- Inks, Coatings, Adhesives & Sealants (ICAS)

- Chrome Pigments Market

Chrome Pigments Market Size, Share, and Growth Forecast, 2026-2033

Chrome Pigments Market by Product Type (Chrome Oxide Green, Chrome Yellow, Chrome Red, & Others), Application (Paints & Coatings, Plastics & Polymers, Ceramics & Glass, Printing Inks, Elastomers), End-Use Industry (Automotive, Construction, Packaging, Textiles, Others), and Regional Analysis for 2026-2033

Chrome Pigments Market Share and Trends Analysis

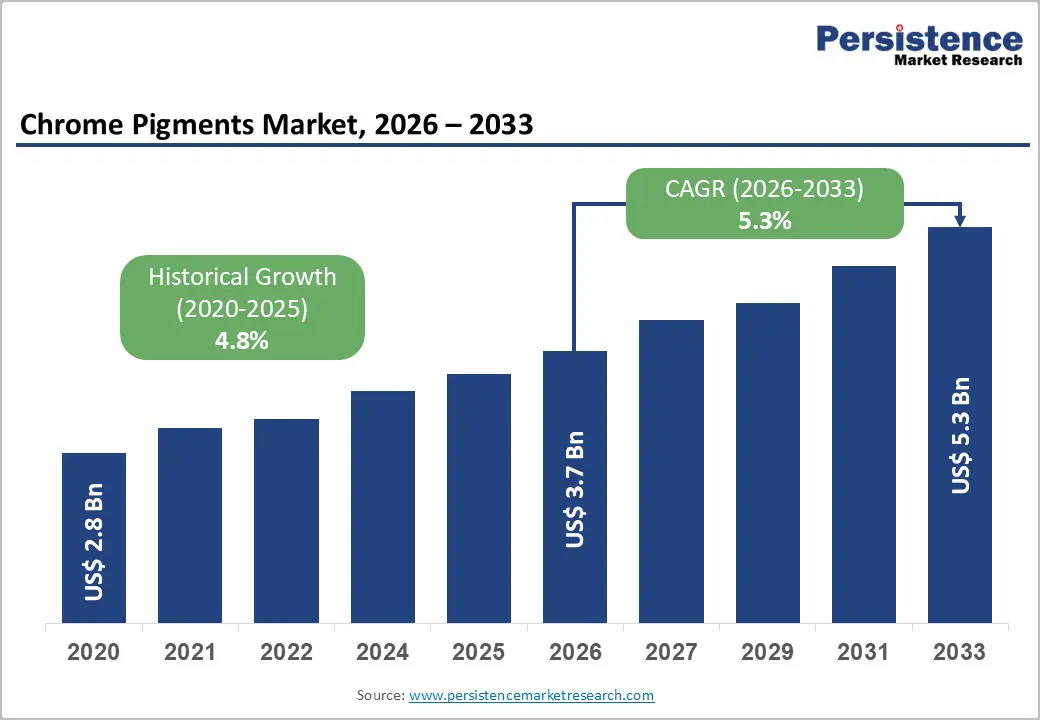

The global chrome pigments market size is likely to be valued at US$ 3.7 billion in 2026, and is projected to reach US$ 5.3 billion by 2033, growing at a CAGR of 5.3% during the forecast period 2026–2033.

Market expansion is being supported by steady demand from paints and coatings, automotive refinishing, and large-scale construction projects that require durable inorganic color solutions. Chrome-based pigments are delivering strong opacity, corrosion resistance, and color stability under extreme environmental conditions. These functional advantages are making them suitable for protective coatings applied in infrastructure, industrial equipment, and transportation assets. As global construction activity continues increasing and vehicle refurbishment cycles remain active, consumption of performance-oriented inorganic pigments is maintaining stable momentum. Regulatory tightening around volatile organic compounds (VOCs) is influencing formulation strategies within the coatings industry.

Manufacturers are reformulating products to comply with stricter emission standards, and inorganic pigment systems are gaining preference due to their chemical stability and lower migration risk. At the same time, infrastructure expansion across Asia Pacific is supporting incremental demand, particularly in emerging economies investing in transport corridors, urban housing, and industrial facilities. Strategic investment in environmentally compliant pigment technologies and localized distribution networks can strengthen competitive positioning through 2033.

