- Industrial Machinery

- Boiler System Market

Boiler System Market Size, Share, and Growth Forecast 2026 - 2033

Boiler System Market by Boiler Type (Fire-Tube Boilers, Water-Tube Boilers, Electric Boilers, Condensing Boilers, Non-Condensing Boilers, Combination Boilers, Steam Boilers, Hot Water Boilers), Fuel Type (Natural Gas, Coal, Oil, Biomass, Electricity, Hydrogen, Waste Heat, Others), Capacity, Application, Industry, and Regional Analysis, 2026 - 2033

Boiler System Market Size and Trend Analysis

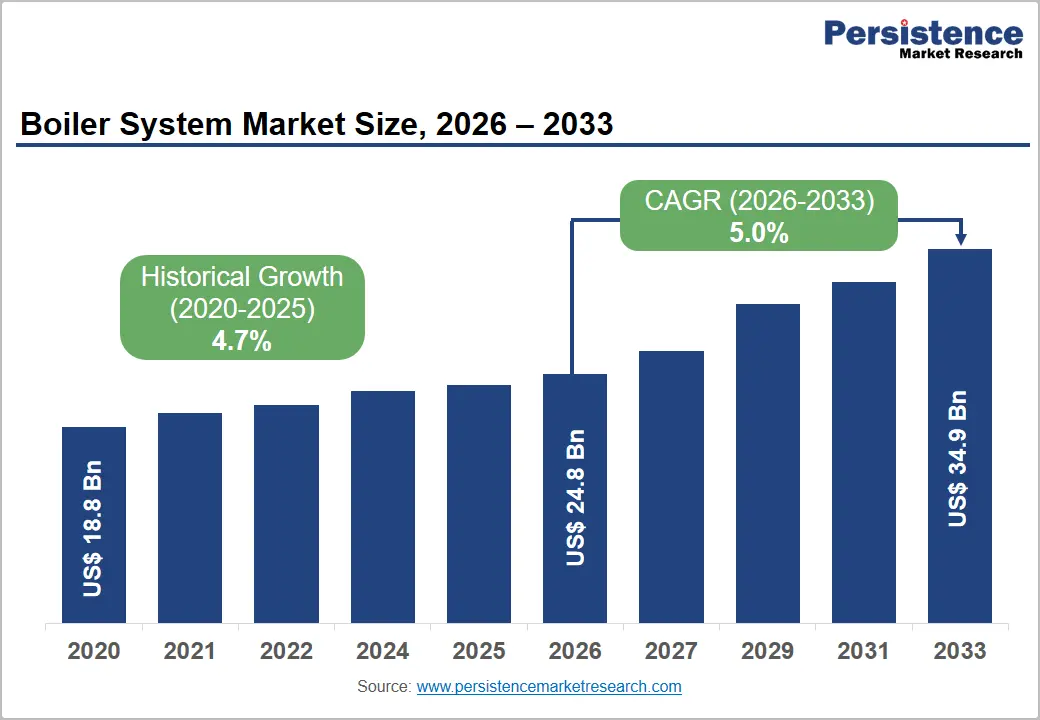

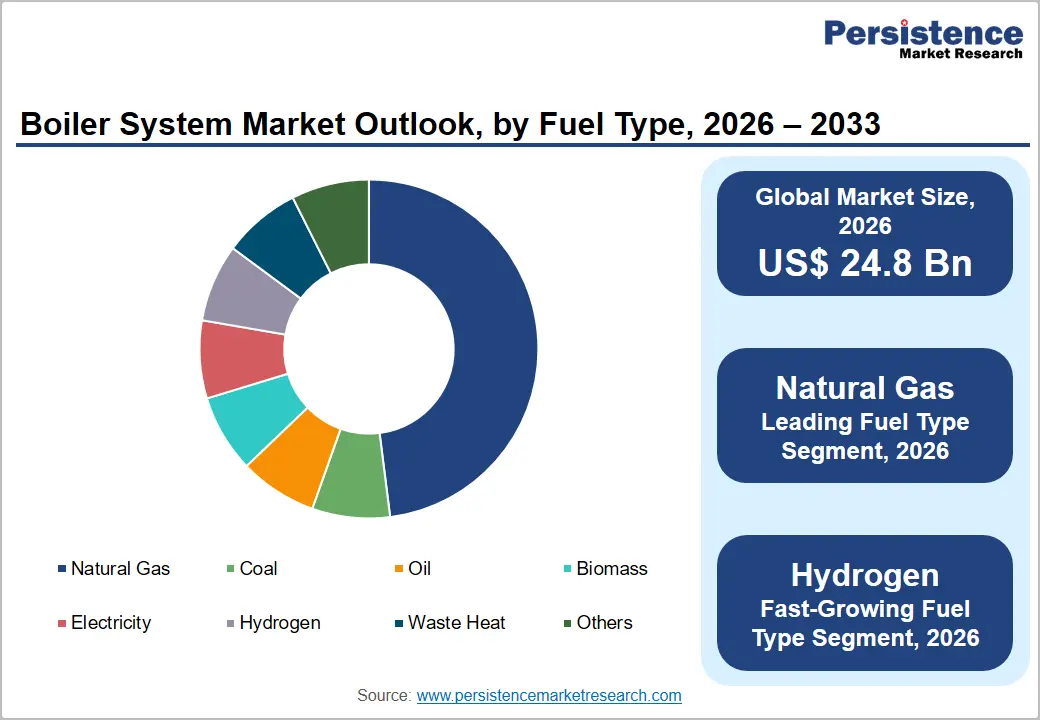

The global boiler system market size is expected to be valued at US$ 24.8 billion in 2026 and projected to reach US$ 34.9 billion by 2033, growing at a CAGR of 5.0% between 2026 and 2033. This expansion is principally driven by accelerating industrial