- Industrial Machinery

- Blast Monitoring Equipment Market

Blast Monitoring Equipment Market Size, Share, and Growth Forecast for 2024 - 2031

Blast Monitoring Equipment Market by Product (Blast Monitors, Real-time Dust Monitors, Dust Samplers, Visibility Monitors), End Use (Defense, Chemicals), Application (Underground Mines, Surface Mining), and Regional Analysis from 2024 to 2031

Blast Monitoring Equipment Market Size and Share Analysis

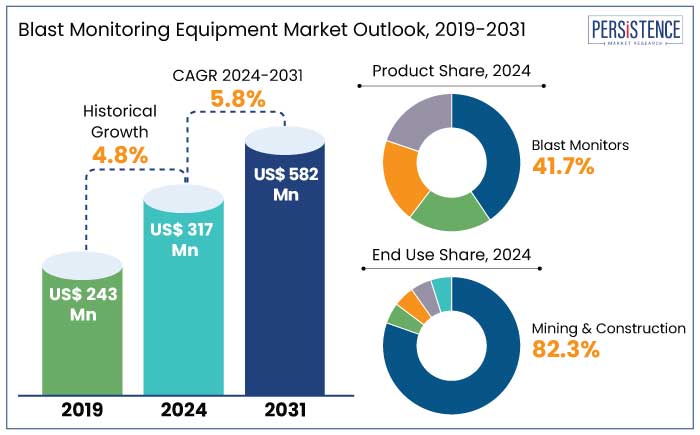

The global blast monitoring equipment market is projected to witness a CAGR of 5.8% during the forecast period from 2024 to 2031. It is anticipated to increase from US$ 317 Mn recorded in 2024 to a decent US$ 582 Mn by 2031.

Blast monitoring equipment are specialized instruments designed to measure, record, and analyze the effects of explosive activities, including mining operations, construction blasts, and military exercises. These devices, such as air overpressure sensors, noise level monitors, seismometers, and data loggers, are essential for ensuring safety, regulatory compliance, and environmental protection. By providing precise and real-time data, blast monitoring technology also enables the design of more efficient and controlled blasting processes that minimize disruption to surrounding environments.

Demand for blast monitoring equipment has continued to rise, driven by strict safety regulations and rising environmental conservation measures. Governments worldwide are implementing stringent rules in industries like mining, construction, and defense to mitigate risks associated with explosive activities. These efforts are aligned with increasing global awareness of the environmental and societal impacts of blasts, leading to broader adoption of unique monitoring technologies.

Rising urbanization and large-scale infrastructure development projects remain a significant factor driving the market. According to the World Bank, Private Participation in Infrastructure (PPI) investments in 2023 amounted to US$ 86.0 Bn, representing 0.2% of the GDP of all low- and middle-income countries.

While this figure reflects a slight decrease from US$ 91.3 Bn in 2022, it marginally surpassed the five-year average (2018 to 2022) of US$ 85.5 Bn. This trend highlights the persistent demand for controlled blasting in infrastructure development despite economic fluctuations.

Key Highlights of the Market

- East Asia is likely to exhibit a CAGR of 5.8% through 2031, driven by its vast mining operations and a significant role in mineral production.

- The Middle East and Africa is the fastest-growing region, with a CAGR of 6.5% through 2031. This growth is fueled by investments in mining and infrastructure development in countries like Saudi Arabia and the United Arab Emirates.

- By end use, the mining and construction segment, with a CAGR of 5.5% through 2031, is driven by rising demand for raw materials, booming of mining activities, and increasing safety regulations.

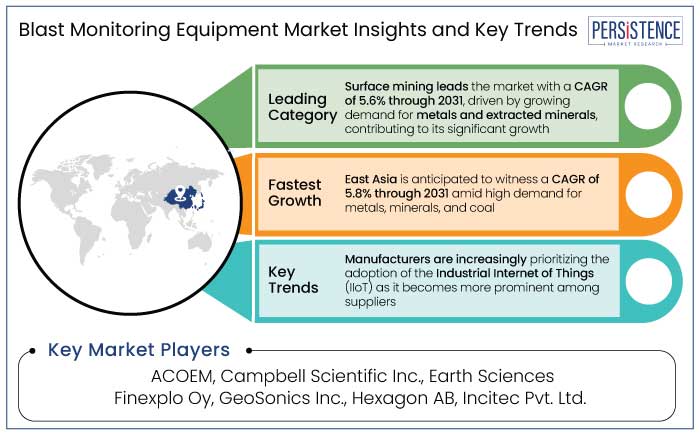

- Surface mining application is set to surge at a CAGR of 5.6% through 2031, supported by high demand for metals and minerals and innovations in mining technologies.

- High demand from the construction and mining sectors is a primary driver, with construction blasting activities significantly increasing demand for industrial explosives and monitoring equipment.