Key Industry Highlights

- Dominant Product Type: Chrome oxide green is expected to hold about 41% share in 2026, while chrome yellow and chrome red are projected to grow fastest through 2033, driven by infrastructure and industrial coatings demand.

- Leading Applications: Paints and coatings are projected to account for roughly 46% of demand in 2026, while plastics and polymers are expected to expand at roughly 6.2% CAGR during 2026–2033, powered by rising automotive production.

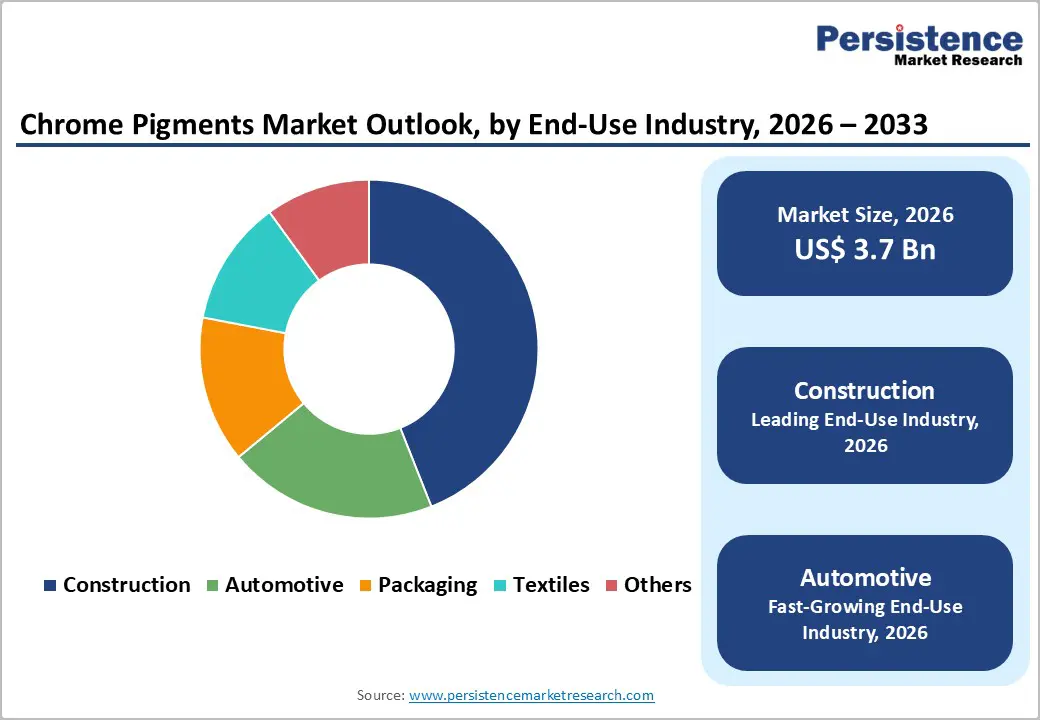

- Dominant End-Use Industry: Construction is anticipated to lead with around 44% share in 2026, while automotive is forecast to grow the fastest at around 6.1% CAGR through 2033, supported by higher vehicle output and refinishing activity.

