- Sensors & Controls

- Battery-free Sensors Market

Battery-free Sensors Market Size, Share, and Growth Forecast, 2026 - 2033

Battery-free Sensors Market by Frequency (High Frequency, Motion & Position, Others), Sensor Type (Temperature Sensors, Motion & Position Sensors, Others), Industry, Power Source, and Regional Analysis for 2026 - 2033

Battery-free Sensors Market Size and Trends Analysis

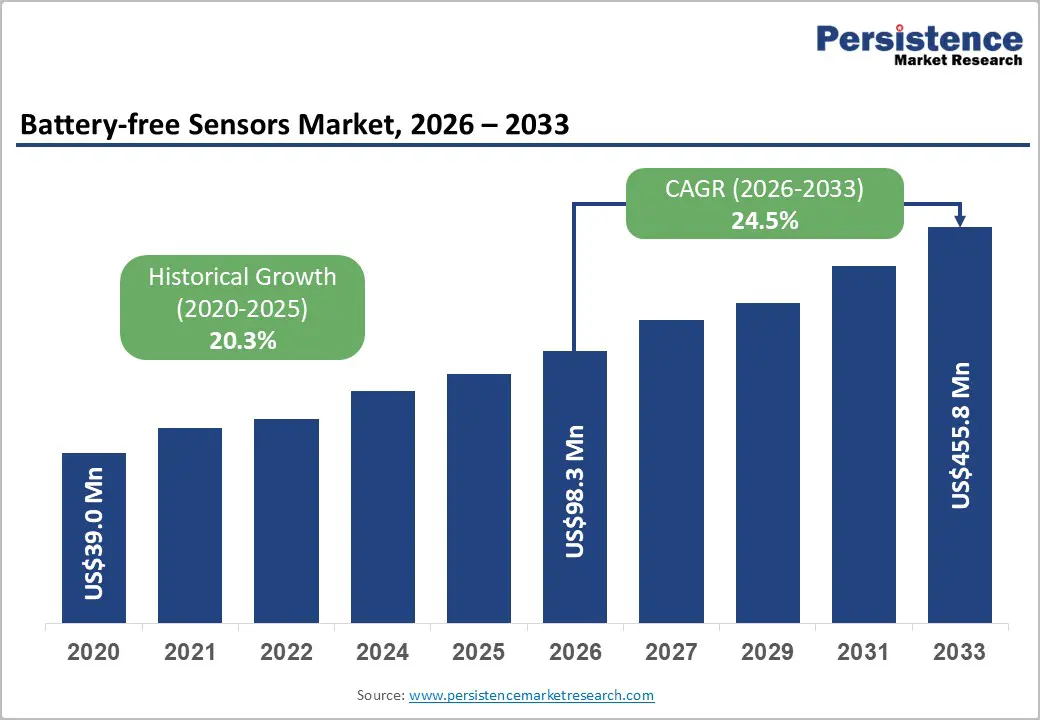

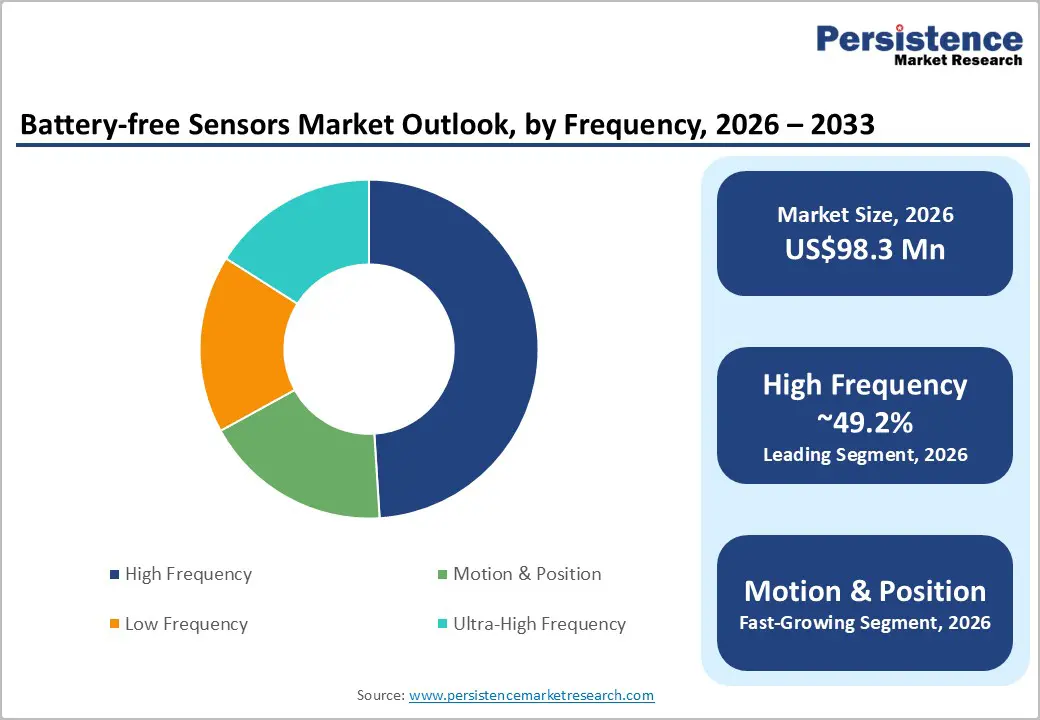

The global battery-free sensors market size is likely to be valued at US$98.3 million in 2026 and is expected to reach US$455.8 million by 2033, growing at a CAGR of 24.5% between 2026 and 2033, driven by rising industrial IoT adoption, demand for asset visibility, and the need to reduce maintenance costs.

Advances in energy harvesting and ultra-low-power connectivity, along with sustainability regulations, are accelerating adoption, especially in industrial monitoring, logistics, and smart buildings, where battery replacement is impractical.

Key Industry Highlights:

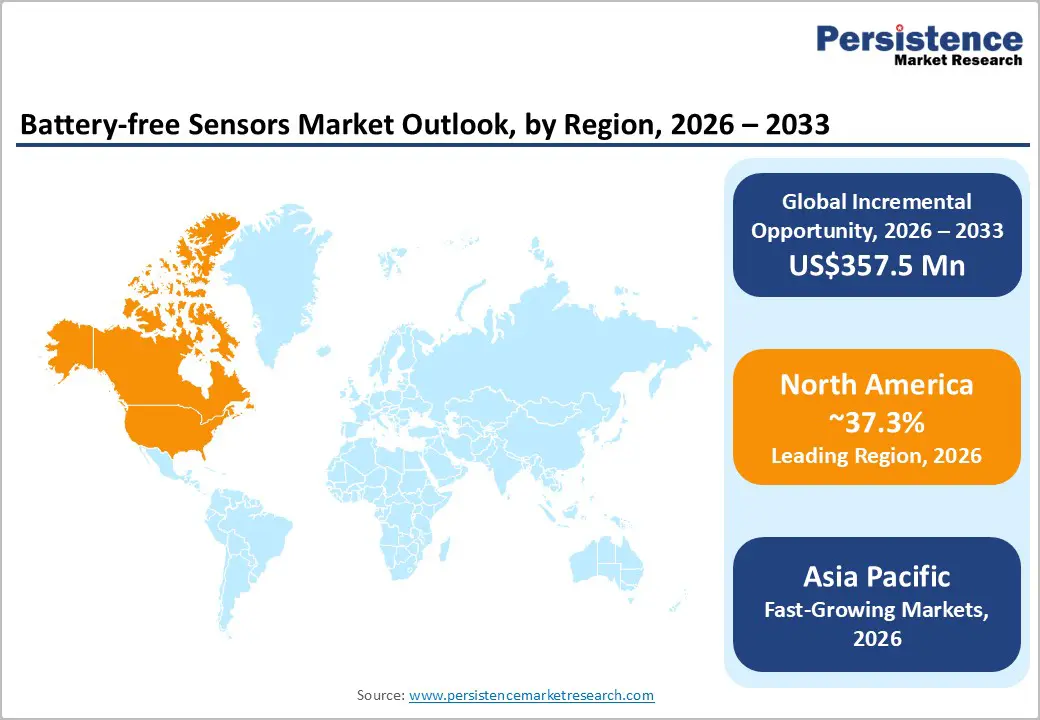

- Leading Region: North America is projected to account for over 37.3% of the market share in 2026, supported by strong industrial IoT adoption and early commercialization of energy-harvesting technologies.

- Fastest-growing Region: Asia Pacific is expected to be the fastest-growing region, driven by rapid industrialization, large-scale manufacturing, and increasing deployment of smart factory and logistics solutions.

- Investment Plans: Investment is increasingly focused on integrated, platform-based solutions combining sensing hardware, low-power connectivity, and analytics, with significant funding directed toward ambient IoT, smart logistics, and industrial automation deployments across North America, Europe, and the Asia Pacific.

- Dominant Frequency: High frequency is anticipated to dominate, accounting for approximately 49.2% of the market share, due to its reliability and suitability for RFID, NFC, and industrial communication applications.

- Leading Sensor Type: Temperature sensors are expected to lead, with around 35.8% market share, driven by strong demand across cold-chain logistics, healthcare, and industrial monitoring applications.

DRO Analysis

Driver - Industrial IoT Expansion and Predictive Maintenance Adoption are Accelerating Demand for Battery-Free Sensing Systems.

Industrial operators are increasingly deploying distributed sensor networks to monitor equipment health, environmental conditions, and asset movement in real time. Traditional battery-powered sensors introduce maintenance overhead, particularly in hard-to-access environments such as rotating machinery, remote infrastructure, and cold-chain logistics. Battery-free sensors eliminate this constraint by leveraging ambient energy sources, enabling continuous monitoring without manual intervention. This capability is particularly valuable in predictive maintenance, where uninterrupted data streams help reduce unplanned downtime and optimize asset performance.

As industries prioritize operational efficiency and cost optimization, battery-free sensing solutions are becoming economically viable, especially when the cost of downtime exceeds the cost of sensor deployment. This shift is transforming battery-free sensors from experimental technologies into practical infrastructure components across manufacturing, logistics, and energy sectors.