decarbonization mandates, rising demand for energy-efficient heating infrastructure across manufacturing and power generation sectors, and the growing deployment of cogeneration and district heating systems in urbanizing economies.

Tightening European Union emissions regulations, expanding industrial base in Asia Pacific, and government-backed incentives for fuel-switching to low-carbon fuels such as hydrogen and biomass are reinforcing demand across both developed and emerging markets through the forecast period.

Key Industry Highlights:

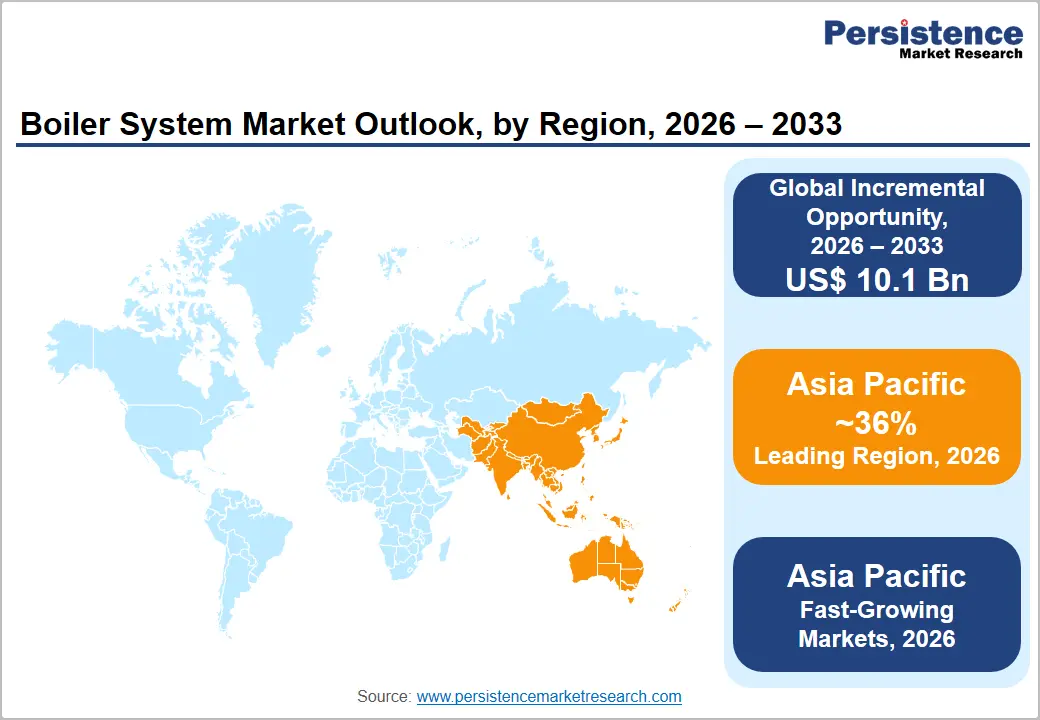

- Leading Region: Asia Pacific leads the global boiler system market with approximately 36% share in 2025, driven by China's vast industrial base, district heating expansion, and India's accelerating industrialization across process-intensive manufacturing sectors.