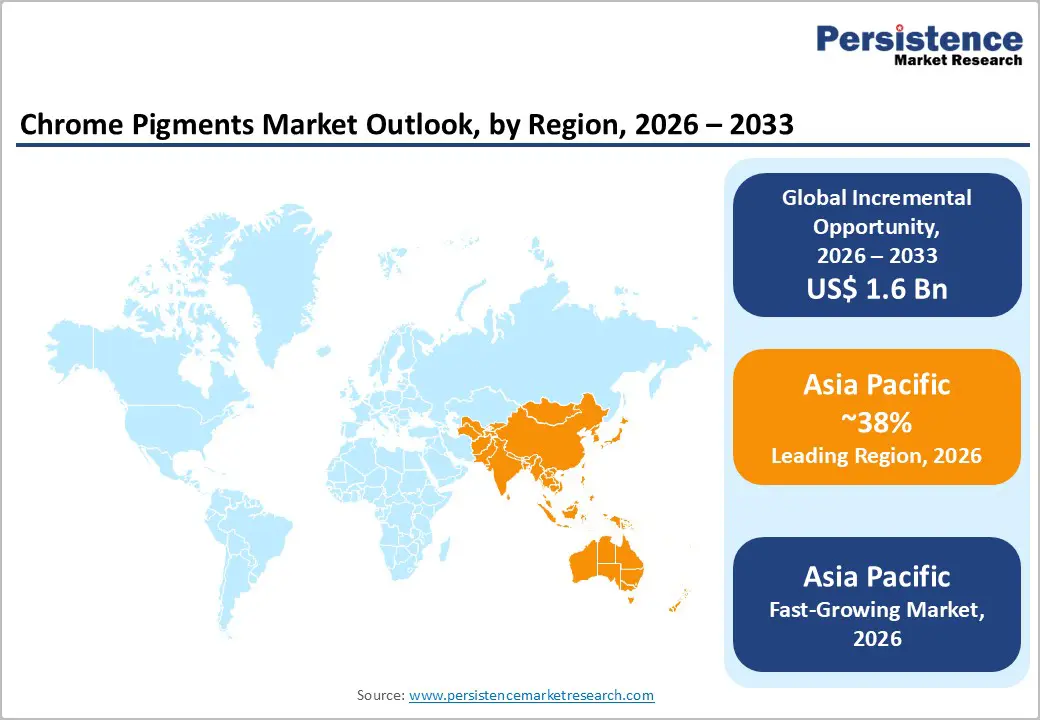

- Regional Leadership: Asia Pacific is projected to represent nearly 38% of global demand in 2026 and remain the fastest-growing market at an estimated 6.4% CAGR through 2033, led by infrastructure expansion and manufacturing advantages.

- Competitive Environment: Competition is driven by regulatory compliance and process innovation, with manufacturers focusing on cleaner formulations and Asia-centric capacity expansion to sustain growth.

| Key Insights | Details |

|---|---|

| Chrome Pigments Market Size (2026E) | US$ 3.7 Bn |

| Market Value Forecast (2033F) | US$ 5.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Regulatory Preference for Durable, Low-VOC Inorganic Pigments

Environmental authorities such as the U.S. Environmental Protection Agency (EPA) and the European Chemicals Agency (ECHA) have progressively tightened regulations governing VOC emissions and pigment leaching in architectural and industrial coatings. These policies align with the European Green Deal’s focus on lifecycle sustainability and reduced maintenance intensity in construction and industrial assets. Under the Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH) framework, inorganic pigments with high thermal and chemical stability are recognized for delivering lower lifecycle emissions than many organic alternatives, reinforcing their role in compliance-driven coating formulations.

Increasing emphasis on lifecycle performance has shifted market attention toward coating systems that require fewer reapplications over time. Chrome pigments, particularly chrome oxide green, remain permitted under controlled-use guidelines due to their chemical inertness and long-term stability. Their ability to withstand harsh environmental exposure extends coating service life in industrial settings. This durability directly reduces repainting frequency and material consumption. Lower maintenance needs also translate into reduced associated emissions. As a result, the adoption has strengthened across industrial and protective coatings applications.

Expansion of Infrastructure and Automotive Manufacturing Activity

Infrastructure development policies and industrial growth programs across major economies increasingly emphasize durability, safety, and lifecycle cost efficiency in public assets and transportation systems. In Asia Pacific, government-led infrastructure frameworks prioritize long-life materials for roads, bridges, transit systems, and urban construction, while automotive manufacturing standards continue to strengthen requirements for corrosion resistance and coating performance. These policy directions elevate the role of high-durability inorganic pigments in both construction and vehicle production environments.

A clear market trigger has been sustained growth in infrastructure execution and vehicle production, particularly across China, India, and Southeast Asia. Chrome pigments are extensively used in automotive original equipment manufacturer (OEM) coatings, road markings, and protective infrastructure paints due to their resistance to UV degradation, corrosion, and environmental stress. The resulting market impact is the continued integration of chrome pigments into performance-driven formulations, where longer service life directly lowers repainting frequency and long-term maintenance costs.

Toxicity Perception and Rising Regulatory Compliance Costs

Although most commercially used chrome pigments are based on trivalent chromium (Cr³+), market perception continues to be shaped by historical concerns linked to hexavalent chromium. Regulatory attention on hexavalent chromium in drinking water and airborne emissions during 2025–2026 intensified broader scrutiny of chromium compounds across environmental and occupational safety frameworks. This heightened focus, despite clear chemical distinctions, increased caution among downstream users in highly regulated end-use industries. Pigment selection is therefore influenced not only by technical compliance but also by reputational risk considerations. Adoption decisions increasingly factor in long-term regulatory exposure. This dynamic continues to restrain penetration in sensitive applications.