Sustainability Regulations and Circular Economy Policies are Strengthening the Adoption of Battery-Free Technologies

Regulatory frameworks focused on reducing electronic waste and improving product lifecycle transparency are influencing sensor design and deployment strategies. Policies promoting sustainable product design encourage the use of long-life, maintenance-free components that minimize material consumption and waste generation. Battery-free sensors align with these objectives by eliminating the need for disposable batteries, reducing environmental impact, and enabling longer operational lifespans.

In addition, emerging product traceability requirements are increasing the need for embedded sensing and identification technologies that can persist throughout a product’s lifecycle. As organizations align with sustainability goals and regulatory compliance requirements, battery-free sensors are evolving into critical enablers of traceability, operational transparency, and environmental responsibility. This regulatory alignment is expected to drive sustained market growth across multiple industries.

Restraint- Limited and Variable Energy Availability Remains a Key Technical and Commercial Constraint

Battery-free sensors rely on ambient energy sources such as radio frequency, light, vibration, or thermal gradients, all of which are inherently variable and environment-dependent. In conditions with insufficient energy availability, sensor performance may be constrained, limiting data transmission frequency, processing capability, or communication range. This introduces design complexity, as systems often require energy storage components, optimized duty cycles, and application-specific tuning to ensure reliability.

The challenge is particularly significant in use cases requiring continuous monitoring, high data throughput, or long-range communication. In such scenarios, conventional battery-powered or wired solutions may still offer more predictable performance and lower implementation risk. As a result, energy availability constraints continue to limit the scalability of battery-free sensors in certain high-demand applications.