- Based on product, the blast monitors segment will likely hold a share of 41.7% in 2024.

- Key investments in mining and infrastructure projects globally are pushing demand for blast monitoring systems.

|

Market Attributes |

Key Insights |

|

Blast Monitoring Equipment Market Size (2024E) |

US$ 317 Mn |

|

Projected Market Value (2031F) |

US$ 582 Mn |

|

Global Market Growth Rate (CAGR 2024 to 2031) |

5.8% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

4.8% |

East Asia Sees Steady Growth Amid Increasing Production of Coal and Metals

East Asia will likely witness a CAGR of 5.8% through 2031 and hold a share of 39.3% in 2024. China is a dominant player in the region due to its substantial contribution to industrialization, construction, and mining activities.

The country’s rapid economic growth has driven significant demand for metals, minerals, and coal. China is the world’s most prominent producer and consumer of coal and a leading producer of over 20 key minerals. These include aluminum, cement, gold, graphite, iron and steel, lead, magnesium, rare earths, and zinc. For example,

- According to the United States Geological Survey, China has accounted for 40 to 50% of global demand for minerals over the past three decades.

While significant amounts of minerals are imported, domestic production forms a substantial part of the supply for almost all commodities. The mining sector in China is vast, with over 1,500 key mining operations, about 75% of which are underground.

- The industry produces over US$ 400 billion Bn, and in 2020, national resources tax revenues totaled US$ 27 Bn (RMB 175.5 Bn), accounting for 1.1% of the national tax revenues.

- China spends around US$ 200 Bn per year on mine supply and services.

- In the past decade, the government has implemented policies to promote green mines construction, resulting in 1,254 mining companies being listed on the national green mine directory by 2021.

- With almost 40,000 mines, the green mining sector presents significant opportunities for international companies.

China has identified 71 demonstration projects on intelligent mines nationwide, with the coal mine stock processing market alone potentially reaching trillions of RMB, and the intelligent equipment market estimated at RMB 800 Bn. As the non-coal sector continues to surge, China’s green mining industry is set to surge by 30% to 50% in the next 20 years, underscoring its key role in East Asia.

Investments in Significant Minerals to Create Opportunities in Middle East and Africa

In the Middle East and Africa, the blast monitoring equipment market is estimated to exhibit a CAGR of around 6.5% through 2031. This growth is driven by substantial investments in mining projects and infrastructure development. For example,

- In the Middle East, Saudi Arabia is making key investments in critical minerals like copper, lithium, nickel, and iron ore. Its US$ 15 Bn commitment to global mining projects provides a strategic opportunity for the U.S. to reduce its reliance on China.

- Saudi Arabia’s US$ 2.5 Bn stake in Vale Base Metals and its investments in copper and nickel projects globally are key to decreasing U.S. dependence on China’s firms.

The United Arab Emirates is also playing a significant role, with the International Holding Company (IHC) anticipated to sign US$ 1 Bn in mining deals this year alone. It includes acquisitions of Zambia’s copper mines and joint ventures for iron ore in Angola, along with discussions for nickel mines in Burundi, Kenya, and Tanzania.

Such developments position the United Arab Emirates as a competitor to China in Africa. The U.S. remains heavily reliant on China for 24 out of 50 critical minerals identified by the U.S. Geological Survey. However, forging new partnerships, especially with GCC nations, Saudi Arabia, United Arab Emirates, Qatar, and Oman, provides an opportunity to access resource-rich markets and reduce this dependence. As a result, the Middle East and Africa is the fastest-growing region for the blast monitoring equipment industry.

Mining and Construction Leads with Booming Underground Mining Operations

In terms of end use, the mining and construction category is anticipated to lead in the foreseeable future by witnessing a CAGR of around 5.5%. The segment is likely to hold a share of 82.3% in 2024. This is due to the significant scale and growth of mining activities worldwide, driven by increasing demand for raw materials and minerals across industries.

- According to the World Mining Data 2023, global mining production has been steadily rising, with over 17.9 billion tons of minerals extracted annually, reflecting the sector's expansive operations.

Surging underground and surface mining operations is a key factor driving demand for blast monitoring equipment. For instance,

- The global surface mining market is projected to rise at a CAGR of 3.4% from 2023 to 2030, as industries like construction, manufacturing, and energy rely heavily on mined resources.

Countries with significant mining operations, such as China, Australia, India, and Brazil, are investing heavily in modernizing their mining infrastructure, including adoption of unique monitoring equipment. Demand for precision in managing ground vibrations, air overpressure, and seismic activity is further set to create new opportunities. In addition, strict safety regulations globally are anticipated to reinforce the segment’s dominance.