Compliance obligations further amplify this restraint. Manufacturers must adhere to stringent requirements for labeling, handling, monitoring, and waste disposal, particularly across Europe and North America. Regulatory authorities have highlighted that these measures add measurable overheads across production, storage, and logistics operations. Increased inspection frequency and documentation requirements have raised compliance-related costs for chromium-based materials. These cost pressures limit pricing flexibility for pigment suppliers. Competitive positioning becomes more difficult in price-sensitive segments. Smaller manufacturers face a disproportionate regulatory burden.

Raw Material Supply Volatility and Input Cost Exposure

Chrome pigment production remains highly dependent on chromium ore availability and energy-intensive processing routes, exposing manufacturers to upstream volatility. Raw material sourcing is concentrated in a limited number of geographies, increasing vulnerability to policy-driven disruptions. The policy discussions in major producing countries such as Zimbabwe and South Africa around chrome ore export controls highlighted growing uncertainty in global chromium trade flows. These initiatives, aimed at promoting domestic beneficiation, introduced additional regulatory risk for international buyers. Logistics constraints and permitting requirements further complicated sourcing strategies. Supply concentration continues to reduce flexibility for pigment producers.

This risk profile is reinforced by the classification of chromium as a critical mineral with notable supply-chain sensitivity, a concern that gained further relevance in 2026. The rollout of carbon-related trade compliance mechanisms affecting mineral-intensive industries added another layer of cost and reporting complexity. Volatility in ore pricing and energy costs has made long-term cost forecasting more challenging, with short-term price fluctuations compressing margins or delaying capacity expansion decisions. Contract negotiations with downstream customers become increasingly complex. These factors collectively constrain operational predictability across the chrome pigments market.

Infrastructure-Led Demand Growth and Regional Expansion

Sustained infrastructure expansion across Asia Pacific is expected to drive long-term demand for chrome pigments through 2030 and beyond. Regional infrastructure spending linked to urbanization, public works, and industrial facilities supports materials such as cement, tiles, and protective coatings that embed chrome pigments for durability. An industry report highlighted Indonesia’s introduction of revised royalty tariffs on chrome ore and refined chromium products, reflecting evolving mineral policy incentives that encourage downstream processing and longer value chains within the region. These policy shifts have reinforced regional self-sufficiency objectives. As a result, domestic pigment consumption is increasingly tied to local construction pipelines.

From a quantitative standpoint, Asia Pacific accounts for the largest share of chromium pigment consumption, supported by strong coatings and ceramics usage. Continued momentum in public and private construction projects is expected to expand chrome pigment uptake in architectural coatings, colored concrete, and industrial surface applications. This positions the region as a key volume driver for chrome pigment demand throughout the forecast period. Infrastructure scale rather than short-term cycles underpins this opportunity. Manufacturing-led spillover effects further support sustained pigment offtake.

Performance Material Adoption in Ceramics, Glass, and Reformulated Solutions

Demand for performance-critical pigments in ceramics and glass manufacturing presents a strong opportunity for chrome pigment producers. Chrome oxide green retains preference due to its ability to withstand kiln temperatures above 1,000°C without chromatic degradation. This property is essential for architectural ceramics, tiles, and specialty glass products. Industry events, including Indian Ceramics Asia, reflected increasing focus on advanced materials, process optimization, and supply chain resilience within the ceramics sector. These discussions emphasized long-term material reliability.

Alongside performance demand, product reformulation initiatives are improving regulatory alignment and market accessibility. R&D efforts aimed at reducing trace impurities and improving encapsulation enhance acceptance under international chemical safety frameworks. These developments support wider adoption in compliance-sensitive applications while enabling entry into higher-value segments. Reformulation also improves customer confidence in regulated end uses. Thus, performance reliability and regulatory alignment expand addressable demand and strengthen long-term market potential for chrome pigments.