Opportunity Analysis - Product Traceability and Digital Lifecycle Management are Creating New Growth Avenues

The increasing emphasis on product traceability and lifecycle transparency is expanding the addressable market for battery-free sensors. Industries such as textiles, electronics, logistics, and manufacturing are adopting digital tracking systems to monitor product origin, usage, and environmental conditions throughout the supply chain.

Battery-free sensors enable continuous data capture without maintenance, making them ideal for long-term deployment in products and packaging. This creates opportunities for replacing traditional tags and loggers with intelligent, self-powered sensing solutions. As global supply chains become more regulated and data-driven, the demand for embedded, maintenance-free sensing technologies is expected to grow significantly, supporting long-term market expansion.

Ambient IoT and Large-Scale Logistics Digitization Are Driving Commercial Adoption

The emergence of ambient IoT ecosystems is enabling large-scale deployment of battery-free sensors for item-level visibility and real-time monitoring. These systems leverage low-power wireless communication and energy harvesting to create networks of connected objects that operate without batteries. In logistics and supply chain environments, this capability supports continuous tracking of goods, environmental monitoring, and process automation.

The value proposition is particularly strong in high-volume operations where battery replacement is impractical. As companies invest in automation, digital twins, and real-time analytics, battery-free sensors are becoming integral to scalable IoT architectures. This trend is expected to unlock new business models, including data-driven services and subscription-based monitoring platforms.

Category-wise Analysis

Frequency Insights

High frequency is expected to be the leading segment, accounting for 49.2% of the market share in 2026. This dominance is driven by its suitability for industrial and logistics applications that require reliable, short- to medium-range communication with consistent data transmission. High-frequency systems are widely used in RFID- and NFC-based environments, where stable connectivity and predictable performance are critical.

For example, battery-free RFID sensor tags deployed in warehouse inventory systems enable real-time tracking of goods without requiring battery maintenance. Similarly, in smart factories, high-frequency sensors are used for machine condition monitoring and tool tracking, ensuring operational continuity. Their ability to deliver repeatable performance with low power consumption makes them the preferred choice for large-scale deployments. As organizations prioritize reliability and ease of integration, high-frequency architectures remain the foundation for many battery-free sensor implementations.

Motion and position sensing represents the fastest-growing application. Growth is driven by increasing demand for real-time tracking and automation in industries such as automotive, robotics, and logistics. For instance, battery-free motion sensors are being integrated into automated guided vehicles (AGVs) and robotic arms in manufacturing facilities to monitor movement and optimize workflows.

In automotive applications, these sensors support functions such as component alignment tracking and in-vehicle motion detection. Logistics companies are also deploying motion-enabled battery-free tags to monitor package handling and detect shocks or movement during transit. Advances in ultra-low-power semiconductors and wireless communication technologies are enabling more sophisticated sensor designs that support these use cases. As automation and digitalization accelerate, motion and position sensing are becoming a critical component of intelligent systems, driving rapid growth within the frequency segment.

Sensor Type Insights

Temperature sensors are anticipated to lead the market with a 35.8% market share in 2026. Temperature monitoring is a fundamental requirement across multiple industries, including healthcare, food and beverage, logistics, and industrial manufacturing. These applications often involve regulatory compliance and quality assurance, making temperature sensing a critical function. For example, battery-free temperature sensors are widely used in cold-chain logistics to monitor vaccine storage conditions and perishable food shipments, ensuring compliance with safety standards.

In industrial settings, these sensors are deployed on machinery to detect overheating and prevent equipment failure. Their ability to operate without batteries makes them ideal for sealed or hard-to-access environments. The combination of regulatory importance and broad applicability ensures that temperature sensors remain the dominant segment in the market.

Motion and position sensors are the fastest-growing segment, with anticipated growth driven by increasing adoption across automation and smart systems. This growth is supported by the rising deployment of robotics, autonomous systems, and connected devices that rely on real-time movement data. For instance, in smart warehouses, motion sensors track pallet movement and optimize storage operations, while in industrial automation, they enable predictive maintenance by detecting abnormal vibrations or positional deviations in machinery.