- Fast-Growing Region: Asia Pacific is also the fast-growing region, projected at a CAGR of ~6.5%, catalyzed by government-backed district heating programs, expanding industrial capacity, and rising adoption of cogeneration infrastructure across China, India, and Southeast Asia.

- Dominant Boiler Type: Fire-tube boilers dominate the boiler type category with approximately 38% share in 2026, sustained by lower capital cost, ease of maintenance, and deep penetration across small-to-medium industrial and commercial applications globally.

- Fastest Growing Fuel Type: Hydrogen-ready boiler systems represent the fastest-growing technology segment, driven by EU REPowerEU hydrogen targets and Japan's hydrogen economy roadmap, creating a concentrated demand window for fuel-flexible combustion system manufacturers by 2033.

- Key Opportunity: The most actionable near-term opportunity is aligning boiler product portfolios with government retrofit incentive programs, including the U.S. IRA and UK Boiler Upgrade Scheme, where subsidy-supported condensing boiler replacement demand is already accelerating in commercial and residential segments.

Market Dynamics

Drivers - Industrial Decarbonization Mandates Driving Boiler Retrofit and Replacement Cycles

For boiler system manufacturers and energy solutions providers, the global industrial decarbonization push is translating directly into a sustained, policy-driven replacement cycle, one that rewards producers capable of offering fuel-flexible, high-efficiency systems over those anchored to conventional fossil-fuel-only designs. European Union's Industrial Emissions Directive (IED) revisions, adopted in 2024, impose significantly stricter NOx and CO2 emission limits on industrial boilers above 1 MW thermal output, compelling operators across chemicals, food processing, and manufacturing sectors to accelerate fleet upgrades ahead of compliance deadlines.

The U.S. Environmental Protection Agency (EPA) similarly tightened its National Emission Standards for Hazardous Air Pollutants (NESHAP) for industrial boilers, creating a regulatory tailwind for high-efficiency condensing and low-emission natural gas boiler systems across North American industry. Manufacturers that invest in modular, fuel-switchable boiler architectures, capable of transitioning from natural gas to hydrogen blends or biomass, are best positioned to capture specification-driven procurement as industrial operators seek future-proof compliance solutions.

Expanding District Heating Networks and Cogeneration Infrastructure in Emerging Economies

The accelerating buildout of district heating and combined heat and power (CHP) infrastructure across China, India, South Korea, and Eastern Europe is generating a structural, multi-year demand corridor for large-capacity industrial boiler systems that market participants cannot afford to overlook. China's 14th Five-Year Plan for Energy explicitly targets the expansion of district heating coverage across northern cities, committing to supply reliable heating to an additional 100 million urban residents by 2025, a goal that requires substantial procurement of industrial water-tube and hot water boiler systems.

The International Energy Agency (IEA) estimates that district heating currently supplies approximately 10% of global space heating demand, but that this share must nearly double by 2030 under net-zero pathways, a volume expansion that translates into sustained procurement of high-capacity boiler systems. Boiler manufacturers with established project execution capabilities in large-scale CHP and district energy applications, including Babcock & Wilcox, Mitsubishi Heavy Industries, and ANDRITZ AG, are uniquely positioned to capture this demand wave as government infrastructure spending accelerates through the late 2020s.

Restraints - Stringent Emissions Regulations Increasing Compliance Costs for Operators and Manufacturers

While decarbonization mandates create a replacement demand opportunity, they simultaneously impose a structural cost burden on boiler system operators and manufacturers that constrains near-term margin expansion and market entry. Compliance with tightening NOx, SO2, and particulate emission standards requires operators to invest in catalytic reduction systems, flue gas desulfurization equipment, and continuous emission monitoring infrastructure, investments that can add 15-25% to the total installed cost of a new industrial boiler system, according to assessments by the European Cement Association (CEMBUREAU) and comparable industrial sector analyses.