Category-wise Analysis

Product Type Insights

Chrome oxide green is estimated to remain the leading product type, accounting for around 46% of the chrome pigments market revenue share in 2026, supported by sustained demand across coatings, plastics, and high-durability industrial applications. Its chemical inertness, UV stability, and broad regulatory acceptance are expected to continue positioning it as a preferred pigment for long-lasting architectural and protective coatings. The pigment’s reliable performance under harsh environmental conditions supports its use in infrastructure and industrial materials. These characteristics are likely to sustain its leadership across construction and automotive refinishing applications. Demand appears structurally linked to performance-driven end uses.

The industry developments in past years indicate continued alignment with this trend. BASF Coatings introduced its Automotive Color Trends collection, emphasizing sustainability and advanced pigment technologies that influence OEM coating formulation strategies. This reflects an industry-wide shift toward durable and expressive finishes. In parallel, chrome yellow and chrome red pigments are projected to be the fastest-growing product types, expanding at an estimated 5.9% CAGR from 2026 to 2033. Their high visibility properties support applications in road markings and safety signage. Infrastructure modernization and stricter visibility standards are expected to underpin continued growth.

End-Use Industry

The construction sector is estimated to command around 39% of the chrome pigment market share in 2026. Expansion of residential, commercial, and public infrastructure continues to drive pigment use in architectural coatings, colored concrete, and exterior finishes. Chrome pigments enhance durability and weather resistance in materials exposed to environmental stress. Longer repainting cycles help reduce lifecycle costs for builders and asset owners. Industry engagement reinforced this trend, as over 25,000 professionals participated in the European Coatings Show 2025, highlighting sustained focus on high-performance and sustainable surface solutions. This engagement underscores the importance of durable pigments in construction applications.

The automotive industry is projected to be the fastest-growing end-use segment, expanding at an estimated 6.1% CAGR through 2033. Growth is supported by rising vehicle production and continued refinishing demand. OEMs and aftermarket players increasingly seek coatings that deliver consistent color retention and corrosion protection over extended service life. Chrome pigments are commonly specified in basecoat and protective clearcoat systems. Their stability under thermal and mechanical stress supports long-term vehicle aesthetics. This positions automotive as a key growth contributor during the forecast period.

Regional Insights

North America Chrome Pigments Market Trends

North America represents a mature and compliance-driven market for chrome pigments characterized by strong emphasis on performance reliability and regulatory adherence. The United States accounts for the majority of regional demand, supported by steady requirements from infrastructure maintenance, automotive refinishing, and industrial coatings applications. Environmental and occupational oversight plays a central role in shaping pigment selection, favoring inorganic materials with proven stability and controlled-use profiles. Demand in the region is largely replacement-driven rather than volume-led. End users prioritize lifecycle performance and regulatory confidence. This market structure supports consistent, predictable consumption patterns.

The U.S. EPA has finalized tighter implementation timelines for chromium-related air toxics monitoring under industrial emissions programs, increasing compliance scrutiny across pigment-adjacent industries. These clarifications prompted coatings and materials suppliers to prioritize pigments with established regulatory histories and transparent documentation. As a result, investment activity increasingly focuses on reformulation, traceability, and process optimization rather than capacity expansion. The growth is expected to remain moderate and value-led, anchored in high-performance and compliance-sensitive applications.

Europe Chrome Pigments Market Trends

In Europe, the market for chrome pigments is greatly shaped by the consistent yet highly tight regulations on chemicals established by the European Union (EU), with Germany, the U.K., France, and Spain serving as key centers of demand. Regulatory harmonization under REACH continues to shape pigment selection and portfolio strategies, favoring compliant chrome oxide formulations. Regional demand for pigments is primarily driven by construction renovation, industrial coatings, and specialty surface applications. Manufacturers operate in a compliance-intensive environment where documentation, lifecycle safety, and controlled-use approvals are critical. Market growth is steady and guided by regulatory adherence, with performance and reliability taking precedence over rapid expansion. End users value technical assurance and long-term product stability.

Recent developments further highlighted Europe’s compliance-driven landscape. Updates to REACH enforcement guidance for chromium-containing substances clarified safety and usage requirements across member states, prompting manufacturers to re-evaluate product portfolios. Companies increasingly focus on process innovation, emission reduction, and documentation to align with regulatory expectations. This approach supports sustained adoption of technically proven pigments in construction and industrial coatings. Market growth is expected to remain steady, with emphasis on reliability, regulatory alignment, and efficiency improvements rather than rapid expansion. European demand continues to favor long-life, high-performance pigments with validated safety profiles.