In consumer electronics and smart devices, battery-free motion sensors are being explored for gesture recognition and user interaction, eliminating the need for frequent maintenance. These sensors play a key role in enabling responsive systems that can trigger actions in response to movement or position changes. As industries move toward real-time decision-making and closed-loop automation, demand for motion and position sensing is expected to increase significantly.

Regional Insights

North America Battery-free Sensors Market Trends

North America is expected to lead the battery-free sensors market, accounting for over 37.3% of the market share in 2026, and is expected to grow at a CAGR of approximately 26.7%. The region’s leadership is driven by strong adoption of industrial IoT technologies, advanced manufacturing capabilities, and a robust innovation ecosystem. The U.S. plays a central role, supported by a high concentration of technology companies and early adopters of energy-harvesting solutions.

U.S. Battery-Free Sensors Market Trends

The U.S. plays a central role, supported by a high concentration of technology companies and early adopters of energy-harvesting solutions such as Powercast Corporation, Wiliot, and Energous Corporation. These companies are actively commercializing RF-powered and battery-free sensing platforms, particularly in logistics and infrastructure monitoring.

Key growth drivers include increasing demand for predictive maintenance, expansion of data centers, and widespread adoption of smart infrastructure. For example, Powercast’s deployment of battery-free RFID sensors in data centers has enabled continuous monitoring of equipment conditions without manual battery replacement, directly improving uptime and reducing maintenance costs.

Similarly, Wiliot’s ambient IoT platform is being adopted by major retailers and logistics operators in the U.S. to enable item-level tracking and real-time visibility across supply chains. The region benefits from a mature industrial base and a strong focus on operational efficiency, both of which support the deployment of battery-free sensors in high-value applications.

Investment activity is concentrated in platform-based solutions that integrate hardware, connectivity, and analytics. Companies such as Semtech Corporation are expanding low-power wide-area network ecosystems (LoRa) to support energy-efficient sensor deployments across industrial and smart city environments. These developments are accelerating commercialization and reducing barriers to adoption. As enterprises continue to prioritize automation and cost reduction, North America is expected to remain a leading market for innovation and early adoption.

Europe Battery-free Sensors Market Trends

Europe represents a policy-driven market where sustainability and regulatory compliance play a central role in adoption. Countries such as Germany, the United Kingdom, France, and Spain are leading the region’s growth, supported by strong industrial sectors and advanced research capabilities.

Germany Battery-free Sensors Market Trends

Germany is poised to lead the adoption of battery-free sensors, supported by its strong manufacturing ecosystem and ongoing Industry 4.0 initiatives. Companies like EnOcean GmbH are advancing energy-harvesting wireless sensors for use in smart buildings and industrial automation.

These sensors are increasingly integrated into building management systems for functions such as lighting control, HVAC optimization, and occupancy detection, eliminating the need for batteries while improving energy efficiency. In addition, Germany’s robust automotive industry is incorporating battery-free sensing solutions into production processes and vehicle systems, further strengthening its position in industrial applications.

U.K. Battery-free Sensors Market Trends

The U.K. is emerging as a key innovation hub, particularly in industrial monitoring and infrastructure applications. Inductosense has developed battery-free wireless sensors for monitoring corrosion and structural integrity in critical infrastructure such as pipelines and offshore platforms. These solutions enable long-term monitoring in harsh environments where battery replacement is impractical, supporting asset longevity and safety. The U.K.’s focus on infrastructure resilience and digitalization is driving demand for such advanced sensing technologies.

The region’s regulatory environment emphasizes circular economy principles, product traceability, and environmental sustainability. These factors are driving demand for battery-free sensors that can operate over long lifecycles without maintenance. As regulatory frameworks evolve, Europe is expected to see increased adoption across sectors requiring compliance and traceability, positioning it as a key policy-driven growth market.