For manufacturers, the engineering complexity of building emission-compliant systems across multiple regulatory jurisdictions, each with distinct limit values and testing protocols, elevates product development costs and extends qualification timelines, creating a barrier that disproportionately disadvantages smaller regional producers relative to global majors such as Bosch Industriekessel and Siemens Energy that can amortize compliance R&D across larger revenue bases.

High Capital Expenditure and Long Replacement Cycles Suppress New Unit Demand

The boiler system market's growth is structurally moderated by the industry's inherent capital intensity and the long operational life of installed equipment, factors that constrain the frequency and volume of new unit procurement and dampen market velocity. Industrial-grade water-tube boilers capable of outputs above 50 MMBtu/hr carry installed costs that routinely exceed US$ 2-5 million per unit, including auxiliary systems, engineering, and commissioning, a capital commitment that most operators defer unless driven by regulatory mandates or catastrophic equipment failure.

Boiler systems in industrial applications typically carry design lifespans of 25-35 years, and operators routinely extend service life further through maintenance and component replacement, compressing the addressable replacement market in any given year. This dynamic forces manufacturers to compete aggressively on service contracts, spare parts, and efficiency upgrade packages, revenue streams that carry lower margins than new equipment sales, while awaiting the periodic fleet renewal events that generate large-volume procurement opportunities.

Opportunities - Hydrogen-Ready and Fuel-Flexible Boiler Systems for Industrial Decarbonization

The development and commercialization of hydrogen-ready boiler systems represents one of the most strategically significant near-term opportunities in the global boiler market, as industrial operators across Europe, Japan, and South Korea move to secure heating infrastructure that can transition seamlessly as hydrogen supply chains mature. The European Commission's REPowerEU Plan commits to producing 10 million tonnes of domestic green hydrogen and importing an additional 10 million tonnes annually by 2030, explicitly targeting industrial heat applications, including process steam generation, as a primary decarbonization pathway.

Boiler manufacturers, including Bosch Industriekessel and Miura Co., Ltd., have already demonstrated prototype hydrogen-blended combustion systems capable of operating on hydrogen fractions up to 30% with minimal modification to existing burner assemblies, establishing a credible near-term migration pathway for industrial clients.

Companies that invest now in certifying hydrogen-compatible burner systems, developing multi-fuel combustion controls, and building service infrastructure for hydrogen boiler operation will capture early-mover specification advantages as hydrogen injection mandates roll out across EU member states and Japan's hydrogen society roadmap advances. This opportunity is time-sensitive: operators making capital procurement decisions in 2025-2028 will select the boiler platforms that define their heating infrastructure through the 2040s.

Condensing Boiler Adoption in Commercial and Residential Retrofit Programs

Government-backed retrofit programs across North America and Europe are creating a concentrated, time-bounded demand window for condensing boiler manufacturers, one that rewards producers with established distribution networks, contractor training programs, and product lines certified under evolving energy efficiency standards.

The U.K.'s Heat and Buildings Strategy mandates the phase-out of new natural gas boiler installations in residential properties by 2035, creating near-term demand for high-efficiency condensing boilers as an interim bridge technology while heat pump infrastructure scales. Germany's Gebaudeenergiegesetz (GEG) similarly incentivizes condensing boiler upgrades in the existing building stock as part of the country's building decarbonization pathway.

The U.S. Inflation Reduction Act (IRA) provides tax credits of up to US$ 600 per unit for high-efficiency boiler replacements in residential applications, channeling meaningful demand toward Energy Star-certified condensing units through at least 2032. Manufacturers that align product portfolios with these subsidy frameworks, build installer certification programs, and invest in digital customer acquisition channels are positioned to capture substantial retrofit volumes across a policy-supported demand cycle that is already underway.