Asia Pacific Chrome Pigments Market Trends

Asia Pacific is estimated to be both the leading and fastest-growing regional market for chrome pigments, accounting for approximately 42% of the total demand in 2026. This demand is driven by China, India, Japan, and ASEAN economies through rapid urbanization, large-scale infrastructure expansion, and rising domestic coatings production. Chrome pigments are widely adopted in construction materials, industrial coatings, and automotive applications across the region. Cost-efficient manufacturing ecosystems facilitate large-scale pigment utilization, while domestic demand increasingly offsets export reliance. The combination of production capacity, workforce expertise, and industrial diversification positions Asia Pacific as the primary hub for volume consumption.

The growth momentum of the regional market was reinforced by significant government-backed infrastructure allocations, including India’s national infrastructure pipeline and China’s urban redevelopment initiatives. These programs stimulated demand for durable construction materials, long-life coatings, and high-performance pigment formulations. Rising domestic automotive production further supported industrial pigment uptake. Investment trends increasingly focus on capacity expansion, localized sourcing, and downstream integration to meet evolving regional requirements. The Asia Pacific market is projected to display a CAGR of approximately 6.2% from 2026 to 2033, maintaining its position as the principal growth engine for this market.

Competitive Landscape

The global chrome pigments market structure is moderately consolidated, with leading players such as BASF, Lanxess, Tronox, Ferro, and Cristal collectively accounting for a significant portion of market revenue. These established manufacturers leverage their extensive distribution networks, regulatory expertise, and integrated production and supply chain capabilities. They continue to invest heavily in R&D and process innovation to maintain technological leadership in high-performance, low-VOC, and environmentally compliant pigment formulations. Their focus on durability, chemical stability, and color consistency supports adoption across coatings, plastics, ceramics, and automotive applications.

Meanwhile, regional and niche players, including Zibo Aobo Chemical and Anhui Dayi Pigments, concentrate on specialty applications and local markets where cost efficiency and specific pigment grades are critical. Barriers such as stringent regulatory compliance, raw material sourcing, and complex formulation requirements limit new entrants, while digitalization trends and process automation enable smaller companies to enhance production efficiency and traceability. Market consolidation is expected to increase gradually, as leading players pursue capacity expansion, mergers, and strategic partnerships, and collaborate with technology providers to optimize pigment quality, sustainability, and application performance.

Key Industry Developments

- In December 2025, JSW Paints officially completed the acquisition of a 61.2% controlling stake in Akzo Nobel India for an enterprise value of approximately € 1.4 billion (US$ 1.64 billion). The deal gave JSW control over premium brands such as Dulux and strengthened its presence in both decorative and industrial coatings. By integrating liquid paints and coatings operations, JSW positioned itself as the fourth-largest player in the Indian paints industry.

- In October 2025, at the K 2025 trade fair in Düsseldorf, LANXESS highlighted its Colortherm and Bayferrox pigment lines for high-temperature engineering plastics. These pigments withstand processing temperatures above 300°C without color degradation, supporting high-performance applications in polyamide, PPS, and PEEK plastics.

- In March 2025, Sudarshan Chemical Industries Limited (SCIL) completed the acquisition of Germany-based Heubach Group, expanding operations to 19 sites across Europe, the Americas, and Asia Pacific. The acquisition significantly strengthened SCIL’s portfolio in organic and inorganic pigments, positioning it as the world’s second-largest pigment player.

Companies Covered in Chrome Pigments Market

- LANXESS AG

- Shepherd Color Company

- Sudarshan Chemical

- Venator Materials

- BASF SE

- Clariant AG

- Ferro Corporation

- Heubach Group

- DIC Corporation

- Kronos Worldwide

- Toyo Ink SC Holdings

- Sudarshan Chemical

- Cathay Industries

Frequently Asked Questions

The global chrome pigments market is projected to reach US$ 3.7 billion in 2026.

Rising demand for durable coatings, automotive applications, plastics, ceramics, and regulatory-compliant low-VOC pigments are driving the market.

The market is poised to witness a CAGR of 5.3% from 2026 to 2033.

Opportunities exist in infrastructure expansion across developing economies, high-temperature ceramics and glass, and safer pigment reformulations for regulatory compliance.

BASF, Lanxess, Tronox, Ferro, and Cristal are among the leading players in the market.