Surface Mining Dominates Owing to High Demand for Extracted Minerals

Based on application, the surface mining segment is projected to exhibit a CAGR of 5.6% during the period from 2024 to 2031. It is anticipated that the segment will hold a share of 60% in 2024.

It is driven by increasing demand for metals and extracted minerals. According to recent statistics, surface mining accounted for over 60% of the total market share. For example,

- Global coal production in 2023 is projected to have risen by 1.8%, reaching an all-time high of 8,741 million tons, with substantial contributions from India, China, and Indonesia. Additionally, total worldwide copper mine production amounted to around 22 million metric tons in 2023.

The aforementioned figures underscore the robust demand for extracted minerals, further fueling growth of the surface mining segment. Moreover, innovations in surface mining techniques, such as the use of highly efficient equipment and technologies like draglines, hydraulic shovels, and conveyor systems, have significantly improved productivity, reduced operational costs, and enhanced safety. These innovations make surface mining the preferred method for extracting minerals, driving its dominance in the market.

Market Introduction and Trend Analysis

The global market for explosion monitoring equipment is seeing notable trends among manufacturers and suppliers. Companies like Orica Limited, Instantel Inc., and Campbell Scientific Inc. are driving the market forward.

They are introducing novel technology for applications in surface mining, underground mining, detonation, and demolition activities. A key trend among these manufacturers is the integration of Internet of Things (IoT) into their blast monitoring equipment, enabling real-time data collection and remote monitoring. This development enhances safety and operational efficiency, allowing manufacturers to provide smarter, more reliable solutions to their clients.

Adoption of the Industrial Internet of Things (IIoT) is becoming increasingly prominent among suppliers. By incorporating IIoT into existing manufacturing processes, suppliers can connect multiple sensors, such as those for explosion, vibration, and temperature monitoring, to the Internet.

It would help in enabling real-time asset monitoring and predictive maintenance. This integration not only improves the efficiency and reliability of operations but also allows manufacturers to offer innovative business process automation solutions.

Growing use of IIoT in industries like manufacturing and oil and gas is driving a significant shift in the blast monitoring equipment market. Suppliers are likely to capitalize on these trends to enhance their product offerings and meet evolving customer demands.

Historical Growth and Course Ahead

The global blast monitoring equipment industry recorded a decent CAGR of 4.8% in the historical period from 2019 to 2023. The industry has seen steady growth in recent years. It is mainly driven by increasing safety regulations and the need for more precise monitoring of blasting activities in industries like mining, construction, and quarrying.

Historically, the market grew at a moderate pace, with developments in sensor technologies and real-time data analytics playing a key role in improving blast control and reducing environmental impact. As regulatory pressures intensify, especially regarding environmental concerns and worker safety, demand for unique monitoring solutions continues to rise.

Sales of blast monitoring equipment are estimated to record a CAGR of 5.8% during the forecast period between 2024 and 2031. The industry is poised for significant growth, driven by innovations in IoT-enabled sensors, automation, and AI-based analytics. These offer more accurate, efficient, and cost-effective monitoring solutions.

Market Growth Drivers

High Demand from Construction and Mining Sectors to Boost Sales

Increasing demand from the construction and mining sectors across the globe is a key driver for the blast monitoring equipment market growth. Rise in construction blasting activities has significantly increased demand for industrial explosives, which are closely linked to the mining sector.

The imbalance between supply and demand for raw materials such as coal for electricity production, iron ore for steel production, limestone for cement production, and aggregates from quarries, especially for mining and infrastructure projects, is substantial. As population density rises, construction activities such as drilling and blasting intensify, driving the need for blast monitoring systems.

Growth in the mining and construction sectors, which is directly proportional to the demand for blast monitoring equipment, fuels the market. Moreover, rising number of infrastructure developments, including roads, tunnels, and bridges, which often involve blasting, further contribute to market growth. For instance,

- In 2021, Europe’s government planned to invest around US$ 339.72 Bn for the development of roads and the construction sector. These factors are likely to impact growth of the blast monitoring equipment industry during the forecast period.

Rising Emphasis on Safety and Regulatory Compliance to Propel Demand

One of the main factors driving demand for blast monitoring systems is the increased focus on safety and regulatory compliance. Commonly used in sectors like mining, building, and quarrying, blasting activities carry several serious concerns. These include flying debris, structural damage, ground vibrations, and noise pollution. These risks have the ability to negatively impact the environment in addition to endangering the security of the workforce and surrounding communities.

Strict regulations are being introduced by governments and regulatory agencies around the world to guarantee that blasting operations are carried out safely and with the least amount of impact possible. For instance,

- Mining operators are required under the U.S. Surface Mining Control and Reclamation Act (SMCRA) to keep an eye on and manage the effects of their blasting operations on the environment and public safety.