Category-wise Analysis

Boiler Type Insights

Fire-tube boilers lead the global boiler system market with approximately 38% market share in 2025 due to their extensive adoption across commercial buildings and small-to-medium industrial facilities. These boilers are widely preferred for applications in food processing, textiles, pharmaceuticals, and commercial heating because of their simple design, lower installation costs, and operational reliability. Their ability to operate with multiple fuel types, including natural gas, oil, and biomass, further strengthens market demand across diverse end-use sectors.

Fire-tube boilers also require comparatively lower maintenance and are easier to install within existing facility infrastructure, making them attractive for replacement and retrofit projects. Strong regulatory familiarity and established certification standards across North America and Europe continue to support procurement confidence, sustaining the segment’s dominance in industrial and commercial heating applications globally.

Fuel Type Insights

Natural gas is likely to dominate the fuel type segment with approximately 44% share in 2026, supported by its widespread pipeline infrastructure, cleaner combustion profile, and strong compatibility with modern industrial boiler systems. Industries such as chemicals, food processing, manufacturing, and commercial facilities continue to prefer natural gas due to its high energy efficiency and relatively lower emissions compared to coal and oil-based alternatives.

The availability of extensive gas distribution networks across North America, Europe, and East Asia significantly reduces fuel supply risks and operating complexity for industrial users. Natural gas boilers are also compatible with low-NOx burner technologies, helping facilities comply with increasingly stringent environmental regulations. Rising industrialization and the modernization of heating infrastructure in developing economies are further supporting demand for natural gas-fired boiler systems across commercial and industrial applications worldwide.

Capacity Insights

The 10-50 MMBtu/hr segment leads the boiler system market with approximately 35% share in 2026 due to its suitability for a broad range of industrial and commercial operations. This capacity range is widely utilized in food and beverage processing, pharmaceuticals, chemicals, district heating systems, and medium-scale manufacturing facilities that require stable steam and heat generation. The segment offers an effective balance between operational efficiency, installation flexibility, and manageable infrastructure requirements, making it highly attractive for both new installations and replacement projects.

Boilers within this range can typically be integrated into existing boiler houses without extensive structural modifications, reducing capital expenditure for end users. Growing industrial activity in emerging economies and the expansion of medium-scale production facilities continue to support procurement demand for boiler systems within this capacity category.

Application Insights

Steam generation remains the leading application segment in the boiler system market with approximately 32% share in 2026, reflecting its critical role across industrial manufacturing and process industries. Steam is extensively used for sterilization, drying, heating, cleaning, and temperature control in sectors such as food and beverage, pharmaceuticals, chemicals, petrochemicals, and pulp and paper.

The widespread integration of steam distribution systems within industrial facilities has created long-term replacement and maintenance demand for boiler systems. Steam also remains one of the most efficient and reliable mediums for transferring thermal energy in industrial operations. Industrial expansion across the Asia Pacific, coupled with increasing demand for process automation and production efficiency, continues to support investment in steam generation infrastructure. The segment’s importance is further reinforced by rising energy efficiency initiatives and the modernization of industrial heating systems globally.

Industry Insights

Power generation leads the industry segment with approximately 26% share in 2026 due to the extensive deployment of large-capacity boiler systems in thermal power plants and industrial cogeneration facilities. Boiler systems are essential for steam production in coal-fired, gas-fired, and biomass-based electricity generation processes, supporting a continuous power supply for industrial, commercial, and residential consumption. The sector benefits from the long operational life and high replacement value of utility-scale boilers, which generate significant procurement opportunities over time.

Rapid electricity demand growth across the Asia Pacific, particularly in China and India, continues to support investments in thermal power infrastructure despite the ongoing energy transition. Upgrades to existing power plants, efficiency improvement programs, and expansion of industrial cogeneration facilities are also contributing to sustained demand for advanced boiler systems in the global power generation sector.

Regional Insights

North America Boiler System Market Trends and Insights

North America holds approximately 27% of the global boiler system market in 2026, driven by a mature installed base of industrial and commercial boiler systems, ongoing replacement cycles spurred by EPA emission compliance mandates, and strong demand from the oil & gas, chemicals, and food & beverage sectors.