Asia Pacific Battery-free Sensors Market Trends

Asia Pacific is the fastest-growing region, with a CAGR of 28.6%, driven by rapid industrialization, expanding manufacturing capabilities, and increasing adoption of digital technologies. Key markets include China, Japan, India, and Southeast Asian countries, each contributing to regional growth through large-scale industrial and logistics operations.

China Battery-free Sensors Market Trends

China plays a critical role as a manufacturing hub and a major adopter of industrial IoT technologies. The country is integrating battery-free sensors into smart factory environments to improve efficiency and reduce maintenance costs. Large-scale electronics manufacturing and logistics networks provide an ideal environment for deploying battery-free RFID and energy-harvesting sensors. Domestic and international semiconductor companies, including STMicroelectronics, are expanding their presence in China to support this demand, strengthening the regional supply chain.

Japan Battery-free Sensors Market Trends

Japan is a leader in advanced electronics and energy-efficient technologies. Companies such as EnOcean GmbH have partnered with Japanese firms to deploy battery-free sensors in smart buildings and energy management systems. For example, energy-harvesting sensors are being used in schools and commercial buildings to optimize energy consumption and reduce operational costs. Japan’s focus on sustainability and smart infrastructure is driving steady adoption of battery-free sensing technologies.

The region’s competitive advantage lies in its strong electronics manufacturing ecosystem and cost-effective production capabilities. Battery-free sensors are gaining traction in smart factories, logistics networks, and consumer IoT applications, where large-scale deployment is required. Government initiatives supporting digitalization, smart infrastructure, and energy efficiency are further accelerating adoption. As the region continues to modernize its infrastructure and supply chains, the Asia Pacific is expected to play a critical role in the global expansion of the battery-free sensors market.

Competitive Landscape

The global battery-free sensors market is fragmented, with a diverse mix of semiconductor manufacturers, energy-harvesting specialists, and IoT solution providers. Companies operate across different segments and applications, resulting in limited direct competition and low market concentration. Competitive positioning is based on technological innovation, application focus, and integration capabilities.

Key players are focusing on innovation, ecosystem partnerships, and vertical specialization. Strategies include developing ultra-low-power hardware, integrating sensing with analytics platforms, and targeting high-value applications where maintenance costs are high.

Key Industry Developments:

- In January 2026, Wiliot announced the launch of its Gen3 IoT Pixel, a next-generation battery-free sensor designed to enable continuous, real-time tracking of products and assets across supply chains. This development strengthens the shift toward ambient IoT by allowing large-scale, maintenance-free deployment of sensing at the item level, accelerating adoption in logistics and retail.

- In May 2025, Powercast Corporation announced its battery-free RFID sensor condition monitoring system, designed for industrial and infrastructure applications. The system enables continuous monitoring of temperature, humidity, and environmental conditions without maintenance, supporting predictive maintenance strategies and reducing operational downtime.

Companies Covered in Battery-free Sensors Market

- Infineon Technologies AG

- STMicroelectronics

- Texas Instruments

- Semtech Corporation

- Powercast Corporation

- Wiliot

- EnOcean GmbH

- Everactive

- Advantech Co., Ltd.

- Axzon

- Farsens

- ONiO

- Inductosense

- Energous Corporation

- Dracula Technologies

- Tageos

Frequently Asked Questions

The global battery-free sensors market is valued at US$98.3 million in 2026.

The battery-free sensors market is projected to reach US$455.8 million by 2033.

Key trends include the rapid adoption of industrial IoT and predictive maintenance, growing deployment of ambient IoT and smart logistics solutions, increasing use of energy-harvesting technologies (RF, vibration, solar), and rising emphasis on sustainability and battery elimination across industries.

The high-frequency segment leads the market with approximately 49.2% share, driven by its strong application in RFID, NFC, and industrial communication systems.

The battery-free sensors market is expected to grow at a CAGR of 24.5% from 2026 to 2033.

Major companies include STMicroelectronics, Infineon Technologies AG, Texas Instruments, Wiliot, and Powercast Corporation.