- Similar to this, the Department of Mines, Industry Regulation and Safety (DMIRS) in Australia enforces strict blasting rules to control the hazards of air overpressure and ground vibrations.

Market Restraining Factors

Lack of Skilled Operators to Hamper Demand in Developing Countries

Lack of skilled operators in developing nations poses a significant restraint to the market for explosion monitoring equipment. The impact of regulatory codes of practice, combined with a shortage of skilled technical resources in data processing, further limits adoption of these systems.

There is also a knowledge gap regarding the long-term maintenance of explosion monitoring equipment. It can lead to maintenance failures, difficulties in explosion measurements, and the risk of false explosion signals.

Experienced users often question the diagnostic capabilities and predictive accuracy of these systems, creating challenges in ensuring process efficiency. Additionally, workers may resist new methods of planning and maintaining process efficiency. It is anticipated to impede the effective implementation of explosion protection equipment.

Demand for explosion monitoring equipment may decline due to these challenges, especially in production settings where the installation of these systems is complex. Liability issues related to the predictive capabilities of control systems are a significant barrier to industry growth, further constraining the market.

Key Market Opportunities

Emergence of IoT and IIoT Technologies to Forge Growth Opportunities

One of the main opportunities for manufacturers and suppliers in the global blast monitoring equipment market lies in the rising adoption of unique technologies such as the Internet of Things (IoT) and the Industrial Internet of Things (IIoT). These technologies enable real-time data collection, remote monitoring, and predictive maintenance, which enhance operational efficiency and safety across various mining and construction activities.

Manufacturers can capitalize on this opportunity by integrating IoT and IIoT solutions into their equipment, offering enhanced features such as data analytics, automated alerts, and predictive maintenance capabilities. This trend not only meets the evolving demands of the mining industry but also positions manufacturers to differentiate themselves in a competitive market. It helps in providing innovative solutions that improve productivity and safety in mining operations globally.

Competitive Landscape for the Blast Monitoring Equipment Market

The competition in the blast monitoring equipment market is highly dynamic, driven by continuous developments and innovations from leading players. Key manufacturers and suppliers such as Orica Limited, Instantel Inc., Campbell Scientific Inc., Yokogawa Electric Corporation, Hexagon AB, and Trolex Ltd are at the forefront of this competitive landscape.

Leading companies are introducing cutting-edge solutions, such as Yokogawa’s explosion-protected wireless steam trap monitoring device and Hexagon’s AI-powered 3D Blast Movement Intelligence (BMI). These technologies enhance blast movement monitoring and safety in mining operations, setting new standards in the market.

Other recent innovations include Orica’s Fortis Protect Series of explosives and Trolex Ltd’s Air XS Silica Monitor, both enhancing operational efficiency and safety. Additionally, Blast Movement Technologies’ FED 2.0 vibration monitor exemplifies the trend toward safer, more integrated solutions for blast monitoring activities.

Such a dynamic environment fosters continuous growth and evolution in the market. Leading companies are competing through technological innovation, safety improvements, and meeting stringent regulatory requirements.

Recent Industry Developments

- In 2024, Japan-based Yokogawa launched an explosion-protected wireless steam trap monitoring device with excellent environmental resistance and wide-area coverage.

- In 2024, Sweden-based Hexagon released its AI-powered 3D blast movement solution, the Hexagon Blast Movement Intelligence (BMI), on a global scale. This innovative technology leverages artificial intelligence to enhance the monitoring and management of blast movement, improving safety and efficiency in mining operations.

Blast Monitoring Equipment Industry Segmentation

By Product

- Blast Monitors

- Real-time Dust Monitors

- Dust Samplers

- Visibility Monitors

By End Use

- Defense

- Chemicals

- Mining and Construction

- Oil and Gas

- Others

By Application

- Underground Mines

- Surface Mining

- Demolition

- Detonation

- Rock Blasting

- Others

By Region

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East and Africa

Companies Covered in Blast Monitoring Equipment Market

- ACOEM

- Campbell Scientific Inc.

- Earth Sciences

- Finexplo Oy

- GeoSonics Inc.

- Hexagon AB

- Incitec Pvt. Ltd.

- Instantel

- MREL

- Orica Limited

- RST Instruments Ltd.

- Sigicom Engineering GmbH

- Stanley Black and Decker

- Svib Software technologies Pvt Ltd.

- Syscom Instruments SA

- Terrock Pty Ltd.

- Trolex ltd.

- Libelium Comunicaciones Distribuidas

Frequently Asked Questions

Yes, the market is set to reach US$ 582 Mn by 2031.

Mining and construction industries are the main industries that companies need to target.

East Asia is set to witness a CAGR of 5.8% through 2031.

The surface mining application is projected to rise at a CAGR of 5.6% through 2031.

Opportunities include the rising adoption of IoT and IIoT technologies for real-time data collection and predictive maintenance.