The U.S. Inflation Reduction Act (IRA) has catalyzed condensing boiler retrofit activity in commercial buildings, while industrial decarbonization incentives are directing capital toward low-emission natural gas and hydrogen-compatible boiler upgrades. The region is moving toward fuel-flexible system procurement, and manufacturers that align product portfolios with federal and state incentive frameworks are positioned to capture above-average revenue growth.

U.S. Boiler System Market Size

The United States accounts for approximately 80% of North America's boiler system market in 2025, underpinned by the country's vast industrial manufacturing base, a regulatory environment actively incentivizing efficiency upgrades, and high replacement demand driven by aging boiler infrastructure. IRA tax credits and DOE advanced manufacturing programs are directing meaningful capital toward high-efficiency and low-emission boiler upgrades in commercial and industrial facilities.

Europe Boiler System Market Trends and Insights

Europe represents approximately 24% of the global share in 2026, shaped by one of the world's most rigorous industrial emissions regulatory environments and a clear policy trajectory toward fossil fuel phase-out in heating applications. The EU Industrial Emissions Directive, REPowerEU hydrogen targets, and national building decarbonization programs in Germany, the U.K., and France are collectively driving a technology upgrade cycle that is restructuring boiler procurement toward high-efficiency condensing systems, biomass-fueled boilers, and hydrogen-ready platforms.

European market participants should anticipate an accelerating shift away from conventional gas boilers in both residential and commercial segments as policy timelines for fossil heating phase-out firm up through the late 2020s.

Germany Boiler System Market Size

Germany accounts for approximately 22% of Europe's boiler system market in 2026, anchored by the country's substantial industrial manufacturing base, spanning automotive, chemicals, and metals sectors, and a residential and commercial heating sector undergoing structured decarbonization under the Gebaudeenergiegesetz (GEG). Demand for high-efficiency condensing boilers and biomass systems is rising as operators navigate compliance timelines. Germany's trajectory toward hydrogen heating infrastructure positions it as the region's leading market for hydrogen-ready boiler system adoption in the coming years.

U.K. Boiler System Market Size

The U.K. represents approximately 16% of Europe's boiler system market in 2026, with demand shaped by the government's Heat and Buildings Strategy mandating the phase-out of new gas boiler installations by 2035 and ongoing incentives for efficiency upgrades through the Boiler Upgrade Scheme (BUS). Commercial and light-industrial condensing boiler replacement activity is robust. The U.K. market is expected to experience a concentrated demand peak for high-efficiency gas condensing boilers in the 2026 - 2033 window before heat pump adoption begins to displace incremental boiler procurement.

France Boiler System Market Size

France holds approximately 13% of Europe's boiler system market in 2026, supported by a large residential and commercial building stock with extensive legacy gas boiler installations and government programs, including the MaPrimeRenov scheme incentivizing energy-efficient heating upgrades. Industrial demand from the country's chemicals, food processing, and aerospace manufacturing sectors provides a stable base of process boiler procurement. France's market is forecast to grow steadily, driven by building retrofit activity and gradual industrial fuel-switching toward biomass and hydrogen-compatible boiler systems.

Asia Pacific Boiler System Market Trends and Insights

Asia Pacific is the largest and fastest-growing regional market, accounting for approximately 36% of global boiler system demand in 2026. The region's growth is propelled by China's vast industrial manufacturing base and ambitious district heating expansion, India's accelerating industrialization across chemicals, pharmaceuticals, and food processing sectors, and Southeast Asia's growing power generation and process industry infrastructure. China dominates regional volume, operating the world's largest installed base of industrial and utility boiler systems, while India and South Korea are among the fastest-growing national markets. Companies seeking to scale in Asia Pacific must invest in localized manufacturing, competitive pricing strategies, and relationships with EPC contractors active in large industrial and infrastructure projects.

India Boiler System Market Size

India accounts for approximately 16% of Asia Pacific's boiler system market in 2025, driven by rapid industrial capacity expansion in pharmaceuticals, chemicals, food & beverage, and textiles, all process-intensive sectors with high steam and heat demand. Government initiatives including the Production Linked Incentive (PLI) scheme are accelerating domestic manufacturing investment that directly drives boiler procurement. India's market is among the region's fastest-growing, with domestic producers Forbes Marshall and Thermax Ltd. well-positioned to capture rising national demand through competitive pricing and strong aftermarket service networks.

