaining high productivity. As a result, machinery suppliers are increasingly targeting North American customers with advanced automation solutions and digital machine monitoring technologies.

Europe Cotton Spinning Machinery Market Trends - Advanced Machinery Innovation and Sustainability-Driven Mill Upgrades

Europe remains an important market for cotton spinning machinery due to its concentration of advanced textile machinery manufacturers and highly specialized textile producers. Countries such as Germany, Italy, the U.K., France, and Spain play significant roles in the regional textile ecosystem, both as machinery suppliers and producers of premium textile products. Germany and Italy, in particular, are home to several globally recognized textile machinery manufacturers that continuously develop advanced spinning technologies.

Companies such as Trützschler Group in Germany and Marzoli in Italy have introduced new spinning preparation and ring spinning solutions designed to improve productivity while reducing energy consumption. These innovations support European textile mills that focus on high-quality fabrics and specialized yarn applications. For instance, European producers supplying luxury fashion brands often require compact spinning technology to achieve the yarn smoothness and strength needed for premium garments.

Sustainability and regulatory compliance are also major drivers of machinery upgrades in Europe. Strict environmental policies on industrial emissions and energy efficiency are encouraging textile mills to replace older machinery with modern equipment that reduces electricity consumption and optimizes fiber utilization. European textile producers serving brands such as Hugo Boss, Inditex, and H&M increasingly require traceable and sustainably produced yarns, prompting spinning mills to invest in advanced machinery with digital monitoring systems that ensure consistent product quality and process transparency. Europe also plays a strategic role as a global exporter of textile machinery technology. Many European manufacturers supply high-end spinning equipment to textile mills in Asia Pacific, Africa, and Latin America. This strong export orientation allows the region to maintain its influence in the global cotton spinning machinery market even though large-scale textile production is concentrated elsewhere.

Asia Pacific Cotton Spinning Machinery Market Trends- Dominant Spinning Capacity and Export-Oriented Textile Manufacturing Expansion

Asia Pacific is projected to dominate the market, accounting for 54.1% of the market share. The region hosts the majority of global spinning capacity and serves as the primary manufacturing base for textile products exported worldwide. Major textile-producing countries, including China, India, Bangladesh, Vietnam, and Indonesia, operate thousands of spinning mills that supply yarn to global markets for apparel, home textiles, and industrial textiles. China remains one of the largest markets for spinning machinery due to its extensive textile manufacturing infrastructure and continued investments in factory automation.

Chinese textile groups have increasingly adopted advanced spinning systems to improve productivity and meet rising quality standards for export markets. Meanwhile, India has emerged as one of the fastest-growing centers of spinning capacity, supported by government initiatives such as the Production-Linked Incentive (PLI) scheme and textile modernization programs aimed at strengthening domestic manufacturing. Major Indian textile companies such as Vardhman Textiles and Arvind Limited continue to expand spinning capacity and upgrade machinery to supply yarn for both domestic and international markets.

Southeast Asia is also experiencing significant growth in spinning capacity as global apparel supply chains diversify away from single-country sourcing. Countries such as Vietnam and Bangladesh have attracted large investments in vertically integrated textile facilities. For example, Bangladeshi textile conglomerates such as DBL Group and Square Textiles have invested heavily in modern spinning equipment to support the country’s rapidly expanding garment export industry. These investments require high-performance ring spinning and compact spinning machinery capable of meeting the production demands of international apparel brands. Government policies supporting textile industry development, combined with competitive labor costs and strong export demand, continue to attract new spinning mill investments across the region. As a result, machinery manufacturers are prioritizing Asia Pacific markets by establishing regional service centers, expanding distribution networks, and introducing cost-competitive equipment designed specifically for high-volume textile production environments.

Competitive Landscape

The global cotton spinning machinery market demonstrates a moderately concentrated structure. A limited number of global machinery manufacturers dominate the high-technology segment, particularly in automated and precision spinning systems. At the same time, numerous regional manufacturers operate in cost-sensitive markets by offering competitively priced equipment and localized service support. Established technology leaders maintain competitive advantages through strong research capabilities, extensive service networks, and advanced product portfolios. Meanwhile, emerging manufacturers compete primarily through price competitiveness and regional distribution channels.

Leading companies focus on automation innovation, energy-efficient machinery development, global service expansion, and aftermarket support programs. Competitive differentiation increasingly relies on digital monitoring systems, predictive maintenance platforms, and turnkey spinning mill solutions that improve operational efficiency for textile manufacturers.

Key Industry Developments

- In September 2025, Rieter Holding AG announced new automation and digital solutions for fully automated spinning mills at ITMA Asia + CITME 2025 in Singapore, including automated material transport, packaging systems, and the OMEGAlap E 40 combing preparation machine. The development reflects the company’s strategy to enable step-by-step automation of spinning mills and improve productivity through smart manufacturing technologies.

- In July 2025, Trützschler Group showcased its next-generation TC 30i carding machine at CAITME 2025, highlighting significant productivity improvements and intelligent gap optimization technology that ensures consistent fiber processing. The machine supports higher yarn quality and more efficient fiber utilization, addressing the growing demand for advanced spinning preparation equipment.

Companies Covered in Cotton Spinning Machinery Market

- Rieter Holding AG

- Trützschler Group

- Saurer Intelligent Technology Co. Ltd.

- Toyota Industries Corporation

- Lakshmi Machine Works Limited

- Marzoli Machines Textile S.r.l.

- Jingwei Textile Machinery Company Ltd.

- Taitan Group (Zhejiang Taitan Co., Ltd.)

- Shandong Tongda Textile Machinery Co., Ltd.

- Savio Macchine Tessili S.p.A.

- Kirloskar Toyoda Textile Machinery Pvt. Ltd.

- A.T.E. Group

- Itema S.p.A.

- Electro-Jet S.L.

- Murata Machinery, Ltd. (Muratec)

- Oerlikon Textile GmbH & Co. KG

- Zinser Textile Systems (Saurer Group)

- Jiangsu Jinlong Technology Co., Ltd.

Frequently Asked Questions

The global cotton spinning machinery market is estimated to be valued at US$3.6 billion in 2026.

The cotton spinning machinery market is projected to reach US$5.0 billion by 2033.

Key trends shaping the market include increasing adoption of automated and energy-efficient spinning machinery, rising demand for premium yarn through compact spinning technologies, and growing investments in textile manufacturing modernization across emerging economies.

Ring spinning machinery is the leading segment in the cotton spinning machinery market, anticipated to account for 48.9% of the market share, due to its ability to produce high-quality yarn suitable for a wide range of textile applications.

The cotton spinning machinery market is projected to grow at a CAGR of 4.7% between 2026 and 2033.

Major companies include Rieter Holding AG, Trützschler Group, Saurer Intelligent Technology Co. Ltd., Toyota Industries Corporation, and Lakshmi Machine Works Limited.