Japan Boiler System Market Size

Japan represents approximately 12% of Asia Pacific's boiler system market in 2026, with demand concentrated in the country's highly automated manufacturing sector, spanning automotive, electronics, and precision machinery, where process steam reliability is a non-negotiable production requirement. Japan's advanced hydrogen economy roadmap, backed by the Ministry of Economy, Trade and Industry (METI), is positioning the country as an early adopter of hydrogen-ready industrial boiler systems. Miura Co., Ltd. and IHI Corporation are key domestic producers with global technology reputations in compact, high-efficiency boiler systems.

South Korea Boiler System Market Size

South Korea accounts for approximately 9% of the Asia Pacific's boiler system market in 2026, supported by strong industrial demand from the country's petrochemicals, shipbuilding, steel, and semiconductor manufacturing sectors, all of which require reliable, high-pressure steam and process heat infrastructure. South Korea's government hydrogen strategy and K-ETS (Korean Emissions Trading Scheme) carbon pricing are creating policy incentives for industrial boiler operators to transition toward low-carbon fuel alternatives, driving near-term investment in fuel-flexible and hydrogen-compatible system upgrades.

Competitive Landscape

The global boiler system market is moderately consolidated at the premium large-capacity tier, where Babcock & Wilcox, Mitsubishi Heavy Industries, Siemens Energy, ANDRITZ AG, and General Electric compete on engineering depth, project execution capability, and long-term service relationships with utility and heavy industrial clients. Scale rewards incumbents in this tier through capital-intensive certification processes, long qualification cycles with major EPC contractors, and service infrastructure that creates structural switching costs.

The mid-market, serving commercial and light-industrial applications, is fragmented and price-sensitive, with regional specialists such as Cleaver-Brooks, Miura, Fulton Boiler Works, and Hurst Boiler & Welding competing primarily on total cost of ownership, lead time, and installer network reach. Key differentiators among leaders include fuel flexibility credentials, hydrogen-readiness certification, digital remote monitoring platforms, and aftermarket service depth. A dominant emerging theme is the shift toward boiler-as-a-service and energy performance contracting models, where manufacturers assume operational risk in exchange for long-term margin-rich service revenues.

Key Developments:

- July 2025: Rheem launched its FT Series super high-efficiency condensing boilers featuring up to 95% AFUE performance, ultra-low NOx emissions, touchscreen controls, and compact designs for residential and commercial heating applications.

- July 2025: Navien introduced the NCB500 System Boiler featuring compact installation, stainless steel heat exchangers, smart control compatibility, LPG conversion capability, and high-efficiency condensing technology designed for modern residential heating applications.

- February 2025: Nyle Water Heating Systems launched the industry’s first commercial heat pump boiler designed as a direct replacement for hydronic fossil-fuel boilers, delivering high-temperature water, lower emissions, and reduced retrofit costs for commercial buildings.

Companies Covered in Boiler System Market

- Bosch Industriekessel

- Babcock & Wilcox Enterprises

- Mitsubishi Heavy Industries

- Siemens Energy

- Cleaver-Brooks

- Fulton Boiler Works

- Hurst Boiler & Welding

- General Electric

- ANDRITZ AG

- Forbes Marshall

- Thermax Ltd.

- Miura Co., Ltd.

- IHI Corporation

- Johnston Boiler Company

- Harbin Electric Boiler Co.

- Viessmann Group

- Vaillant Group

- Alfa Laval AB

- Trane Technologies

- Yokogawa Electric Corporation

Frequently Asked Questions

The global Boiler System market is valued at US$ 24.8 billion in 2026 and is projected to reach US$ 34.9 billion by 2033, growing at a CAGR of 5.0%.

Demand is driven by industrial decarbonization initiatives and expanding district heating and cogeneration infrastructure.

Asia Pacific leads the market with around 36% share due to rapid industrialization and infrastructure expansion.

Hydrogen-ready and fuel-flexible boiler systems represent a major growth opportunity for industrial decarbonization.

Key players include Bosch Industriekessel, Babcock & Wilcox Enterprises, Mitsubishi Heavy Industries, Thermax Ltd., Cleaver-Brooks, and Miura Co. Ltd.